Share this link via:

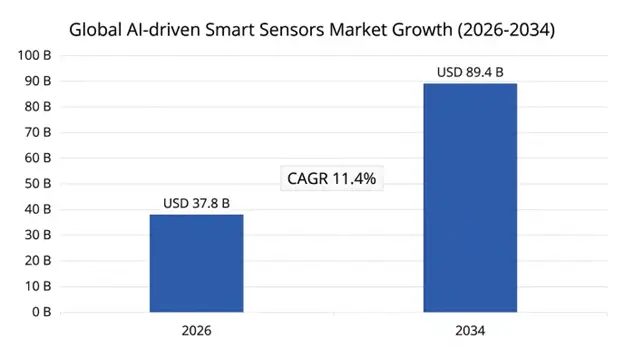

The global AI-driven smart sensors market size was valued at USD 33.2 billion in 2025 and is projected to reach USD 37.8 billion in 2026, expanding to USD 89.4 billion by 2034, growing at a CAGR of 11.4% during the forecast period (2026-2034).

Smart sensors with AI capabilities are a paradigm shift in the field of sensing technology, as they are built using sophisticated sensing technologies and embedded artificial intelligence, which is changing the way devices interact with and analyze their physical surroundings. Unlike traditional sensors that only collect and send raw measurement data to a processing unit in the cloud or external systems, AI-powered smart sensors embed AI technology into the sensor itself, allowing for real-time data analysis, pattern recognition, self-decision-making, and self-adaptation, with no need for cloud-based infrastructure or centralized processing.

Technological underpinnings of AI-powered smart sensors include high-end MEMS sensor integration with low-power neural processing units, low-power CMOS imaging arrays that are able to process image data on-device, and complex sensor fusion platforms combining multiple sensing modalities with embedded Artificial Intelligence (AI) to derive useful information from complex streams of environmental data. They use quantized neural networks, pruned machine learning networks, and event-driven architectures designed to operate at ultra-low power levels, thereby enabling continuous intelligent sensing for battery powered systems, remote industrial deployments, and resource constrained Internet of Things deployments where it is impractical or not economical to implement traditional cloud-dependent processing systems.

The commercial landscape of AI-supported smart sensors moves beyond hardware and covers everything from intelligent sensing software development kits to model deployment pipelines for making algorithm updates on the fly, sensor network management systems for thousands of devices in a wide distributed network, and sophisticated analytics platforms (combined with AI) that can collect data from large-scale sensor deployments to improve system-level performance. In industrial applications using AI sensor networks, this translates to millions of data points being processed every day, generating value-added intelligence that unlocks parallel market opportunities such as predictive analytics, cybersecurity solutions, and sensor lifecycle management services, which can have a major impact on the value of the hardware market.

From smart manufacturing environments where AI vision sensors can monitor quality in real-time as fast as production, to autonomous vehicle perception systems that can recognize objects and avoid collisions in real-time under challenging traffic conditions, to continuous healthcare monitoring systems where AI biosensors can track patients health and identify early signs of cardiovascular events or metabolic disorder to a physician with on-device accuracy, without requiring sensitive physiological information to be continuously transmitted to external systems.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 33.2 Billion |

| Forecast Value | USD 89.4 Billion |

| CAGR | 11.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Sensor Type, Intelligence Level, Technology, Application, End-Use Industry, Component |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, China, Japan, India, South Korea, Australia, Brazil, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Bosch Sensortec, STMicroelectronics, NXP Semiconductors, Texas Instruments, Sony Semiconductor, Infineon Technologies, Analog Devices |

Get more details on this report - Request Free Sample

Accelerating Industry 4.0 Adoption and Predictive Maintenance Revolution

The growing adoption of AI-powered smart sensors is being supported by the manufacturing industry's shift toward smart automation and predictive maintenance systems, which are revolutionizing the way the industry operates and manages assets. Conventional reactive maintenance practices cause catastrophic equipment failures, resulting in production downtime at a cost of USD 50,000 per hour on average for the automotive industry and asset utilization rates of less than 65% across heavy industry sectors due to conservative maintenance scheduling that prioritizes reliability over optimization.

