Ball Bearings Market Size to Reach USD 14.33 Billion by 2034 — Growth, Trends, and Competitive Analysis

Author:

Intellectual Market Insights Research

Published Date:

22 Jun 2026

Top 10 Ball Bearings Companies Driving Innovation in Global Industrial Machinery

The global Ball Bearings Market is rapidly solidifying its position as one of the most indispensable segments within the broader industrial machinery and precision engineering landscape. Ball bearings are mechanical components that reduce rotational friction between moving parts by using steel balls held in a cage between inner and outer bearing rings. This fundamental engineering solution underpins the efficient operation of machinery across virtually every industrial vertical from automotive drivetrains and aerospace actuation systems to robotics joints, wind turbine generators, and miniature medical devices.

As industrial automation accelerates, electric vehicle adoption surges, and precision manufacturing demands reach new heights, the ball bearings market is experiencing a structural uplift driven by the convergence of multiple high-growth end-use sectors. Manufacturers of ball bearings are responding by investing heavily in advanced materials science, IoT-enabled smart bearing technology, and sustainable lubrication solutions to meet the evolving performance requirements of next-generation machinery.

Advancements in ceramic bearing materials, self-lubricating polymer cages, and sensor-embedded smart bearing platforms are reshaping performance benchmarks across the industry. Numerous product development programs are underway targeting deep groove ball bearings, angular contact ball bearings, self-aligning ball bearings, and thrust ball bearings for specialized high-speed, high-load, and extreme-temperature applications.

Increasing investments from automotive OEMs, aerospace prime contractors, industrial machinery manufacturers, and renewable energy developers are supporting the development of next-generation bearing platforms. Strategic partnerships, licensing agreements, and global manufacturing expansions continue to reshape the competitive landscape.

As industrial systems increasingly prioritize energy efficiency, predictive maintenance capabilities, and extended service life, ball bearings are expected to play a crucial and expanding role across the full spectrum of mechanical systems. The market presents significant opportunities for manufacturers and innovators capable of delivering higher-precision, lower-friction, and longer-lasting bearing solutions.

Market Snapshot: Ball Bearings Market

The global Ball Bearings Market continues to expand as industrial manufacturers, automotive OEMs, aerospace companies, and renewable energy developers increasingly demand higher-performance and longer-life bearing solutions capable of supporting advanced machinery and automation systems.

