Pharma Industry Faces Legal Precedents, Privacy Crackdowns, and Digital Transformation Wave

Author:

Intellectual Market Insights Research

Published Date:

07 Apr 2026

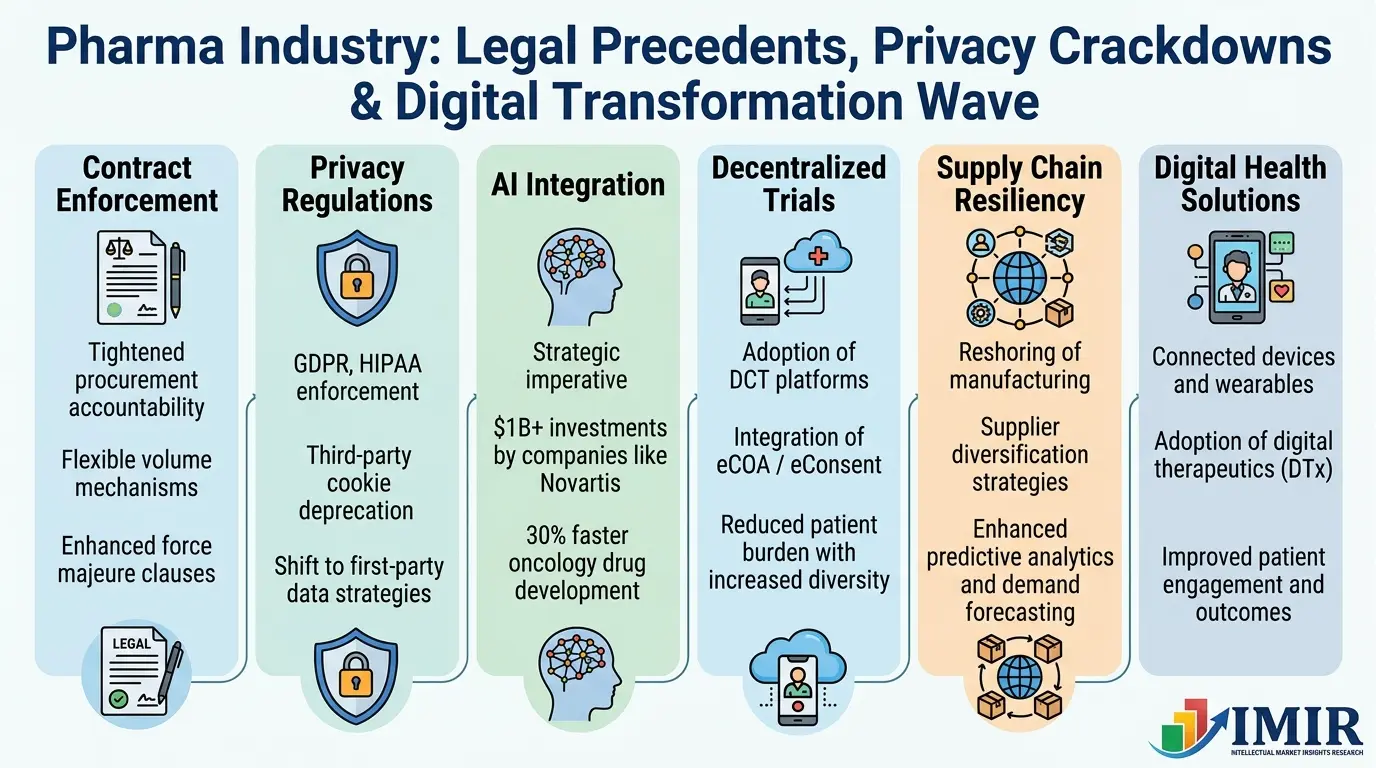

Contract Trends To Enforcement Tighten Procurement Accountability.

The legal professionals are following the new trends in the enforcement of pharmaceutical contracts, especially with respect to the government procurement relationships that are formed in case of emergencies. The recent legal trends indicate that courts are becoming less prone to finding extraordinary circumstances to strike down binding commercial contracts even where the public health conditions cause unforeseen demand shifts.

This legal interpretation has seen drug manufacturers come up with more intricate contract frameworks that would strike a balance between the risk management and the security of supply promises. Businesses are adopting flexible volume mechanisms, improved force majeure provisions, and risk-sharing guarantees that are aimed at safeguarding both the sides as well as securing consistent supply access in the event of health emergencies.

Government procurement departments across the globe are updating their contracting models to reflect the experience of the pandemic-related procurement issues, and are creating contracts that are more balanced and provide security in supply but control the fiscal cost.

Privacy Rules Destroy the Traditional Digital Marketing.

The marketing activities of the pharmaceutical industry are undergoing a complete change with the world privacy laws limiting the customary ways of digital interaction. The implementation of GDPR in Europe, changing HIPAA interpretations in the United States, and the use of cookies by third-party services in large digital platforms have all erased the marketing tools that the industry used to communicate with healthcare professionals and patients.

Firms are retaliating by establishing advanced first-party data approaches and spending a lot on proprietary digital ecosystems. Broad-based digital advertising is being supplanted by patient support applications, healthcare professional portals, and educational content platforms as the main tool of brand engagement.

