Share this link via:

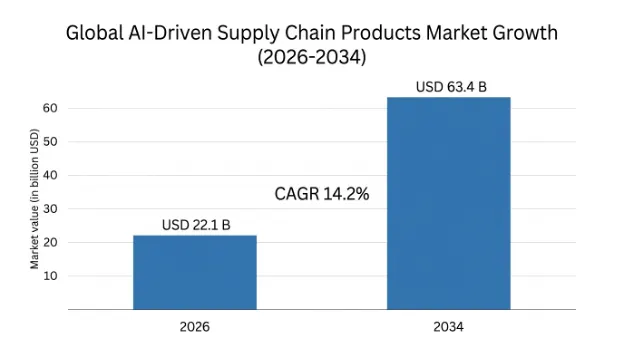

The global AI-driven supply chain products market size was valued at USD 18.6 billion in 2025 and is projected to reach USD 22.1 billion in 2026, expanding to USD 63.4 billion by 2034, growing at a CAGR of 14.2% during the forecast period (2026-2034).

AI-enabled supply chain products represent a paradigm shift in business logistics and operations management. The products employ cutting-edge AI technologies, which include machine learning, deep learning, natural language processing, computer vision, and generative AI, and develop autonomous and self-adaptive supply chain networks that have capabilities for making decisions in real time as well as adapting to market dynamics. Technology enables the organization to build autonomous cognitive systems that handle huge amounts of structured and unstructured data coming from internal enterprise systems, external market dynamics, IoT sensors, and global information platforms.

Technology architecture entails a combination of several interwoven levels of intelligence that work together to achieve never-seen-before optimization. These sophisticated demand sensing algorithms apply machine learning techniques to predict demand using POS data, social media trends, weather trends, economic factors, and promotions with MAPE reduction of 25-40%, mathematically stated as:

$$ ext {MAPE} = frac{1}{n} sum_{t=1} ^n left| frac {A_t - F_t} {A_t} ight| imes 100%$$

where $A_t$ is the actual demand, and $F_t$ is the forecasted demand. The multi-echelon inventory optimization engines use this information, along with other information such as lead time variability, carrying cost considerations, and service level requirements to calculate optimal inventory positions in complicated logistics systems, resulting in savings of between 15-25% in carrying costs, in addition to higher product availability.

Integration with generative AI technology is an example of the next step in evolution, allowing natural language dialogue with data from the complicated field of supply chains. Supply chain experts will be able to ask questions about their processes in common parlance, getting a full analysis that draws upon different data sources and receiving concrete recommendations on actions along with predictions about their effects. Generative AI models keep a pulse on all the thousands of external sources available, such as news, regulatory changes, filings, and social media sentiment. This provides companies with real-time risk management capabilities for their suppliers, weeks in advance of disruption.

Commercial importance is not only associated with efficiency but also with competitiveness in a world where superior supply chain operations are becoming the key determinant of customer loyalty, market presence, and profitability. Companies adopting AI-based supply chain management solutions have seen an average reduction in inventory levels by 15-25%, savings in logistics costs by 10-18%, increased forecast accuracy by 20-40%, and reduced planning cycle times by 30-50%, resulting in tens or even hundreds of millions of dollars annually in value generation.

The addressable market consists of all enterprises that have control over their physical logistics in all industry verticals, where the penetration level will be most intense in the following verticals, which experience fluctuations in demand, multi-level suppliers, and high financial implications if their supply chain fails retail & e-commerce, manufacturing, healthcare/pharmaceutical, automotive, and high-tech electronics.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 18.6 Billion |

| Forecast Value | USD 63.4 Billion |

| CAGR | 14.2% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Component, Technology, Application, Deployment, Enterprise Size, End-User Industry |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | SAP SE, Oracle Corporation, Microsoft Corporation, IBM Corporation, Blue Yonder Group, Kinaxis Inc., o9 Solutions, Coupa Software, Manhattan Associates, C3.ai |

Get more details on this report - Request Free Sample

The primary factor that drives the uptake of AI-powered supply chain products arises from the organization’s realization that traditional models of efficient and cost-effective supply chains are fundamentally unsuitable for operation within a world characterized by disruption and geopolitical instability, alongside increasingly unpredictable customer demand. The coronavirus pandemic became a full-fledged test case for all the challenges that a business would face in a world where traditional supply chain models could not cope with unpredictable disruptions to supplier networks, production processes, and customer demands.

The economic implications of disruptions within the supply chains between 2020-2022 have been unparalleled. The automobile industry suffered losses of around USD 210 billion due to the shortage of semiconductors, which can be partly attributed to a failure to use the technology for effective demand sensing and monitoring of suppliers. Retail companies were suffering from the problem of stockouts in popular categories and excess inventory in declining products at once, and their combined cost of retail inventory distortion exceeded USD 1.8 trillion globally.

These experiences changed the focus and direction of priorities and spending by business executives, making it critical for boards of directors to make resilience of the supply chain and investment in AI technology a priority. Businesses that spent money on AI visibility and risk management platforms between 2020-2023 performed significantly better when encountering disruption compared to their peers using traditional strategies.

