Top Leading Companies Blog Global Hydroponics Market 2025-26

Author:

Intellectual Market Insights Research

Published Date:

25 Jun 2026

Top 10 Leading Companies in the Global Hydroponics Market Driving Industry Growth in 2026

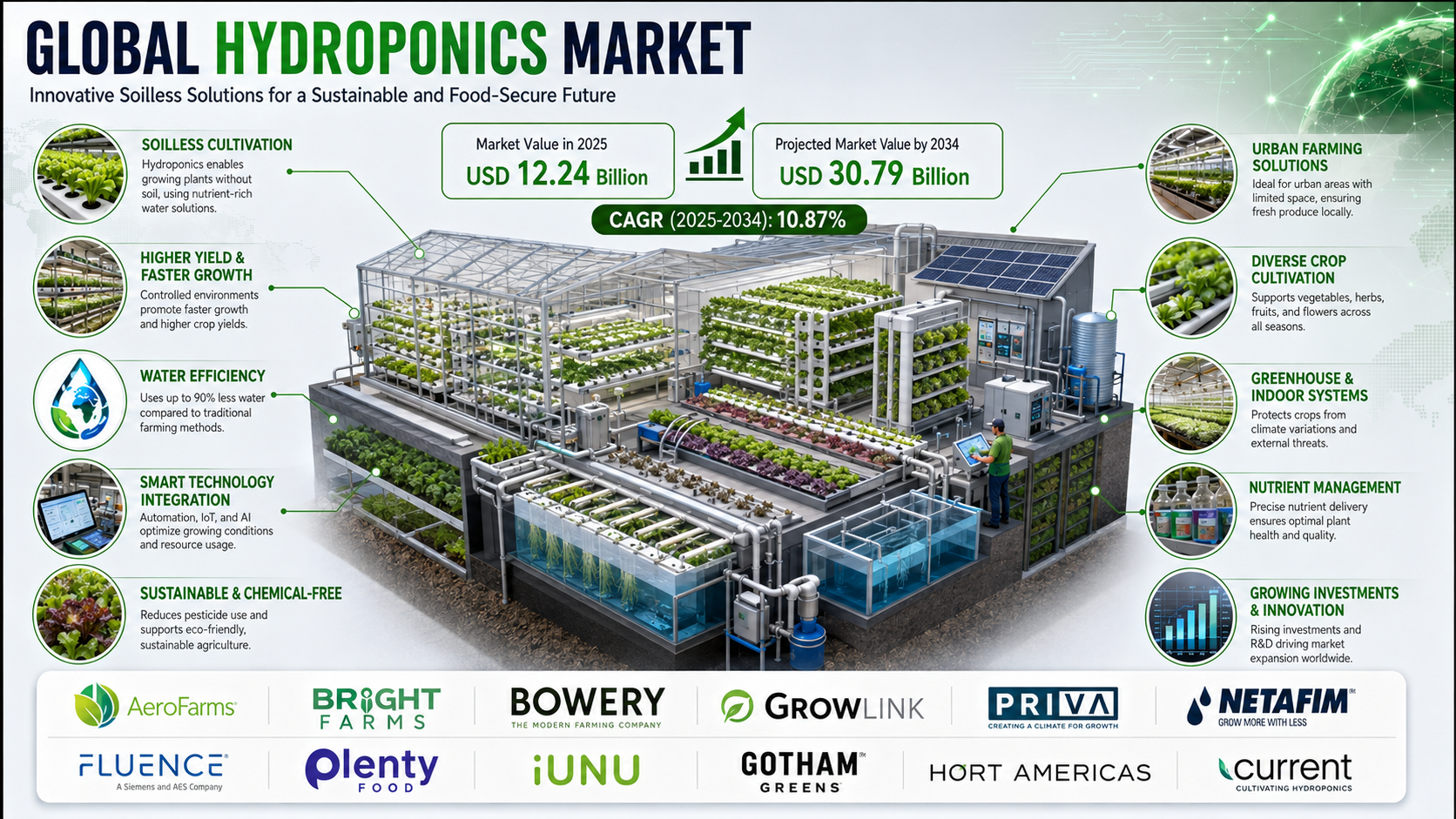

The global Hydroponics market has evolved from a niche agricultural technique into one of the most strategically important sectors at the intersection of food technology, controlled-environment agriculture, and sustainable production. As traditional farmland comes under pressure, water scarcity intensifies, and consumer demand for fresh, local, pesticide-controlled produce surges, the hydroponics industry stands at a defining growth inflection point entering 2026.