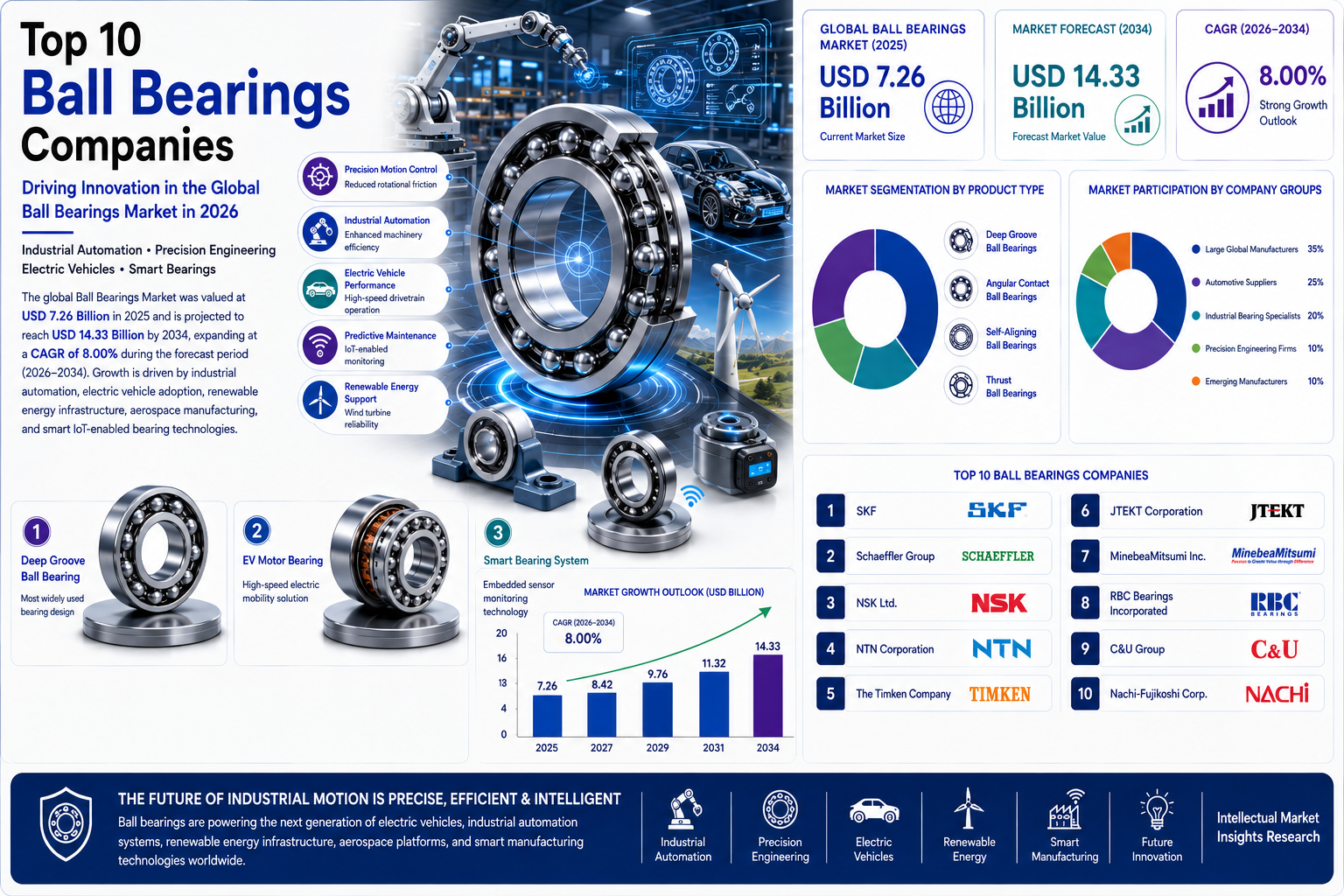

Current Market Size (2025): USD 7.26 Billion

Forecast Market Value (2034): USD 14.33 Billion

Expected CAGR (2026–2034): 8.00%

Growth momentum is being supported by increasing industrial automation adoption, surging electric vehicle production, expanding renewable energy infrastructure, rising aerospace manufacturing activity, and growing precision engineering demand worldwide.

Major Growth Drivers Include:

- Rising global demand for industrial automation and robotics across manufacturing sectors

- Surging electric vehicle production driving specialized bearing requirements for motors and drivetrains

- Expanding renewable energy infrastructure particularly wind turbines requiring high-load precision bearings

- Growth in aerospace and defense manufacturing demanding ultra-precision bearing solutions

- Increasing adoption of smart IoT-enabled bearings for predictive maintenance applications

- Rising infrastructure and construction activity globally boosting heavy machinery bearing demand

- Growing demand for miniature and micro-precision bearings in electronics and medical devices

- Rapid industrialization in Asia-Pacific fueling high-volume bearing consumption

Industries Generating the Strongest Demand Include:

- Automotive and Electric Vehicle Manufacturing

- Aerospace and Defense

- Industrial Machinery and Equipment

- Renewable Energy (Wind Turbines and Solar Tracking Systems)

- Robotics and Factory Automation

- Consumer Electronics and Appliances

- Medical Devices and Precision Instruments

- Railway and Transportation Infrastructure

Key Takeaways

- Ball bearings are becoming a critical enabler of next-generation electric vehicle drivetrains, industrial robots, and wind energy systems.

- Smart bearing technology with embedded IoT sensors is transforming predictive maintenance across heavy industrial applications.

- Combination of electrification and automation megatrends is creating dual demand uplift across automotive and industrial sectors simultaneously.

- Asia-Pacific remains the dominant regional market, accounting for over 45% of global ball bearings revenue in 2025, led by China, Japan, South Korea, and India.

