Insulin Companies Market Analysis on Novo Nordisk, Sanofi, Eli Lilly, Biocon & Tonghua Dongbao

Author:

Intellectual Market Insights Research

Published Date:

22 May 2026

Insulin Market, 537 Million Diabetics, 3 Manufacturers: The Economics Behind Insulin's Oligopoly

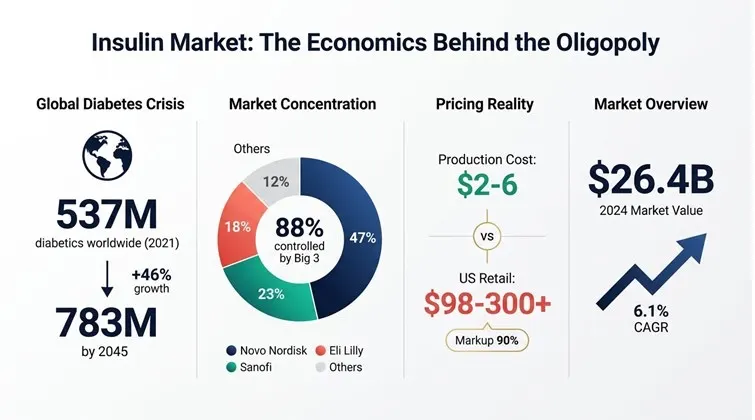

In 2024, the global insulin market was valued at USD 26.4 billion and is one of the most critical segments in pharmaceutical healthcare. The market is expecting a steady but constant growth of 6.1% during the forecast period 2034. The market's growth is directly correlates with diabetes prevalence statistics. According to the International Diabetes Federation (IDF), in 2021, 537 million adults worldwide were living with diabetes, with projections indicating this number will surge to 783 million by 2045 representing a 46% increase over 24 years. The 1.6% annual growth in the diabetic population, creating sustained demand pressure on insulin supply chains.

Regional Demand Patterns

- Asia-Pacific Region: The fastest-growing demand market, owing to China and India, majorly driven by urbanization, dietary transitions, and massive population bases

- North America: Holds approximately 35% of global revenue despite smaller patient volumes, due to premium pricing of analog insulins

- Europe: Represents 27% of global insulin revenue along with the strong biosimilar adoption

- Low and Middle-Income Countries (LMICs): Account for over 75% of global diabetes cases but face severe access constraints

Supply Side: Manufacturer Concentration

The insulin market is oligopoly, however, posses a huge opportunity for the emerging companies

|

Manufacturer |

Country |

Market Share |

Key Products |

|

Novo Nordisk |

Denmark |

~47% |

NovoLog, Lantus biosimilars |

|

Sanofi |

France |

~23% |

Lantus, Toujeo |

|

Eli Lilly |

USA |

~18% |

Humalog, Trulicity |

|

Big 3 Total |

- |

~88-90% |

- |

|

Biocon Biologics |

India |

~3-4% |

Biosimilar insulins |

|

Tonghua Dongbao |

China |

~2-3% |

Regional supply |

|

Other Regional Players |

Various |

~5-7% |

Local markets |

This oligopolistic structure creates significant barriers to entry due to:

- High capital requirements for biomanufacturing facilities

- Complex regulatory approval processes taking 5-8 years

- Specialized cold-chain distribution infrastructure requirements

- Established relationships with healthcare systems and payers

Emerging Competition:

The biosimilar insulin segment is gradually challenging this concentration. The global biosimilar insulin market valued at USD 1.9 billion in 2025 and growing at approximately 8.9% CAGR. Key developments include Biocon-Viatris's Semglee becoming the first interchangeable biosimilar insulin approved in the US (2021), and Civica Rx launching biosimilar insulin glargine at USD 30 per vial in 2024.

Production & Manufacturing Landscape

Major manufacturing hubs include Denmark, France, Germany (European production), United States (domestic supply), and emerging centers in China, India, Brazil, and Mexico serving both domestic and export markets.

Supply Chain Complexity & Vulnerabilities

Insulin's protein structure necessitates strict temperature control throughout the entire supply chain. Products must be maintained between 2°C and 8°C from manufacturing to patient delivery. This requirement creates several critical vulnerabilities:

- Cold Chain Failures: Approximately 25-30% of insulin is wasted in some developing regions due to inadequate refrigeration infrastructure

- Distribution Costs: Cold chain logistics can represent 15-20% of final product cost

- Geographic Limitations: Remote areas often lack reliable cold storage, limiting patient access

Pricing Dynamics:

Insulin pricing demonstrates extreme geographic variation:

- Manufacturing Cost: USD 2-6 per vial across all insulin types

- US Retail Pricing: USD 98 (human insulin) to USD 300+ (premium analogs) before insurance

- Developing Market Pricing: USD 3-10 per vial in markets like India and Bangladesh

- Recent US Reforms: Inflation Reduction Act (2022) Medicare cap of USD 35 per month, with major manufacturers voluntarily extending similar caps

Market Trends & Future Outlook: Biosimilar Market Expansion

The biosimilar insulin segment represents the most significant near-term market disruption, with projections indicating 15-20% market capture by 2028. Key drivers include patent expiration of major analog insulins and increasing payer pressure for cost containment.

Emerging trends include:

- Smart Insulin Delivery: Integration with continuous glucose monitors (CGM) growing at ~12% CAGR

- Digital Health Platforms: AI-driven dosing optimization and remote patient monitoring

- Alternative Delivery Methods: Inhaled insulin (Afrezza) and ongoing oral insulin development

Key Market Statistics Summary

- Global Market Size: USD 25-28 billion (2023-2024)

- Projected Growth: 5.8-6.2% CAGR through 2030

- Global Diabetes Population: 537 million (2021) → 783 million (2045)

- Insulin-Dependent Patients: 70-80 million globally

- Market Concentration: Big 3 manufacturers control ~88-90%

- Access Gap: Only ~50% of those needing insulin have reliable access

- Cold Chain Waste: 25-30% in developing regions

- Biosimilar Growth: 8-9% CAGR, targeting 15-20% market share by 2028

- US Patient Population: 8.4 million insulin users

- Regional Revenue Distribution: North America 35%, Europe 25-28%, Asia-Pacific fastest growing