According to Intellectual Market Insights Research, the Hydroponics market was valued at approximately USD 12.24 Billion in 2025 and is projected to grow at a CAGR of 10.87%, reaching USD 30.79 Billion by 2034. This robust trajectory is anchored by increasing pressure on arable land and freshwater resources, rapid urbanization, advances in farming technologies, and government efforts to improve food production and strengthen food security.

North America led the market with a revenue share of 36.02% in 2025, generating USD 4.41 billion, driven by widespread indoor vertical farming and well-developed greenhouse infrastructure. Meanwhile, the UAE is forecast to register a CAGR of 11.83% over the forecast period the fastest-growing national market propelled by harsh climate conditions and ambitious food security investments.

Market Overview

|

Parameter |

Details |

|---|---|

|

Market Size (2025) |

USD 12.24 Billion |

|

Market Size (2026) |

USD 13.45 Billion |

|

Projected Market Size (2034) |

USD 30.79 Billion |

|

CAGR (2026–2034) |

10.87% |

|

Leading Region (2025) |

North America (36.02% share) |

|

Fastest-Growing Country |

UAE (CAGR 11.83%) |

|

Leading System Type |

Nutrient Film Technique (NFT) |

|

Second-Largest System Type |

Drip Hydroponics (CAGR 10.69%) |

|

Leading Growing Environment |

Controlled Greenhouse Hydroponics |

|

Fastest-Growing Environment |

Fully Indoor Hydroponics (CAGR 11.42%) |

|

Leading Crop Type |

Leafy Greens |

|

Second-Largest Crop Type |

Tomatoes (CAGR 10.85%) |

|

Leading End User |

Protected Agriculture Enterprises |

|

Fastest-Growing End User |

Large Commercial Growers (CAGR 11.22%) |

|

Key Growth Drivers |

Water scarcity, urbanization, automation, AI precision growing |

|

Key Challenges |

High capital intensity, limited small grower adoption |

|

Major Players |

Netafim, Richel Group, Priva, Signify (Philips), Hydrofarm, Haifa Group |

|

Forecast Period |

2026–2034 (Intellectual Market Insights Research) |

|

Study Period |

2021–2034 |

Why the Hydroponics Market Is Growing

1. Water Scarcity and Land Constraints Accelerate Adoption

One of the primary structural drivers is increasing pressure on arable land and freshwater resources globally. Hydroponic systems use significantly less water than traditional farming while producing more crops in the same space. This makes them especially compelling in cities, water-stressed regions such as the Middle East and parts of Asia Pacific, and densely populated areas in North America and Europe where the economics of conventional agriculture are under growing pressure. The precision delivery of nutrients directly to plant root systems enhances yield consistency and resource efficiency simultaneously.

2. Rapid Urbanization and Demand for Local, Traceable Produce

Rapid urbanization combined with rising consumer demand for locally grown, traceable produce is driving market demand for decentralized cultivation models. Hydroponic systems positioned near urban consumption centres reduce transport costs, post-harvest food waste, and environmental impact while supporting retailers' sustainability goals. This approach also enables cities to build more resilient, self-sufficient food supply networks creating long-term structural demand independent of seasonal weather variability.

3. Automation Integration and Technology-Driven Production Models

A major trend reshaping the market is the move toward automation and data-guided cultivation. Growers are increasingly integrating sensors, climate-control software, automated nutrient dosing, and remote monitoring to achieve higher yield consistency and reduce labour dependency. Advanced systems such as deep water culture setups support rapid plant growth by suspending roots in oxygenated nutrient solutions, improving uptake efficiency and yield stability. The market is steadily consolidating from many small growers toward larger, more professionally managed commercial businesses leveraging these technologies.

4. AI and Precision Nutrient Dosing Drive Commercial Returns

Artificial intelligence and precision nutrient dosing allow growers to maximize yield consistency while minimizing input waste. As sensors become cheaper and software becomes easier to deploy at scale, commercial operations are running more efficiently and demonstrating better returns on investment. This creates a reinforcing cycle improved economics attract investment, which accelerates further technology adoption and scale.

