Share this link via:

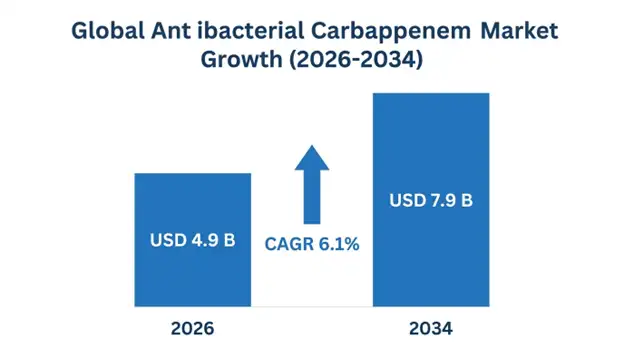

The global antibacterial carbapenem market was valued at USD 4.6 billion in 2025 and is projected to reach USD 4.9 billion in 2026, expanding to USD 7.9 billion by 2034, growing at a CAGR of 6.1% during the forecast period (2026-2034).

Carbapenems represent the most clinically critical class of beta-lactam antibiotics, acting as last resort therapeutic options kept for life threatening infections linked to multidrug resistant gram-negative as well as gram-positive organisms, when alternative therapies are ineffective or unavailable.. They are advanced bicyclic beta-lactam molecules, with a special carbapenem nucleus where a carbon atom ends up taking the place of the sulfur at position 1 within the thiazolidine ring, plus there is unsaturation between positions 2-3. Those structural details provide remarkable resistance to hydrolysis, including by most bacterial beta-lactamase enzymes such as extended-spectrum beta-lactamases, which are able to inactivate third and fourth generation cephalosporins.

Pharmacologically, carbapenems possess a very broad antimicrobial spectrum., covering basically all relevant aerobic and anaerobic gram-positive and gram-negative bacteria. Action works through high affinity binding to several penicillin-binding proteins at the same time. This “many targets” binding idea can lower the likelihood of resistance arising, especially compared to antibiotics that focus on a single penicillin-binding protein. Also, because they remain stable to beta-lactamases in the first place, they still work therapeutically even when the pathogens produce common resistance enzymes that previously made older drug classes ineffective.

The clinical significance extends well beyond antimicrobial efficacy, as carbapenems address some of the most critical challenges in modern healthcare, like the kinds of problems modern healthcare keeps bumping into where carbapenem-resistant organisms are among the most urgent antimicrobial resistance threats globally. The World Health Organization has placed carbapenem-resistant Enterobacteriaceae, Pseudomonas aeruginosa, and Acinetobacter baumannii in the critical priority category, highlighting the urgent need for intervention., and in endemic healthcare settings carbapenem resistance rates can reach 30–60%.

The market includes established generic molecules whose patent protection has long expired., like meropenem, imipenem-cilastatin, and ertapenem, plus newer carbapenem-beta-lactamase. inhibitor combinations meant to bring back activity against carbapenemase-producing organisms. This market segmentation creates distinct competitive dynamics.: generic manufacturers tend to fight mainly on price and supply reliability, while innovators usually pursue premium pricing for the novel combinations tackling resistant infections that used to be, in practical terms, untreatable.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 4.6 billion |

| Forecast Value | USD 7.9 billion |

| CAGR | 6.1% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Spectrum of Activity, Indication, Route of Administration, End-User, Distribution Channel, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, Saudi Arabia, UAE, South Africa |

| Key Market Playes | Merck & Co. Inc., Pfizer Inc., AstraZeneca PLC, Shionogi & Co. Ltd., Sumitomo Dainippon Pharma, Fresenius Kabi, Aurobindo Pharma, Hikma Pharmaceuticals |

Get more details on this report - Request Free Sample

The first major driver behind the growth in carbapenem markets lies in the continually growing problem of antimicrobial resistance across the globe, which limits therapeutic choices for infections caused by multidrug-resistant bacteria, thereby rendering carbapenems critical choices for treating such infections. According to the data provided by WHO on global antimicrobial resistance surveillance, the prevalence rate of resistance to third-generation cephalosporin in Klebsiella pneumoniae, E. coli, and other Enterobacteriaceae has exceeded 40-60% in many healthcare settings around the world, thus positioning carbapenems as the sole treatment choice for severe gram-negative infections.