- Emerging manufacturers in China and India are driving competitive intensity, compelling established players to accelerate innovation in premium and specialty bearing segments.

Featured Snippet

What is driving the Ball Bearings Market?

The Ball Bearings Market is being driven by rising industrial automation and robotics adoption, surging electric vehicle production creating specialized bearing demand, expanding renewable energy infrastructure requiring high-load precision bearings, growing aerospace manufacturing activity, and increasing deployment of IoT-enabled smart bearings for predictive maintenance. Automotive OEMs, industrial machinery manufacturers, and renewable energy developers are increasingly requiring advanced bearing solutions that deliver improved performance, longer service life, and reduced operational downtime, creating strong and diversified demand for ball bearing technologies worldwide.

The 2026 Buyer Playbook: What Really Drives Purchase Decisions

Purchase decisions in the ball bearings market have evolved significantly as end-users across automotive, aerospace, industrial machinery, and renewable energy sectors demand more from their bearing suppliers than ever before.

Industrial OEMs, maintenance procurement teams, and engineering design departments increasingly evaluate ball bearing technologies based on performance specifications, total cost of ownership, supply chain reliability, and product traceability rather than unit price alone.

Functional Benefits

Engineering performance remains the top purchase priority.

Procurement teams and design engineers increasingly evaluate:

- Load-carrying capacity and dynamic load rating specifications

- Operational speed ratings and high-speed performance characteristics

- Friction reduction efficiency and energy consumption impact

- Service life and fatigue resistance under cyclical loading

- Temperature resistance and environmental sealing performance

- Compatibility with automation and smart factory control systems

The most successful ball bearing manufacturers position their products around measurable engineering performance improvements and total lifecycle cost reductions.

Pricing Psychology

Procurement decision-makers increasingly focus on total cost of ownership rather than unit bearing price alone.

Organizations evaluate:

- Extended bearing service life reducing replacement frequency and downtime costs

- Energy efficiency gains from reduced friction lowering operating costs

- Predictive maintenance capability reducing unplanned failure costs

- Warranty terms and failure rate guarantees

- Global spare parts availability and replacement lead times

- Total lifecycle cost across installation, operation, and replacement phases

Advanced bearing solutions that demonstrate superior service life and operational efficiency can command significant pricing premiums while still delivering positive total cost of ownership outcomes for industrial customers.

Trust Factors

Trust plays a critical role in ball bearing supplier selection, particularly for demanding aerospace, automotive, and industrial applications where bearing failure can result in costly downtime or safety incidents.

Industrial procurement teams prefer suppliers with:

- Demonstrated track record across demanding application environments

- ISO, ABEC, and application-specific quality certification portfolios

- Strong failure analysis and technical application engineering support

- Traceable manufacturing processes and material certification documentation

- Established distribution and aftermarket service networks

- Peer-reviewed technical publications and application case studies

Strong engineering credibility and quality certification portfolios significantly influence supplier selection and long-term supply agreements in the ball bearings market.

Convenience

Industrial organizations increasingly prioritize supply chain reliability and procurement convenience when selecting ball bearing partners.

Preferred suppliers offer:

- Reliable global manufacturing capacity and inventory availability

- Consistent product quality across high-volume supply agreements

- Technical application engineering and design support services

- Rapid delivery capabilities for maintenance and emergency replacement orders

- Digital catalog access and e-commerce procurement channels

- Comprehensive global distribution and aftermarket service networks

Comprehensive supply chain support and technical service capabilities improve adoption rates and strengthen long-term customer relationships in the ball bearings market.

Brand Perception

Leading ball bearing manufacturers are often associated with:

- Precision engineering excellence and manufacturing quality leadership

- Materials science innovation and advanced metallurgy capabilities

- Strong application-specific engineering expertise across key verticals

- Reliable global supply chain and aftermarket service capabilities

- Sustainability and environmental responsibility commitments

- Proven commercialization track record across automotive, aerospace, and industrial sectors

Strong brand perception based on engineering excellence and supply reliability creates durable competitive advantages and supports premium pricing throughout the product lifecycle.