5. Retail Sustainability Demands Create Structural Market Pull

Health-conscious consumers and major retailers increasingly require year-round, locally sourced, pesticide-controlled fresh produce. Hydroponic systems particularly fully indoor vertical farms are uniquely positioned to meet these specifications reliably and at scale. This retail-driven pull supports long-term commercial demand in North America and Europe, where food safety standards and sustainability commitments are most demanding.

6. Government Food Security Programmes Support Emerging Markets

Governments across the Middle East, Asia Pacific, and beyond are directly investing in controlled-environment agriculture to reduce food import dependency. The UAE's high growth rate of 11.83% is directly linked to government-backed food security strategies investing in greenhouse and indoor hydroponic infrastructure. Singapore, Japan, Saudi Arabia, and India are similarly deploying public-sector capital to support hydroponic adoption at commercial scale.

Top 10 Companies in the Global Hydroponics Market

- Netafim Ltd. (Israel)

- Richel Group / Richel Serres de France (France)

- Priva Holding B.V. (Netherlands)

- Signify N.V. Philips Horticulture LED Solutions (Netherlands)

- Argus Control Systems Ltd. (Canada)

- AmHydro American Hydroponics (U.S.)

- LumiGrow Inc. (U.S.)

- Hydrofarm Holdings Group, Inc. (U.S.)

- Nutriculture UK Ltd. (U.K.)

- Haifa Group (Israel)

Company Profiles

1. Netafim Ltd. (Israel)

Headquarters: Tel Aviv, Israel

Industry Focus: Drip Irrigation and Precision Hydroponic Water Systems

Global Presence: 110+ countries across all major growing regions worldwide

Company Overview: Netafim is a global pioneer in drip irrigation and precision water management for agriculture, with deep expertise in hydroponic fertigation systems. As the world's largest manufacturer of drip and micro-irrigation systems, Netafim has become a cornerstone supplier to commercial greenhouse operators and large-scale hydroponic growers across all major markets. The company's greenhouse water systems deliver nutrient-rich water precisely to plant root zones, maximizing efficiency and minimizing waste a critical competitive differentiator in water-stressed agricultural markets where hydroponics is growing fastest.

Key Products and Services: Netafim supplies drip emitters, sub-surface irrigation lines, fertigation controllers, and integrated greenhouse hydroponic systems. Its NetBeat digital farming platform integrates sensor data with automated irrigation scheduling, supporting precision nutrient delivery across large commercial growing operations.

Market Position: Netafim is recognized as one of the top players in the global hydroponics market, with operations spanning more than 110 countries. Its dominance in drip hydroponics the second-largest system type in the market growing at a CAGR of 10.69% through 2034 positions it to benefit significantly from the expanding preference for drip systems in fruiting-crop greenhouse operations across Europe, the Americas, and Asia Pacific.

Strategic Advantages: Unmatched global scale in irrigation infrastructure, strong long-term relationships with protected agriculture enterprises, digital precision farming capabilities through the NetBeat platform, and proven reliability in high-intensity commercial greenhouse environments across multiple climate types.

2. Richel Group (Richel Serres de France) France

Headquarters: Eyragues, France

Industry Focus: Greenhouse Design, Manufacture, and Construction

Global Presence: Europe, North Africa, the Americas, Middle East

Company Overview: Richel Group is one of Europe's leading greenhouse builders, specializing in the design, manufacture, and installation of high-performance protected cultivation structures. With decades of experience in controlled-environment agriculture, Richel's greenhouse systems form the physical infrastructure within which hydroponic systems operate. The company serves commercial vegetable growers, cannabis cultivators, and research institutions spanning a diverse portfolio of protected agriculture applications.

Key Products and Services: Richel designs and builds tunnel, multi-span, and Venlo glass greenhouse structures integrated with hydroponic growing systems. Its product portfolio covers production environments for tomatoes, peppers, cucumbers, and cannabis, with solutions adaptable to diverse climates from Mediterranean to northern European conditions.

