Share this link via:

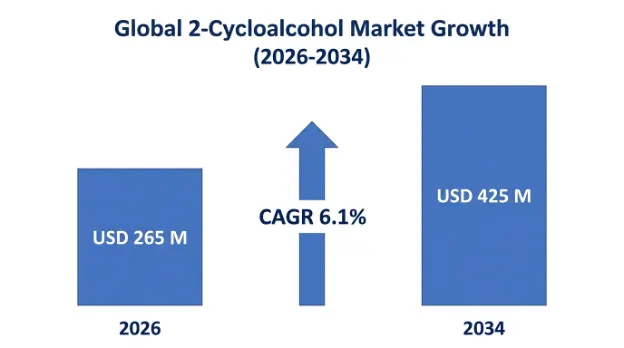

The global 2-cycloalcohol market was valued at USD 245 million in 2025 and is projected to reach USD 265 million in 2026, expanding to USD 425 million by 2034, growing at a CAGR of 6.1% during the forecast period (2026-2034).

2-cycloalcohols are a special class of cyclic secondary alcohols in which a a hydroxyl functional group is found on the second carbon position of saturated or partly unsaturated carbocyclic ring systems. The class of chemicals includes commercially important 2-cyclohexanol, 2-cyclopentanol, 2-methylcyclohexanol and 2-cyclohexen-1-ol, all of which are used across various applications as versatile synthetic intermediates, chiral building blocks, and precursors in specialty chemistry in pharmaceutical, agrochemical and fragrance sectors. The stereochemistry and conformation of the hydroxyl group at the 2-carbon are unique and different from those at the 1-position and from linear alcohol analogs.

The commercial value of 2-cycloalcohols is mainly related to their use as intermediates in the pharmaceutical industry, where the cyclic structure with the presence of secondary alcohol groups allows very selective transformations, such as oxidation to the corresponding ketone, esterification reactions, etherification reactions, and asymmetric functionalization reactions, which are necessary for the synthesis of complex active pharmaceutical ingredients. The cycloalcohol scaffold has been frequently encountered in biologically active molecules such as prostaglandin analogs in the field of ophthalmology and obstetrics, antiviral nucleoside derivatives and central nervous system therapeutics for which conformational rigidity improves selectivity and metabolic stability.

The derivatives of 2-cycloalcohols are key raw materials for fragrance and flavor chemistry, where they are used to create synthetic 2-cycloalcohol derivatives which are used as replacements for valuable essential oils from natural sources. Indeed, synthetic sandalwood products such as the compound 2-methylcyclohexanol represent critical intermediates in the production of synthetic sandalwood, meeting the demand for sandalwood in cosmetics and personal care products made by global manufacturers that have been hampered by the availability of natural sandalwood from endangered forests.

The synthesis of 2-cycloalcohols is complex, as it involves sophisticated catalytic transformations such as selective hydrogenation of the corresponding cyclic ketones or alkenes, hydroboration-oxidation sequences and stereoselective reduction reactions require careful control of the reaction conditions to achieve the desired stereoisomeric ratios and purity levels. Production is generally carried out in large specialty chemical manufacturing facilities in plants that feature multipurpose reactors and specific purification systems as well as quality control support systems to comply with pharmaceutical-grade requirements, such as ICH Good Manufacturing Practice standards.

The expansion of the market is driven by an increase in investment in pharmaceutical research on structurally complex small molecules, rising demand for sustainable fragrance ingredients and increasing use of 2-cycloalcohol-derived building blocks in agrochemical production due to the more selective and environmentally friendly active ingredients preferred by regulatory authorities. The special characteristic of these compounds is reflected in the generally moderate volume growth, but relatively inelastic demand pattern associated with specific downstream applications, which gives these compounds relatively stable pricing.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 245 Million |

| Forecast Value | USD 425 Million |

| CAGR | 6.1% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Europe |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Purity Grade, Application, End-User Industry, Distribution Channel, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Spain, Italy, Netherlands, Russia, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | BASF SE, Merck KGaA, Evonik Industries, Tokyo Chemical Industry, Thermo Fisher Scientific, Symrise AG, Solvay S.A. |