ESBL-producing Enterobacteriaceae strains have emerged as the most common cause of complicated UTI, intra-abdominal infection, and bloodstream infections among others. With ESBL rates among Enterobacteriaceae having exceeded 20-30% in many hospitals, third-generation cephalosporins have have proven ineffective. as the initial treatment regimen for high-risk patients. Carbapenems have therefore become the primary empirical treatment choice for such patients due to their efficacy and reliability. As far as the consequences of using ineffective initial treatment are concerned, it should be noted that mortality costs for such cases remain high.

In 2019, the global mortality burden of deaths due to antimicrobial resistance was 1.27 million deaths, and projections suggest that number would rise to 10 million deaths each year by 2050 in the absence of successful measures. The mortality rate associated with carbapenem-resistant microorganisms is exceptionally high; carbapenem-resistant Klebsiella pneumoniae bacteremia has case-fatality rates of 40–60%., and carbapenem-resistant Acinetobacter baumannii ventilator-associated pneumonia exceeds 50% death rate.

A major growth driver is the successful development of novel carbapenem-beta-lactamase inhibitor combinations. Carbapenem resistance among Enterobacteriaceae producing KPC, NDM, OXA-48, and VIM enzymes can render traditional carbapenems ineffective., leaving gaps in the provision of treatment options in endemic healthcare facilities. The approval of imipenem-cilastatin-relebactam. and meropenem-vaborbactam by the FDA confirmed the commercial viability of carbapenem-beta-lactamase inhibitor combinations. and proved their restored efficacy against KPC-producing carbapenem-resistant strains. These advanced therapies command premium pricing due to limited therapeutic alternatives. due to the lack of alternatives and the importance of such medications when there are no other treatment options; these advanced therapies can be acquired for around USD 3,000-5,000 per treatment regimen, compared to USD 200-400 for generics of carbapenems.

These successes have paved the way for novel compounds in the pipeline through various means of regulatory approval, including FDA Qualified Infectious Disease Product status that provides market exclusivity and expedited development pathways. Combinations that address the production of metallo-beta-lactamases and other mechanisms of resistance continue to represent significant potential innovations within this important class of therapies.

The steady growth of ICU capacity, advanced surgical practices, and populations of immunocompromised patients results in structurally increasing demands for treatment with carbapenems. In the US alone, there are around 96,000 intensive care beds, 200,000 beds in Europe, and rapidly rising capacities in emerging economies, all of which form the centers of aggregated demands for broad-spectrum antibiotics, including carbapenems..

Patient groups undergoing myelosuppressive chemotherapy as part of their cancer therapy, transplant recipients of either solid organs or hematopoietic stem cells, and patients under biologic immunosuppressive drugs are at risk of becoming significantly susceptible to serious bacterial infections requiring empirical treatment. There were 20 million new cases of cancer per year in 2022, with the forecast pointing to 30 million cases by 2040. Solid organ transplants exceed 150,000 per year globally.

A major factor limiting carbapenem market volume growth is the restriction of indications through antimicrobial stewardship programs. through antimicrobial stewardship programs. According to Infectious Diseases Society of America and Society for Healthcare Epidemiology guidelines, intervention strategies related to carbapenem stewardship should be key parts of stewardship programs in healthcare institutions.. Prospective audit and feedback, prior authorization, automatic stop orders and de-escalation result in carbapenem consumption decrease between 15-35 percent in institutions with implemented interventions.

Intervention strategies have proven effective in lowering carbapenem consumption. without negative impact on patient survival rates. According to the results of several meta-analyses, reduction of carbapenem usage is achieved in range of 20-40 percent with improved survival rates. Antimicrobial stewardship programs are required by the Centers for Disease Control and Prevention in hospitals providing services to Medicare and Medicaid beneficiaries.

A transformational market opportunity lies in the development of effective oral carbapenem formulations., which will be able to broaden the scope of addressing the carbapenem market beyond intravenous administration in the hospital setting to the outpatient setting where multidrug-resistant organisms are treated. Currently, there is one investigational oral carbapenem, tebipenem pivoxil hydrobromide, which is under investigation in clinical trials for complicated UTIs that can change the paradigm of treating infections caused by ESBL-producing organisms.

An oral carbapenem will be able to open the retail pharmacy distribution channel as well as lower costs associated with complicated UTIs and intra-abdominal infections because of treatment in hospitals. It will be possible to grab market share from the already multi-billion-dollar market of outpatient treatments that include fluoroquinolones, as well as other less effective oral agents.

There is considerable market potential for the development of carbapenem-combination products that would be active against metallo-beta-lactamases, which are currently resistant to available carbapenem-inhibitor combinations that target only serine beta-lactamases. The production of NDM and VIM metallo-beta-lactamases represents a dire unmet clinical need, where treatment options are limited to highly toxic agents. such as colistin and tigecycline.