Market Position: As a key provider of the physical infrastructure underpinning the controlled greenhouse hydroponics segment which held the largest share of the market in 2025 Richel plays a critical enabling role in the industry's growth. Its expansion into cannabis greenhouse design diversifies its addressable market into a high-value regulated crop category with significant long-term potential.

Strategic Advantages: European greenhouse construction leadership, comprehensive design-to-installation project delivery capability, long track record in high-value crop environments, and demonstrated adaptability to both temperate and arid climate conditions across multiple continents.

3. Priva Holding B.V. (Netherlands)

Headquarters: De Lier, Netherlands

Industry Focus: Climate Control and Automation for Greenhouse Horticulture

Global Presence: Netherlands, Europe, Americas, Asia Pacific

Company Overview: Priva is a world leader in automation and data management systems for greenhouse horticulture and indoor farming. Founded in the Netherlands the global centre of advanced greenhouse technology Priva develops integrated climate control, process automation, and energy management solutions that are central to the intelligent operation of commercial hydroponic facilities. Its technology enables growers to automate nutrient dosing, monitor environmental conditions in real time, and optimize energy consumption across entire large-scale growing facilities.

Key Products and Services: Priva offers climate computers, process management systems, fertigation controllers, and its Priva Connext platform for data-driven greenhouse management. This integrated software-hardware ecosystem directly supports the automation trend that is one of the defining structural drivers reshaping the global hydroponic market in 2026.

Market Position: Priva is a tier-1 technology partner for the largest and most sophisticated protected agriculture enterprises globally the end-user segment that led the hydroponics market in 2025. Its Netherlands base gives it proximity to the world's most advanced horticulture innovation cluster, enabling continuous product development aligned with the needs of the most demanding commercial growers.

Strategic Advantages: Deep horticulture automation expertise, integrated hardware-software ecosystems that reduce reliance on multiple vendors, strong commercial relationships in Europe and North America, and proven scalability across large multi-site greenhouse network operations.

4. Signify N.V. Philips Horticulture LED Solutions (Netherlands)

Headquarters:

Industry Focus:

Global Presence:

Company Overview:

Key Products and Services:

Market Position:

Strategic Advantages:

5. Argus Control Systems Ltd. (Canada)

Headquarters:

Industry Focus:

Global Presence:

Company Overview:

Key Products and Services:

Market Position:

Strategic Advantages:

Competitive Landscape

The global Hydroponics market in 2026 is characterized by moderate fragmentation, with most competition occurring at different points in the value chain rather than among companies serving the entire market end-to-end.

Market Structure

The market includes a diverse range of player types global technology providers, greenhouse builders, irrigation specialists, nutrient manufacturers, lighting companies, and local system integrators. Unlike some industries where a handful of vertically integrated giants dominate, the hydroponics market's competitive dynamics are shaped by specialization at the component or subsystem level, with the most sophisticated growers assembling best-in-class solutions from multiple specialist suppliers.

Technology Differentiation as the Competitive Battleground

Firms focusing on drip irrigation, climate control, LED lighting, and fertigation systems compete through better technology performance, greater product reliability, and deeper integration of their offerings within grower operations. Technological differentiation and integrated solutions are intensifying competitive dynamics across the entire hydroponics value chain, as growers reward suppliers who can reduce operational complexity and improve yield predictability.

Market Expansion as the Primary Growth Strategy

Market expansion both geographic and into new crop categories is the key strategy which is supporting product sales growth and overall market development. Companies that successfully enter the fastest-growing markets in the Middle East, Asia Pacific, and South America with proven technology solutions are securing first-mover advantages in markets projected to grow substantially through 2034.

Consolidation Reshaping the Retail and Distribution Tier

Both the retail distribution and commercial production segments are consolidating rapidly. Hydrobuilder Holdings' acquisition of New England Hydroponics in July 2025 and Blue River Financial Group's acquisition of Simply Hydroponics in April 2025 illustrate how well-capitalized players are using acquisitions to rapidly expand geographic retail presence, customer base, and product range accelerating the market's maturation from fragmented to more organized commercial structures.