Investment Opportunities in the Ball Bearings Market

Investors continue identifying significant growth opportunities across multiple segments of the ball bearings market:

- Smart IoT-enabled bearing platforms for predictive maintenance applications

- Specialty bearings for electric vehicle motor and drivetrain applications

- High-performance wind turbine main shaft and gearbox bearing solutions

- Ultra-precision miniature bearings for medical devices and robotics

- Ceramic and hybrid bearing materials for extreme temperature and corrosive environments

- Aerospace-grade bearing solutions for next-generation aircraft platforms

- Emerging market manufacturing expansion across India and Southeast Asia

- Advanced bearing lubrication and sealing technology innovation

- Digital bearing monitoring and condition intelligence software platforms

- Sustainable and biodegradable lubrication technology development

As industrial automation, electric mobility, and renewable energy infrastructure continue expanding, investment activity across the ball bearings sector is expected to accelerate throughout the forecast period.

Top 10 Ball Bearings Companies Driving Market Growth

1. SKF

2. Schaeffler Group

3. NSK Ltd.

4. NTN Corporation

5. The Timken Company

6. JTEKT Corporation

7. MinebeaMitsumi Inc.

8. RBC Bearings Incorporated

9. C&U Group

10. Nachi-Fujikoshi Corp

1. SKF

Overview

SKF is one of the world's foremost manufacturers of ball bearings and rotating equipment technology, headquartered in Gothenburg, Sweden. The company holds a globally recognized position as a precision engineering leader, offering a comprehensive portfolio of ball bearings, roller bearings, seals, lubrication systems, and condition monitoring solutions across a vast range of industrial, automotive, aerospace, and energy applications. SKF's deep groove ball bearings are among the most widely specified bearing solutions globally, used in applications spanning electric motors, automotive transmissions, machine tools, and consumer appliances. The company's engineering heritage spanning more than a century and its global manufacturing footprint across more than 100 facilities in 30 countries underpin its market leadership position.

Recent Moves

- Expanded smart bearing and sensor-integrated product portfolio for industrial IoT applications.

- Increased investment in electric vehicle-specific bearing solutions for motors and wheel hubs.

- Accelerated development of sustainable lubrication and energy-efficient bearing platforms.

- Strengthened digital service and predictive maintenance technology offerings.

Competitive Edge

SKF benefits from a globally recognized engineering brand, an unmatched breadth of bearing product portfolio, extensive application engineering expertise across every major industrial vertical, and a well-established global distribution and aftermarket service network. Its integrated approach combining bearings with seals, lubrication, and condition monitoring creates a comprehensive mechanical system solution that is difficult for narrower competitors to replicate.

Future Outlook

SKF is expected to continue expanding its smart bearing and electric vehicle bearing portfolios while leveraging its digital service capabilities to build recurring condition monitoring revenue streams. Growing demand for energy-efficient and longer-life bearing solutions across industrial and automotive sectors is likely to further strengthen SKF's market position through 2034.

2. Schaeffler Group

Overview

Schaeffler Group is a German precision engineering conglomerate and one of the world's largest manufacturers of rolling bearings, linear guidance systems, and direct drive technology. Operating through its INA, FAG, and LuK brands, Schaeffler serves automotive OEMs, industrial machinery manufacturers, aerospace companies, and renewable energy developers across more than 50 countries. The company's FAG brand is particularly renowned for its high-precision ball bearings used in demanding applications including machine tool spindles, electric motor drives, and aerospace systems. Schaeffler's deep integration into the global automotive supply chain including significant EV platform partnerships and its growing industrial automation bearing portfolio position it as one of the most strategically positioned bearing manufacturers in the current market cycle.

Recent Moves

- Expanded EV-specific bearing and mechatronic product portfolio for electric drivetrain applications.

- Increased investment in smart bearing technology integrating IoT sensor capabilities.

- Advanced high-precision angular contact ball bearing development for machine tool markets.

- Strengthened strategic partnerships with major automotive OEM electric vehicle platforms.