Get more details on this report - Request Free Sample

Expanding Pharmaceutical Intermediate Demand and Complex API Manufacturing Growth

The key structural stimuli fueling the 2-cycloalcohol market growth are a continued increase in pharmaceutical manufacturing applications that demand structurally complex synthetic intermediates, along with therapeutic applications requiring cyclic alcohol scaffolds for their conformational rigidity and stereochemical control. The cyclopentane ring system is the core structure of prostaglandin analogs, and the 2-cyclopentanol-based building block is in demand for this application in the global pharmaceutical industry for more sophisticated small molecule drugs containing the cycloaliphatic structural elements.

Prostaglandin therapeutics are a very prominent application area, and the global prostaglandin analog market is projected to grow to more than USD 4.8 billion by 2025, in used in ophthalmology, obstetrics, and gastroenterology. Synthetic routes such as cyclopentanol derivatives have been used for some key commercial products such as Verify intended drug names; likely erroneous terminology (for glaucoma) and inopportune (for induction of labor). As several major branded prostaglandin products are approaching patent expiration, it is signifying generic pharmaceutical production growth, especially in India and China, thus ensuring continuous demand for 2-cyclopentanol intermediates used in the manufacture of these drugs.

The antiviral drug manufacturing sector also generates additional demand to produce the carbocyclic nucleosides, which are precursors to produce HIV antiretroviral drugs and other antiviral drugs containing cycloaliphatic sugar mimetics. The continually increasing global market for HIV treatment and the emerging pipeline for novel antiviral drugs for hepatitis B, herpesvirus, and new infections consistently demands high purity cycloalcohol intermediates with strict pharmaceutical quality requirements.

The second biggest 2-cycloalcohols market is the fragrance and flavor sector, which mainly utilizes 2-methylcyclohexanol and its derivatives in the synthesis of woody perfumes. With the growth of the worldwide synthetic perfume industry, because there is a rising reliance on cosmetics, personal grooming and household items, there continues to be strong demand for 2-cycloalcohol-derived scent compounds that replicate expensive or tightly regulated natural materials.

The most important use is the synthetic production of sandalwood, where 2-methylcyclohexanol is an important intermediate in the production of sandalwood fragrance compounds that are sustainable alternatives to natural sandalwood oil from Santalum species found in endangered forests. However, with the diminishing natural supply of sandalwood and growing regulatory limitations on sandalwood harvesting, the use of synthetic alternatives has become crucial for ensuring a reliable supply chain for the USD 6.2 billion global fragrance market.

The technical benefits of 2-cycloalcohol-derived fragrances are excellent batch-to-batch uniformity, good chemical stability during formulation, and reduced formulation costs compared to natural extracts, which may not be economically viable for mass-market personal care products due to price sensitivity. of these products. Commercial fragrance companies have developed proprietary synthetic pathways that rely on 2-cycloalcohol isomers for distinct fragrance notes that give them the edge in applications to consumer products.

Technical challenges and high capital costs associated with manufacturing processes to produce pharmaceutical and fragrance grade 2-cycloalcohol materials required to meet stringent purity and stereoisomer specifications are the biggest constraints to market expansion. Multi-step catalytic synthetic processes with various stereoselective hydrogenation, chromatographic separation of stereoisomers and intricate purification steps are often required to obtain the >99% purity levels that are necessary for pharmaceutical applications of the synthesis of specific 2-cycloalcohol isomers.

For example, the production of pharmaceutical-grade 2-cyclopentanol often require catalytic hydrogenation of 2-cyclopentenone using specific chiral catalysts and/or enzymatic reduction methods followed by purification processes such as fractional distillation and crystallization to achieve the desired enantiomeric excess. These processes demand high capital expenditures on specialized reactors, separation equipment and analytical instruments, which are barriers to entry for smaller manufacturers and ensure that premium pricing structures are in place that limit the range of applications in which these compounds can be used.