Regional Analysis

North America 36.02% Revenue Share (2025)

North America leads the global hydroponics market, generating USD 4.41 billion in 2025. The United States is the dominant national market at USD 3.49 billion, driven by widespread indoor vertical farming, well-developed greenhouse vegetable production, and strong retail demand for locally sourced, pesticide-controlled produce. Leafy greens are the main crops grown indoors, while tomatoes and cucumbers are the top choices in greenhouse operations. Canada contributes significantly through its large greenhouse tomato sector, while Mexico focuses on protected vegetable production for export. High-tech integration and retailer localization strategies continue to support steady commercial expansion across the region.

Asia Pacific One of the Fastest-Growing Regions

The Asia Pacific market was valued at USD 2.86 billion in 2025 and is one of the fastest-growing regions globally, driven by urbanization, food security initiatives, and rapidly expanding controlled-environment agriculture investment. China and India are scaling greenhouse hydroponics at pace, while Japan and Singapore are leading with sophisticated indoor plant factory models focused on consistent leafy green production in fully controlled environments. The region balances both greenhouse and indoor systems. Key figures: China reached approximately USD 0.97 billion (7.89% of global share), Japan approximately USD 0.44 billion (3.58%), and India approximately USD 0.32 billion (2.58%) in 2025.

Europe Advanced Technology, Export-Oriented Production

The European market reached USD 3.46 billion in 2025, underpinned by extensive greenhouse cultivation particularly in the Netherlands, Spain, and France supported by advanced horticulture technologies and strong export-oriented vegetable supply chains. Drip hydroponics is the dominant system for tomato and pepper production across southern Europe, while indoor hydroponics is gaining traction in Germany and the U.K. where retail localization drives adoption. Germany reached approximately USD 0.36 billion and the U.K. approximately USD 0.31 billion in 2025. Growth is moderate compared to emerging markets but supported by sophisticated existing infrastructure.

South America Emerging Growth Market

The South America market recorded USD 0.75 billion in 2025, with significant growth expected through the forecast period. Brazil, Argentina, and Chile lead with greenhouse hydroponics focused on exporting tomatoes and peppers. Indoor hydroponics remains less widespread due to higher setup costs, but urban expansion in major cities is gradually driving adoption of indoor systems as access to financing and technology improves.

Middle East and Africa Food Security and Water Scarcity Drive Investment

The Middle East and Africa market reached USD 0.76 billion in 2025. Food security and water scarcity are the primary market drivers, making hydroponics a strategic national priority in several Gulf states. Saudi Arabia and the UAE are making the most substantial investments in greenhouse and indoor hydroponic infrastructure to reduce food import dependency. The UAE is set to grow at a CAGR of 11.83% during the forecast period the fastest of any country market reflecting both the severity of climate constraints and the scale of government commitment to food self-sufficiency through controlled-environment agriculture.

Segmentation Analysis

By Hydroponic System Type

Nutrient Film Technique (NFT) Market Leader

The NFT segment held the largest market share in 2025. NFT systems continuously move a thin layer of nutrient solution over plant roots, keeping roots well-oxygenated while reducing water and nutrient waste. This setup enables precise nutrient control and supports rapid growth making it especially well-suited to commercial indoor farms and vertical growing facilities. NFT's water efficiency and modular design also make it a strong choice for urban spaces where maximizing yield per square meter is a priority.

Drip Hydroponics Second-Largest, CAGR 10.69%

Drip hydroponics holds the second-largest market share and is expected to grow at a CAGR of 10.69% through 2034, driven by its versatility and effectiveness for fruiting crops such as tomatoes, peppers, and cucumbers. Unlike NFT, drip systems deliver nutrients directly to the roots via emitters enabling more precise control of water and fertilizer for larger, longer-growing plants that require higher and more variable nutrient inputs during different growth stages.

Other System Types: DWC (Raft), Ebb and Flow, and Wick systems serve more specialized commercial and hobbyist applications across the market.

By Growing Environment

Controlled Greenhouse Hydroponics Market Leader

The controlled greenhouse hydroponics segment held the largest market share in 2025, combining climate control, scalability, and cost efficiency. Unlike fully indoor systems, greenhouses use natural sunlight reducing the energy requirements for artificial lighting and making long-term operations more economically sustainable, especially for fruiting crops requiring high light levels and longer growing seasons. Existing greenhouse infrastructure across key horticulture regions in Europe, North America, and Asia Pacific makes adoption within protected agriculture frameworks faster and less capital-intensive.