Competitive Edge

Schaeffler benefits from dual-brand strength across both the INA and FAG product families, deep integration into major automotive OEM supply chains globally, advanced manufacturing capabilities in precision rolling element bearings, and substantial R&D investment supporting continuous product innovation. Its growing mechatronics portfolio combining bearings with actuators and sensors creates additional differentiation beyond traditional bearing supply.

Future Outlook

Schaeffler is expected to continue strengthening its position in the electric vehicle bearing segment while expanding its industrial automation and renewable energy bearing portfolios. The company's investment in smart bearing technology and integrated mechatronic systems is expected to open new revenue streams as industrial and automotive customers increasingly demand intelligent mechanical components.

3. NSK Ltd.

Overview

NSK Ltd. is a Japanese precision equipment manufacturer and one of the world's leading producers of ball bearings, linear motion systems, and automotive components. Headquartered in Tokyo, NSK serves a global customer base spanning automotive, industrial machinery, aerospace, medical equipment, and precision instrument applications. The company is particularly known for its high-precision deep groove ball bearings and angular contact ball bearings, which are widely specified in machine tools, electric motors, and automotive applications. NSK's strong engineering culture and significant R&D investment have established the company as an innovation leader in bearing tribology, advanced materials, and precision manufacturing technology.

Recent Moves

- Expanded high-speed precision ball bearing portfolio for machine tool and EV motor applications.

- Increased investment in self-lubricating and maintenance-free bearing development.

- Advanced ultra-clean bearing solutions for semiconductor manufacturing equipment.

- Strengthened global manufacturing capabilities to support growing demand in Asia-Pacific.

Competitive Edge

NSK benefits from a long-established reputation for bearing precision and reliability, strong customer relationships across the machine tool and automotive sectors, significant technical expertise in bearing tribology and advanced lubrication, and a well-developed global distribution network. Its specialized expertise in ultra-clean and ultra-high-speed bearing applications for semiconductor equipment creates differentiated positions in high-value market niches.

Future Outlook

NSK is expected to continue expanding its precision bearing portfolio with particular focus on electric vehicle motor bearings, semiconductor equipment bearings, and high-speed machine tool applications. Growing industrial automation adoption across Asia-Pacific is likely to drive significant volume growth in the company's industrial bearing portfolio through the forecast period.

4. NTN Corporation

Overview

Recent Moves

Competitive Edge

Future Outlook

5. The Timken Company

Overview

Recent Moves

Competitive Edge

Future Outlook

Market Drivers

Several factors are contributing to the growth of the global Ball Bearings Market:

- Rising global industrial automation and robotics adoption accelerating precision bearing demand.

- Surging electric vehicle production requiring specialized high-speed, low-friction bearing solutions.

- Expanding renewable energy infrastructure particularly wind turbines demanding high-load precision bearings.

- Growth in aerospace and defense manufacturing requiring ultra-precision bearing solutions.

- Increasing adoption of IoT-enabled smart bearings for predictive maintenance across industrial sectors.

- Rising construction and mining activity globally boosting heavy machinery bearing consumption.

- Growing demand for miniature precision bearings in medical devices, consumer electronics, and robotics.

- Expanding aftermarket and replacement bearing demand driven by aging industrial equipment fleets.

Current Growth Trends

Electric Vehicle Bearing Specialization

Automotive OEMs and their Tier 1 suppliers are increasingly requiring specialized ball bearing solutions designed for electric motors, regenerative braking systems, and high-voltage drivetrain components, creating a fast-growing premium bearing application segment within the broader automotive market.

Smart Bearing Technology Adoption

Ball bearing manufacturers are embedding IoT sensors, vibration monitoring capabilities, and condition intelligence platforms into their products, enabling real-time bearing health monitoring and predictive maintenance applications that reduce unplanned industrial downtime and extend equipment service life.

Ceramic and Hybrid Bearing Material Innovation

Advanced ceramic and hybrid bearing materials combining steel rings with ceramic rolling elements are gaining adoption in high-speed, high-temperature, and corrosion-sensitive applications, offering superior performance in demanding environments compared to all-steel bearing solutions.