Environmental and safety regulations for hydrogen gas, organic solvents and catalytic materials bring extra costs and operating restrictions, especially for small-scale hydrogen production units without a complete environmental management system. The waste streams created during purification processes must be treated and the volatile organic compounds (VOCs) emitted must be abated using advanced abatement systems that add to the total production costs.

The structural supply chain risk primarily arises from geographic concentration of production capacity and a dependence on certain petrochemical feedstocks as the raw material, thereby reducing supply chain flexibility. Most of the commercial-scale 2-cycloalcohol production is in Europe and Asia, and only a few manufacturers around the world have the technical expertise and regulatory compliance systems to produce 2-cycloalcohol on a pharmaceutical scale.

The concentration of this supply opens the door to single-source dependency risks for pharmaceutical companies who need to have reliable supplies of their intermediates to continue the production of their APIs and reduce competitive pricing pressure which could have a wider impact on market uptake. High purity 2-cycloalcohol grades are also very specialized and have added vulnerabilities in the supply chain, with alternative suppliers needing to go through lengthy qualification processes that can take 12-18 months to complete, such as analytical method validation, impurity profiling and regulatory documentation.

The market opportunity for developing and commercializing environmentally friendly production processes for 2-cycloalcohols using biocatalytic methods, renewable raw materials and green chemistry principles to meet the increasing commitments of the pharmaceutical and specialty chemicals industry in the field of sustainability. Engineered ADHs can be used for enzymatic reduction of cyclic ketones to obtain high stereoselectivity with mild reaction conditions, which can avoid dangerous chemicals and save energy during the traditional chemical synthesis process.

The growing attention on green chemistry metrics such as atom economy, solvent consumption, and waste generation in the pharmaceutical sector provides market potential for manufacturers of cleaner processes to produce 2-cycloalcohol. If a company can bring a product to market that is produced using a "biocatalytic" process or feed that is renewable, charge a premium price to customers who have sustainability requirements and differentiate themselves from competitors offering petrochemical-derived products. that is derived from petrochemicals.

Another important opportunity for process intensification and cost reduction in the manufacture of 2-cycloalcohol is continuous flow chemistry applications. The flow chemistry platforms can facilitate fine-tuning reaction conditions, better heat and mass transfer and better safety in hydrogenation reactions to lower production costs, while maintaining product quality consistency for pharmaceutical production.

New opportunities for specialized 2-cycloalcohol derivatives needed for specific synthetic chemistry demands in drug discovery programs are afforded by the growing pharmaceutical pipeline investigating novel therapeutic targets. Growing demands for personalized medicine strategies and orphan drug development require unique cycloalcohol building blocks, which cannot be easily obtained commercially.

Custom 2-cycloalcohol synthesis has high value market applications such as contract research organizations and pharmaceutical companies that are working on complex natural product analogs, novel prostaglandin derivatives, and structurally sophisticated central nervous system therapeutics. The ability to supply development scale quantities with complete analytical characterization and regulatory documentation is of competitive value for specialty chemical suppliers to pharmaceutical research applications.

The 2-cycloalcohol manufacturing industry is witnessing gradual adoption of digital solutions such as process analytical technology, advanced process control systems and predictive maintenance platforms that enhance production efficiency and improve product quality consistency. During catalytic hydrogenation and purification processes, critical process parameters can be monitored in real time allowing optimization of yield and selectivity, while minimizing the variability of each batch, which can affect pharmaceutical customers with a requirement for consistent intermediate specification.

Machine learning algorithms are being used on historical production data to optimize the performance of catalysts, the efficiency of solvent recovery and purification conditions, thereby minimizing production costs and optimizing environmental factors (waste minimization, energy optimization). Digital technologies are especially beneficial for manufacturers with pharmaceutical customers where there is a need for detailed batch genealogy, process validation, and quality documentation.

The global pharmaceutical regulatory landscape continues to evolve, particularly regarding the requirements for chemical starting materials and those synthetic intermediates, they are changing, and it’s pushing a broader standardization of quality specifications and documentation needs, which directly impacts 2-cycloalcohol suppliers. When ICH Q7 is being implemented for active pharmaceutical ingredient manufacturing, there are more opportunities for suppliers who can handle the heightened quality system requirements.

