Share this link via:

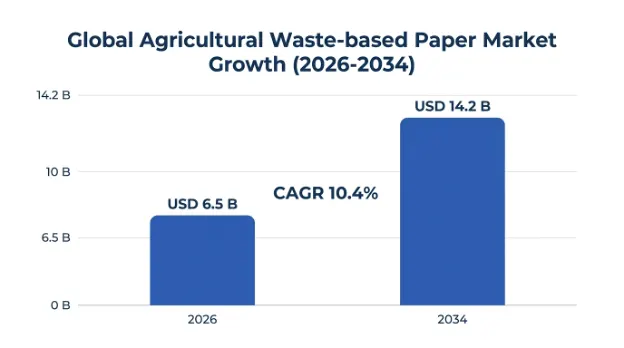

The global agricultural waste-based paper market size was valued at USD 5.8 billion in 2025 and is projected to reach USD 6.5 billion in 2026, expanding to USD 14.2 billion by 2034, growing at a CAGR of 10.4% during the forecast period (2026-2034).

Agricultural waste-based paper represents an entirely new paradigm when it comes to sustainable manufacturing, where instead of relying on wood, non-wood fiber sources such as wheat straw, rice straw, bagasse, corn stover, and cotton stalks are being used to make paper and paperboards. In doing so, this emerging sector is not only helping to solve the environmental issues associated with the production of paper from wood, which involves large scale deforestation, biodiversity loss, and carbon dioxide emissions from forests, but is also helping solve another major environmental issue: crop residue burning by farmers in open fields.

The technical feasibility of producing paper from agricultural waste has improved significantly due to advancements in pulping technology, silica handling systems, and fiber preparation techniques. Modern plants use state-of-the-art chemical recovery systems designed to handle high-silica agricultural residues, an enzyme-based preprocessing method to facilitate efficient fiber separation without damaging the cellulose component, as well as a composite fiber furnish combining agricultural waste material with recycled fibers to obtain ideal mechanical properties. These developments have enabled agricultural waste-based paper to achieve performance levels comparable to traditional wood-pulp paper across various applications, from corrugated containers to fine writing papers.

The commercial value of the market extends beyond simple material substitution to include full-circle economy solutions whereby agricultural waste streams can be converted into valuable raw materials for industry. With more than 2.5 billion tons of agricultural residues produced annually worldwide of which only about 12% is utilized for industrial purposes, the market targets a vast underutilized resource of biomass along with promoting the growth of the rural economy through organized systems for collecting such agricultural residues. In addition, use of agricultural waste papers in existing supply chains helps companies achieve cost savings, diversify their supplies, and enhance their sustainability profiles.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 5.8 Billion |

| Forecast Value | USD 14.2 Billion |

| CAGR | 10.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Europe |

| Segments Covered | By Product Type, Raw Material, Pulping Technology, Application, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Trident Group, JK Paper, DS Smith, Smurfit Kappa, Stora Enso, International Paper, ITC Limited |

Get more details on this report - Request Free Sample

The primary structural factor accelerating growth in the agricultural waste-based paper market is the creation of a regulatory framework aimed at supply chains involving forest conversion, especially the EU’s Deforestation Regulation, which mandates businesses to demonstrate that their paper products are not linked to deforestation or forest conversion after December 2020. Such regulation, along with similar regulations being developed in the U.S., U.K., and other major markets, and other key markets, imposes significant compliance challenges on regular wood pulp supply chains while making compliance easier for agricultural waste-based supply chains that use crop residues from agricultural land without causing any land use changes.

Environmental, social, and governance commitments from corporations have increased the pressure on paper producers and their clients to make measurable progress towards goals of deforestation-free sourcing. Fortune 500 companies across the consumer goods, retail, and e-commerce sectors have set sustainability targets to achieve verified sustainable packaging by 2030, with most of these targets specifying a minimum amount of non-wood sources or deforestation-free sources as a condition of procurement. Agricultural waste-based paper provides an immediate solution to these challenges, as well as carbon savings of up to 25-35% compared to virgin wood pulp paper due to no deforestation and biomass usage instead of decomposition/burning.

Agricultural wastepaper provides an edge in regulations not only with respect to deforestation, but also in terms of other environmental criteria that are increasingly considered part of the policy criteria related to government procurements and business sustainability indexes. Life-cycle assessments have repeatedly shown better performance in terms of water usage, air pollution, and waste production, making agricultural wastepaper a better choice for companies that want overall environmental improvement.

Government Policies Targeting Crop Residue Burning and Air Quality Improvement

Government intervention has become a key market driver, as increasingly stringent regulations is directed at addressing issues of open field burning of crops, which is a prevalent method among farmers, contributing to dangerous crises of air pollution in large agricultural areas. In India alone, farmers burn approximately 92 million tons of straw from rice and wheat in states such as Punjab and Haryana each year, causing toxic smog for over 100 million people and becoming one of the causes of respiratory diseases. Burning bans, financial penalties, and farmer incentive programs are stimulating demand for agricultural wastepaper.