Advanced vibration analysis, acoustic signature recognition, and thermal pattern detections by smart sensors powered by artificial intelligence can continuously monitor the condition of an industrial machine, detecting mechanical degradation weeks before failures or critical events occur within the machine. The embedded machine learning models are trained on historical failure patterns and can identify deviations from normal operation and alert maintenance personnel to a potentially failing component so that maintenance can be scheduled during a planned downtime window, while equipment is maximized.

The impact on the business is significant and in manufacturing, a wide range of sensors are deployed in a comprehensive network, with their results showing a reduction of 25-35% in maintenance costs, 40-50% in the number of unplanned downtime events, and a 15-20% improvement in overall equipment effectiveness by optimizing maintenance schedules and prolonging the lifespan of assets. AI sensor infrastructure is expected to account for 18-22% of total automation investments across global manufacturing industries in 2025, as manufacturers focus on increased investments in data-driven operations to help manage and optimize their business.

Key Performance Metrics:

One of the most technologically challenging and rapidly growing application areas for AI-powered smart sensors is the automotive industry, where the number of sensors in modern vehicles continues to grow due to advanced sensor fusion architectures using LiDAR, radar, ultrasonic, and computer vision, that utilize embedded AI processing for autonomous navigation, avoid collisions, detect pedestrians, and monitor occupants. In 2025, the global market for autonomous and semi-autonomous vehicles (ASVs) was valued at USD 62.4 billion, and AI sensor systems contributed about 20-24% of the total costs of vehicle technology content.

While they are standard in most compact and lower-range models, ADAS features are becoming mandatory in most mid-range and premium vehicles sold in developed markets since the European Union's General Safety Regulation mandates that all new vehicles sold from 2024 will include automatic emergency braking, lane departure warning and driver monitoring systems, generating global mandatory demand for AI-powered sensing solutions in production volumes of over 95 million vehicles per year.

To move from Level 2 partial automation to Level 4 high automation, the number of sensor modalities used in AI processing needs to grow by orders of magnitude, as fully autonomous vehicles have 25-35 sensor modalities, while current advanced driver assistance use 8-12. Each sensor needs to be able to analyze complex environmental data in real-time, with latency of less than 10 milliseconds to perform critical safety functions, which requires robust edge AI processing ability that is embedded in the sensor, not in centralized vehicle computing platforms.

Automotive AI Sensor Metrics:

The healthcare industry is becoming one of the fastest expanding application areas for biosensors based on artificial intelligence and physiological monitoring devices because of aging world population with the need for constant health monitoring, capacity constraints within healthcare systems driving demand for remote management of patients and the advancement of technology that allows accurate clinical measurements using wearable sensors. AI-based biosensors are increasingly being used for continuous monitoring of glucose level, cardiac activity, blood pressure, and early sepsis detection are changing their role from being clinical devices to becoming healthcare management devices.

The combination of miniaturization of biosensing with AI inference allows wearables to conduct advanced clinical testing traditionally conducted in laboratories, such as atrial fibrillation detection using photoplethysmography data with 96% accuracy, hypoglycemia detection from optical readings that do not involve any invasive procedures, and detection of patient deterioration four to six hours prior to clinical diagnosis by continuously analyzing their vital signs.

Such possibilities help address major healthcare system concerns associated with minimizing hospital readmission, intervening into diseases early, and allowing elderly patients more time at home thanks to monitoring their vital signs around the clock. The remote patient monitoring market involving AI-enabled biosensors was valued at USD 31.8 billion in 2025, with annual growth of 22%.

Healthcare AI Sensor Performance Metrics:

The major drawback that comes in the way of acceptance of smart sensors powered by artificial intelligence revolves around the huge investment that is required upfront, alongside complications involved in the integration process. AI-powered sensors, equipped with special neural processing power and firmware stacks along with capabilities for computing, cost significantly higher than ordinary sensors. They can be estimated at 3-5 times more expensive than regular sensors.

The implementation process within enterprises usually takes between 12-18 months to complete, including sensor network installation, system integration, training sessions for employees, as well as optimizing system performance. The total cost of ownership varies from USD 2.8-4.2 million depending on the scale of industry facilities. Small to medium enterprises are unable to afford comprehensive implementation of such solutions due to their lack of skills and funding.

