Share this link via:

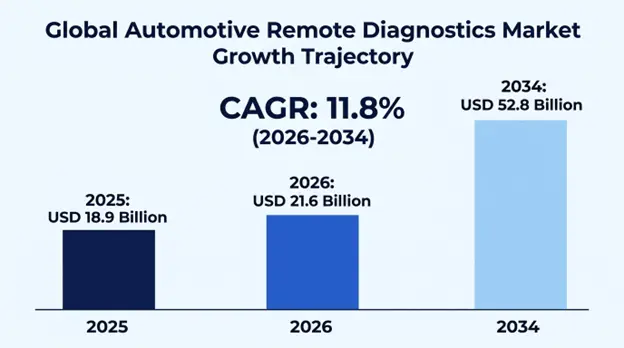

The global automotive remote diagnostics market size was valued at USD 18.9 billion in 2025 and is projected to reach USD 21.6 billion in 2026, expanding to USD 52.8 billion by 2034, growing at a CAGR of 11.8% during the forecast period (2026-2034).

Automotive remote diagnostics is the combination of telematics technology, cloud computing infrastructure, embedded connectivity and sophisticated sensor networks that provide real-time monitoring, analysis and troubleshooting of vehicle systems without necessarily physically inspecting the vehicle or making a visit to the service center. It is an ecosystem of technology that gathers constant data streams in electronic control units located across the current vehicles, such as engine parameters, transmission behavior, battery health status, brake system integrity, emission levels, and hundreds of other functioning variables that are sent to centralized cloud platforms where advanced algorithms are used to detect anomalies, predict component failures, and prescribe preventive maintenance interventions.

Its commercial impact is far more comprehensive than conventional maintenance planning because predictive analytics can cut the number of unexpected vehicle failures by 35-45% to fundamentally change the business model of automotive by supporting usage-based insurance pricing models, facilitating the warranty claim validation process, and the operation of connected and autonomous cars where continuous system health verification is necessary to ensure. Fleet operators use remote diagnostics to ensure optimal vehicle availability, minimize maintenance expenses through condition-based maintenance, enhance vehicle safety through real-time notices of critical system malfunctions. Car makers use collective diagnostic information to discover design flaws in the vehicle groups, speed up the pace of the recall, and provide over-the-air program updates that corrects problems without visiting the dealer.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 18.9 Billion |

| Forecast Value | USD 52.8 Billion |

| CAGR | 11.8% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

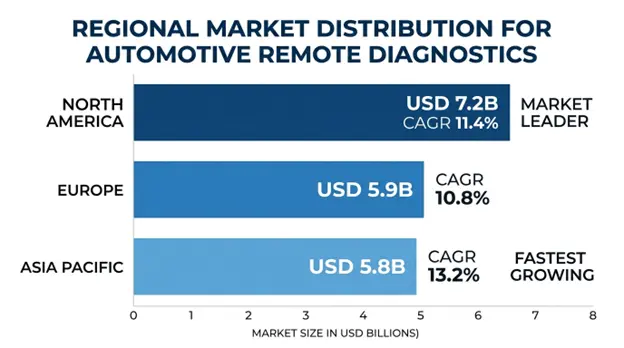

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Vehicle Type, Component, Technology, Application, Connectivity, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Robert Bosch GmbH, Continental AG, Verizon Connect, Geotab Inc., Harman International, Delphi Technologies |

Get more details on this report - Request Free Sample

The most powerful structural force that is driving market growth is the introduction of the mandatory systems of telematics and emergency calls in key automotive markets of the world. The European Union regulation on eCall which is technically obligatory since April 2018 on all new passenger cars and light commercial cars but not on older vehicles specifies that any car must have an automatic emergency call facility with inbuilt telematics capabilities, effectively standardizing the hardware infrastructure needed to implement a comprehensive implementation of remote diagnostics. This regulatory platform provided a baseline connectivity platform on which automotive manufacturers have been building on to have full diagnostic capabilities to the extent of meeting the emergency response requirement.

Other regulatory initiatives have also sprung up across the world such as in Russia, the progressive eRA-GLONASS emergency response scheme and in Brazil, the progressive legislation on eCall and in a few Asian markets, the emerging connected car systems which require the ability to record and transmit data. These requirements eradicate gradual costs in hardware implementation that were earlier attributed to telematics implementation since manufacturers are required to include cellular connection component, GPS positioning and data transmission functionalities irrespective of implementation of other diagnostic features. The regulatory framework has been successful in assisting in subsidizing the underlying technology investments needed in remote diagnostics to support penetration of all the vehicle segments and price range.

Key Performance Metrics:

The increasing pace of the world switching to the use of electric vehicles has posed essential requirements of sophisticated remote diagnostics plants that constantly check the state of battery packs, thermal management and control performance, charging infrastructure relationships, and high-voltage system integrity. Electric vehicle batteries constitute 35-42 percent of the total vehicle prices and have complicated degradation profiles based on charging patterns, exposure to ambient temperatures, variations in discharge depth and cell-level performance which have to be constantly monitored to ensure the use of optimal operation life and avoidance of safety events.