Sustainable Lubrication Development

Bearing manufacturers are investing in biodegradable and long-life lubrication technologies, self-lubricating polymer cage materials, and maintenance-free bearing designs that reduce environmental impact and lower total lifecycle operating costs for industrial customers.

Expansion into Emerging Industrial Verticals

Ball bearing demand is expanding beyond traditional automotive and general industrial applications into renewable energy, semiconductor manufacturing equipment, medical robotics, and food processing diversifying the end-market base and creating new specialty bearing segments with premium pricing potential.

Segmentation Analysis

By Product Type

Deep Groove Ball Bearings

This segment dominates the global ball bearings market due to its exceptional versatility across a wide range of applications and load directions. Deep groove ball bearings are the most widely used bearing type globally, employed in electric motors, automotive applications, consumer appliances, and general industrial machinery due to their low friction, high-speed capability, and low maintenance requirements.

Angular Contact Ball Bearings

Growing adoption of angular contact ball bearings is driven by increasing demand in machine tool spindles, gearboxes, and high-precision automotive applications where combined axial and radial load handling is required. This segment is experiencing accelerated demand from the machine tool and electric vehicle drivetrain sectors.

Self-Aligning Ball Bearings

This segment is projected to exhibit the highest CAGR among all bearing types, driven by increasing industrial automation adoption where shaft misalignment conditions must be accommodated. Self-aligning ball bearings are particularly valued in conveyor systems, agricultural equipment, and heavy industrial machinery.

Thrust Ball Bearings

Demand for thrust ball bearings is growing in automotive steering systems, vertical pump applications, and machine tool rotary tables, driven by increasing automotive production volumes and expanding industrial machinery investment globally.

By Application

Automotive

The largest application segment, driven by ongoing global vehicle production volumes, the transition to electric vehicles requiring specialized bearing solutions, and growing demand for precision bearings in ADAS sensor actuators and advanced transmission systems.

Industrial Machinery

Growing factory automation investment, expanding robotics deployment, and increasing heavy machinery production globally continue supporting strong bearing demand across industrial machinery applications.

Aerospace and Defense

Ultra-precision bearing demand in aircraft engines, landing gear systems, and defense equipment represents a high-value application segment expected to grow steadily with expanding aerospace production and defense spending worldwide.

Electronics and Medical Devices

The medical application segment is expected to grow at the highest CAGR during the forecast period, driven by increasing demand for ultra-precision miniature bearings in surgical robots, medical imaging systems, and diagnostic equipment.

Renewable Energy

Expanding wind turbine installation globally is creating significant demand for high-load, long-life ball and roller bearings capable of operating reliably in harsh outdoor environments across multi-decade turbine service lifetimes.

By End User

Automotive OEMs and Tier 1 Suppliers

The largest end-user segment, requiring high-volume, precision-specification ball bearings across engine, transmission, wheel hub, and drivetrain applications, with growing demand for specialized EV-specific bearing solutions.

Industrial Machinery Manufacturers

Machinery OEMs are significant bearing consumers, integrating precision ball bearings into machine tools, conveyors, pumps, compressors, and industrial robots during original equipment manufacturing.

Aftermarket and Maintenance Organizations

The replacement and aftermarket bearing segment provides stable, recurring revenue for bearing manufacturers, driven by the large global installed base of industrial equipment and vehicles requiring periodic bearing replacement.

Aerospace and Defense Prime Contractors

High-value, low-volume precision bearing demand from aerospace primes and defense manufacturers represents a premium market segment with rigorous qualification requirements and strong pricing discipline.

Regional Analysis

Asia-Pacific

Asia-Pacific dominates the global Ball Bearings Market, accounting for over 45% of global revenue in 2025, driven by robust automotive manufacturing in China, Japan, South Korea, and India, rapid industrial automation adoption, and the region's vast industrial machinery manufacturing base. China is the world's largest bearing production and consumption market, with domestic manufacturers like C&U Group competing alongside global majors. Japan hosts several world-class precision bearing manufacturers including NSK, NTN, JTEKT, MinebeaMitsumi, and Nachi-Fujikoshi, collectively making it the world's most sophisticated precision bearing engineering ecosystem. India is emerging as a fast-growing bearing market supported by expanding automotive manufacturing and government-backed infrastructure investment.

