Share this link via:

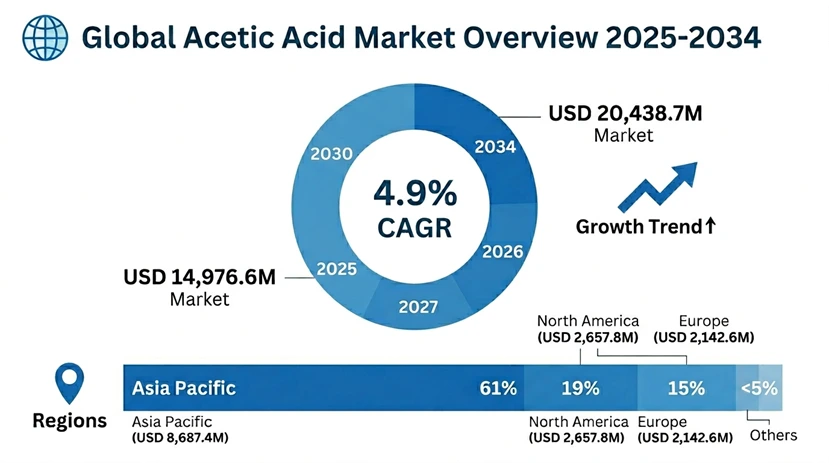

The global market size of acetic acid is estimated to be USD 14,287.6 million in 2025 and is expected to grow to USD 14,976.3 million in 2026 with a CAGR of 4.9% throughout the forecast period (2026-2034).

Acetic acid (systematically named ethanoic acid, molecular formula CH₃COOH) is one of the most vital commodity chemicals in the world industrial production and is a key building block to produce vinyl acetate monomer, purified terephthalic acid, acetic anhydride, and many acetate esters that are the basis of industrial production of plastics, textiles, coatings, adhesives, and This flexible carboxylic acid is at the boundary between conventional petrochemical production and new sustainable chemistry, acting as both a high-volume industrial intermediate and a platform chemical to the next generation bio-based and carbon utilization technologies.

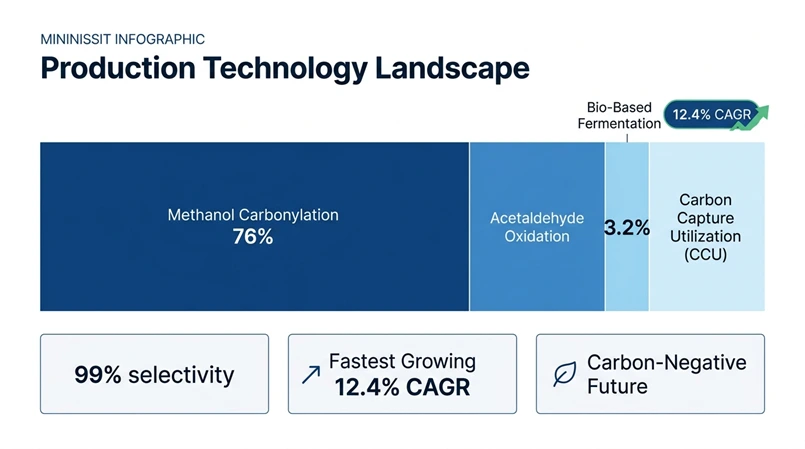

The industrial value of acetic acid is found literally in all major manufacturing industries, with about 65-70% of the total world production being used as chemical starting materials to the production of downstream products, and the remaining 30-35% found in direct use as a preservative, textile processing, pharmaceutical synthesis, and cleaning formulations. The most common contemporary process is the methanol carbonylation process, which consumes about 75% of the total world capacity, which reacts to methanol with carbon monoxide in the presence of rhodium or iridium catalysts to produce acetic acid with an extremely high selectivity of over 99% and a much higher energy efficiency than the old technologies of oxidation to acetaldehyde.