Fully Indoor Hydroponics Fastest-Growing Environment, CAGR 11.42%

Fully indoor hydroponics is the second-largest and fastest-growing environment segment at a CAGR of 11.42% through 2034. Fully enclosed systems do not rely on outside weather conditions, enabling year-round crop production anywhere regardless of season, climate, or geography. This makes indoor hydroponics especially appealing in regions with harsh weather, insufficient water, or limited farmland. Indoor farms are typically optimized for fast-growing crops such as leafy greens and herbs, which command consistent retail demand for fresh, pesticide-free produce.

By Crop Type

Leafy Greens Market Leader

The leafy greens segment led the global market in 2025. Lettuce, spinach, arugula, and mixed salad greens thrive in NFT and deep water culture systems, benefiting from steady nutrient and oxygen levels that drive rapid development. Their small root systems suit vertical stacking in indoor farms, maximizing output per square meter. Year-round health-conscious consumer demand provides reliable and predictable commercial offtake for growers.

Tomatoes Second-Largest, CAGR 10.85%

Tomatoes are the second-largest crop segment and are projected to grow at a CAGR of 10.85% through 2034 as the leading fruiting crop in greenhouse hydroponic systems globally. Unlike leafy greens, tomatoes require longer growth cycles and structural support making drip hydroponic systems in protected greenhouse environments particularly suited to their production. Hydroponic cultivation enables precise nutrient control during the critical flowering and fruiting stages, resulting in more consistent yields, larger fruit size, and superior quality compared to field-grown production.

Other crop segments: Herbs, cucumbers, peppers, and others each serve distinct commercial and retail segments within the broader market.

By End User

Protected Agriculture Enterprises Market Leader

The protected agriculture enterprises segment led the global market in 2025. These operators work in well-structured, high-investment greenhouses and controlled environments designed specifically for efficient commercial crop production. Their business models are aligned with retail contracts, export markets, and year-round supply commitments requiring the kind of reliable, scalable, and precisely controlled hydroponic production that only purpose-built professional systems can deliver.

Large Commercial Growers Fastest-Growing End User, CAGR 11.22%

Large commercial growers represent the fastest-growing end-user segment at a CAGR of 11.22% through 2034. These operations use hydroponic systems at significant scale to boost productivity and resource efficiency across diverse crop portfolios. They typically manage a range of crops and deploy hydroponics specifically to achieve better yields from high-value produce such as leafy greens and tomatoes, while benefiting from economies of scale in procurement and distribution.

Other end-user segments: Urban vertical farm operators, institutional and research facilities, and residential/hobby growers each represent distinct demand pools across the market's full commercial spectrum.

Key Industry Developments

July 2025 Hydrobuilder Holdings Acquires New England Hydroponics Hydrobuilder Holdings LLC acquired New England Hydroponics, gaining five retail stores and one warehouse across Massachusetts and Maine. The acquisition made Hydrobuilder a stronger leader in the U.S. hydroponics, Controlled Environment Agriculture, and specialty agriculture equipment market and significantly expanded its Northeastern U.S. retail footprint.

April 2025 Blue River Financial Group Acquires Simply Hydroponics Blue River Financial Group acquired Simply Hydroponics, LLC, one of the leading U.S. hydroponics companies. The deal helped broaden Blue River's product offering, strengthen its online presence, and expand reach across both commercial and enthusiast grower segments.

January 2025 AeroGarden Launches New Sustainability-Focused Product Line AeroGarden introduced a new product line offering improved performance and reinforcing the brand's commitment to sustainability in consumer and hobbyist hydroponics. The launch underscores continued R&D investment at the residential grower end of the market.

November 2024 GrowGeneration Launches Three Premium Own-Brand Product Lines GrowGeneration Corp., a leading U.S. hydroponics retailer and distributor, launched three new premium product lines under its own brands covering grow lights, key accessories, and growing media designed specifically for indoor and greenhouse hydroponics. The own-brand strategy is aimed at improving margins and differentiating the company's retail offering from commodity competitors.

