India's USD 7.4 Billion Earthmoving Empire: The Heavy Machinery Driving 1 Billion Tonnes of Coal

Author:

Intellectual Market Insights Research

Published Date:

01 Jun 2026

India's USD 7.4 Billion Earthmoving Empire: The Heavy Machinery Driving 1 Billion Tonnes of Coal

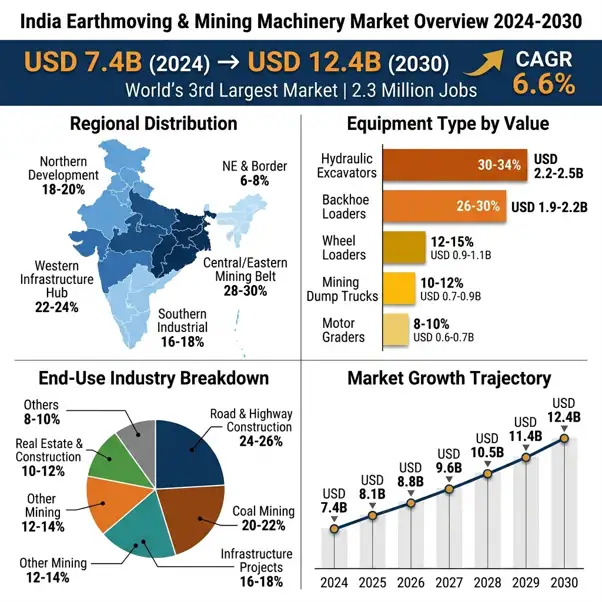

Growth in India is occurring through bricks, cement, and soil. And at its very heart lies a force which is strong and mostly unnoticed - the market for earthmoving and mining machinery, which is worth around USD 7.4 billion in 2024.

This market is expected to grow up to USD 12.4 billion in 2030. This growth will be fueled by three equally massive forces working together: construction of world-class infrastructure on a national scale, increase in production of coal and minerals, and the establishment of industrial belts throughout the country. Underlining all this growth is one goal that stands out in particular for the entire nation of India - its desire to produce 1 billion tonnes of coal each year by 2026-27.

Today, India is placed third in the global market for construction equipment after China and the US. About 70-75 % of the market of construction equipment consists of earth moving and mining equipment, and employment of more than 2.3 million people is directly and indirectly associated with the industry.

The Geography of Heavy Metal: Where India's Machines Work

Distribution of heavy machinery does not take place uniformly throughout India. Distribution depends on the clustering of industries or mining activities in certain areas to form an ecosystem that influences distribution strategies designed by companies.

Central and Eastern Mining Belt consisting of the states of Chhattisgarh, Jharkhand, and Odisha accounts for 28-30 % of total market demand measured in terms of value. The region is known as the heart of coal mining in India and consists of over 400 coal mines operating in this region. About 65 % of total coal produced in India comes from this region. Equipment in this region is primarily comprised of large capacity mining excavators and dumpers.

West Infrastructure Hub including Gujarat, Maharashtra, and Rajasthan makes up for 22-24% market share. The area is driven by Delhi Mumbai Industrial Corridor, major highway construction activities through Bharatmala project, and large limestone quarries in Rajasthan. Gujarat alone contributes to 12% of total cement output in India. This makes for constant demand for equipment throughout the year.

North Development Corridor including Uttar Pradesh, Haryana, Punjab, and Delhi NCR is estimated to contribute 18-20% market share. This is driven by the largest highway construction project in the world and urban infrastructure development. 9,100 km of highway expansion in Uttar Pradesh alone leads to constant demand for equipment at dealerships.

Southern industrial states such as Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana contribute to 16-18% of the market share. The demand in this region is backed by large-scale irrigation projects, urban metro projects, and granite mining activities which help in creating a broad demand base.

Northeastern and Border States contribute to 6-8% of market share; however, their share is rising rapidly owing to border roads projects and connectivity initiatives. Though not contributing much, the growth rate is one of the fastest in the country.

Breaking Down the USD 7.4 Billion: What Machines Drive the Market

Tracing the sources of funds needs one to look at what equipment is being bought and by whom it is being bought. It shows some interesting trends about infrastructure development in India.

