Top 15 Leading Companies in the Global Anti-Drone Market

Author:

Intellectual Market Insights Research

Published Date:

06 Jul 2026

Introduction

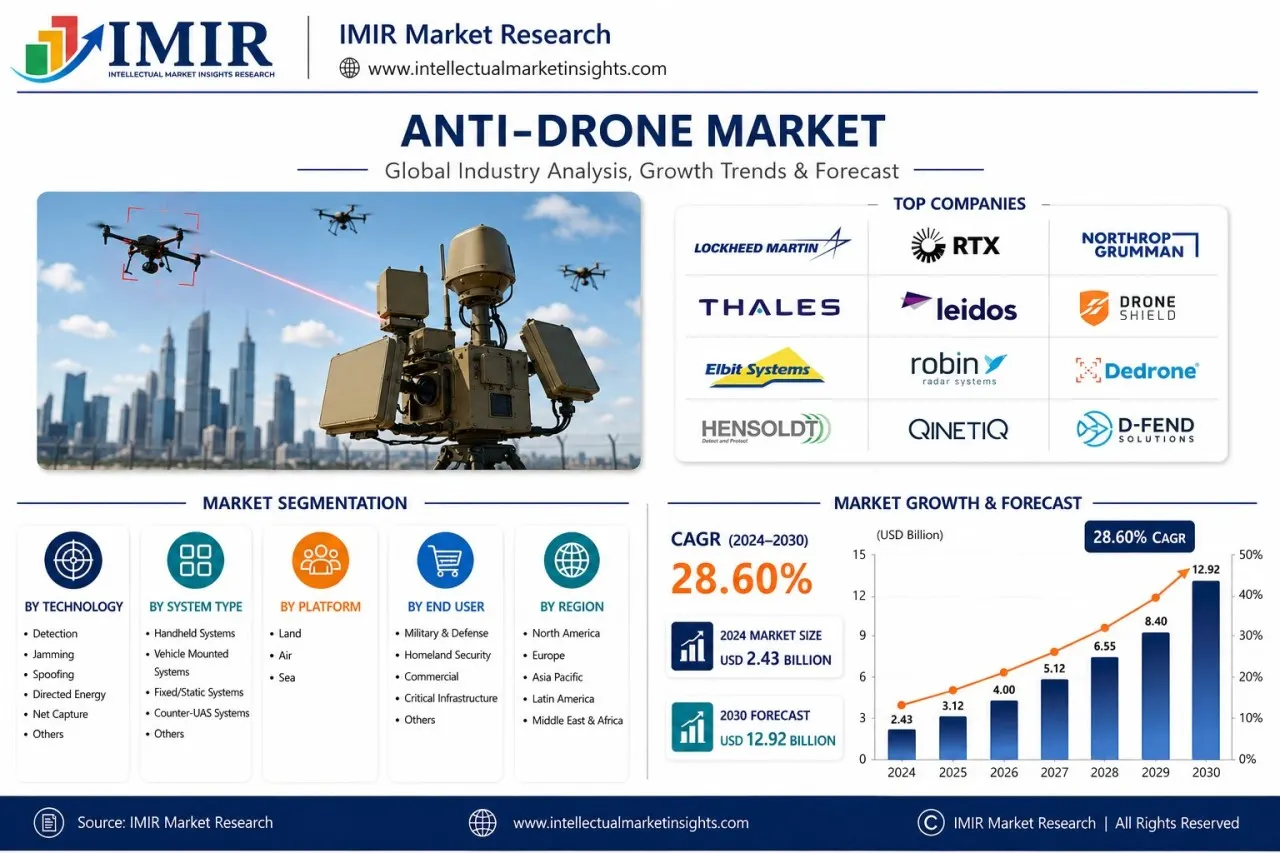

Drones stopped being a novelty threat years ago. Airports have closed runways over unauthorized sightings, militaries have watched cheap commercial quadcopters get strapped with explosives, and critical infrastructure operators now treat low-altitude airspace as an active attack surface. That shift in perception is what's fueling the anti-drone (counter-UAS) market's growth: estimates place the market anywhere from roughly USD 3.1–4.5 billion in 2025, climbing toward USD 14.5–19.8 billion by 2030–2033, depending on the research house and methodology used. Whatever the exact figure, the direction is the same — sustained annual growth in the mid-20% range, among the fastest-growing segments of the broader defense and homeland security industry.

