Top 20 Companies in the Global Hyperscale Data Center Market Driving Industry Growth

Author:

Intellectual Market Insights Research

Published Date:

22 Jun 2026

Top 20 Companies in the Global Hyperscale Data Center Market Driving Industry Growth in 2026

Introduction:

In an era defined by cloud computing, artificial intelligence, and real-time digital services, hyperscale data centers have emerged as the foundational pillars of the global technology economy. These massive, purpose-built facilities are not merely storage warehouses for data — they are the beating heart of the internet, powering everything from streaming services and financial transactions to AI model training and enterprise cloud applications.

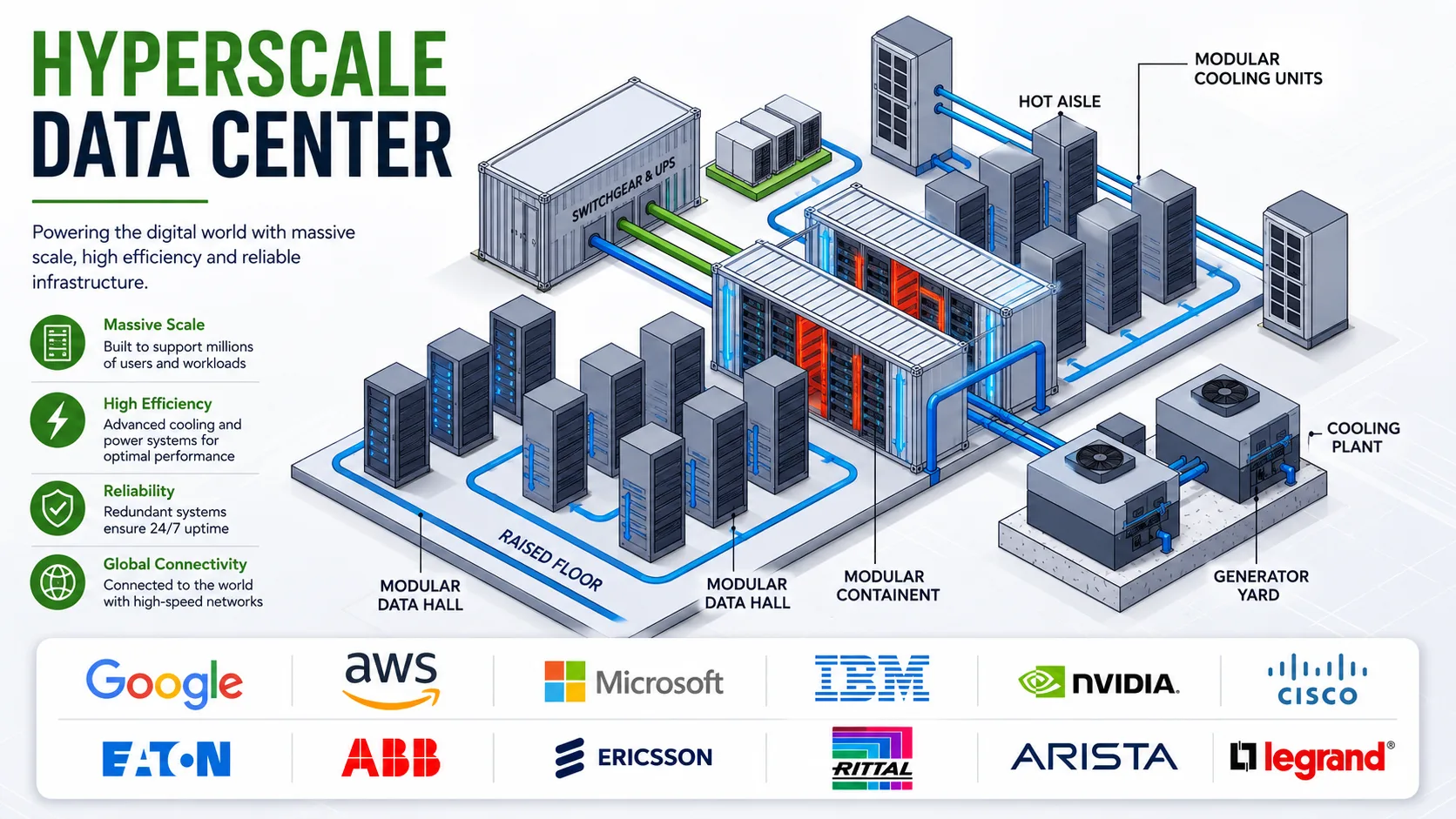

A hyperscale data center is distinguished by its extraordinary scale: typically housing a minimum of 5,000 servers and spanning at least 10,000 square feet. More importantly, these facilities are designed with a single-architecture compute model that dynamically scales in response to fluctuating workloads. This elasticity — the ability to expand and contract seamlessly — is what makes hyperscale infrastructure indispensable to cloud providers, colocation operators, and large enterprises navigating the demands of the modern digital landscape.

According to market research from Intellectual Market Insights Research (IMI-001580), the global hyperscale data center market was valued at USD 62 billion in 2021 and is forecast to reach an extraordinary USD 596 billion by 2031, expanding at a compound annual growth rate (CAGR) of 28.52%. This staggering trajectory makes it one of the fastest-growing sectors in the entire technology industry.

Several converging forces are propelling this growth. The explosive adoption of public cloud services by enterprises across every sector is creating insatiable demand for compute capacity. The rise of AI and machine learning — particularly large language models and generative AI — requires massive GPU clusters that only hyperscale environments can economically host. Simultaneously, the global rollout of 5G networks is enabling edge computing use cases that depend on distributed hyperscale infrastructure for low-latency data processing.

From a business perspective, hyperscale data centers also address a critical corporate imperative: cost efficiency. By centralizing IT infrastructure in optimized, high-density facilities, organizations achieve significant reductions in both capital expenditure (CAPEX) and operational expenditure (OPEX). The economies of scale inherent to hyperscale operations translate directly to lower cost-per-workload, making them the preferred infrastructure model for organizations of all sizes.