Top pharmaceutical marketers say that these privacy-friendly strategies are enhancing the quality of engagement and creating a better brand trust than earlier mass-based digital advertisement practices. The transition will however involve massive initial investment in technology infrastructure, data analytics capabilities and content development resources.

Artificial Intelligence goes strategic in all operations.

The application of artificial intelligence in all aspects of pharmaceutical operations has moved beyond experimental programs to become an essential part of business infrastructure. Firms indicate that AI applications are now used in drug discovery, optimization of clinical trials, control in manufacturing processes, supply chain management and preparation of regulatory submissions.

The deployment of AI has become a strategic requirement instead of an optional improvement. Big pharma are setting up specific AI research divisions, buying specialty technology companies and partnering with major AI developers. The partnerships of Roche and AI in oncology drug development have been cited to shorten timelines of developing a drug by an average of 30 years and Novartis has formed AI research departments that have a dedicated investment of over 1 billion dollars.

The implications of AI integration on the workforce are not as obvious as they seem. Although automation is abolishing some of the traditional jobs, businesses are also introducing new jobs that demand specific skills in data science, machine learning, and computational biology, which leads to change in the workforce, not to its total elimination.

Restructuring in the Industry is a reflection of strategic reorientation.

The pharmaceutical industry is undertaking major organizational restructuring programs in an attempt to streamline operations in response to market changes across the globe. These fluctuations indicate reaction to the reforms in pricing, patent cliff and regulatory complexity and huge capital demand to develop technologies.

The most common types of restructuring include the consolidation of manufacturing processes, streamlining of commercial organizations, and refocusing research on high-value therapeutic areas. Firms are selling non-core businesses and making large investments in biologics, gene therapies, and precision medicine technologies with better growth opportunities.

By 2024, merger and acquisition activity had been more than $200 billion worldwide, as the trend towards consolidation under pressure of patent cliffs and capital requirements to support advanced technology integration. Alliances are becoming as significant as direct takeovers, and firms are entering into strategic alliances to distribute the risks of development and to eliminate the difficulties of complementary capabilities.

The complexity of regulatory compliance is at the new level.

In the leading pharmaceutical markets, regulatory requirements are growing in size and complexity in parallel. The Real-World Evidence programs and European Medicines Agency adaptive pathways initiatives allow companies with advanced data solutions opportunities as well as increase the regulatory engagement requirements throughout the industry.

The environmental, social and governance requirements are gaining greater prominence in both regulatory frameworks and commercial assessment by institutional investors. Business organizations are increasingly under pressure to show sustainable production, ethical clinical trial operations, and initiatives to provide equitable access to patients.

Business Models are developing in the direction of value integration.

The commercial paradigm of the pharmaceutical industry is radically shifting in the direction of the value-based model, which focuses on the measurement of outcomes, patient support, and integration into the healthcare system. The old-fashioned approach to selling in volumes yields to advanced relationships with the healthcare providers that link the success of pharmaceutical companies to patient outcomes and cost management goals of healthcare.

Combinations and digital therapeutics are developing new business opportunities, but may necessitate more sophisticated regulatory and reimbursement approaches. Firms that create such new methods have to maneuver through complicated approval processes as they establish a market preference of new treatment methods that involve the use of digital health technologies with conventional pharmaceuticals.

Market Impact Analysis: Structural Transformation Accelerates Industry Evolution

The intersection of the suggested policy frameworks, legal accountability tendencies, enforcement of privacy regulations, and integration of artificial intelligence is causing fundamental structural changes that will permanently alter the competitive patterns the world pharmaceutical market.

Integration of Technology Becomes Key Competitive Differentiator.

The trend towards market consolidation seems to gain momentum with firms attempting to gain the scale that will allow them to cope with the growing complexity of their operations and the financial demands of technology integration. Strong balance sheets, AI development, and geographic diversification will allow organizations to take a leading role in market share acquisition by means of organic growth and strategic acquisition.

The presence of competitive data capabilities, AI integration, and regulatory expertise is proving to be more evident. Those companies that are effectively investing in these areas and remain operational in an efficient manner are creating a sustainable differentiation where the conventional aspects of competition are being commoditized.

Geographic Redistribution of Manufacturing Competitively.

Diversification of the supply chain and investment in domestic manufacturing is a structural change not an episodic policy reaction. The pandemic experiences have demonstrated the business case of supply chain resiliency, and businesses are making long-term investments that will transform the geography of pharmaceutical manufacturing globally over the next decade.

Such developments present business prospects to nations and nations with competitive production conditions, human resource, and favorable regulatory systems. The world of pharmaceutical manufacturing will also be less concentrated in one geographic area and thus will be more distributed and resilient and this will fundamentally change the trade patterns and competitive positioning on a global basis.

The future of the pharmaceutical industry will be characterized by those organizations that will be able to manage this complicated transition without losing sight of creating and delivering life-saving treatment to those in need around the globe. Firms that are able to implement the changes in these structures fast without losing innovation focus and operational excellence will be seen as powerhouses in a more competitive and technologically advanced global market.