By Equipment Type

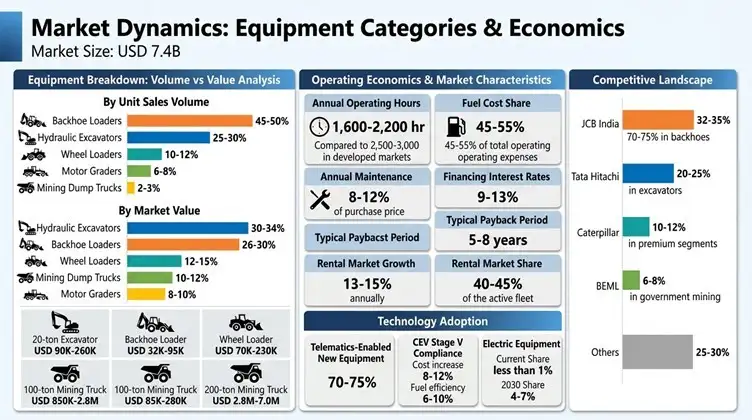

- Hydraulic Excavators rule the top segment in terms of value, contributing 30-34% of total market value or about USD 2.2-2.5 billion. This is the category with the highest growth potential, with a distinct trend towards larger excavators weighing between 30-50 tons for mining and big construction jobs. Although they contribute just 25-30% of sales volume, their sheer value makes them the top performer in terms of revenue.

- Backhoe Loaders have been made in India and are widely known as the country’s national product, contributing 45-50% of total machine sales, but only 26-30% of total market value of about USD 1.9-2.2 billion. The difference in sales and value is a result of their widespread application as the jack-of-all-trades machines of Indian construction industry, which are inexpensive and highly versatile.

- Wheel Loaders make up 12-15% of the market value with sales valued at USD 0.9-1.1 billion, playing very important roles in quarrying, port applications, and material handling operations throughout the nation.

- Mining Dump Trucks constitute only 2-3% of unit sales yet generate 10-12% of the market value at USD 0.7-0.9 billion. A mere 200-ton mining dump truck sells at more than USD 4-7 million, thus accounting for that extreme percentage difference between volume and value.

- The Motor Grader makes up 8-10% of the market value of USD 0.6-0.7 billion, with demand depending solely on the rate of highway construction in the nation.

By End-Use Industry

- Construction of Roads and Highways constitutes the largest segment at 24-26%, owing to programs of national highways and roads of the states. This segment is responsible for the maximum consumption of graders, excavators, backhoes, and compaction machines.

- Coal Mining constituting 20-22%, is directly connected with the 1 billion tonne production objective. This segment consumes equipment that has the maximum value among all categories, thereby making it possibly the most significant in terms of equipment values, although in terms of market share it ranks second.

- The construction of Infrastructure, such as railways, metros, and ports comprises 16-18%, backed by freight corridors, metro rail expansion programs, and development of ports.

- Iron ore mining and other minerals contribute another 12-14%, while real estate and general construction contribute 10-12%.

The Giants Moving India's Earth: Market Leaders

The Indian earthmoving market features a concentrated competitive structure where global manufacturers maintain strong positions through decades of localized manufacturing and deep service networks.

- around 32-35 per cent market share, JCB India is the undisputed market champion and has a 70-75 per cent market share in the backhoe loaders segment. JCB currently has manufacturing plants in Ballabgarh, Pune and Jaipur with over 75,000 machines produced every year and over 10,000 people employed directly. JCB India is one of the biggest operations of the parent company with an estimated turnover of USD 1.9-2.2 billion.

- JCB is the breadth of their distribution network. JCB has penetrated the market with 750+ dealer touchpoints from tier-1 cities to rural areas, making it hard for the competition to catch up.

- Tata Hitachi Construction Machinery, a strategic alliance between Tata Motors and Hitachi, holds about 20-25% of the market share for the hydraulic excavators and has manufacturing plants in Dharwad and Kharagpur. Tata Hitachi has developed strong relationships with Coal India (subsidiaries) and its estimated revenues of USD 450-550 Million offer a stable recurring revenue base.

- Caterpillar India (CIL) is based at its Thiruvallur manufacturing base and has a good market share in premium mining and large construction application markets. The estimated USD 750-950 million in revenues represents their share of the overall market, which is 10-12%, but is much higher in terms of value share, with premium pricing. Caterpillar's large excavators, motor graders and mining dump trucks top the list among large machines that are especially well-liked in large mining operations.

- BEML Limited is in a unique position in this field being the leading public sector organisation in India. BEML is the only local manufacturer of ultra-heavy mining machines in the 150-ton-plus range and is the lone supplier to government mining companies. They estimate their construction equipment division to bring in USD 420-520 million in revenue.

- Komatsu India offers good capabilities in mining equipment, whereas, Volvo CE India is more suited to the premium segment, L&T Construction Equipment is representing the domestic market and, the Chinese OEMs like SANY and XCMG are gaining aggressively in the standard equipment segments.

