Share this link via:

The global augmented reality smart glasses market size was valued at USD 7.2 billion in 2025 and is projected to reach USD 8.9 billion in 2026, expanding to USD 28.4 billion by 2034, growing at a CAGR of 15.6% during the forecast period.

Augmented reality smart glasses represent a revolutionary convergence of advanced optical engineering, miniaturized computing hardware, sensor fusion technology, and artificial intelligence integrate into a wearable platform designed to overlay contextually relevant digital information right onto the user’s actual view, in a seamless manner. And unlike virtual reality setups that fully replace real-world perception with synthetic environments, AR smart glasses keep the full awareness of the physical surroundings, while simultaneously enhancing the user’s visual environment using dynamic digital layers, things like three dimensional models, real time data streams, navigational help, instructional notes, and even collaborative communication interfaces.

AR smart glasses rely on a sophisticated technological architecture that must simultaneously address multiple complex engineering challenges at the same time. For example, waveguide optics must that maintain sufficient brightness under daylight conditions, even when the display is supposed to be see-through. Then there are the computing systems; they must do real time rendering while staying inside tight heat and power limits. In addition, spatial mapping and environmental recognition algorithms, which are designed to maintain stable spatial positioning of digital content to real physical surfaces without significant positional drift or visual instability. And finally, the design for the human body matters, it must remain ergonomically suitable for extended usage durations.

The optical subsystem represents one of the most technically challenging components. Waveguide based systems often use diffractive or holographic gratings to direct display light into thin glass or polymer sheet and then steer it toward the user’s eyes, all while trying to keep the scene outside still visible and not blocked.

spatial computing side, which gives the “brain” the ability to interpret and react to physical environments. This intelligence layer transforms passive display systems into intelligent contextual assistance platforms. World tracking algorithms, typically based on simultaneous localization and mapping, plus plane detection, object recognition, and semantic scene interpretation, enable digital content to maintain accurate spatial registration as you move around. The system must also maintain performance under changing lighting conditions, or your viewing angle shifts. This capability significantly broadens the range of commercial applications, like industrial assembly help where instructions sit directly on the physical parts, or surgical navigation where patient anatomy reconstructions are displayed aligned with the operative field.

The commercial value extends beyond hardware sales alone. It’s also about the larger platform ecosystem, including application development environments, cloud based spatial computing infrastructure, enterprise software integration frameworks, and managed service offerings. Collectively, these components define the end-user value proposition. In enterprise deployments such as manufacturing, logistics, and healthcare, recurring revenue opportunities can be substantial, coming from software subscriptions, content management systems, and workflow integration services. These revenue streams frequently surpass the original hardware income over the full deployment lifecycle.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 7.2 Billion |

| Forecast Value | USD 28.4 Billion |

| CAGR | 15.6% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Display Technology, Application, Connectivity, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Microsoft Corporation, Apple Inc., Meta Platforms, Google LLC, Vuzix Corporation, Magic Leap Inc., Epson America, Lenovo Group |

Get more details on this report - Request Free Sample

The primary structural driver accelerating augmented reality smart glasses market growth, is the accelerating adoption of Industry 4.0 ideas across global manufacturing, logistics, and field service operations. In many organizations AR smart glasses are being deployed to deal with workforce productivity issues, quality concerns, and knowledge management challenges that keep growing, mainly because expert workers are aging, products are getting increasingly complex, and competition keeps forcing companies to cut operating costs while still lifting output quality.

Manufacturing operations represent the most mature and fastest growing enterprise AR use case. Smart glasses there support free access to assembly instructions, quality inspection help, real-time equipment telemetry and even remote expert collaboration, all right inside what the worker can see. Several big manufacturers Boeing, General Electric, Volkswagen, and Siemens included have reported productivity gains in the range of 20–40% for demanding assembly jobs. They also mention error-rate drops of about 30–60% versus paper-based instruction delivery. And training time seems to shrink by roughly 40–60% when onboarding new employees.

Another adoption pull comes from the knowledge transfer crisis triggered by retiring skilled workers. Industrial companies are dealing with a soon-to-happen departure of experienced technicians, employees with decades of tacit know-how. Smart AR glasses make remote expert collaboration models possible, where specialists can coach field workers through complicated steps using shared visual experiences. This significantly expands expert accessibility beyond local sites, across geographic borders, while also generating documented knowledge repositories

Key Performance Metrics:

Technological breakthroughs in optical engineering represent a major structural growth driver for smart AR glasses, enabling form factors increasingly comparable to conventional eyewear while maintaining acceptable visual performance standards at a level that people can accept. And honestly, the commercial “growing up” of diffractive plus reflective waveguide tech has already solved a core problem, like how to throw bright high-resolution images across a wide field of view, without needing those bulky optical combiners

Waveguide systems that use precision made gratings, light can be injected into thin glass or polymer substrates, then it stays trapped by total internal reflection, and it gets extracted with high accuracy straight into the user’s eye. That means the display engine can be tucked into the glass’s temples, while the overall design stays slim. At the same time, the move from Liquid Crystal on Silicon display panels toward MicroLED engines has significantly improved for brightness and power efficiency. MicroLEDs now produce brightness that’s over 5 million nits at the source, thereby improving overlay visibility under direct sunlight conditions even in direct sunlight

Technology Performance Metrics:

Global deployment of 5G wireless networks, with peak throughputs above 10 gigabits per second and latency kept under 10 milliseconds, is helping resolve computational bottlenecks that have been holding back AR smart glasses performance. With 5G connectivity in place, cloud rendering designs including remote rendering architectures, can shift computationally intensive tasks such as scene reconstruction, holographic content rendering and computer vision processing toward edge computing sites. That means allowing AR glasses to maintain lighter form factors and deliver experiences previously requiring tether to powerful computer systems.