This article profiles the top 20 companies leading the global hyperscale data center market in 2026, examining their competitive strategies, key service offerings, recent developments, and the strategic advantages that cement their market positions. We also analyze market segmentation, regional dynamics, emerging trends, and the future outlook through 2031 — providing investors, technology leaders, and industry analysts with a comprehensive, authoritative perspective on one of the most consequential markets of our time.

Market Overview:

The hyperscale data center market encompasses a wide spectrum of solutions (servers, storage, networking, software) and services (consulting, installation, maintenance) deployed across cloud providers, colocation operators, and enterprises of all sizes. The table below provides a consolidated snapshot of the market's key parameters.

|

Parameter |

Detail |

|---|---|

|

Market Value (2021) |

USD 62 Billion |

|

Market Value (2031, Forecast) |

USD 596 Billion |

|

CAGR (2023–2031) |

28.52% |

|

Base Year |

2022 |

|

Forecast Period |

2023–2031 |

|

Leading End-User Segment |

Cloud Providers |

|

Leading Component Segment |

Solutions (Server, Storage, Networking) |

|

Leading Industry Segment |

IT & Telecom |

|

Dominant Region |

North America |

|

Fastest-Growing Region |

Asia-Pacific |

|

Key Growth Driver |

Cloud Computing & AI Workloads |

|

Major Market Restraint |

High Infrastructural Overhead Costs |

|

Emerging Opportunity |

Edge Computing & Hybrid Cloud |

|

Market Concentration |

High — dominated by global tech majors |

Market Segmentation at a Glance

|

Segment |

Sub-Segments |

|---|---|

|

By Component |

Solutions (Server, Storage, Networking, Software) | Services (Consulting, Installation & Deployment, Maintenance & Support) |

|

By End-User |

Cloud Providers | Colocation Providers | Enterprises |

|

By Enterprise Size |

Large Enterprises | SMEs |

|

By Industry |

BFSI | IT & Telecom | Government | Energy & Utilities | Others |

|

By Region |

North America | Europe | Asia-Pacific | Latin America | Middle East & Africa |

Why the Hyperscale Data Center Market Is Experiencing Explosive Growth

The 28.52% CAGR registered by this market is not coincidental — it reflects a perfect storm of technological, economic, and societal forces that are fundamentally reshaping how the world manages, processes, and stores data.