In the carbapenem market, there are changes taking place via integration with rapid diagnostic technologies for precise targeting of new combinations of carbapenem based on the identification of resistance mechanisms within a few hours after the patient presents. With the help of multiplex PCR tests and rapid susceptibility tests, detection of carbapenemases is possible within 2-6 hours as opposed to 48-72 hours required by conventional cultures, which can enable immediate use. of the right carbapenem and avoid using broad-spectrum drugs when it is not necessary.

The use of rapid diagnostic tests in conjunction with carbapenem therapy enables targeted administration of novel combinations., high-value novel combinations will be administered where applicable and the standard carbapenems will be preserved through de-escalation where applicable.

The trend towards optimized carbapenem therapy based on pharmacokinetics entails extended and continuous infusion therapy taking advantage of the time dependency of killing. Meropenem and other carbapenems delivered via an extended infusion regimen increase the concentration above the minimum inhibitory concentration for a longer period and reach pharmacodynamics target achievement of 85-95%, whereas only 40-60% are attained by conventional intermittent infusions.

The North American market registered the highest carbapenem market size at USD 1.85 billion in 2025, accounting for 40% of the global market, due to fast-growing uptake of premium novel carbapenems., advanced antimicrobial stewardship program implementation, and complete reimbursement environment for expensive innovative medicines. The U.S. is severely affected by carbapenem-resistant Enterobacteriaceae infections, which are recognized by the CDC as an urgent threat., which facilitates the uptake of efficient novel combinations despite their cost.

The regional market enjoys solid reimbursement opportunities for innovative antibiotics under Medicare Part B and commercial insurance, and leadership among academic hospitals and large health systems in implementing evidence-based carbapenem utilization. Innovating pharmaceutical companies, along with various incentives, such as those provided by the DISARM Act, continue to drive development initiatives related to next generation of carbapenem medications.

Asia-Pacific is the fastest-growing regional market. with an expected CAGR of 7.8% until 2034 because it has the highest incidence of AMR, a large, hospitalized population base, and developing healthcare infrastructure. China holds the position of being the largest national market due to carbapenem usage driven by its population size, hospitals, and the incidence of MDR infections which require a broad-spectrum antibiotic.

India remains a major global hotspot for antimicrobial resistance (AMR). because NDML-producing bacteria have been distributed worldwide after first being reported in India. Carbapenem-resistant bacteria have been found in 30-55% of patients receiving care at tertiary care hospitals in India, thereby ensuring the need for carbapenem therapy as well as resistance-busting therapies.

The availability of generic manufacturing ensures access to cost-effective carbapenems. Government efforts to provide healthcare coverage for underrepresented regions are expected to boost the growth of the market.

The global antibacterial carbapenem market presents an oligopolistic structure characterized by competition between mature generic carbapenems and innovative combination carbapenems. The mature generic market for carbapenem antibacterials such as meropenem, imipenem-cilastatin, and ertapenem involves stiff competition among several players in terms of pricing, reliability of supply, and regulation compliance in global markets. These players include Aurobindo Pharma, Hikma Pharmaceuticals, Fresenius Kabi, and Asian companies.

However, the innovative market for novel carbapenem-inhibitor products is more concentrated, where Merck & Co leads through the product imipenem-cilastatin-relebactam; whereas, there are other competing firms like AstraZeneca, Shionogi, and other antimicrobial firms with innovative agents. Competitiveness here depends on superiority of their agents against bacteria strains, regulatory aspects such as QIDP designation, and interactions with ID specialists from academic medical centers.

March 2026: Merck & Co. has reported that its drug, imipenem-cilastatin-relebactam, which is under phase III development for hospital-acquired and ventilator-associated pneumonia, has shown positive results; this will support a supplemental regulatory filing. with the FDA for an extended indication.

January 2026: Shionogi & Co. got approval from European Medicines Agency for its cefiderocol drug as a non-carbapenem-based treatment for carbapenem-resistant organism infections, offering an essential treatment alternative for metallo-beta-lactamase producers in Europe.

November 2025: The World Health Organization revised treatment protocols including the new classes of beta-lactamase inhibitors as recommended treatment for KPC-producing carbapenem-resistant Enterobacteriaceae infections, reflecting treatment paradigm change underway at leading institutions globally.

September 2025: A leading pharmaceutical firm secured FDA Fast Track status for experimental oral carbapenem compound for treating complicated UTIs due to ESBL-producing bacteria in outpatients.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

20 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.