April 2023 AYR Wellness Acquires Tahoe Hydroponics Company AYR Wellness Inc., a leading vertically integrated U.S. multi-state cannabis operator, acquired Tahoe Hydroponics Company, LLC, one of the leading producers of high-quality cannabis flower using professional hydroponic cultivation methods. This acquisition extends the application of commercial hydroponics further into the regulated cannabis sector.

Market Dynamics

Market Driver Water Scarcity and Land Constraints

The global market's primary growth driver is the increasing pressure on arable land and freshwater resources worldwide. Hydroponic systems address both constraints simultaneously using dramatically less water than conventional soil-based farming while producing significantly more output per unit of land area. This dual advantage makes hydroponics economically and strategically compelling in the regions experiencing the fastest growth: the Middle East, parts of Asia Pacific, and urban centres in North America and Europe where land costs and water availability are acute commercial challenges.

Market Restraint High Capital Intensity

The most significant structural challenge facing the market is the high upfront cost of establishing commercial hydroponic operations. Setting up professional systems requires substantial investment in protected growing infrastructure, irrigation equipment, climate control, lighting, and automation. This capital intensity particularly limits adoption among small and mid-sized growers who may struggle to secure financing, even when long-term operating economics are attractive. Reducing the capital barrier to entry through modular systems, financing programmes, and shared infrastructure models represents one of the key unlocks for the next phase of market growth.

Market Opportunity AI, Precision Technology and Urban Food Networks

Rapid urbanization creates structural demand for decentralized, urban-proximate food production that reduces transport costs, post-harvest waste, and environmental impact while supporting retailers' sustainability objectives. Simultaneously, AI and precision nutrient dosing are making commercial operations progressively more productive and financially viable. As sensors become cheaper and software more scalable, the technology cost barrier is declining widening the addressable market for professional hydroponic systems beyond the largest commercial operators toward mid-sized growers who were previously priced out of the technology.

Future Outlook 2026–2034

The global Hydroponics market is on track to more than double in value from USD 12.24 Billion in 2025 to USD 30.79 Billion by 2034, driven by converging forces across food security imperatives, commercial agriculture technology adoption, urbanization, and retail market transformation.

Growth Projections

Commercial applications particularly leafy greens, tomatoes, and herbs will drive volume expansion in both NFT and drip hydroponic segments. The fully indoor hydroponics environment sub-segment is projected to be the fastest-growing growing environment at a CAGR of 11.42%, while the UAE represents the fastest-growing national market at 11.83%. Large commercial growers represent the fastest-growing end-user segment at a CAGR of 11.22%, reflecting the broader market consolidation trend toward professionally managed, scaled operations.

Investment Opportunities

The highest-value opportunities lie across several distinct domains: high-efficiency LED horticultural lighting systems for indoor vertical farms; integrated climate and nutrient automation software platforms for multi-site greenhouse operators; advanced NFT and drip system hardware for large-scale commercial leafy green and fruiting crop production; AI-powered precision agronomy advisory services; and turnkey protected agriculture infrastructure solutions for the emerging markets of the Middle East, India, and Southeast Asia.

Industry Transformation

The hydroponics industry is transitioning from a niche premium growing technology into a mainstream commercial food production system capable of competing with field-based agriculture on quality, reliability, and increasingly on cost. Operators who combine systems integration capability with deep agronomic expertise, technology reliability, and alignment with major retail supply chain requirements will be best positioned to capture disproportionate share of the market's growth through 2034 and beyond.

FAQ Section

Q1: What is the current size of the global Hydroponics market? The global Hydroponics market was valued at approximately USD 12.24 Billion in 2025 and is projected to grow at a CAGR of 10.87%, reaching USD 30.79 Billion by 2034, according to Intellectual Market Insights Research.

Q2: Which companies are the top leaders in the global Hydroponics market? The top Hydroponics market companies include Netafim Ltd., Richel Group, Priva Holding B.V., Signify N.V. (Philips Horticulture LED Solutions), Argus Control Systems Ltd., AmHydro (American Hydroponics), LumiGrow Inc., Hydrofarm Holdings Group, Nutriculture UK Ltd., and Haifa Group.

Q3: Which region dominates the global Hydroponics market? North America dominated the Hydroponics market in 2025 with a revenue share of 36.02%, generating USD 4.41 billion. The United States alone accounted for USD 3.49 billion, driven by widespread indoor vertical farming and well-developed greenhouse vegetable production infrastructure.