1. Unstoppable Cloud Migration

Enterprise migration to cloud platforms has accelerated dramatically post-pandemic. Organizations across BFSI, healthcare, retail, and manufacturing are decommissioning legacy on-premise infrastructure in favor of cloud-based models. This migration directly fuels demand for hyperscale capacity, as cloud providers must continuously expand their infrastructure footprints to accommodate surging workloads. Cloud providers — the largest end-user segment — require hyperscale environments capable of delivering Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), and Software-as-a-Service (SaaS) at global scale.

2. The AI & Machine Learning Revolution

The training and inference requirements of modern AI models — particularly large language models (LLMs) and generative AI systems — are unprecedented in computing history. A single LLM training run can consume thousands of NVIDIA GPUs for weeks. Only hyperscale infrastructure provides the density, power capacity, and cooling efficiency required to support such workloads economically. Investment in AI infrastructure by companies like Microsoft (backing OpenAI), Google (Gemini), and Meta is directly translating into hyperscale construction booms globally.

3. IoT and Data Volume Explosion

The proliferation of connected devices — forecast to exceed 75 billion globally by 2025 — generates data volumes that traditional data centers cannot handle. Hyperscale facilities, with their elastic scaling architectures, are uniquely positioned to ingest, process, and store the torrent of IoT data emanating from smart cities, autonomous vehicles, industrial sensors, and consumer devices.

4. 5G Network Deployment

Global 5G rollout is enabling latency-sensitive applications — autonomous driving, AR/VR, real-time gaming, remote surgery — that demand compute resources positioned close to the network edge. This is driving hyperscale operators to develop distributed data center architectures, combining centralized hyperscale campuses with geographically distributed edge nodes.

5. Cost Reduction Imperatives

With CAPEX and OPEX reduction a board-level priority for most large enterprises, the economic case for hyperscale colocation — versus building and operating private data centers — has never been stronger. Colocation in a hyperscale facility provides access to enterprise-grade power, cooling, connectivity, and security infrastructure without the massive upfront capital commitment of self-build.

6. Sustainability & Energy Efficiency Mandates

Hyperscale operators are investing billions in renewable energy, advanced cooling (liquid immersion, direct-to-chip), and Power Usage Effectiveness (PUE) optimization. These initiatives not only reduce environmental impact but also lower long-term operating costs — a compelling value proposition as corporate ESG commitments intensify globally.

Top 20 Companies in the Global Hyperscale Data Center Market (2026)

Based on the IMIR market research report and corroborating industry intelligence, the following companies represent the most influential players shaping the competitive landscape of the global hyperscale data center market. Each profile examines headquarters, founding year, industry focus, global presence, key offerings, market position, recent developments, and strategic advantages.

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud Platform (GCP)

- Equinix, Inc.

- Meta Platforms (Facebook)

- NVIDIA Corporation

- Cisco Systems, Inc.

- Intel Corporation

- IBM (International Business Machines)

- Alibaba Cloud (Aliyun)

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Arista Networks

- Apple Inc.

- Baidu, Inc.

- NTT Communications

- Western Digital Corporation

- Ericsson

- QTS Realty Trust (Blackstone)

- Mellanox Technologies (NVIDIA)

01. Amazon Web Services (AWS)

Headquarters: Seattle, WA, USA

Founded: 2006

Parent: Amazon.com, Inc.

Global Market Share: ~31%

Regions: 33+ globally (99+ Availability Zones)

Industry Focus: Cloud Computing, AI, Enterprise IT

Company Overview: Amazon Web Services is the world's largest and most comprehensive cloud platform, offering over 200 fully featured services from data centers globally. As the pioneer of cloud infrastructure, AWS has set the benchmark for hyperscale data center design, operations, and service delivery. Its infrastructure spans 33 geographic regions across North America, Europe, Asia-Pacific, the Middle East, Africa, and Latin America.

Key Products & Services: AWS offers a complete hyperscale ecosystem including EC2 (compute), S3 (storage), RDS and DynamoDB (databases), SageMaker (AI/ML), CloudFront (CDN), and a sprawling portfolio of security, analytics, and developer tools. AWS Outposts extends hyperscale infrastructure to on-premises environments, enabling true hybrid cloud deployments.