North America

North America is a significant and technology-sophisticated ball bearings market, driven by automotive OEM manufacturing concentrated in the U.S. Midwest, strong aerospace and defense procurement, expanding industrial automation investment, and growing renewable energy infrastructure. The U.S. CHIPS Act-related semiconductor manufacturing expansion is also creating incremental demand for ultra-precision miniature bearings used in semiconductor fabrication equipment. Leading players including Timken and RBC Bearings maintain strong domestic manufacturing capabilities serving both domestic demand and export markets.

Europe

Europe maintains a strong ball bearings market anchored by premium automotive manufacturing in Germany, France, and Italy, a sophisticated aerospace industry centered in France and the UK, and continued industrial machinery investment across Germany and Scandinavia. SKF from Sweden and Schaeffler Group from Germany represent two of the world's most technically advanced bearing manufacturers, maintaining strong engineering innovation and premium product positioning across the global market. The region's accelerating EV transition is creating growing demand for specialized bearing solutions in electric drivetrain applications.

Latin America

Latin America represents a developing ball bearings market, with Brazil and Mexico serving as the primary consumption centers driven by automotive manufacturing, mining equipment, and agricultural machinery applications. Market growth is supported by gradual industrial modernization, expanding automotive assembly operations, and growing infrastructure investment, though the region's market development pace remains slower than Asia-Pacific and North America.

Middle East and Africa

The Middle East and Africa represent an early-stage but developing ball bearings market, with demand driven by oil and gas equipment, construction machinery, and expanding infrastructure projects. The Gulf region's ongoing industrial diversification initiatives and growing manufacturing investment are creating incremental bearing demand, while South Africa serves as the primary African consumption center for industrial and mining equipment bearings.

Competitive Landscape

The global Ball Bearings Market is moderately concentrated at the premium end and highly competitive in the standard bearing segments, with leading companies focusing on:

- Smart bearing and IoT sensor technology integration for predictive maintenance differentiation

- Electric vehicle-specific bearing portfolio development targeting the fastest-growing automotive application segment

- Advanced materials innovation in ceramic, hybrid, and polymer bearing components

- Strategic acquisitions expanding product range and distribution reach

- Sustainable lubrication and energy-efficient bearing design investment

- Aftermarket service and condition monitoring platform development

- Global manufacturing capacity expansion in high-growth emerging markets

- Application engineering investment deepening customer technical relationships

Competition is expected to intensify as Asian manufacturers continue upgrading quality systems and targeting premium segments, while established global leaders accelerate innovation in smart bearing technology and specialty application segments to maintain their competitive positions.

Investment Opportunities

Significant opportunities exist across several high-growth areas within the Ball Bearings Market:

- Smart IoT-enabled bearing platforms and condition monitoring software

- Electric vehicle motor and drivetrain specialty bearing solutions

- Wind turbine main shaft and gearbox high-load precision bearings

- Ultra-precision miniature bearings for medical robotics and semiconductor equipment

- Ceramic and hybrid bearing materials for extreme operating environment applications

- Aerospace-grade ball bearing solutions for next-generation aircraft platforms

- Emerging market bearing manufacturing expansion across India and Southeast Asia

- Sustainable and energy-efficient bearing lubrication technology

- Aftermarket bearing distribution platform and e-commerce channel development

- Advanced bearing design simulation and digital twin engineering software

SWOT Analysis

Strengths

- Universal mechanical necessity across virtually all rotating machinery applications.

- Well-established global manufacturing and distribution ecosystems.

- Strong alignment with high-growth end markets including EVs, robotics, and renewable energy.

- High switching costs in precision and specialty application segments protecting incumbent suppliers.

Weaknesses

- Commodity pricing pressure in standard bearing segments from low-cost Asian manufacturers.

- Significant capital intensity of precision bearing manufacturing facilities.

- Raw material cost exposure to steel, chrome, and specialty alloy price volatility.