The market is undergoing fundamental change due to three converging forces: the structural growth in demand of polyester and packaging industries to use purified terephthalic acid and vinyl acetate monomer derivatives; the accelerated move towards sustainable production and supply chains using bio-based feedstocks and carbon capture technologies, and the strategic role of acetic acid in circular economy efforts, where it is used as a platform chemical to convert captured industrial carbon dioxide into valuable downstream chemicals and intermediates, thereby enhancing resource efficiency, reducing emissions, and supporting closed-loop industrial ecosystems.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 14,287.6 Million |

| Forecast Value | USD 20,438.7 Million |

| CAGR | 4.9% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2024 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Grade, By Derivative, By Application, By Production Technology, By End-User Industry |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Spain, Italy, Netherlands, China, Japan, India, South Korea, Taiwan, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Celanese Corporation, BP plc, Eastman Chemical Company, SABIC, LyondellBasell Industries, Jiangsu Sopo Chemical |

Get more details on this report - Request Free Sample

Structural Demand from Polyester Value Chain and Renewable Energy Applications

The main driving force behind the active growth of the acetic acid market is the long-term structural demand of the world polyester market, especially via purified terephthalic acid production that utilizes acetic acid as a solvent medium, as well as oxidation catalyst in the transformation of paraxylene to terephthalic acid. In 2024, the world output of polyester fiber was 58.4 million metric tons, 54% of the total textile fiber usage in the world and is expected to grow by 4.2-4.8% per annum through 2034 due to the need to satisfy demand in the fast-growing apparel sector in emerging markets, technical applications, and home furnishing consumption.

An average of 0.04-0.06 metric tons of acetic acid is used to produce a metric ton of PTA, and this means that the world requires 2.8-3.4 million metric tons of acetic acid each year to produce PTA. This is mainly consumed in built-in petrochemical complex whereby acetic acid is used as the reaction solvent to ensure the optimum oxidation conditions and the minimal formation of byproducts and effective recovery of crystallized terephthalic acid and the reaction mixture.

At the same time, the production of vinyl acetate monomer is the biggest single use of acetic acid, which consumes around 33-35% of the world production. The water-based construction adhesives, low-VOC paints and coatings and most importantly, ethylene vinyl acetate films employed in the encapsulation of solar panels are driving unprecedented growth in VAM demand. The world solar energy growth, which is growing by more than 400 GW per year, generates ultra-pure acetic acid to produce optical EVA films, which is used to cover photovoltaic cells to help them withstand the effects of the environment.

Key Performance Metrics:

In 2024-2025, Asia Pacific polyester production capacity grew by 4.8 million metric tons and this necessitated 192,000-288,000 metric tons of acetic acid consumed annually in PTA manufacturing activities. The increase in solar panel production in East Asia by 22% resulted in a direct correlation with the 450,000 metric ton feedstock increase in acetic acid required by the global solar photovoltaic industry in 2025 over the demand in 2023, necessitating an increase in the global acetic acid feedstock. Adhesive procurement using VAM in upcoming construction markets showed a growth of 7.8 times a year as compared to the previous year with water-based adhesive formulations replacing the solvent-based adhesive formulations in line with strict environmental rules. In the construction chemicals industry, 6.85 million metric tons of acetic acid is used in the form of VAM derivatives in 2025, which is the largest single demand stream and shows the strength of the market due to the diversified use of end-use.

Methanol Feedstock Volatility and Production Overcapacity Pressures

The greatest limitation, which impacts on the profitability of the acetic acid market, is the structural reliance on methanol as the main feedstock to the modern production plants, putting direct exposure to the volatility of natural gas prices and the dynamics of the methanol markets that often squeeze the production margins during the high feedstock prices. Methanol carbonylation processes use about 0.70-0.75 metric tons of methanol per metric ton of acetic acid produced that is, methanol costs are 45-60% of total variable production costs depending on the price of natural gas in a region and the balance of the supply and demand of methanol.

This feedstock sensitivity makes the economics difficult when the price of methanol rises at a rate higher than the rate of changes in the price of acetic acid contracts, especially in areas where production can be changed more slowly or in areas where there are long-term supply contracts that cannot be adjusted to alteration of prices. This would further be compounded in 2024-2025 as global methanol prices ranged between USD 280-520 per metric ton due to the volatility of natural gas prices, the economics of production of coal-to-methanol in China and the rate of capacity utilization at major methanol production plants.

Adding to this difficulty is the cyclical excess capacity in major producing areas, especially China, where a few large and integrated producers and state-owned units have ordered world-scale plants based on methanol carbonylation and other alternative routes that take effective global nameplate capacity far beyond global demand at different times of the cycle. This overcapacity, which is structural in form, is reflected in the fluctuation of prices in the global and regional contract and spot exchanges, reduced plant operating rates during downturns in the 70-80% range to marginal producers, and stiff competition among integrated players who also trade downstream products such as VAM and PTA.

