Share this link via:

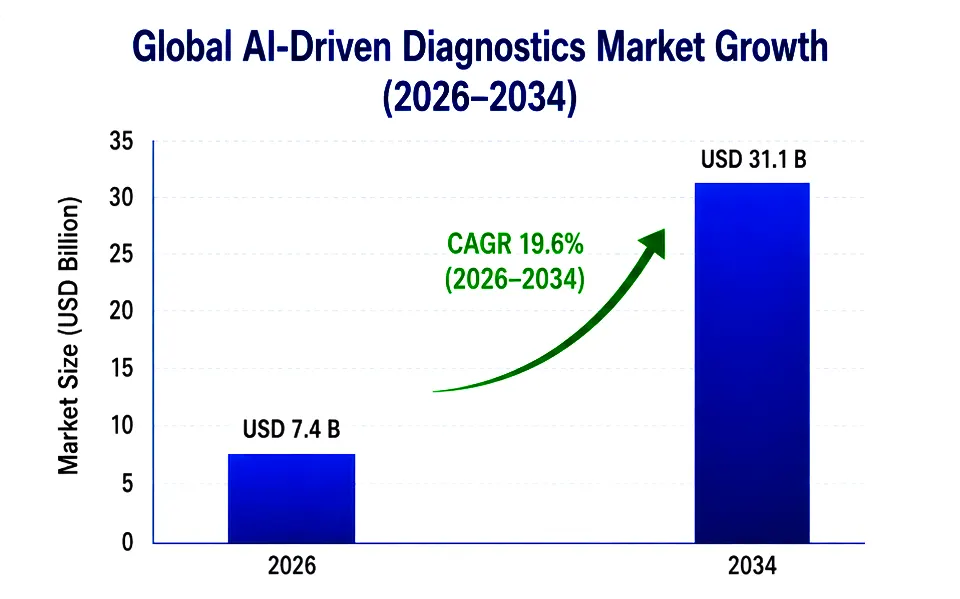

The global AI-driven diagnostics market size was valued at USD 6.2 billion in 2025 and is projected to reach USD 7.4 billion in 2026, expanding to USD 31.1 billion by 2034, growing at a CAGR of 19.6% during the forecast period (2026-2034).

AI-driven diagnostics involves advanced computational technologies that use high-performance machine learning algorithms, deep neural networks, computer vision and natural language processing to improve medical disease diagnosis and classification accuracy, speed and efficiency across a variety of clinical modalities. These systems are able to analyze large amounts of complex medical information such as high-resolution imaging studies, digital pathology slides, genomic sequences, laboratory results and unstructured electronic health records, identifying subtle pathological patterns often undetectable by human clinicians that can lead to earlier disease detection, more accurate risk stratification, and provide better treatment recommendations for patients, resulting in improved patient outcomes and reduced healthcare costs.

In what is described as an unprecedented set of systemic problems in the healthcare industry, the radiologist shortage is projected to reach 42,000 in the United States alone by 2030, with more than 4.7 billion imaging studies performed annually worldwide, more than 1.7 billion people suffering from multifactorial chronic diseases and diagnostic errors estimated to affect 12 million Americans annually. AI-powered diagnostic technologies solve these problems by providing automated triage systems to prioritize critical findings, computer-aided detection algorithms to detect early-stage pathologies, workflow optimization tools to reduce interpretation time by 30–50%, and decision support platforms that enforce diagnostic quality uniformity across institutions and geographic regions.

These platforms include a variety of AI technologies, such as convolutional neural networks for pixel-level tissue classification in radiology and pathology, transformer-based language models for extracting actionable insights from clinical documentation, and federated learning systems for collaborative model training across institutions while maintaining patient privacy. By combining AI diagnostics with current HIT systems, such as picture archiving and communication systems, laboratory information management systems, and electronic health records, healthcare organizations can establish full diagnostic ecosystems. These diagnostic ecosystems provide a seamless interface that improves clinical processes, reduces the time to diagnosis for critical cases and aids in population health management initiatives.