5G Integration Metrics:

The most significant limitation that affects the widespread implementation of smart glasses technology in terms of AR is a trade-off between technical performance and socially acceptable eyewear design of glasses. It is impossible to ensure good visual experience without a proper size and weight of optical components, which makes such glasses significantly heavier and bulkier than regular eyewear.

State-of-the-art AR systems are 180-400 grams in weight while standard glasses weigh around 25-35 grams; as a result, long-term operation causes neck strain and user discomfort during prolonged usage. Besides, heat generation by computing equipment becomes an important concern when using AR glasses.

Ergonomic Constraint Metrics:

The inherently high production costs of advanced optics and miniature electronics presents significant challenges for widespread commercialization. Waveguide components need to be etched or nano-imprinted with sub-nanometer accuracy, where minor imperfections can result in uneven color distribution and light leakage, thereby reducing manufacturing yields and increasing unit costs. Top-tier enterprise AR headsets are available at a price point between USD 2,200-USD 3,800, whereas consumer-grade devices sell for more than USD 800-1,200.

Cost Structure Metrics:

A transformative market opportunity is emerging in the convergence of AR smart glasses and generative AI with multiple input modes. AR smart glasses function as integrated sensor platforms, AR glasses feed live audiovisual data from the user's surroundings to the AI systems. With big vision-language models, the glasses are able to perceive what the user sees and deliver context-aware digital augmentation, representing a fundamental evolution from display technology to digital assistive tech.

AI Integration Opportunity Metrics:

The most significant commercial application opportunity is associated with a potential consumer breakthrough made possible driven by optical technologies that progressively reduce device weight of AR glasses approaching the form factor of conventional eyewear. New waveguide-based technologies, such as nanoimprint lithography diffractive waveguides and laser beam scanning systems, permit developing ultra-thin display modules for integrating into regular-looking frames.

Consumer Opportunity Metrics:

The market is witnessing a pivotal shift from disjointed pilot projects to enterprise-wide implementations of standardized, digitally integrated enterprise deployments. Enterprises that proved the ROI through their pilot projects are now moving forward with deployments of AR smart glasses at various locations, facilities, and geographies under centralized management and toolchain standardization.

Such a shift alters the vendor evaluation criteria to include device manageability, fleet health tracking, security, and long-term product roadmaps by vendors capable of supporting enterprise operational requirements over many years. As AR smart glasses become core infrastructure for business operations, uptime and service guarantees become key differentiators among vendors.

Enterprise Scaling Metrics:

The inclusion of big language models and generative artificial intelligence in AR devices is changing AR technology from being a device that can only show information to becoming a machine capable of understanding context and providing relevant recommendations without the user having to ask for anything. This can be achieved by combining the visual streams coming from the camera on the outside and using natural language processing to observe the user's actions.

AI Convergence Metrics:

In 2025, North America accounted for the largest regional market share, reaching USD 3.1 billion, and that was about 43.1% of the global market value, with a forecast CAGR of 15.2% all the way to 2034. This regional dominance seems tied to the clustering of major AR technology developers such as Microsoft, Apple, Meta, and Google along with the world’s highest enterprise technology adoption rates, plus large-scale defense procurement programs. The region also benefits from a sophisticated venture capital ecosystem that keeps backing AR innovation.

For the United States specifically, the enterprise market leans on long-running digital transformation investment cultures, where Fortune 500 companies allocate substantial technology investment budgets for operational efficiency upgrades. On the healthcare side, adoption is pushed by value-based care incentives, and thereby creating premium application opportunities for things like surgical navigation, clinical training, and telemedicine.

North American Performance Metrics:

Asia Pacific emerged as the fastest- growing regional market, Clarify whether USD 2.2 billion refers to 2025 or future forecast year. The regional expansion is mostly fueled by China’s huge manufacturing ecosystem which continues to generate substantial enterprise AR deployment opportunities, Japan’s culture of advanced technology adoption, South Korea’s leadership in 5G infrastructure, and India’s tech services sector that’s growing quickly.

China accounts for 52% of the market value, and the government’s Made in China 2025 initiatives are openly backing AR technology adoption inside manufacturing modernization programs. At the same time, domestic AR players like Rokid, XREAL, and Nreal are building more capable platforms, pairing aggressive pricing with better technical skills.