The USD 1.2 Billion Customer: Coal India's Equipment Empire

The annual capital expenditure of all subsidiaries of CIL is about USD 1.1-1.6 billion, which is around 14-16 % of the total market. The company has a vibrant heavy equipment fleet of over 40,000 units and purchases 3,500-4,500 units of new heavy equipment each year.

CIL's equipment needs are being accelerated rapidly, as its current production is 773 million tonnes and by 2027, the target is to reach 1 billion tonnes. To attain this target, an estimated 18,000 to 25,000 heavy machines are needed in the coming four years, which will result in continued high market demand through the early 2020s and beyond.

Each of CIL's subsidiaries is a large customer for equipment itself. SECEF is aiming for 170-180 million tonnes of procurement annually valued at USD 180-220 million. Mahanadi Coalfields plans on targeting 160-170 million tonnes and expects to spend USD 160-190 on equipment. The country's mining demand is consistently strong with the Northern Coalfields, Central Coalfields, Western Coalfields and others providing significant equipment demand.

Infrastructure Megaprojects: The Silent Demand Multipliers

- Bharatmala Pariyojana is India's flagship highway development program to build 34,800 km of economic corridors across the country for a total investment of USD 127.7 billion. Bharatmala involves about 50,000-60,000 machines in earth-moving activities throughout the country during peak periods of construction.

- To make this point clear, there are 15-20 motor graders, 25-35 hydraulic excavators, 40-50 backhoe-loaders, 20-25 compactors and 60-80 dump trucks for 100 km of highway construction. The total of equipment needs throughout the entire 34,800 km program is between 55,000 and 73,000, which is why highway construction makes up 24-26% of the total market demand.

- PM Gati Shakti and Dedicated Freight Corridors. The 3,300 km combined length of the two Dedicated Freight Corridors, the Eastern and Western, will need dedicated heavy earthmoving equipment for railway embankment, tunnelling and grade separation works. Demand for equipment from railway infrastructure is estimated to be USD 900 million -1.3bn during the project's lifetime.

- The government's Jal Jeevan Mission of building pipelines and laying utilities in all districts for piped water access to 192 million rural households entails significant work of trenching. This program creates the demand for 12,000-15,000 more backhoe loaders and specialized trenching equipment in the country.

Manufacturing Ecosystem: India as a Global Production Hub

India has transformed itself from merely being an end market to become a global manufacturing and exporting hub for earthmoving machinery. This has been made possible by the success of Make in India programs and the creation of complex supply chains.

Manufacturing complexes have emerged in the vicinity of important industrial centers. In the case of Delhi NCR and Rajasthan, there are several factories of JCB along with several suppliers for different components. Some of the factories operating within the industrial complex of Pune include JCB, Volvo CE, SANY, Hyundai CE, and hydraulic component factories. Some of the factories present in Chennai and Tamil Nadu are that of Caterpillar, Komatsu, and precision components.

Indians have been able to localize their earth moving equipment up to 80-90% while localization in mining equipment has reached 60-70%. India currently exports around 25,000-30,000 units of earthmoving equipment every year, which earns an income of USD 1.8-2.3 billion from its exports that grow at a rate of 12-15% annually for the last five years.

Export destination of the products includes the Middle East, Africa, Southeast Asia, Latin America, and CIS nations.

Equipment Economics: The Business of Moving Earth

Understanding the costs and economics of using such equipment is necessary to gain insights into market forces and consumer psychology. The reason for varied costs is due to the diverse applications of the equipment as well as differences in quality among different models.

A 20-ton hydraulic excavator typically costs between USD 90,000-260,000 depending on brand, features, and application requirements. Backhoe loaders range from USD 32,000-95,000, while wheel loaders with 3-4 cubic meter buckets cost USD 70,000-230,000. Motor graders typically run USD 85,000-280,000, and 100-ton mining dump trucks range from USD 850,000-2.8 million. The largest 200-ton mining dump trucks can cost USD 2.8-7.0 million depending on configuration.

The special features of operating economics in India. Equipment usually runs 1,600-2,200 hours per year, as opposed to 2,500-3,000 hours in developed regions. The percentage that fuel costs take up of total operating expenses is significant at 45-55% which means the diesel price movements play a significant role in any contractor's profitability. Most purchases of equipment are financed at 9-13% interest rate, and the annual maintenance costs are generally 8-12% of the equipment purchase price with typical payback periods 5-8 years.

The rental market is growing at a dramatic rate; 13-15% per year and 40-45% of the active fleet. This mirrors the general trend of choosing asset-light business models by contractors, with daily rates of USD 18-30 for a backhoe loader, USD 34-50 for a 20-ton excavator and USD 54-84 for a motor grader.