Economic Challenge Metrics:

Industry analysis shows that the margins of production of acetic acid have narrowed between USD 185-240 per metric ton in Q1 2024 to USD 95-145 per metric ton in Q3 2024 when there was an increase in methanol spot prices by 42% and acetic acid contracts prices changed by 18% because of quarterly pricing and dynamics of the Spot methanol procurement European producers recorded negative contribution margins in 16 weeks of 2024, which necessitated production cuts amounting to 340,000 metric tons of lost production. In historical declines, acetic acid spot prices in Asia have decreased 20-30% in a year as fresh capacity enters a weak market, and Chinese capacity utilization decreases in response to oversupply periods, dropping to 84% to 71%. The tightening of environmental policy in China on coal-based chemistry and processes with high emissions has given some rationalization of capacity, but timing and implementation are unclear, posing strategic risk to both producers and downstream customers.

Bio-Based Production Pathways and Carbon Capture Utilization Technologies

The most radical change that is transforming the market of acetic acid is the creation and commercialization of carbon capture utilization technologies that transform industrial carbon dioxide emissions and renewable hydrogen into acetic acid utilizing electrochemical synthesis, biological fermentation, or thermochemical transformation pathways. These new production lines will have a two-fold value proposition: they will create carbon-negative or carbon-neutral acetic acid, which fetches sustainability premiums in the environmentally conscious markets, and at the same time will provide the industrial facilities with the economically feasible pathways of using carbon dioxide that will be able to provide revenues on waste streams that would otherwise need expensive disposal or release into the atmosphere.

Various technology routes have been piloted to demonstrate, such as anaerobic bacterial fermentation routes using acetogenic microorganisms that directly reduce carbon dioxide and water to acetic acid using renewable electricity with energy efficiencies of 45-58, and electrochemical reduction routes that directly convert carbon dioxide and water to acetic acid using renewable electricity with energy efficiencies of 45-55 These technologies place the use of acetic acid as a strategic element of industrial carbon management policies, which creates a chance of generating carbon credit revenues whilst generating commodity chemicals.

The market segmentation is not confined to new production technologies but includes higher product placement of bio-based acetic acid in food, pharmaceuticals, and personal care products where consumers and regulatory authorities are turning more towards sustainable ingredients. In such uses, bio-based acetic acid produced by fermentation of agricultural waste or by using carbon dioxide can fetch a price premium of 15-35% above conventional products based on petrochemicals, and at the same time, gain renewable content credits, carbon reduction incentives, and sustainable chemistry certifications.

Opportunity Metrics:

The market size of carbon capture utilization and storage will be USD 7.8 billion in 2030, and acetic acid production will comprise 8-12% of all potential carbon dioxide utilization applications, which will be equivalent to USD 624-936 million of addressable market opportunity. Bio-based and low-carbon volumes of acetic acids will experience a high single- to low-digit CAGR, compared to current small base volumes, and outpacing the market. Initial business agreements indicate that certified bio-based or low-carbon acetic acid will have 10-25% above conventional product price points, especially in applications to food/pharmaceutical and branded consumer goods. Regulatory frameworks in the European Union such as the Renewable Energy Directive II provide economic incentives, on a metric ton of CO₂ equivalent per unit of bio-based chemical production, between EUR 85-140, enhancing the economic competitiveness of carbon utilization pathways as compared to conventional production processes.

Integrated Petrochemical Complex Optimization and Supply Chain Localization

One of the fundamental changes that have taken place in the acetic acid industry is the strategic positioning of production facilities in large-scale petrochemical complexes that maximize the use of carbon in multi-chemical value chains, specifically via C1 chemistry platforms that convert methane, methanol, and carbon monoxide to a wide range of chemical products such as acetic acid, formaldehyde, methyl methacrylate, and downstream This integration approach maximizes the efficiency of feedstock utilization, minimizes the waste streams, achieves the economies of scale in utility systems and infrastructure, and offers flexibility in operations to switch production between products in response to the relative market economics.