Europe had the highest 2-cycloalcohol market share at USD 98 million in 2025, accounting for 40% of the global market value, due to its highly concentrated fragrance and flavor industry, the world's most advanced pharmaceutical research and development base, and well-established specialty chemical manufacturing capabilities. The top fragrance houses in Switzerland, Germany, and France are major consumers of 2-cycloalcohol derivatives for the manufacture of synthetic woody fragrances: Givaudan, Firmenich and Symrise.

The European pharmaceutical industry's emphasis is on complex small molecule development; this, coupled with Europe's fine chemical manufacturing prowess, provides a steady demand for high-purity 2-cycloalcohol intermediates. The severity of the REACH regulatory framework comes with its own price tag but also offers competitive protection for well-established European manufacturers that can produce full registration and safety documentation.

Asia Pacific is the fastest-growing regional market. With China and India being the dominant players in the global generic pharmaceutical manufacturing sector, the rise of their specialty chemical production capacity, and the increased investment in their domestic pharmaceutical research sector, the CAGR is estimated at 7.8% through 2034. The Indian pharmaceutical industry, the world's largest volume producer of generic drugs, is a heavy user of 2-cycloalcohol intermediates for the synthesis of prostaglandin analogs and other complex API.

The Chinese chemical industry growth also includes manufacturing capacity for specialty intermediates, with domestic companies successfully building capacity to export to both the international market and China's expanding domestic pharmaceutical and perfume sectors. Highly engineered 2-cycloalcohol derivatives are becoming increasingly popular in the Chinese drug discovery programs due to the government's support of pharmaceutical innovation and the growing contract research organization industry.

The global 2-cycloalcohol market has a moderate level of concentration and comprises a blend of specialty chemical manufacturers , pharmaceutical intermediate suppliers, and fine chemical firms competing across different purity ranges and application segments. BASF SE, Merck KGaA, and Evonik Industries rely on wide-ranging chemical collections, global production networks, and long standing pharmaceutical industry connections to keep their leading positions, especially in the higher purity pharmaceutical-grade slices.

More specialized fine chemical manufacturers like Tokyo Chemical Industry, Acros Organics, and certain regional custom synthesis firms go after research-grade and custom derivative niches. They do it via know-how, adaptable production capacity, and practical analytical support services. In addition, Asian suppliers, especially those from China and India, have gained meaningful market share in industrial-grade segments, and they are increasingly obtaining pharmaceutical-grade approvals by upgrading facilities and strengthening their quality system controls.

Competition primarily focuses on repeatable product quality, regulatory compliance know-how, hands-on technical support, and dependable supply chain execution, not only raw price pressure. This trend is attributable to since the market serves specialty uses in pharmaceutical and fragrance contexts, where product performance and regulatory compliance often matter more than pure cost.

March 2026: BASF SE announced the completion of an EUR 15 million expansion of its fine chemicals plant in Ludwigshafen, Germany thereby increasing pharmaceutical-grade 2-cycloalcohol output by about 25% to meet growing European pharmaceutical demand.

January 2026: Merck KGaA launched a fresh high-purity 2-cyclopentanol grade, the one they claim meets upgraded pharmaceutical requirements for prostaglandin analog synthesis, targeted primarily at generic drug manufacturers in emerging markets.

November 2025: Evonik Industries successfully scaled up a continuous flow method for 2-methylcyclohexanol manufacturing, achieving approximately a 15% increase in yield, along with an approximately 30% reduction in solvent consumption versus traditional batch handling.

September 2025: Tokyo Chemical Industry expanded its customized synthesis options for chiral 2-cycloalcohol derivatives, and established dedicated production lines for enantiopure material.

July 2025: An Indian manufacturer of pharmaceutical intermediates received US FDA facility qualification for 2-cyclopentanol production, so it can supply US-regulated pharmaceutical players thereby widening the competitive choices available to American drug companies.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

20 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.