Generative AI technology, as well as its adoption by enterprises, has been recognized as a catalytic accelerator of transformation, providing new abilities far more advanced than those offered by the first-generation AI tools used in predictive analysis and optimization. Generative AI technology offers capabilities for interacting naturally using language in handling complicated supply chain data, generating scenario analysis and risk assessment, synthesizing unstructured information from outside sources such as news and suppliers, as well as making recommendations for optimization and reasoning about the context of the problem.

Incorporation of large language models results in democratization of the process of accessing AI-generated insights, allowing for engagement with complex business data in the form of conversations rather than having special skills in analytical processes. Supply chain managers will be able to ask questions to the platform powered by generative AI about the reason behind the poor service level of the certain product and get not only thorough analysis that covers all aspects such as demand forecasts, suppliers, transportation, and inventory positions, but also concrete recommendations.

Generative AI technology also allows for supplier risk assessments via automation using an extensive analysis of thousands of data sources, including financial reports, press releases, social media, regulations, geopolitical risks, and more to keep the constantly updated supplier risk profiles. The problem with traditional approaches to supplier risk management is that they involve regular manual supplier risk assessments, which focus only on tier-one suppliers, thereby leaving companies oblivious to cascading risks within their supplier networks.

The predominant issue affecting the application of artificial intelligence to achieve business results from the use of AI-driven supply chain products is that of ensuring adequate data for algorithms to work effectively based on clean and up-to-date information. The operations within the supply chain result in huge amounts of data that can be collected through ERP solutions, warehousing platforms, transportation management solutions, supplier’s portals, and even IoT solutions, yet the problem is that data can often be found dispersed in multiple systems, improperly structured, containing errors and missing data points.

Organizations trying to implement an AI-based supply chain solution find that the process often takes more time than originally expected because 40-60% of efforts must be invested in data cleaning and integration, which were overlooked during the evaluation of the solutions. Poor quality of master data such as inaccurate data about the supplier hierarchy, erroneous information about suppliers, and wrong geographic classification affects AI algorithms negatively by exacerbating problems inherent in the data set.

The technical challenge associated with integrating AI systems into the current enterprise landscape, which normally involves the presence of many ERP systems and legacy WMS, as well as other point solutions accumulated due to many years of investment in technologies, poses a high risk for implementation.

The potential for market development in leveraging AI within supply chains in the small and medium-sized enterprise market space, where 90% of companies exist globally, which have considerable supply chain complexity but have not yet had access to enterprise-grade AI solutions because of prohibitive costs, technical challenges, and personnel skill sets required, represents a large untapped market opportunity. However, the evolution of cloud-based AI supply chain systems with a modular structure and subscription-based payment models, integrated into popular SME ERP systems, is revolutionizing access to this technology.

SME-focused cloud-based AI logistics solutions can help deliver up to 65-80% TCO savings against on-premises enterprise solutions, through economies of scale due to a standardized deployment approach, economies of scale in infrastructure utilization, and pre-configured industry-specific AI modules that require minimal customization. The SME market segment has been estimated at over USD 18 billion by 2034, currently enjoying penetration levels below 12%.

The use of digital twin technologies with AI-based supply chains is arguably among the most important developments taking place today that are transforming how supply chains plan for risk. Digital twins make it possible to build virtual representations of real-world supply chains with all its components such as suppliers' sites, factories, distribution centers, and transport routes. This means that companies can test the effects of any disruption or change on their operations through simulation.

The real-time data-driven digital twin continuously consumes real-time data to sustain its virtual representation of the current state of the network to perform dynamic what-if analyses by testing thousands of different solutions within a matter of minutes. When a firm is dealing with the failure of a key supplier, it can instantly assess the effects on the company’s ability to deliver goods at an acceptable service level.

Market dynamics are rapidly changing in terms of switching from monolithic on-premises software to modular cloud-native systems through supply chain as a service models that democratize access to cutting-edge technologies for using artificial intelligence, thus making it possible for small and mid-size companies to use enterprise-class algorithms. Cloud-native architecture allows the easy integration of external sources of data such as global weather and maritime information as well as constant over-the-air updates of AI algorithms for maintaining their accuracy amid changes in market conditions.

The North America region has been dominating the market with USD 7.1 billion share in 2025 and is expected to register CAGR of 13.5% till 2034 due to the region being most advanced in terms of technological innovation, having the highest level of enterprise technology culture adoption, and presence of global technology firms that develop and deploy AI-enabled supply chains solutions. North America holds 88% market value of the region due to the presence of Fortune 500 companies with ample budgets for technology investments and global AI research institutions that bring constant innovation, along with an established venture capital environment.

The advantages of the regional market lie in having well-established regulatory structures that encourage information sharing and AI implementation in a business setting, sophisticated cloud-based systems that allow for scalable AI solution implementations, and the presence of a culture of technological innovation leading to a welcoming market for groundbreaking AI supply chain capabilities. Retail and manufacturing together contribute 58% to regional investments in AI supply chains, thanks to cutthroat competition and profitability resulting from AI solutions for inventory optimization and logistic operations.