Strategic Advantages: AWS's first-mover advantage, global footprint, deepest service catalog, and unmatched ecosystem of 100,000+ partners create extraordinary switching costs. Its Graviton custom ARM-based processors deliver superior price-performance, further entrenching its competitive position. Continued billion-dollar investments in AI-optimized infrastructure ensure AWS remains the go-to platform for enterprise AI workloads.

02. Microsoft Azure

Headquarters: Redmond, WA, USA

Founded: 2010 (Azure launch)

Parent: Microsoft Corporation (est. 1975)

Global Market Share: ~20%

Regions: 60+ globally

Industry Focus: Enterprise Cloud, AI, Hybrid IT

Company Overview: Microsoft Azure is the second-largest hyperscale cloud platform globally, commanding approximately 20% of the cloud infrastructure market. Azure's strategic differentiation lies in its deep integration with the Microsoft enterprise software ecosystem — Office 365, Teams, Dynamics 365 — which creates a powerful on-ramp for enterprise cloud migration. Microsoft's multi-billion-dollar investment in OpenAI has positioned Azure as the leading platform for generative AI deployment.

Key Products & Services: Azure Virtual Machines, Azure Kubernetes Service (AKS), Azure OpenAI Service, Azure Synapse Analytics, Microsoft Fabric (unified analytics), Azure Arc (hybrid/multi-cloud management), and Azure Stack for on-premises deployments. Microsoft's hyperscale data centers are strategically positioned across 60+ regions with additional planned expansions in Southeast Asia, Africa, and the Middle East.

Strategic Advantages: Azure benefits from Microsoft's existing 300+ million enterprise software users, who represent a natural conversion funnel to cloud services. The $13 billion+ OpenAI partnership has made Azure the default AI cloud for enterprises globally. Microsoft's sustainability commitments — 100% renewable energy by 2025, carbon negative by 2030 — also resonate strongly with ESG-focused enterprise buyers.

03. Google Cloud Platform (GCP)

- Headquarters :

- Founded:

- Parent:

- Global Market Share :

- Regions:

- Industry Focus:

- Company Overview:

- Key Products & Services:

- Strategic Advantages:

04. Equinix, Inc.

- Headquarters :

- Founded:

- Parent:

- Global Market Share :

- Regions:

- Industry Focus:

- Company Overview:

- Key Products & Services:

- Strategic Advantages:

05. Meta Platforms (Facebook)

- Headquarters :

- Founded:

- Parent:

- Global Market Share :

- Regions:

- Industry Focus:

- Company Overview:

- Key Products & Services:

- Strategic Advantages:

Competitive Landscape & Market Concentration

The global hyperscale data center market is characterized by high concentration at the top — the three largest cloud providers (AWS, Microsoft Azure, Google Cloud) collectively command approximately 60–65% of global cloud infrastructure spending, which directly translates to hyperscale data center dominance. This concentration is further reinforced by enormous barriers to entry: building a single hyperscale data center campus requires capital investment in the range of $1–5 billion and 18–36 months of construction time, effectively limiting competition to well-capitalized incumbents.

Market Concentration Snapshot

|

Company |

Estimated Cloud Market Share |

Strategy |

|---|---|---|

|

Amazon Web Services (AWS) |

~31% |

Global expansion, AI infrastructure, developer ecosystem |

|

Microsoft Azure |

~20% |

OpenAI partnership, enterprise integration, hybrid cloud |

|

Google Cloud Platform |

~10–12% |

AI-first differentiation, TPU silicon, open source |

|

Alibaba Cloud |

~4% (global) / ~30% (China) |

APAC dominance, proprietary silicon, government cloud |

|

IBM Cloud |

~7% |

Hybrid cloud, regulated industries, Red Hat OpenShift |

|

Others (Equinix, NTT, QTS, etc.) |

~26%+ |

Colocation, interconnection, regional specialization |

Key Competitive Dynamics

Mergers & Acquisitions: The hyperscale sector has seen landmark M&A activity — NVIDIA's $6.9B acquisition of Mellanox (2020), Microsoft's OpenAI partnership ($13B+), Cisco's $28B Splunk acquisition (2024), Blackstone's $10B privatization of QTS (2021), and ongoing consolidation among colocation providers. Expect further M&A as hyperscale operators seek to vertically integrate AI hardware, software, and infrastructure capabilities.