The commercial value of these innovations extends beyond software licensing revenue; it includes cloud-based diagnostic platforms, AI-powered medical imaging equipment, clinical validation services, regulatory advisory, and integration middleware that seamlessly integrates AI systems with existing hospital information systems. The market responds to the high unmet need in the healthcare delivery system, ranging from high-throughput diagnostics in tertiary academic medical centers to specialist-level diagnostics, made available via AI-powered telemedicine platforms in rural health centers.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 6.2 Billion |

| Forecast Value | USD 31.1 Billion |

| CAGR | 19.6% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Component, Technology, Application, Modality, Disease Area, End-User, Deployment |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Siemens Healthineers, GE HealthCare, Philips Healthcare, Google Health, IBM Watson Health, Aidoc, PathAI, Tempus AI |

Get more details on this report - Request Free Sample

The primary driver of market growth is in the AI-based diagnosis market can be identified as the increasing disparity between the rising demands for diagnostics and the existing capacity to provide specialist expertise, especially radiologists, pathologists, and subspecialized diagnosticians who contribute their expert interpretation to the current process of diagnosing and classifying diseases. In the US alone, the radiologist shortage is projected to reach approximately 42,000 by 2030, while the global pathology workforce will be shrinking at 2.3% annually due to more people retiring than entering the profession.

Exponential increase in the demand for diagnostic imaging occurred in the last decade, and in 2025, it is estimated that 4.7 billion images will be taken globally, with a yearly growth rate of 3.8%. Reasons behind this increase are population aging, advanced cancer screening, and increased aggressiveness of diagnosis, thanks to innovative imaging techniques. The training period required to become a qualified radiologist, which spans more than ten years of education and residency, poses serious challenges in meeting the capacity demands and cannot be easily resolved using traditional strategies.

Clinical benefits provided by the AI diagnostic tool can be attributed to the following facts: automated triaging of patients helps reduce time spent before performing an examination; in particular, stroke door-to-needle times have been found to be reduced by 23-31% when AI triaging systems were applied. The sensitivity rate of mammography imaging reached 88-94% compared to 73-87% for a single radiologist reading. As for cancer staging, AI-assisted platforms have shown concordance with consensus panels of pathologists at more than 90%.

The growing global disease burden of chronic illnesses, cancer, and neurodegenerative disorders leads to constant need for high throughput and highly accurate diagnostics systems that work at throughput levels that surpass the existing clinical facilities. Approximately 20 million new cancer cases are diagnosed worldwide each year., while projections show that by 2040 this number will rise to 29.5 million.

Cardiovascular diseases continue to be the number one killer in the world and have claimed 17.9 million lives every year because diagnostic imaging is vital in the risk assessment, lesion detection, and management planning in patients diagnosed with coronary artery disease, heart failure, and structural heart problems. There is an urgent need for accurate and early diagnosis because it is economically proven that early detection of cancer saves on costs (reduction of 60-75%) and increases five-year survival rate by 30-55%.

The diagnostic capacity of AI systems allows for early detection of changes in the pathological condition, which is before they become apparent through symptoms. Deep learning models used to analyze images of the lungs have been found capable of detecting lung cancer nodules that are smaller than those detectable by current diagnostic tools, and AI-based heart disease prediction models show better results than traditional risk factors.

One of the major restraints is poor data quality and algorithmic bias., which reduces clinical acceptance of AI-based decisions when AI-based applications trained using databases that were geographically or demographically less diverse tend to lose efficiency in clinical settings where conditions are not like the training process conditions. Some of the instances of algorithmic bias are as follows: AI-based dermatological algorithms that have proven to be far less sensitive to detect skin cancer in individuals with darker skin; AI-based chest X-ray algorithms with poor performance in lower-income hospitals due to the presence of different disease prevalence rate; cardiac risk predictors that are known to underpredict risk for women.

Healthcare facilities are now insisting on evidence that the AI algorithm has been tested across diverse patient populations, imaging equipment, and clinical procedures before making any commitment to adopting such technology. The need to test and validate biases and demographics of an algorithm can take another 18-24 months in addition to 40-60% rise in clinical validation expenses as opposed to normal medical device development projects.

A market revolutionizing opportunity lies in the expansion of AI diagnostics from hospital settings to point-of-care settings and primary care centers using portable AI diagnostic instruments and smartphone-based applications. AI-enabled portable ultrasound devices, AI-based screening apps for skin conditions, and portable lab analyzers embedded with AI interpretative algorithms help in detecting diseases at an early stage, thus preventing unnecessary referrals to specialists and expensive diagnostic imaging studies.

The decentralized diagnostics proposition holds even more potential in developing countries and rural healthcare environments where there is a lack of specialists, thereby leaving a large demand for diagnosis unfilled, thanks to AI technologies which can help community health workers or general practitioners carry out diagnoses that earlier needed a specialist’s knowledge or lab equipment. There is huge potential in the global POC diagnostics industry, set to reach USD 84.2B by 2030, for companies offering AI diagnostic platforms with device integration and cloud computing.