The latest integrated complexes use high intensity processes of process intensification such as reactive distillation systems, which integrate acetic acid production and purification in single unit operations, saving capital costs 28-35% and energy usage 18-24% over traditional separated reaction and distillation systems. These plants have a net carbon efficiency of 94-97% (i.e. 94-97% of carbon atoms in feedstock methanol found in saleable acetic acid product with the rest of the carbon captured in byproduct streams or converted to carbon dioxide that can be recycled to methanol synthesis units in closed loops).

The trend of integration is also applied in the so-called hyper-localization of supply chains, in which organizations are building integrated acetyls complexes nearer to consumption centers, instead of global shipping via the traditional production centers. This removes the movement of dangerous acetic acid over long routes, enhances energy efficiency by integrating heat, and protects producers against the impact of freight rates and shipping emission taxes, like the EU ETS expansion to sea transport.

Trend Performance Metrics:

Integrated acetyls complexes were also projected to have 4-6% higher operation margins than non-integrated standalone producers in 2025, mostly because of logistics savings of USD 40-60 per metric ton and utility infrastructure sharing. In 2025, there was a 3.5% year-on-year decline in the volume of acetic acid traded through deep-sea shipping, although aggregate demand grew, and captive consumption within integrated facilities was on the rise, by 6.2%. The capital intensity per metric ton of capacity of Chinese petrochemical complexes commissioned in 2023-2025 is 15-20 lower than that of standalone facilities due to integration of acetic acid production with methanol, formaldehyde, and the production of downstream derivatives. According to industry analysis, integrated facilities have a 12.4-16.8% ROI on invested capital versus 8.2-11.3% of standalone acetic acid plants due to better economies of scale, lower logistics expenses, and operational flexibility that facilitates production maximization through a variety of product streams.

Asia Pacific: Leadership in the Market and Production.

Asia Pacific had the biggest market share of USD 8,687.4 million in 2025 at 61% of global market value with a forecasted CAGR of 5.4 in 2034. The huge market domination in the region is indicative of the high concentration of the polyester industry, high levels of manufacturing of vinyl acetate monomers that serve the construction industry and the automotive industry, the presence of large quantities of methanol feedstock due to coal gasification plants and the built in complex development of petrochemicals that maximize production economies of scale and integration.

China has 68% and 52% market value in the region and 11.8 million metric tons per year production capacity of acetic acid covering about half of the global capacity respectively, as of 2025. In 2024-2025, Chinese production capacity increased by 1.2 million metric tons with new facility commissioning and capacity debottlenecking projects, due to the growth of domestic polyester industry that used 4.8 million metric tons of acetic acid per year to make PTA and demand of 2.1 million metric tons of vinyl acetate monomer to use in adhesive, coating, and text

The Chinese market enjoys the advantage of vertically integrated value chains of coal-to-chemicals where the coal gasification results into the production of syngas that is used in the production of methanol which in turn feeds into the production of acetic acid through the carbonylation processes thus creating a cost advantage of USD 85-140 per metric ton against other regions that use natural gas-based methanol production routes. Nevertheless, the volatility of supply through the dual control energy policies of China has led to the lack of effective capacity utilization globally by 4.2% as regulatory shutdowns in heavy-industry regions have lowered the utilization of effective capacity in 2025.

Regional Performance Indicators:

The market of acetic acid in India is expected to reach USD 847.3 million in 2025, with a 6.2% CAGR until 2034 due to the growth of the textile industry, the demand of the acetic acid in the pharmaceutical intermediate and food processing sector. The Indian production is equal to 840,000 metric tons per year, domestic demand is equal to 720,000 metric tons per year and 180,000220,000 metric tons of imports are necessary every year. The Japanese market has a mature nature with a 2.8% CAGR forecast as it has a market of USD 623.8 million with high-purity specialty grade production used in the pharmaceutical and electronic chemical market. The Southeast Asian countries have a collective market value of 18% of the region and Vietnam is the most rapidly expanding market with 7.8% CAGR, propelled by foreign direct investment in textile production and electronics assembly services.

North America: Technology Leadership and Cost Advantages.

In 2025, North America had USD 2,657.8 million market value with forecasted 3.9% CAGR through 2034 based on sophisticated production technologies, high levels of vertical integration in petrochemical complexes, presence of natural gas feedstock to provide competitive methanol production economics, and diversified demand in chemical intermediates, food processing, and pharmaceutical uses. The location has the advantage of having an established infrastructure linking natural gas production, methanol production, and acetic acid production in co-located Gulf Coast petrochemical corridors.