Innovation Strategies: Leading players are investing in proprietary silicon (AWS Graviton, Google TPU, Apple Silicon, Alibaba Yitian, Meta MTIA) to reduce unit economics and differentiate their platforms. Liquid cooling, direct-to-chip thermal management, and advanced power distribution are becoming competitive battlegrounds as AI workloads drive power densities beyond the capabilities of traditional air-cooled infrastructure.

Regional Analysis: Where Hyperscale Growth Is Happening

North America

The dominant region, anchored by Northern Virginia (the world's largest data center market), Silicon Valley, Dallas-Fort Worth, and Chicago. The US accounts for the majority of global hyperscale investment, driven by AWS, Azure, Google, Meta, and Apple. Canada is emerging as an attractive secondary market due to its cool climate (natural cooling advantage), renewable energy availability, and proximity to US markets.

Europe

Europe's data center market is concentrated in the FLAP-D markets (Frankfurt, London, Amsterdam, Paris, Dublin), though energy costs and regulatory pressures are driving diversification into the Nordics (Stockholm, Helsinki), Iberian Peninsula (Madrid, Lisbon), and Central Eastern Europe. The EU AI Act and GDPR are creating demand for in-region data sovereignty solutions that benefit local colocation providers.

Europe's data center market is concentrated in the FLAP-D markets (Frankfurt, London, Amsterdam, Paris, Dublin), though energy costs and regulatory pressures are driving diversification into the Nordics (Stockholm, Helsinki), Iberian Peninsula (Madrid, Lisbon), and Central Eastern Europe. The EU AI Act and GDPR are creating demand for in-region data sovereignty solutions that benefit local colocation providers.

Asia-Pacific

The fastest-growing region globally, with hyperscale buildouts accelerating across Singapore, Tokyo, Seoul, Osaka, Sydney, Mumbai, and Jakarta. China's domestic hyperscale market — led by Alibaba, Tencent, and Baidu — is among the world's largest. India represents a particularly significant growth opportunity, driven by 900M+ internet users, government digitalization initiatives, and rapidly rising enterprise cloud adoption.

Latin America

An emerging market with significant growth potential, particularly in Brazil (São Paulo), Mexico (Mexico City), and Chile (Santiago). Brazil's combination of a large digital economy, growing cloud adoption, and renewable energy resources makes it the region's primary hyperscale destination. All three major cloud providers (AWS, Azure, GCP) have established data center regions in Brazil.

Middle East & Africa

A rapidly emerging hyperscale destination, with the UAE (Dubai, Abu Dhabi) and Saudi Arabia (NEOM, Riyadh) emerging as the region's primary hubs, backed by sovereign wealth fund investment. AWS, Azure, Google, and Alibaba have all established data center regions in the Gulf. Africa's market remains nascent but offers long-term potential driven by mobile-first internet adoption and cloud government services initiatives.

Japan

Japan is one of Asia-Pacific's leading hyperscale data center markets, with Tokyo serving as the primary hub and Osaka providing key disaster recovery and redundancy capabilities. Strong demand for cloud computing, AI, 5G, and enterprise digital transformation is driving continuous infrastructure expansion. Major cloud providers including Amazon Web Services, Microsoft, and Google continue to invest heavily in the country. Japan's advanced connectivity, reliable power infrastructure, and growing AI adoption position it as a strategic hyperscale growth market in the Asia-Pacific region.

Emerging Trends Shaping the Hyperscale Data Center Market

AI & Generative AI Infrastructure Boom: The generative AI wave is driving unprecedented hyperscale investment. Enterprises are building private AI clouds, and hyperscale providers are racing to develop AI-optimized data centers with 50–100MW+ power densities, liquid cooling, and NVLink/InfiniBand GPU fabrics. This is the single largest demand catalyst for the market through 2031.