The emergence of large language models (LLMs) trained on imaging reports, pathology results, and clinical records related to imaging reports, pathological results, and other clinical records is revolutionizing the process of diagnostic reporting through automatic generation of structured reports, conversion of diagnoses into patient-friendly language, and natural language querying of diagnostic databases. Specialized large language models for radiology can produce preliminary diagnostic reports based on imaging results to the extent that such reports are suitable as drafts for a review by radiologists as opposed to generating reports from scratch. These reports can be produced up to 40-60% faster on average.

The incorporation of generative AI into the diagnostic process will facilitate automatic quality assurance verification, standardized templates for better inter-specialty collaboration, and immediate decision support through integrating diagnostic information with guidelines and individual patient conditions. Nevertheless, generative AI deployment needs thorough validation processes to avoid hallucination, which would make it necessary to establish human-AI-based hybrid reporting models.

North America accounted for the largest market share of USD 2.6 billion in 2025 and is expected to register a CAGR of 18.4% during 2026–2034. Key factors driving dominance include the most advanced AI healthcare regulatory environment, characterized by the Digital Health Center of Excellence from the FDA; the presence of companies leading the way in developing new AI diagnostics, evidenced by 58% of global AI medical device authorizations originating from the United States; large investments in AI healthcare, surpassing USD 8.9 billion in 2025 and readiness of healthcare systems to allocate funds for diagnostic technology development aimed at solving issues such as shortage of personnel and quality improvements.

The US alone accounts for 84% of the North American market value due to a fee-for-service reimbursement model providing economic motivation for the implementation of diagnostic tools and quality improvement measures; increasing Medicare coverage of AI-assisted diagnosis and comprehensive coverage of novel diagnostic technologies provided by commercial insurance. Other factors that positively impact the market include an array of existing academic medical centers focused on research into AI, sophisticated IT solutions, and well-developed clinical networks.

The Asia Pacific region became the leader in growth with an expected CAGR of 22.3%, achieving USD 1.4 billion by 2034. Growth in the region is driven by its large population, increasing demand for diagnostics, substantial government investment in AI healthcare infrastructure, and rapid digital health adoption. by governments in the AI technology infrastructure of health, rapid growth of digital health capabilities, and an increasing number of middle-class people with greater concern for healthcare quality and accessibility.

China is leading growth in this region with 38% market share, fueled by its national AI healthcare program that involves the commitment of USD 15 billion in developing medical AI technologies up to 2030, presence of robust digital health infrastructures to facilitate the large-scale use of AI and government policies supporting the use of AI in tier-1 and tier-2 hospital systems. In Japan, the presence of an aging population and advanced medical imaging infrastructures provides a fertile ground for the use of AI diagnostic tools.

Software holds the largest component share at 67% worth USD 4.2 billion by 2025 and growing at a rate of 21.3% during the forecast period. This market category is further split into components like AI diagnostic algorithms, clinical decision support systems, automated reporting software, and integration software offering diagnostic solutions within the existing clinical IT infrastructures. In terms of advantages, the software component includes scalable cloud deployment models for easy adoption without huge investments on physical assets; subscription-based business models for alignment with clinical usage; and model improvements based on new clinical data.

The services segment accounts for 19% of market revenue at USD 1.2 billion in 2025, which includes areas like implementation consultancy, clinical validation, regulatory assistance, and performance analysis of AI diagnostic models. Hardware represents the remaining 14% of market share with components like imaging equipment optimized for use with AI advanced computing infrastructures, and edge computing devices for real-time diagnostic solutions.

Deep Learning is the leading technology segment with a market share of 44%, estimated to be worth USD 2.7 billion in 2025 and forecasted to grow at 22.1% CAGR through 2034. Convolutional neural network-based deep learning technology is used in medical imaging applications for the purpose of automated detection, segmentation, and classification of pathological findings, achieving levels of accuracy comparable to that of clinical experts.

Computer Vision accounts for 28% of the market and is valued at USD 1.7 billion in 2025. Applications include surgical assistance software, dermatology screening tools, and digital pathology whole-slide analysis systems. and digital pathology whole slide analysis systems. NLP is a technology segment comprising 16% of market share in the global market.