For a full breakdown of market sizing, segmentation, and forecasts, see Intellectual Market Insights' Anti-Drone Market Size and Trends report, which underpins much of the sizing referenced here.

The technology landscape is diversifying quickly. Early counter-drone systems relied almost entirely on RF jamming and basic radar. Today's systems combine radar, radio-frequency detection, electro-optical/infrared sensors, and acoustic sensors into fused, AI-assisted detection stacks — then pair that detection layer with a widening menu of neutralization options: kinetic interceptors, high-energy lasers, high-powered microwave weapons, and net-capture drones. This layered, "detect-then-defeat" architecture is becoming the industry standard because no single sensor or effector handles every threat profile, from slow-moving hobbyist drones to coordinated swarm attacks.

Demand is being pulled from multiple directions at once. Defense ministries are modernizing air-defense doctrine around drone swarms and loitering munitions, a shift accelerated by lessons from the Russia-Ukraine conflict. Airports and border agencies are procuring detection systems to comply with tightening aviation-security regulations. Large public events — from the Olympics to G7 summits — now routinely deploy temporary counter-drone perimeters. And energy, oil & gas, and prison operators are beginning to treat drone intrusion as a standard part of physical security planning, not an edge case.

Looking ahead, the biggest opportunities sit at the intersection of cost and scale. Traditional interceptor missiles cost tens to hundreds of thousands of dollars per shot — uneconomical against drones that cost a few hundred dollars to build. That cost asymmetry is pushing investment toward directed-energy weapons and software-defined jamming, where the marginal cost per intercept drops close to zero. Companies that can pair affordable neutralization with AI-driven detection and open, modular architectures are positioned to capture disproportionate share as government procurement scales up through the rest of the decade.

Growth Drivers

Rising drone incursions and asymmetric threats. The conversion of low-cost commercial drones into surveillance or strike tools has made counter-UAS a frontline defense priority rather than a niche capability. Modern conflicts have repeatedly shown cheap quadcopters neutralizing far more expensive conventional assets, which is reshaping military procurement priorities worldwide.

Defense modernization and government initiatives. NATO members, the U.S. Department of Defense, and Asia-Pacific militaries (China, India, Japan, South Korea) are all funding dedicated counter-UAS programs. The U.S. Replicator initiative and similar efforts are accelerating investment in AI-driven autonomous interceptors.

AI and automation adoption. AI-enabled threat classification, automated tracking, and sensor fusion are reducing false-alarm rates and response times — a critical improvement given how fast small drones can approach a target.

Investment and funding momentum. Venture and government funding into specialist counter-drone firms has surged; companies like Epirus and DroneShield have both posted major funding or revenue jumps in the past two years, signaling investor confidence in the segment's long-term trajectory.

Consumer and commercial drone proliferation. As commercial drone adoption expands across delivery, agriculture, and inspection use cases, the addressable population of both legitimate and rogue UAVs grows in parallel — expanding demand for detection and de-confliction technology even in non-military settings.

Top 20 Leading Companies in the Global Anti-Drone Market

- RTX Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Thales Group

- Leonardo S.p.A.

- Saab AB

- Israel Aerospace Industries

- Rafael Advanced Defense Systems

- Elbit Systems Ltd.

- Dedrone

- DroneShield Limited

- Anduril Industries

- CACI International Inc.

- SRC, Inc.

- QinetiQ Group plc

- Hensoldt AG

- Rohde & Schwarz

- CerbAir

- BlueHalo

- Fortem Technologies

1. RTX Corporation

Headquarters: Arlington, Virginia, USA

Founded: 2023 (formed through the merger of Raytheon Technologies and Raytheon Company businesses)

RTX Corporation is one of the world's leading aerospace and defense companies, offering advanced counter-unmanned aerial system (C-UAS) technologies for military, homeland security, and critical infrastructure protection. Through its defense business, the company develops integrated radar systems, electronic warfare solutions, command-and-control software, and precision interceptors capable of detecting, tracking, identifying, and neutralizing hostile drones.