Liquid Cooling Revolution: Traditional air cooling cannot handle the 300W+ TDP of modern AI GPUs. Direct-to-chip liquid cooling, rear-door heat exchangers, and full liquid immersion are moving from niche to mainstream in hyperscale AI deployments. Operators like Microsoft and Google are piloting subsea and underground data center concepts to further reduce cooling energy costs.

Sustainability & Carbon Neutrality: Hyperscale operators face intense ESG pressure to decarbonize. Major players including Google, Apple, and Microsoft have committed to 24/7 carbon-free energy. Investments in on-site solar, wind PPAs, geothermal, and long-duration energy storage are fundamentally changing the power procurement strategies of hyperscale data centers globally.

Edge Computing Proliferation: The shift toward edge computing — processing data close to where it's generated — is creating demand for a new class of smaller, distributed hyperscale-adjacent facilities. 5G network slicing, autonomous vehicles, and industrial IoT are driving investments in edge data centers co-located with telecom infrastructure, expanding the total hyperscale addressable market.

Power Density & Nuclear Energy: The explosion in AI compute demand is exhausting power grid capacity in major data center markets. Hyperscale operators are pursuing nuclear power agreements (Microsoft's Three Mile Island restart deal, Amazon's SMR investments) and on-site generation to secure the reliable, carbon-free power needed for next-generation AI data centers.

Sovereign Cloud & Data Residency: Governments globally are enacting data localization laws requiring sensitive data to be processed and stored within national borders. This is driving hyperscale operators to develop sovereign cloud offerings — physically and logically isolated cloud regions with enhanced security assurances — in markets from Saudi Arabia to Australia and India.

Future Outlook 2026–2031: The Road to a $596 Billion Market

The hyperscale data center market's trajectory through 2031 is compelling and largely irreversible. The fundamental demand drivers — AI compute, cloud migration, IoT data volumes, 5G network deployment — are structural forces that will sustain investment cycles for decades. Several specific themes will define the market's evolution through 2031:

AI Infrastructure as the Defining Investment Theme

Every major technology company globally has committed to multi-billion-dollar AI infrastructure investments that will flow directly into hyperscale data center construction and equipment. Microsoft has announced $80B in data center investment for fiscal 2025 alone; Google and Amazon are on comparable trajectories. This investment wave will sustain extraordinary CAGR through at least 2028, potentially beyond.

Vertical Integration & Proprietary Silicon

The major hyperscale operators are progressively designing their own chips — reducing dependence on external semiconductor suppliers and creating infrastructure optimized specifically for their own workloads. By 2031, a significant portion of hyperscale compute will run on proprietary silicon, reshaping the semiconductor supply chain and creating new competitive moats for the vertically integrated players.

Data Center as Critical National Infrastructure

Governments are increasingly treating hyperscale data centers as strategic national infrastructure — comparable to electricity grids and telecommunications networks. This is driving government investment in data center parks, preferential land and energy access, and national cloud initiatives that will accelerate hyperscale buildouts in emerging markets including India, Saudi Arabia, Brazil, and Indonesia through 2031.

The $596 Billion Opportunity

At the projected 28.52% CAGR, the global hyperscale data center market will more than 9× in value between 2021 and 2031 — from $62 billion to $596 billion. This growth represents one of the largest wealth creation opportunities in the history of the technology industry, spanning equipment manufacturers, colocation operators, cloud providers, software vendors, and the broader ecosystem of services that support hyperscale infrastructure.

|

Year |

Estimated Market Size |

Key Growth Theme |

|---|---|---|

|

2021 (Base) |

USD 62 Billion |

Post-pandemic cloud acceleration |

|

2023 |

~USD 103 Billion |

Cloud migration + early AI infrastructure |

|

2025 |

~USD 170 Billion |

Generative AI buildout, 5G edge integration |

|

2027 |

~USD 280 Billion |

Sovereign cloud, liquid cooling at scale |

|

2029 |

~USD 430 Billion |

Nuclear power integration, custom silicon dominance |

|

2031 (Forecast) |

USD 596 Billion |

Full AI economy infrastructure backbone |

Frequently Asked Questions (FAQ)

Q1. What is the global hyperscale data center market size?