The policy mechanisms recognize that industrial use of crop residues is the only solution to ensure complete elimination of burning along with offering economic incentives to the farming community. Policy measures such as provision of government subsidies in setting up equipment for collecting residues, financing schemes for setting up plants for processing agricultural waste, and carbon credits for avoiding emissions from burning ensure cost reductions on the side of paper producers and help meet economic development goals for rural areas.

In regions where agricultural wastepaper is already being used by industries, policies involving both bans on burning and incentives to promote industrial use have been successful in achieving better air quality outcomes. This can provide a basis for replicating such policies elsewhere in agricultural regions that struggle with the same air quality issues, thereby providing more market opportunities.

The rapid growth of global e-commerce has created substantial demand to produce corrugated materials due to an 8-12% rise in shipment container needs per year caused by the increase in sales in the e-commerce industry. This rising demand has coincided with increasing pressure to phase out single-use plastics and move towards more environmentally friendly packaging materials.

Fibers obtained from agricultural waste exhibit great suitability for corrugated medium and liner use in situations where shortened fiber length does not adversely affect mechanical properties, as well as the sustainability story of turning agricultural waste into packaging material resonates highly with eco-conscious consumers and buyers who consider such attributes important. Leading e-commerce companies such as Amazon and Alibaba, as well as their local counterparts, enforce green packaging policies on their suppliers whereby suppliers must switch to sustainable packaging materials that are often made from agricultural waste material.

The superior packaging qualities of agricultural waste fiber, especially the natural water-resistant quality of sugarcane bagasse and high printability quality of wheat straw, allow for the use of the product in premium applications for communication of sustainable values via the package. It is easy to achieve mechanical properties equivalent to conventionally recycled paperboard while offering better environmental value.

A major constraint affecting market growth is the substantial capital investment required to construct or upgrade paper production plants to ensure efficient production processes of agricultural waste which have specific properties like being rich in silica, varying water content and having different seasonality patterns. In contrast to other paper mills which use wood pulp, an agricultural waste treatment plant needs specific machinery to handle silica, a special chemical recovery system and improved material handling due to its low bulk density.

Silica content in rice and wheat straws is between 10-20%, while wood pulp has silica content of 0.1-0.5%, thus leading to processing difficulties such as silica scaling in the recovery boiler, higher consumption of chemicals, and wear of machinery which necessitates the use of special silica removal technologies as well as special recovery processes. The increase in capital costs required for the processing capacity of agricultural waste is 25-35% more than the cost of wood pulp mills.

Residue harvesting and storage constitute major operational issues owing to the scattered distribution of crop production, seasonal timing, and low bulk density attributes that hamper efficient transport systems. Residue harvesting economically becomes viable only within 80–120 kilometers of processing plants, thereby restricting plant locations to those areas where there is adequate density of residue supply along with complex logistics infrastructure for gathering material from several small suppliers.

Seasonality of crops means that the paper manufacturing companies need to keep a 6–12-month supply of the raw materials needed for their business operations to ensure consistency, resulting in significant working capital needs along with quality retention problems that help prevent fungus formation and ensure proper fiber retention qualities.

The innovation lies in the possibility of using molded pulp products made from agricultural waste material in food service packaging as well as consumer packaging because of the worldwide ban on expanded polystyrene and plastic disposables. The sugarcane bagasse and wheat straw show remarkable potential for thermoforming such items as clamshells, plates, and bowls providing excellent insulation, grease resistance, and complete composting within 60-90 days.

Market demand for molded pulp is considerably more profitable when compared to commoditized paper-based products, whereby the best uses of molded pulp in food service will generate sales prices twice as high as those of similar packaging made from corrugated materials, meeting the demand for PFAS-free compostable options for single-use plastic tableware. Market interest in these alternative solutions has already been shown by some key players in the food service industry.

The agriculture wastepaper projects have a unique opportunity to tap into the world of carbon finance and sustainability-linked instruments because of the quantifiable benefits for the environment in terms of emissions from avoiding burning, lessening the burden on deforestation, and decreased carbon footprints throughout the project lifetime.

The opportunity of methodology for calculating the carbon benefits of agriculture waste usage leads to an opportunity for further integration with environmental credits that could provide up to USD 15-25 per ton of CO2 equivalent in carbon credits sales, as well as funding through sustainability-linked loaning at advantageous interest rates.

Enzymatic Processing and Bio-Pulping Technology Advancement

The agricultural wastepaper industry is currently undergoing its own technology boom in the form of using bioprocessing techniques such as enzymatic treatment and bio-pulping techniques that selectively break down lignin without disrupting the cellulose fibers. This type of biological process employs specific enzymes or fungi that help decrease chemical usage by 20-25% along with increasing fiber output.

Bio-pulping plants at an advanced level show savings of about 15-20% in energy usage during fiber processing in addition to high-quality paper production from the mild process of separating the fibers in their natural state of strength. The application of this technological trend greatly increases competitiveness and environmental performance.