RTX's anti-drone portfolio combines multi-layered defense technologies, making it a preferred supplier for armed forces worldwide.

Why RTX Leads the Anti-Drone Industry

- Advanced radar and electronic warfare capabilities.

- Integrated kinetic and non-kinetic counter-drone systems.

- Strong global defense customer base.

- Continuous investment in AI-enabled battlefield technologies.

- Proven military deployment experience.

Company Snapshot

|

Attribute |

Details |

|---|---|

|

Company |

RTX Corporation |

|

Founded |

2023 |

|

Headquarters |

Arlington, Virginia, USA |

|

Industry |

Aerospace & Defense |

|

Core Products |

Radar Systems, Electronic Warfare, Missile Defense, Counter-UAS |

|

Key Markets |

Defense, Homeland Security, Airports |

|

Competitive Advantage |

Integrated multi-layer drone defense |

|

Growth Drivers |

Military modernization, border security, drone threats |

|

Why It Stands Out |

Comprehensive layered C-UAS solutions |

2. Lockheed Martin Corporation

Headquarters: Bethesda, Maryland, USA

Founded: 1995

Lockheed Martin is among the world's largest defense contractors and a major innovator in counter-drone technologies. The company develops advanced surveillance radars, AI-powered command systems, directed-energy weapons, and electronic warfare platforms designed to defend military bases and strategic infrastructure against UAV threats.

Its integrated air defense capabilities make it a key player in modern C-UAS programs.

Why Lockheed Martin Leads

- Directed-energy weapon expertise.

- Advanced integrated air defense systems.

- Strong U.S. Department of Defense partnerships.

- AI-enabled target identification.

- Large-scale defense manufacturing capabilities.

Company Snapshot

|

Attribute |

Details |

|---|---|

|

Company |

Lockheed Martin Corporation |

|

Founded |

1995 |

|

Headquarters |

Bethesda, Maryland, USA |

|

Industry |

Aerospace & Defense |

|

Core Products |

Lasers, Radar, Missile Defense, Counter-UAS |

|

Key Markets |

Military, Government |

|

Competitive Advantage |

Advanced air defense integration |

|

Growth Drivers |

Defense spending, autonomous warfare |

|

Why It Stands Out |

High-energy laser counter-drone technologies |

3. Northrop Grumman Corporation

Headquarters: Falls Church, Virginia, USA

Founded: 1994

Northrop Grumman develops sophisticated anti-drone systems using advanced radar, artificial intelligence, electronic warfare, and integrated command platforms. The company specializes in protecting military installations and critical infrastructure from increasingly complex drone threats.

Its solutions emphasize early detection, rapid tracking, and automated threat neutralization.

Why Northrop Grumman Leads

- AI-powered surveillance systems.

- Cutting-edge electronic warfare.

- Integrated air defense expertise.

- Strong military contracts.

- Continuous R&D investment.

Company Snapshot

|

Attribute |

Details |

|---|---|

|

Company |

Northrop Grumman Corporation |

|

Founded |

1994 |

|

Headquarters |

Falls Church, Virginia, USA |

|

Industry |

Aerospace & Defense |

|

Core Products |

Radar, Sensors, Electronic Warfare, Counter-UAS |

|

Key Markets |

Defense, Government |

|

Competitive Advantage |

AI-enabled threat detection |

|

Growth Drivers |

Rising drone attacks, defense modernization |

|

Why It Stands Out |

Advanced battlefield surveillance capabilities |

4. Thales Group

Headquarters: Paris, France

Founded: 2000

Thales Group offers integrated anti-drone systems that combine radar, electro-optical sensors, radio-frequency detection, AI analytics, and electronic jamming technologies. The company's C-UAS platforms protect airports, military installations, and critical infrastructure across Europe and other global markets.

Why Thales Leads

- AI-assisted drone detection.

- Multi-sensor surveillance systems.

- Strong European defense presence.

- Advanced electronic countermeasures.