The global hyperscale data center market was valued at USD 62 billion in 2021 and is projected to reach USD 596 billion by 2031, according to Intellectual Market Insights Research (Report ID: IMI-001580). This represents a compound annual growth rate (CAGR) of 28.52% over the forecast period 2023–2031.

Q2. Who are the leading companies in the hyperscale data center market?

The leading companies include Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform, Equinix, Meta Platforms, NVIDIA, Cisco Systems, Intel, IBM, Alibaba Cloud, Dell Technologies, HPE, Arista Networks, Apple, Baidu, NTT Communications, Western Digital, Ericsson, QTS (Blackstone), and Mellanox/NVIDIA. AWS leads with approximately 31% of the global cloud market share.

Q3. What is the forecast CAGR for the hyperscale data center market?

The hyperscale data center market is forecast to grow at a CAGR of 28.52% from 2023 to 2031. This makes it one of the fastest-growing segments in the global technology industry, driven by AI infrastructure demand, cloud migration, IoT expansion, and 5G rollout.

Q4. Which region dominates the hyperscale data center market?

North America — particularly the United States — dominates the global hyperscale data center market, driven by the presence of the world's largest cloud providers (AWS, Azure, Google Cloud) and the concentration of technology investment. However, Asia-Pacific is the fastest-growing region, with China, India, Japan, and Southeast Asia experiencing explosive hyperscale development.

Q5. What are the key growth drivers for the hyperscale data center market?

Key growth drivers include: (1) explosive demand for cloud-based services and AI infrastructure; (2) growing enterprise requirements for high application performance; (3) the need to reduce CAPEX and OPEX through shared hyperscale infrastructure; (4) IoT proliferation generating unprecedented data volumes; (5) 5G network deployment enabling new edge computing use cases; and (6) digital transformation initiatives across all industry verticals.

Q6. What is a hyperscale data center?

A hyperscale data center is a type of data center facility that supports and manages an extremely large number of physical and virtual servers simultaneously. Typically defined as housing a minimum of 5,000 servers in a facility of at least 10,000 square feet, hyperscale data centers are designed with a single, massively scalable compute architecture that can dynamically expand or contract to meet demand. They are operated by cloud providers, colocation companies, and large internet platforms.

Q7. What are the main market restraints for hyperscale data centers?

The primary market restraint is the high infrastructural overhead required to build and operate hyperscale facilities, including costs for land, construction, power systems (generators, UPS), advanced cooling infrastructure, and highly skilled technical staff. Additionally, securing adequate power supply in data center-dense markets (Northern Virginia, Singapore, Dublin) has become a significant constraint as AI workloads drive power requirements to unprecedented levels.

Q8. What are the key market segments in the hyperscale data center industry?

Q9. How is AI impacting the hyperscale data center market?

Q10. Which company has the largest market share in the hyperscale data center market?

Q11. What sustainability initiatives are hyperscale data center operators pursuing?

Q12. What is the colocation segment in hyperscale data centers?

Q13. How is edge computing related to hyperscale data centers?

Q14. What is the role of BFSI in the hyperscale data center market?

Q15. What technologies will define the hyperscale data center market by 2031?

Conclusion

The global hyperscale data center market stands at the nexus of every transformative technology trend of the 21st century — artificial intelligence, cloud computing, 5G, IoT, and digital transformation. With a projected market size of USD 596 billion by 2031 and a CAGR of 28.52%, it represents one of the most compelling investment and business opportunities in the modern economy.

The top companies profiled in this report — from hyperscale cloud giants like AWS, Microsoft Azure, and Google Cloud, to infrastructure providers like NVIDIA, Cisco, Equinix, and Dell Technologies — are collectively investing hundreds of billions of dollars to build the digital infrastructure backbone that will power the global economy for decades to come. Their innovations in AI silicon, liquid cooling, sustainable energy, and software-defined infrastructure are not merely expanding market capacity — they are fundamentally redefining what is possible in computing.

For investors, technology leaders, and industry analysts, understanding the competitive dynamics, regional growth vectors, and emerging technology trends in the hyperscale data center market is essential to navigating the digital decade ahead. The companies that build, operate, and enable hyperscale infrastructure today are building the foundations of tomorrow's AI-powered civilization.