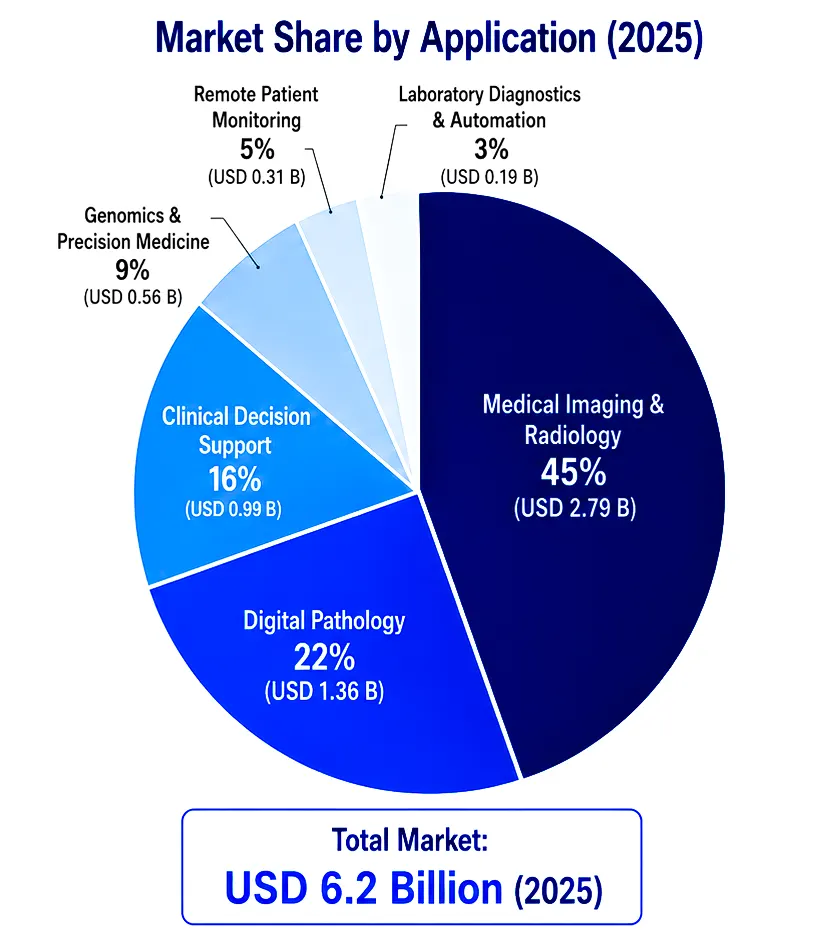

Medical Imaging and Radiology holds the largest share in terms of market value of USD 2.8 billion in 2025, growing at a CAGR of 19.1% during the forecast period from 2025 to 2034 due to huge volume of global radiological imaging studies, standardization of DICOM format that allows AI implementation, and robust evidence of AI capabilities for chest, breast, and neuroimaging applications. Digital Pathology is valued at USD 1.4 billion in 2025, growing at a CAGR of 21.7%.

Clinical decision support is the most popular use case with 24.7% CAGR because healthcare systems invest in technologies for analyzing patient data from different sources to provide better treatment and diagnostic decisions.

The global AI-driven diagnostics market is moderately fragmented., as the existing medical technology companies such as Siemens Healthineers, GE HealthCare, and Philips Healthcare incorporate AI technologies in their existing imaging systems along with the development of specialized AI diagnostics firms such as Aidoc, PathAI, Tempus AI, and Zebra Medical Vision. The leading companies in the market hold a share of about 52% of the market value, and competitive advantage is driven by factors such as the quality of evidence, approval across various jurisdictions, workflow integration capabilities, and real-world evidence.

Partnerships between AI companies and established healthcare technology providers are accelerating market consolidation. and well-known healthcare technology providers are aiding the process of market consolidation, and some of the notable acquisitions include that of Biotelemetry by Philips for USD 2.8 billion and investment of USD 890 million by GE HealthCare in the AI diagnostics firms in 2025.

March 2026: The Siemens Healthineers AI diagnostic platform combining radiological, pathological, and laboratory analysis capabilities achieved FDA approval after showing 18 percent increase in diagnostic accuracy in oncology use cases in a validation study involving 47,000 patients.

February 2026: Google Health’s multimodal AI technology using imaging analytics combined with genomics interpretation for precision oncology applications won breakthrough device designation, with rollout planned across 200 hospitals by 2026.

January 2026: USD 410 million funding for PathAI has been secured to boost the commercial rollout of its digital pathology artificial intelligence platform, which will be rolled out to an additional 150 pathology labs globally.

December 2025: Aidoc introduced an AI triage solution supporting 14 additional imaging indications, including cardiac CT and liver lesions. such as cardiac CT studies as well as liver lesions, earning FDA clearance and CE Mark at the same time.

November 2025: Tempus AI partnered with Epic Systems to integrate the AI diagnostics into Epic’s clinical workflow, thus enabling automatic results to appear in doctors’ notes on behalf of 350 health networks.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.