Asia Pacific Growth Metrics:

Binocular Smart Glasses dominate the market, holding around 54% of share, and in 2025 valued at USD 3.9 billion in 2025, then they’re set to keep growing about 16.2% CAGR all the way till 2034. These binocular setups, which deliver stereoscopic three-dimensional AR experiences, show up as the go-to platform for immersive enterprise use cases spatial computing, surgical navigation, and training simulations, where depth perception along with spatial registration precision.

Monocular Smart Glasses take 32% market share at USD 2.3 billion in 2025. They still stay relevant because industrial teams often prefer cost efficiency, easier handling, and extended battery life more than the maximum immersive experience. Head-Mounted Displays make up 14% market share, covering premium platforms that push for the widest field of view and stronger computing capability.

Waveguide Display technology is on track for 48% market share, reaching about USD 3.5 billion in 2025 and, growing around 17.8% CAGR. It stays the dominant optical architecture for see-through AR glasses, because it helps keep the display integration very thin, while still preserving see-through clarity. This architecture remains the preferred choice for enterprise deployments and premium consumer platforms. for enterprise builds and for premium consumer platforms.

Birdbath Optics meanwhile hold 28% market share, or roughly USD 2.0 billion in 2025. They’re usually picked for use cases where optical efficiency and brightness matter more than having an ultra-thin form factor. Then MicroLED technology lands at 15% market share, and it’s expected to grow at about 22.4% CAGR. The main idea there is cleaner outdoor brightness plus better power efficiency.

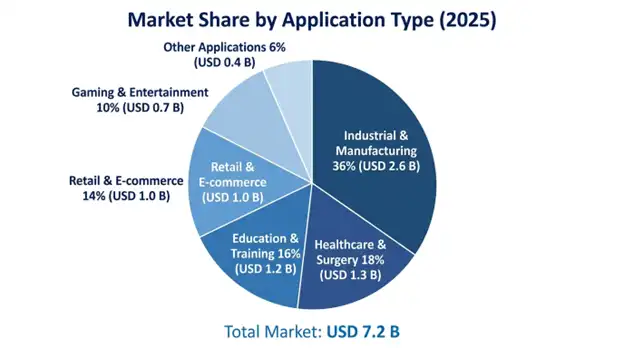

Industrial & Manufacturing is still the biggest application slice, sitting at around 36% market share, valued at USD 2.6 billion in 2025, and it’s projected to grow at a CAGR of 15.8% because of reported productivity gains plus quality enhancement across global manufacturing.

Healthcare & Surgery comes next with 18% market share at roughly USD 1.3 billion in 2025, but it also shows 19.2% CAGR the highest-growth application segment, pushed by surgical navigation, medical training, and telemedicine applications associated with premium pricing structures. Logistics & Warehousing has around 16% market share. This part is mostly driven by vision picking efficiency improvements, plus inventory management applications that keep things organized and fast.

Enterprise and Commercial users dominate at 62% market share, reaching USD 4.5 billion in 2025, and reflecting the maturity how mature industrial AR apps are now, plus how many enterprises are willing to invest heavily in productivity boosting technology. Meanwhile Consumer sits at 22% market share but it’s still growing fast around 18.4% CAGR, and it should turn into the leading segment by 2032 as device form factors increasingly resemble a lot more like conventional eyewear styles.

The global AR smart glasses market is highly dynamic, with three types of competition: platform ecosystem competition amongst technology leaders, enterprise hardware competition amongst specialized AR firms, and consumer market competition driven by advances in lightweight form factor development. The eight leading players capture a roughly 64-72% market share, although competition is increasing as specialty competitors gain footholds in application-specific domains.

Microsoft preserves its enterprise market leadership position through platform ecosystem integration with Azure cloud services and enterprise applications. Apple’s entrance into the market with AR glasses targeted at consumers represents a major competitive force within the market, as it brings consumer-level reputation as well as developer community strength. Meta has shown its determination toward platform dominance by partnering Ray-Ban for a dedicated product line.

March 2026: Apple Inc. declared that development of Apple Glasses using proprietary waveguide display technology and 58-degree field of view with a lightweight 48-gram form factor has been completed, aiming at consumer AR market launch by late 2026, leading analysts to revise long-term market growth forecasts. about future growth potential of the market.

February 2026: Microsoft has released HoloLens 3 with significant 35% reduction in weight, enhanced to 72-degree field of view, generative AI integration, and upgraded battery life of 4.8 hours, with its launch slated for Q4 2026.

January 2026: Meta Platforms has completed strategic collaboration with Essilor Luxottica for incorporation of Ray-Ban smart glasses into consumer markets via integration with innovative AR display technology.

December 2025: Vuzix Corporation has received strategic investment worth USD 150 million for further developing and manufacturing the next generation of waveguide displays for enterprise markets.

November 2025: Magic Leap has successfully raised USD 350 million funding in Series E round to strengthen expansion into healthcare and defense applications, channeling funds towards surgical navigation applications.

List of Top Companies in Augmented Reality Smart Glasses Market

Global Augmented Reality Smart Glasses Market Segments

By Product Type:

By Display Technology:

By Application:

By Connectivity:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

14 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.