Technology Revolution: From Iron to Intelligence

The Indian earthmoving industry faces a transformational technology revolution, one that is not only redefining the machines' performance, but also how they are managed and maintained. The change is occurring at a faster rate than many industry watchers had predicted.

The advent of telematics and fleet management have become commonplace and are not considered a premium feature. More than 70-75% of the major manufacturer new equipment now comes with a factory-installed telematics system that allows for real-time location tracking, fuel monitoring, predictive maintenance messages, and operator behavior tracking. The aftermarket services market is expected to grow to USD 280-350 million by 2028 due to telematics.

The drive for emission standards transitions has resulted in major technological upgrades. Up to 6-10% more efficient advanced engine technologies have boosted fuel efficiency and implementation of CEV Stage V emission norms has added 8-12% to the upfront cost of equipment. This shift also has helped spur the retirement of ageing and outdated equipment, further contributing to the demand for new equipment.

Electric and alternative fuel equipment is still in its infancy but is gaining traction. Electric earthmoving equipment is less than 1% of new sales now but is expected to increase to 4-7% of sales by 2030, mainly in urban applications where charging infrastructure is more readily available.

Features are moving into the premium market segment, both stand-alone and semi-autonomous. Coal India has trialed autonomous haulage at some of its mines and semi-autonomous modes such as auto-dig and collision avoidance are becoming part of the specs for high-end machinery. The path towards full autonomy in Indian conditions is still 6-8 years away because of the issues of mixed fleet operations and changing regulatory landscape.

Market Challenges and Competitive Pressures

The sector has strong growth in drivers but is grappling with some structural issues that need careful navigation.

The volatility of demand is still a feature of cyclical demand. The government expenditure pattern, the effects of the election and the monsoon-related effects on construction activities are both significant and sensitive to equipment demand. Equipment utilization rates and decisions on the level of capital expenditure by contractors are both greatly impacted by delays in projects and the length of payment periods.

Most buyers are impacted by financing constraints. The bulk of equipment purchasers (around 70-75%) are small-to-medium contractors who have weak balance sheets. The NBFC credit tightening and higher interest rates directly affect the availability of equipment financing, especially for small-size operators.

The Chinese equipment competition is heating up in all the standard categories. In general construction, the prices of some manufacturers such as SANY, XCMG, LiuGong and Shantui are 20-35% lower than the established brands. In cases of critical mining equipment, quality and service issues are restricting the market share of Chinese equipment, but its ability to take market share in areas of price sensitivity is starting to be significant.

Supply chain vulnerability is due to import dependency of critical components. Acquisition costs of hydraulic components and electronic control systems are sensitive to currency fluctuations and global supply disruptions as around 60-70% of hydraulic components and 45-55% of electronic control systems are imported in India.

Government Policy Tailwinds

The policy environment strongly supports market growth through multiple structural initiatives.

The process of liberalization of the mining industry via the Mines and Minerals Amendment Act, 2021 brought about privatization of coal mining and auctioning of more than 50+ coal blocks that need investments ranging between USD 100 – 200 million in equipment to achieve operational capacity. The Critical Minerals Mission, which focuses on lithium and rare earth elements, will result in increased equipment needs for previously untouched geography.

Make in India initiatives push for local content laws, where the requirement of local content ranges from 50%. This benefits both Indian companies and MNCs with an extensive manufacturing footprint in India.

Increased infrastructure spending through the National Infrastructure Pipeline and Green Hydrogen Mission leads to emergence of new equipment demands that did not even exist a few years ago.

The Road to 2030: What the Next Phase Looks Like

India Earthmoving & Mining Equipment Market is set to experience continuous growth fueled by the country’s structural economic change rather than cyclical factors. A combination of infrastructure spending, mining sector reforms, technological advancements, and localization of production results in entirely new fundamentals compared to past growth periods.

Market evolution shows steady progression from the current USD 7.4 billion market size to USD 8.1 billion by 2025 owing to the construction peak of Bharatmala and the rapid growth in Coal India projects. The market is expected to be worth USD 8.8 billion by 2026 on account of a boost in private mining activities along with metro projects. This trend will continue up to USD 9.6 billion by 2027 due to investments in green hydrogen technologies. The market is forecast to be worth USD 10.5 billion by 2028 and USD 11.4 billion in 2029, followed by USD 12.4 billion by 2030.

Companies that are likely to be successful would have certain commonalities: strong localization manufacturing capability coupled with efficient costs, wide-ranging service networks capable of serving rural areas, technical competence that involves both telematics and automation, financing solutions involving small contractors, and export strategy based on India's manufacturing strengths.