The United States has 86% of the North American market share amounting to USD 2,285.7 million and production capacity of 2.1 million metric tons per year in Texas and Louisiana plants. The US Gulf Coast production plants enjoy cash costs of USD 285-340 per metric ton, which take advantage of natural gas prices of USD 2.80-3.40 per MMBtu that support competitive economics of methanol production. The region is also forefront in the use of carbon capture technologies with two large-scale facilities declaring retrofit programs to draw in CO₂ to make methanol.

In 2025, US acetic acid exports grew 4.1%, and it took advantage of the curtailment of production in Europe due to high energy prices, which made the US a pivotal export center to serve deficit markets in South America and Europe. High value applications are also high in domestic consumption with 31% used in the production of vinyl acetate monomers, 24% used in the production of acetate esters to be used as solvents, 19% used in food and beverage applications, and 26% used in pharmaceutical synthesis and industrial applications.

Europe: Regulatory Leadership and Sustainability Focus.

Europe retained USD 2,142.6 million market worth in 2025 with an estimated 3.4% CAGR until 2034, high-quality criteria, advanced environmental laws, high purity specialty grade manufacturing, and new bio-based manufacturing endeavors to meet the aims of the circular economy. The region has structural issues such as high costs of natural gas impacting the economics of methanol feedstock, low growth in production capacity, and growing competition in imports by the Middle Eastern and Asian producers.

The average cost of producing acetic acid in Europe is USD 445-520 per metric ton, which represents high natural gas prices and high environmental compliance costs of EUR 18-28 per metric ton due to emissions monitoring, waste treatment and regulatory reporting requirements. In 2025, the capacity utilization of the region was 76% against 82% in 2022-2023, which can be explained by the presence of competitive pressure on the imports and the lack of demand in the construction-related applications.

But Europe is at the forefront of sustainability efforts, and by 2025 the European market is projected to see 12% growth in demand of the so-called Green Acetic Acid certificates. The Carbon Border Adjustment and the REACH rules are technically establishing price floors that prefer domestic production or imports based on decarbonized facilities. In 2024-2026 European Commission funding programs provided EUR 240 million to carbon capture utilization projects such as the production of acetic acid using CO2 industrial emissions.

Middle East & Africa and Latin America: New Growth Markets.

Middle East & Africa continued to have USD 943.2 million market value in 2025 with an estimated 5.8% CAGR until 2034 due to the availability of hydrocarbon feedstock, increasing construction and automobile industries, and strategic orientation to downstream petrochemical value-added products. The region also takes advantage of cheap natural gas prices to establish integrated petrochemical complexes such as the production of acetic acid to be used domestically and to export to the markets.

Latin America USD 856.7 million in market value in 2025 with a forecasted 4.3% CAGR through 2034 due to growing middle-class consumption, packaged food and beverages, growing textile industry and increased construction and automotive use of acetic acid derivatives. The region is still partially import-reliant but shows increased interest in regional investment in chemicals to enhance supply security.

Glacial Acetic Acid has the highest market share with USD 10,287.1 million, the highest-purity anhydrous acetic acid with a minimum of 99.5% content acetic acid in 2025. The grade finds use in chemical synthesis processes that need high precision in stoichiometry, such as the production of vinyl acetate monomers, acetate ester synthesis, and pharmaceutical intermediate synthesis.

Vinyl Acetate Monomer Production is the leader of consumption applications with USD 4,715.3 million in 2025, which is 33% of the overall acetic acid consumption. The production of VAM needs about 0.58-0.62 metric tons of acetic acid per metric ton of VAM output, and worldwide production of VAM is 7.8 million metric tons in 2024, used in the manufacturing of adhesives, finishes, fabrics, and encapsulation films on solar panels.

PTA/PET Manufacturing makes up 28% of market value at USD 4,000.6 million in 2025, the quickest developing derivative application with 5.6% CAGR forecast up to 2034. The PTA manufacturing processes use both acetic acid as a reaction solvent and catalyst and worldwide PTA capacity of 78.4 million metric tons a year needs 3.1-4.7 million metric tons of acetic acid usage.