- Integrated command-and-control platforms.

Company Snapshot

|

Attribute |

Details |

|---|---|

|

Company |

Thales Group |

|

Founded |

2000 |

|

Headquarters |

Paris, France |

|

Industry |

Defense & Security |

|

Core Products |

Radar, RF Detection, Electronic Warfare |

|

Key Markets |

Defense, Airports, Critical Infrastructure |

|

Competitive Advantage |

Multi-sensor integrated systems |

|

Growth Drivers |

Airport security, military upgrades |

|

Why It Stands Out |

Highly scalable C-UAS architecture |

5. Leonardo S.p.A.

Headquarters: Rome, Italy

Founded: 1948

Leonardo develops comprehensive anti-drone solutions integrating radar surveillance, electro-optical tracking, AI analytics, RF sensors, and electronic countermeasures. The company serves military organizations, airports, government agencies, and critical infrastructure operators worldwide.

Why Leonardo Leads

- Strong radar expertise.

- Advanced AI-based target classification.

- European defense leadership.

- Integrated electronic warfare.

- Global military presence.

Company Snapshot

|

Attribute |

Details |

|---|---|

|

Company |

Leonardo S.p.A. |

|

Founded |

1948 |

|

Headquarters |

Rome, Italy |

|

Industry |

Aerospace & Defense |

|

Core Products |

Counter-UAS Systems, Radar, Electronic Warfare |

|

Key Markets |

Defense, Government |

|

Competitive Advantage |

Integrated surveillance technologies |

|

Growth Drivers |

NATO modernization, airport security |

|

Why It Stands Out |

Proven European counter-drone systems |

6. Saab AB

Headquarters: Stockholm, Sweden

Founded: 1937

Saab develops advanced air surveillance radars and integrated counter-UAS solutions designed to detect, identify, and neutralize unauthorized drones across military and civilian environments.

7. Israel Aerospace Industries

Headquarters: Lod, Israel

Founded: 1953

Israel Aerospace Industries (IAI) is globally recognized for developing sophisticated drone defense technologies, including radar systems, electronic warfare, AI-enabled surveillance, and integrated counter-UAS platforms used by defense organizations worldwide.

8. Rafael Advanced Defense Systems

Headquarters: Haifa, Israel

Founded: 1948

Rafael provides advanced anti-drone technologies including the Drone Dome system, integrating radar, RF sensors, electro-optics, electronic jamming, and laser interception technologies.

9. Elbit Systems Ltd.

Headquarters: Haifa, Israel

Founded: 1966

Elbit Systems develops comprehensive C-UAS solutions for military, border security, and critical infrastructure protection using AI, electronic warfare, and sensor fusion.

10. Dedrone

Headquarters: Sterling, Virginia, USA

Founded: 2014

Dedrone specializes exclusively in AI-powered drone detection, tracking, identification, and mitigation software. Its solutions are widely deployed across airports, stadiums, prisons, utilities, and government facilities.

11. DroneShield Limited

Headquarters: Sydney, Australia

Founded: 2014

DroneShield develops AI-powered drone detection systems, RF sensors, electronic jammers, handheld counter-drone devices, and command-and-control software for military and commercial customers.

12. Anduril Industries

Headquarters: Costa Mesa, California, USA

Founded: 2017

Anduril Industries combines autonomous AI software, sensor fusion, autonomous towers, and electronic warfare technologies to provide next-generation counter-drone defense systems.

13. CACI International Inc.

Headquarters: Reston, Virginia, USA

Founded: 1962

CACI develops advanced electronic warfare and RF-based counter-UAS technologies capable of detecting and defeating drone threats in complex operational environments.

14. SRC, Inc.

Headquarters: Syracuse, New York, USA

Founded: 1957

SRC designs advanced radar-based drone detection systems, electronic warfare technologies, and integrated air surveillance solutions for military and homeland security applications.

15. QinetiQ Group plc

Headquarters: Farnborough, England, UK

Founded: 2001

QinetiQ offers integrated counter-drone systems combining radar, RF detection, electro-optical sensors, AI software, and electronic countermeasures.