Asia Pacific is the fastest growing regional market with a forecasted CAGR of 17.2% during 2034, valued at USD 5.2 billion in 2025, owing to the world’s largest manufacturing industry in China, Japan, South Korea, and Southeast Asia, complemented by expanding e-commerce industry and digitalization programs backed by government initiatives. The manufacturing industry of China, which comprises the largest manufacturing industry of the world by value, is witnessing widespread adoption of AI technology in its supply chain operations owing to increasing labor costs driving automation, growing complexity of the supply chain of Chinese manufacturers transitioning into more advanced supply chains, and government backing.

The Japanese industry is highly industrialized, especially in the automotive and electronics sectors, making the Japanese market highly advanced regarding AI supply chain optimization that requires high-levels of integration to optimize such highly complicated just-in-time manufacturing processes. South Korea is home to advanced technology-based companies such as the semiconductor industry and consumer electronic industry, which utilize AI supply chain systems at component and sub-assembly level.

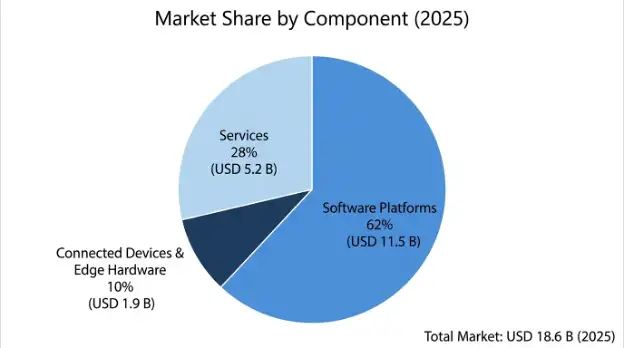

Component Insights: Software Platforms have a majority market share of 62% worth USD 11.5 billion in 2025, including end-to-end AI suites, control towers, and AI software modules. The market share of services is 28% worth USD 5.2 billion and is growing as more organizations need dedicated expertise in AI deployments and change management within their organization. Connected devices and edge hardware make up for 10% market share and grow as businesses deploy IoT sensors and warehouse automation needs.

Technology Insights: The market share of Machine Learning and Deep Learning platforms is 42% worth USD 7.8 billion, acting as the base for other technologies in the AI supply chain market. Generative AI proves to be the fastest-growing technology segment with a 67% CAGR, starting from a market base of USD 580 million in 2025. The digital twin technology has a market size of USD 890 million with a 38% CAGR.

Application Insights: Demand Forecasting & Planning is the biggest end-use application market worth USD 4.2 billion in 2025 due to its necessity in terms of demand intelligence. Inventory Optimization makes up USD 3.8 billion, which can be attributed to its financial benefits through working capital optimization. Supply Chain Visibility & Risk Management is the fastest-growing end-use application market due to 31% CAGR after the pandemic.

End-User Industry Insights: Manufacturing makes up the biggest end-user industry vertically in terms of market share at USD 5.1 billion by 2025 with 13.8% CAGR, mainly due to complexities in manufacturing supply chains and needs to optimize production planning. Retail & E-commerce makes USD 4.7 billion with 15.2% CAGR mainly due to investments in demand and fulfillment optimizations.

The AI-driven Supply Chain Products market is moderately concentrated with the top ten companies holding around 52-58% market share based on their platform-based solutions encompassing the entire supply chain function, industry-specific solution libraries, and enterprise customers to which they are well entrenched and generate substantial switching costs. Market differentiation lies in terms of precision of AI models and constant learning, scope of pre-integration with enterprise data, functional industry-specific solutions, and ability to drive financial gains from implementation.

Market competition can be segregated into established enterprise software players like SAP, Oracle, and Microsoft leveraging AI within a complete supply chain platform suite, and specialist AI-driven supply chain vendors such as Blue Yonder, Kinaxis, and o9 Solutions, which offer purpose-built AI platforms that include more sophisticated algorithms. Emerging generative AI-based startup competitors pose competition in selected supply chain functions such as supplier risk management, demand sensing, and logistics optimization.

April 2026: SAP SE introduced an advanced version of its AI Supply Chain Control Tower featuring integration with large language models for natural language supply chain queries and automated exception handling, resulting in 145% rise in platform daily active users while testing beta version among enterprise customers.

March 2026: Blue Yonder Group revealed partnership with Microsoft Azure for running its Luminate Platform on Azure cloud services, thus allowing for increased generative AI functionality as well as access to its solutions by mid-sized enterprises via Azure Marketplace.

February 2026: Kinaxis Inc. made acquisition of supply chain digital twin provider for USD 290 million, adding digital twin simulation technology into its Rapid Response supply chain platform and improving competitive standing relative to other enterprise software providers.

January 2026: Oracle Corporation unveiled the Supply Chain AI Agents for autonomous routine decision making and execution related to procurement actions, inventory repositioning activities, and carrier selection within defined criteria - becoming the industry's first commercially available autonomous supply chain execution technology.

December 2025: o9 Solutions secured USD 500 million in Series D financing round at a USD 3.7 billion valuation, with investment earmarked for generative AI platform creation, global business expansion, and product improvements in manufacturing industry use case.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.