Food Grade Acetic Acid is high market segment worth USD 1,714.4 million in 2025, with price differentials of 35-55% above technical grades based on purity requirements and regulatory mandatory requirements of food preservation, pH adjustment, and flavor enhancement usage.

Methanol Carbonylation is the leading technology (76% market share) that feeds on rhodium or iridium catalyst at 150-200 C and 30-60 bars and yields acetic acid selectivity over 99%. The newer processes of carbonylation use sophisticated catalysts systems that allow the operation to be carried out at lower pressures and temperatures but still achieve productivity of 15-20 metric tons per cubic meter of reactor volume per hour.

Bio-Based Fermentation is the most rapidly developing technology of production with 12.4% CAGR projections over the next 3 years, yet with only 3.2% of the world production volume today. This technology makes use of acetogenic bacteria or designed microorganisms to ferment agricultural waste streams, industrial waste gases or carbon dioxide into acetic acid with yields of 0.72-0.88 metric tons of glucose equivalent feedstock.

Carbon Capture Utilization technologies are becoming the new generation of production directions, and electrochemical and thermochemical technologies transform the industrial CO2 emissions into acetic acid. These technologies had pilot scale demonstration with energy efficiencies of 45-58% and hold the potential of a paradigm shift to carbon-negative chemical production.

The world market of acetic acid is a moderately consolidated industry with ten major manufacturers that dominate the global production capacity of about 58-64%. Competitive differentiation focuses on production cost leadership in terms of feedstock integration and process optimization, geographic diversification to assure supply security and logistics optimization, downstream integration to derivative production, and sustainability programs such as carbon capture use and bio-based production pathways.

The major firms have vertically integrated businesses that include the production of methanol or its acquisition, the production of acetic acid, and the production of the derivative downstream products such as vinyl acetate monomer, acetic anhydride, and acetate esters. Competitive environment focuses on operational excellence by having high levels of process control and energy efficiency optimization and reliability maximization that gave 88-94 capacity utilization rates, which is higher than the industry rates of 78-84.

The strategic focus areas are capacity building in advantaged cost positions where there is access to low-cost methanol feedstock, geographic diversification into high-growth Asian markets, sustainability measures that drive to carbon-neutral production pathways, and downstream integration of higher-margin derivative markets. Firms are spending heavily on digital solutions to predictive maintenance, optimization of processes, and supply chain management and are building hydrogen-enabled and bio-based manufacturing.

March 2026: Celanese Corporation has announced USD 1.2-billion investment in Singapore manufacturing complex expansion, which will have 600,000 metric tons of acetic acid capacity with 450,000 metric tons of VAM production with novel methanol carbonylation technology with carbon efficiency of 98.7% and energy consumption of 22% lower than the current facilities.

February 2026: Jiangsu Sopo Chemical commissioned 900,000 metric ton per year acetic acid plant in Zhenjiang, China, which used proprietary catalyst systems that allowed it to operate at 18% of the pressure of conventional processes with an acetate selectivity of 99.4, and a downstream production capability of 400,000 metric tons per year of vinyl acetate monomer (VAM), strengthening its integrated value chain while significantly improving energy efficiency and reducing operational costs and carbon intensity compared to conventional acetic acid production technologies.

January 2026: BP plc won USD 340 million in European Union funding to use in the carbon capture to Hull, UK facility, to develop electrochemical synthesis technology that transforms industrial CO₂ emissions into 120,000 metric tons of acetic acid each year, with commercial operation targeted in 2029 with a carbon intensity 92% lower than normal production.

December 2025: Eastman Chemical Company also reported strategic alliance with LanzaTech Global to develop a commercial scale gas fermentation plant to manufacture 200,000 metric tons of bio-based acetic acid per year on industrial waste gases at the Kingsport, Tennessee complex with a USD 420 million investment to position the company at the apex of food and pharmaceutical markets.

November 2025: SABIC acquired European acetic acid manufacturer with 280,000 metric tons capacity and increased geographic reach and secured feedstock to make acetate esters to serve coatings and adhesives markets in Middle East and European markets.

List of Key Players in Global Acetic Acid Market

Global Acetic Acid Market Segments

By Grade:

By Derivative:

By Application:

By Production Technology:

By End-User Industry:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

26 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.