16. Hensoldt AG

Headquarters: Taufkirchen, Germany

Founded: 2017

Hensoldt specializes in sensor technologies, surveillance radars, and integrated counter-UAS systems designed for military and critical infrastructure protection.

17. Rohde & Schwarz

Headquarters: Munich, Germany

Founded: 1933

Rohde & Schwarz develops RF monitoring, spectrum analysis, drone detection, and electronic countermeasure solutions used by governments and security agencies worldwide.

18. CerbAir

Headquarters: Montrouge, France

Founded: 2015

CerbAir provides AI-enabled drone detection, RF analysis, GNSS protection, and anti-drone systems for airports, prisons, defense organizations, and critical infrastructure.

19. BlueHalo

Headquarters: Arlington, Virginia, USA

Founded: 2019

BlueHalo develops directed-energy weapons, RF countermeasures, AI-enabled surveillance, and integrated C-UAS technologies for military and government customers.

20. Fortem Technologies

Headquarters: Pleasant Grove, Utah, USA

Founded: 2016

Fortem Technologies specializes in autonomous drone defense solutions featuring TrueView radar, AI-powered tracking software, and DroneHunter interceptor drones designed to safely capture hostile UAVs.

Segment Analysis

- By System Type. Hybrid systems — combining radar, RF, electro-optical, and jamming into one architecture — currently hold the largest share, since no single sensor type reliably handles the full range of drone sizes, speeds, and materials. Directed-energy (laser) systems are the fastest-growing segment as costs fall and reliability improves, offering near-zero marginal cost per intercept.

- By Platform. Ground-based systems dominate due to ease of deployment and maintenance for protecting fixed assets like airports and military bases. UAV-based counter-drone platforms — drones designed to intercept other drones — are growing at a solid clip as swarm-defense doctrine matures.

- By Application. Detection and disruption applications lead the market, since end-to-end threat management (identify, track, then neutralize) is what most government and critical-infrastructure buyers actually need, rather than detection alone.

- By End Use. Government and defense remains the largest end-use category, expected to hold roughly a third of the market, driven by rising defense budgets. Commercial and public-event security (large gatherings, summits, airports) is the fastest-growing end-use segment as the technology becomes more affordable and portable.

- By Range. Short and medium-range systems dominate current deployments, protecting localized assets like border checkpoints and event perimeters, while long-range systems are more concentrated in military and national-airspace-defense applications.

Regional Analysis

- North America. The largest regional market, holding roughly 30% of global share, driven by high U.S. defense spending, TSA-reported drone sightings near airports, and rapid adoption of layered counter-UAS architectures across military and homeland security agencies.

- Europe. Growth here is closely tied to NATO's air-defense posture following the Russia-Ukraine conflict, plus European Defense Fund-backed programs pushing sovereign capability through firms like Thales, Rheinmetall, and Saab, reducing reliance on U.S. technology.

- Asia-Pacific. Projected to post the fastest regional CAGR, driven by China's military modernization, and matching investments from India, Japan, South Korea, and Australia. India in particular has scaled indigenous procurement (e.g., Bharat Electronics Limited-linked programs) alongside border-security deployments.

- Latin America. A smaller but emerging market, with growth concentrated around critical infrastructure protection (energy, oil & gas) and select national border-security initiatives.

- Middle East & Africa. Demand is shaped by high-profile regional conflicts and the need to protect energy infrastructure; Israeli and Gulf-state procurement of counter-drone systems (including Israeli-developed platforms deployed for allied nations) is a notable driver.

Frequently Asked Questions

1. What is the anti-drone (counter-UAS) market? It's the industry building systems to detect, track, and neutralize unauthorized drones, spanning radar, RF detection, jamming, directed-energy weapons, and interceptor drones.

2. How big is the global anti-drone market? Estimates vary by research firm, generally placing 2025 market value between roughly USD 3.1 billion and USD 4.5 billion, with most forecasts projecting growth to somewhere between USD 14.5 billion and USD 19.8 billion by 2030–2033.