Opportunities

- Expansion into smart bearing and IoT-integrated condition monitoring product categories.

- Growth of electric vehicle-specific bearing requirements creating new premium segments.

- Increasing demand for sustainable and energy-efficient bearing solutions globally.

- Emerging market industrialization in South and Southeast Asia creating new high-volume demand.

Threats

- Intensifying competition from Chinese manufacturers upgrading into premium bearing segments.

- Raw material supply chain disruptions affecting steel and specialty alloy availability.

- Potential market share erosion from magnetic levitation and air bearing technology in select applications.

- Trade tariff and geopolitical risks affecting global bearing supply chains.

Frequently Asked Questions (FAQs)

What are ball bearings?

Ball bearings are mechanical components that reduce rotational friction between moving parts by using steel balls held in a cage between inner and outer bearing rings, enabling smooth, low-friction rotation in machinery across virtually all industrial applications.

What is driving the Ball Bearings Market?

Rising industrial automation and robotics adoption, surging electric vehicle production, expanding renewable energy infrastructure, growing aerospace manufacturing activity, and increasing deployment of IoT-enabled smart bearings for predictive maintenance are the primary growth drivers.

Which region dominates the market?

Asia-Pacific currently dominates the global Ball Bearings Market with over 45% of global revenue in 2025, led by China, Japan, South Korea, and India.

What is the forecast market value?

The global Ball Bearings Market is projected to reach USD 14.33 billion by 2034, growing at a CAGR of 8.00% from 2026 to 2034.

What are the major application segments?

Automotive, industrial machinery, aerospace and defense, consumer electronics, renewable energy, medical devices, and railway and transportation infrastructure are the major application segments.

Why are ball bearings important?

Ball bearings are essential mechanical components that enable efficient rotation in machinery by reducing friction, extending equipment service life, reducing energy consumption, and enabling the high-speed precision operation required by modern industrial, automotive, and aerospace systems.

What opportunities exist for investors?

Smart IoT-enabled bearings for predictive maintenance, electric vehicle drivetrain bearing solutions, renewable energy bearing applications, ultra-precision miniature bearings for medical and semiconductor applications, and emerging market manufacturing expansion offer significant investment opportunities.

What challenges does the industry face?

Commodity pricing pressure from low-cost Asian manufacturers, raw material cost volatility, capital intensity of precision manufacturing facilities, and intensifying competition in standard bearing segments are the key challenges facing the global ball bearings industry.

Which companies lead the market?

SKF, Schaeffler Group, NSK Ltd., NTN Corporation, The Timken Company, JTEKT Corporation, MinebeaMitsumi Inc., RBC Bearings Incorporated, C&U Group, and Nachi-Fujikoshi Corp are among the leading global companies in the ball bearings market.

What trends will shape future growth?

Smart IoT-enabled bearing technology, electric vehicle drivetrain specialization, ceramic and hybrid bearing material innovation, sustainable lubrication development, and expansion into medical robotics and semiconductor equipment applications will shape future growth in the global ball bearings market.

Conclusion

The global Ball Bearings Market is positioned for sustained and accelerating growth as industrial systems worldwide undergo a fundamental transformation driven by electrification, automation, and the pursuit of energy efficiency. The ability of precision ball bearings to enable efficient, high-speed, low-friction rotation in machinery across virtually every industrial vertical makes them a foundational technology that underpins the entire global manufacturing and energy ecosystem.

Growing adoption of electric vehicles, rapid expansion of industrial automation and robotics, increasing renewable energy infrastructure investment, and the emergence of smart bearing technology with IoT-integrated condition monitoring are collectively creating a more valuable and more differentiated market than the commodity bearing industry of a decade ago. Manufacturers that successfully integrate intelligence, sustainability, and application-specific engineering expertise into their bearing solutions will be best positioned to capture the premium growth opportunities emerging within this expanding market.

Organizations capable of delivering clinically validated engineering performance, extended service life, IoT-enabled predictive maintenance capabilities, and specialized solutions for electric vehicles and renewable energy applications will be best positioned to capitalize on the significant opportunities emerging within this rapidly evolving and strategically important market.