The trend towards market development tends to promote advanced fiber mixing systems which incorporate agricultural waste along with recycling and only small amounts of virgin fibers to create optimal performance properties while at the same time being highly sustainable. Such blends allow one to engineer paper with certain qualities while remaining compatible with current recycling facilities.

Asia Pacific dominated the market share in 2025 with valuation at USD 2.6 billion with expected CAGR of 10.8% during the forecast period till 2034. It is evident that Asia Pacific has dominant presence due to generation of maximum agricultural residues across the globe, including China, India, Indonesia, and Thailand that generate 1.2 billion tons of agricultural crop residue. Asia Pacific has advantage of developed agricultural wastepaper production facilities including bagasse manufacturing plants situated adjacent to sugar factories.

India is the country with the highest growing market due to air pollution issues caused by burning crops in its northern regions as well as through government-sponsored financial incentive programs for residue collection and processing. India enjoys a huge advantage with its market due to agricultural wastepaper companies that cater to local and international demand.

The fastest growing region was Europe with expected CAGR of 11.2% until 2034, reaching revenue of USD 1.8 billion by 2025. The increased growth is attributed to the influence of EU Deforestation Regulation on the requirements for fiber sourcing, development of the entire cycle economy framework, as well as sophisticated consumer markets that allow higher prices for sustainable packaging materials.

European companies are investing in agricultural waste processing technologies for processing agricultural waste to comply with the new regulations and consumer expectations, mainly focusing on the use of straw of wheat and barley grown within the region.

Packaging Paper & Board is the largest category in terms of market share, accounting for 52% and valued at USD 3.0 billion in 2025, and growing at 11.2% CAGR over the forecast period until 2034. Packaging Paper & Board remains dominant because of the increasing demand for e-commerce corrugated packaging and foodservice products, along with increasing corporate sustainability goals to use sustainable packaging materials.

Printing & Writing Paper occupies 24% market share. The printing and writing paper category comprise emerging markets, where agricultural wastepaper offers more economical solutions than wood pulp imports, also providing economic benefits to local agricultural communities.

Raw Material Insights

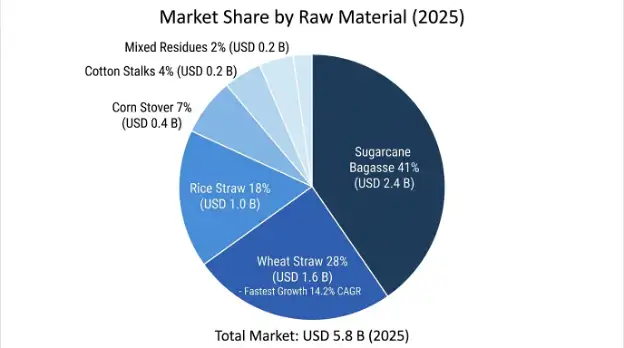

The Sugarcane Bagasse Market commands the largest market share of 41%, valued at USD 2.4 billion in 2025, thanks to the existing processing facilities located adjacent to sugar processing plants, favorable fiber quality, and constant availability throughout the year.

Wheat Straw represents the fastest-growing segment at 14.2% CAGR, driven by abundant availability across major wheat-producing regions, improving silica management technologies, and strong government incentives for straw utilization in India, China, and Europe.

Food & Beverage Packaging is the leading segment constituting 45% market share, thanks to its high adoption rate in molded pulp tableware, sustainable food containers, and secondary packaging solutions that offer competitive benefits in terms of biodegradability and food safety credentials.

E-commerce & Logistics contributes 28% market share and 12.1% CAGR owing to phenomenal demand for packaging material in e-commerce and sustainability focus of businesses on eco-friendly materials.

The industry shows fragmentation levels that are not extreme, where established players in the production of paper are using agricultural waste together with specialist regional processors who deal exclusively with waste streams. Competitive advantage is based on material procurement security from farm partners, efficient processing technology for processing high silica content materials, and sustainability certification.

Leading companies are adopting vertical integration strategies to ensure stable sources of agricultural waste by forming partnership and agreement arrangements coupled with adoption of state-of-the-art processing technologies.

March 2026: Stora Enso has invested EUR 150 million in wheat straw processing facilities across Europe to produce 200,000 tons of environmentally friendly packaging materials per year.

January 2026: Trident Group commissioned an innovative enzymatic processing system at its lead Indian plant and managed to achieve a 22% decrease in chemical consumption as well as a fiber yield increase of 8% through wheat straw processing.

November 2025: Agricultural waste packaging solutions, based on wheat straw and featuring 70% wheat straw content, have been launched by DS Smith in European markets as part of their corrugated range of products.

September 2025: An Asian paper manufacturer received government approval for establishing a 180,000-tonne capacity rice straw processing facility using state-of-the-art silica extraction technology as part of the crop burning elimination subsidy program.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.