3. Who are the top companies in the anti-drone market? Leading players include RTX (Raytheon), Lockheed Martin, Northrop Grumman, Thales, Leonardo, Saab, Israel Aerospace Industries, Rheinmetall, Anduril Industries, Rafael, DroneShield, Dedrone, Epirus, Blighter, and ParaZero.

4. Which region leads the anti-drone market? North America currently holds the largest share, roughly 30%, due to high defense spending and airport/homeland-security investment. Asia-Pacific is generally forecast to grow fastest.

5. What technologies are used in anti-drone systems? Radar, RF detection, electro-optical/infrared sensors, acoustic sensors, RF jamming, directed-energy (laser and microwave) weapons, and kinetic interceptor drones — usually fused together rather than deployed individually.

6. Why are directed-energy weapons gaining popularity in counter-drone defense? Because their marginal cost per intercept is far lower than traditional missile-based systems, which can cost USD 100,000–500,000 per shot against drones that cost only hundreds of dollars to build.

7. How is AI changing the anti-drone industry? AI improves threat classification accuracy, reduces false alarms, and enables faster automated response — critical given the limited reaction time small, fast-moving drones allow.

8. What industries use anti-drone technology? Military and defense, airports, border security agencies, critical infrastructure (energy, oil & gas), correctional facilities, and large public-event security operations.

9. What is the difference between counter-UAS and anti-drone systems? The terms are largely used interchangeably in industry reporting, though "counter-UAS" is more common in formal defense and government procurement contexts.

10. Which company is the largest player in the anti-drone market by revenue? Among specialists profiled here, RTX (Raytheon) reports the highest total company revenue, though it's worth noting these are diversified defense conglomerates where counter-drone is one business line among many, not standalone segment revenue.

11. Are venture-backed startups competing with traditional defense contractors? Yes — companies like Anduril, Epirus, DroneShield, and ParaZero have grown quickly by focusing specifically on software-defined and specialist counter-drone technology, in some cases out-innovating larger, slower-moving primes.

12. What regulatory challenges affect the anti-drone industry? Export controls (ITAR/EAR) on electronic warfare technology, aviation-safety regulations, and spectrum-licensing rules all constrain how quickly counter-drone systems can be sold and deployed internationally.

Conclusion

The anti-drone market's growth story is less about any single breakthrough technology and more about a structural shift in how governments and infrastructure operators think about low-altitude airspace. What used to be an open, largely unmonitored layer of sky is now treated as contested territory that requires active defense — a shift accelerated by real-world conflicts, high-profile airport disruptions, and the sheer affordability of commercial drones as improvised weapons.

The competitive landscape reflects that shift clearly. Traditional defense primes — RTX, Lockheed Martin, Northrop Grumman, Thales, Leonardo, Saab — bring scale, existing government relationships, and deep radar and missile-defense expertise that newer entrants can't easily replicate. But the fastest-growing companies in this list (DroneShield, Anduril, Epirus) are the ones betting on software-defined, AI-first, and directed-energy approaches that sidestep the cost economics that make traditional missile interceptors impractical against cheap drones. That tension — legacy scale versus specialist agility — will likely define competitive dynamics through the rest of the decade.

Regionally, expect North America to remain the largest market on the back of sustained U.S. defense and homeland-security spending, while Asia-Pacific's growth rate outpaces it as China, India, Japan, and South Korea all scale indigenous and imported counter-drone capability in response to regional tensions. Europe's trajectory will hinge heavily on how quickly NATO members translate Ukraine-conflict lessons into procurement budgets, and how successfully firms like Thales, Rheinmetall, and Saab can build sovereign European capability that reduces reliance on U.S. suppliers.

Looking further out, the innovation roadmap points toward three converging trends: AI-driven sensor fusion becoming table stakes rather than a differentiator, directed-energy weapons moving from experimental to mainstream as reliability improves and costs fall, and software-defined, subscription-based business models (following DroneShield's SentryCiv approach) potentially reshaping how counter-drone technology gets sold and priced. For investors and procurement teams alike, the companies best positioned for the next five years are likely those that can combine defense-grade reliability with the iteration speed of a software company — a combination that, historically, few traditional defense contractors have managed well, but that several of the newer entrants profiled here are explicitly built around.