Q4: What is the forecast CAGR for the Hydroponics market? The global Hydroponics market is projected to grow at a CAGR of 10.87% during the forecast period from 2026 to 2034, according to Intellectual Market Insights Research.

Q5: What are the primary growth drivers of the Hydroponics market? Key growth drivers include water scarcity and land constraints accelerating adoption across urban and climate-stressed agricultural markets; increasing urbanization and consumer demand for locally grown traceable produce; automation integration driving technology-led production models; AI and precision nutrient dosing improving commercial returns; and government food security investment programmes in the Middle East, Asia Pacific, and emerging markets.

Q6: Which system type segment holds the largest share in the Hydroponics market? The Nutrient Film Technique (NFT) segment held the largest market share in 2025, driven by continuous nutrient flow efficiency, superior root oxygenation, and scalable modular design suited to commercial indoor farms. Drip hydroponics holds the second-largest share at a CAGR of 10.69%, preferred for fruiting crop greenhouse operations.

Q7: Which growing environment leads the Hydroponics market? Controlled greenhouse hydroponics led the market in 2025 by combining climate control, scalability, and natural sunlight-driven cost efficiency. Fully indoor hydroponics is the faster-growing environment at a CAGR of 11.42%, offering year-round weather-independent production appealing to urban and climate-stressed markets.

Q8: Which crop type leads the Hydroponics market? Leafy greens led the global market in 2025, driven by short growth cycles, high plant density compatibility, and consistent year-round retail demand. Tomatoes are the second-largest crop segment, projected to grow at a CAGR of 10.85% through 2034 as the leading fruiting crop in greenhouse hydroponic systems.

Q9: Which end-user segment leads the Hydroponics market? Protected agriculture enterprises led the global market in 2025, operating in high-investment export-oriented controlled environments with retail and year-round supply commitments. Large commercial growers are the fastest-growing end-user segment at a CAGR of 11.22%, deploying hydroponics at scale to drive productivity and resource efficiency improvements.

Q10: What is the major market trend in Hydroponics? The major trend is automation integration accelerating the transition toward technology-driven hydroponic production models. Growers are deploying sensors, automated nutrient dosing, climate-control software, and remote monitoring at increasing scale driving consolidation toward larger, more professionally managed commercial operations that leverage data for competitive advantage.

Q11: What are the key challenges facing the Hydroponics market? The primary challenge is high capital intensity. Establishing commercial hydroponic systems requires large upfront investment in infrastructure, climate control, lighting, and automation limiting adoption among small and mid-sized growers. Secondary challenges include energy costs for fully indoor operations, skilled agronomic labour requirements, and the need for consistent technical expertise to maximize system performance and crop yield.

Q12: Which country has the fastest-growing Hydroponics market? The UAE is set to grow at a CAGR of 11.83% during the forecast period the fastest of any major country market. The UAE's extreme climate conditions and ambitious national food security objectives are driving rapid government-backed investment in greenhouse and indoor hydroponic systems to reduce dependence on food imports.

Conclusion

The global Hydroponics market is at a defining inflection point in 2026. What began as a niche premium growing technique has evolved into a multi-billion dollar commercial food production ecosystem spanning indoor vertical farms, protected greenhouse enterprises, urban food networks, and international export horticulture. With a projected market value of USD 30.79 Billion by 2034, hydroponics represents one of the most strategically consequential growth opportunities in global agriculture and food technology.

The top companies profiled in this analysis represent the full spectrum of this evolving value chain from global irrigation infrastructure giants like Netafim and precision growing technology leaders like Priva and Signify, to established North American distributors like Hydrofarm and specialist nutrient innovators like Haifa Group. What unites them is a shared recognition that precision growing technology, automation integration, and comprehensive system solutions are the decisive enablers of commercial hydroponics at scale.

For businesses, investors, and agri-food strategists seeking to understand where the hydroponics industry is headed, the message from 2026's competitive landscape is clear: the systems, technologies, and market structures that will define this industry by 2034 are being engineered and financed today and the companies and investors who recognize the convergence of food security imperatives, urban growth, and precision agriculture technology are already building the future of food production.