A major opportunity exists in the rapidly evolving edge AI processing market in the ongoing development of capabilities in edge AI processing and Tiny Machine Learning technology that allow advanced neural network processing to take place at ultra-low power levels on microcontrollers within sensors themselves. Through Tiny Machine Learning technology, machine learning models capable of running at milliwatt power levels can carry out tasks like advanced pattern recognition and prediction.

Edge AI brings about an economic transformation of the way sensor networks operate by cutting down on cloud connectivity, lowering costs of transmitting information, and allowing autonomous operation when there is limited bandwidth available. Companies developing highly efficient neural network architectures and special hardware for AI to accelerate calculations will be in the best position to claim market dominance as edge processing approaches cloud-level performance while using very little power.

The area of AI-powered smart sensors is experiencing significant technological advancements based on neuromorphic sensors mimicking biological neural structures which detect environmental changes instead of capturing data at fixed intervals and thereby delivering substantial improvements in energy efficiency and speed of sensing over digital sensors in use. DVS cameras have emerged as the most advanced neuromorphic sensors, able to sense light intensity changes at individual pixels on a microsecond timescale while only using 5-15 milliwatts of power against 800-1,500 milliwatts used by traditional cameras.

Since neuromorphic sensors produce sparse event-based data streams, their integration with neural networks is highly compatible, because data stream processing by spiking neural networks is much more effective, and it allows achieving a much higher energy efficiency of processing. As a result, applications such as fast industrial inspection, reliable perception of surroundings by self-driving vehicles in difficult illumination conditions and constantly working consumer interface devices are pushing neuromorphic sensors onto the market, which is expected to reach USD 8.4 billion in value by 2034.

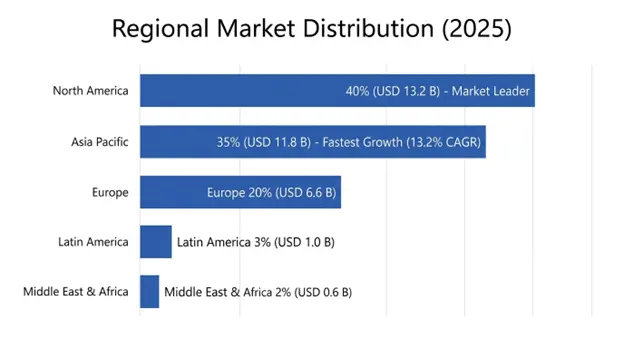

North America represented the largest regional market share by value at USD 13.2 billion in 2025, with a predicted CAGR of 10.8% until 2034. This was owing to a highly skilled regional environment in AI-based technology development, enterprise-level technological uptake environment, major procurement of advanced sensing systems in defense and aerospace, and robust venture capital investment landscape for startups engaged in the development of AI sensors. North America comprises 84% of the regional market valuation, with key contributions from automotive technology centers in Michigan, semiconductor fabrication centers in Arizona and Texas, and technology centers in California.

The federal government’s procurement activity is one of the driving forces in this market, as its applications, such as battlefields surveillance, threats identification, and navigation of autonomous systems, require high-performance AI sensors, specifications exceed those required for the commercial sector. According to the Department of Defense, about USD 3.8 billion was spent on research and development of AI-based sensors in 2025.

The Asia Pacific region is the fastest growing market for sensors in the world with CAGR forecast at 13.2% between 2024-2034, estimated to reach USD 11.8 billion by 2025. Growth in the region is underpinned by the largest number of manufacturing operations in the world leading to huge industrial requirements for AI sensors, presence of semiconductor and electronics manufacturing leaders with strong sensor manufacturing capabilities, significant government investments in smart city initiatives, and growth in automotive production involving ADAS.

China accounts for 41% of the regional market value based on its strong policy implementation through government-mandated intelligent manufacturing strategies, high volume of production of electric vehicles along with the incorporation of advanced AI sensors in them, and considerable funding put into developing domestically manufactured AI chips to lessen reliance on foreign processing technologies of AI sensors.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.