Electric vehicle remote diagnostics systems monitor the voltages of individual cells within battery packs, temperature fields within pack assemblies, state-of-charge error, internal resistance responses history, and full charging history to forecast the remaining useful life and provide early warning of possible thermal runaway events before safety concerns occur. The ability to monitor this range anxiety directly is that it offers more precise predictions of the remaining capacity, manufacturers can check the warranty claim of battery performance degradation, and V2G, whereby the battery health status is certified to use in bidirectional charging.

EVDIMM: Electric Vehicle Metrics of Impact Diagnostic:

Commercial fleet operators have become the most aggressive users of remote diagnostics technology, as they have strong economic incentives of lowering vehicle downtime, streamlining maintenance scheduling, and enhancing asset utilization rates which directly translate to profitability. Unexpected vehicle failure has become an economic strain on fleet operations due to missed deliveries, unsatisfied customers, emergency repairs that cost an average of 3.5-4.2 times the previously planned maintenance, and regulatory compliance issues of hours-of-service and emissions monitoring.

Remote diagnostics systems deal with all these operational weaknesses by helping detect any developing mechanical problems at an early stage when the repair process is less serious and the timing can be planned according to the workload instead of any emergency response procedures. The technology also allows the replacement of calendar-driven maintenance schedules with condition-driven interventions, which match the timing of services with the actual wear pattern of components and not with the conservative manufacturer guidelines, which unnecessarily leads to maintenance, and at the same time reduces catastrophic failures by 22-32% by using early warning systems.

Fleet Economic Performance Indicators:

The greatest weakness that curbs the growth of the automotive remote diagnostics market includes the increasing cyber crimes and diverse regulatory laws on data privacy that pose challenges in implementation and consumer adoption. Current remote diagnostics provides granular data such as exact location history, driving behavioral patterns, vehicle usage frequency, and full operational features that jointly develop rich profiles of individual mobility patterns that become the cause of legitimate privacy concerns on the potential use of these methods of surveillance, discriminatory pricing of insurance, unauthorized access of personal information by third-party, and state surveillance possibilities.

Privacy concerns are further complicated by cybersecurity risks because connected cars are increasingly offering malicious acts more attack surfaces to steal sensitive personal data or manipulate significant safety systems by means of remote access entry. Large-scale public displays of the car hacking potential and recorded cybersecurity attacks have made consumers more aware of these threats, providing an obstacle to connectivity options even though their manufacturers guarantee security and cybersecurity regulatory work in the industry.

The lack of harmonized data protection laws directly focusing on automotive telematics in various jurisdictions makes implementing compliance challenging in 43 different data protection laws that cover automotive remote diagnostics in the key markets of the globe, raising implementation costs and causing ambiguity in terms of the ownership rights of data, constraints on proper use and liability schemes in the case of security breach.

Automobile aftermarket: The automotive aftermarket poses significant implementation issues to a complete deployment of remote diagnostics implementation because it lacks uniform networks of service providers, there is no uniformity in technical capabilities of repair shops, and the diagnostic implementation between the manufacturers of the same vehicle models is inconsistent. Although the original equipment manufacturers retain a proprietary interest on the access and interpretation algorithms of diagnostic data, the independent repair facilities that currently provide services to approximately 65% of out of warranty vehicles have strong obstacles to accessing full diagnostic information that would support effective repairs and maintenance services.

This fragmentation of the market produces a scenario where diagnostic features are underused because of the restrictions of the service network and not the capacity of systems such as diagnostic ones, consumer is unable to take full advantage of diagnostic information when the repair locations are restricted to a network of dealers or equally competent facilities that are independent of technology. The market Standardization work such as Worldwide Harmonized On-Board Diagnostics protocols has yet to be fully successful in setting up universal diagnostic communication standards because manufacturers still have competitive advantages with proprietary systems and are unwilling to share comprehensive data with one enabling the commodification of repair services and loss of aftermarket revenue streams.

One market opportunity that can be transformed is to use remote diagnostics data to transform the business models of automotive insurance based on usage-based insurance models that accurately reflect the pricing of premiums and the assessment of vehicle conditions and the real-time risks exposure instead of the conventional demographic proxies and historical actuarial data. The traditional insurance pricing is based on large demographic segments and past claims information that establish high levels of cross-subsidy between risky and safe drivers in rating groups which creates market inefficiency and consumer dissatisfaction with the pricing accuracy.

Remote diagnostics make it possible to assess the unique risk characteristics of each person individually by constantly analyzing driving patterns such as acceleration activity, braking force, cornering speeds, time of day vehicle activity, choice of the road type, and vehicle condition indicators that directly correlate with the likelihood of accidents and the severity of claims. This type of data driven process helps insurers to provide significant premium discounts averaging between 18-28 to proven safe drivers as well as charge high risk behaviors more accurately, making a market efficiency gain and fairness improvements that are beneficial to both insurers and policyholders.

It is also used in conjunction with parametric insurance models which automatically instigate claims payments upon the diagnostic confirmation of qualifying events like collisions, component failures or environmental damages, that do not require the traditional claims adjustment process and incurs less administrative cost by 42-51 percent plus, and enhances customer satisfaction by increasing claim resolution times.

Insurance Market Opportunity Metrics:

The progress to increased autonomy of the vehicle generates new demands of self-service-wide remote diagnostics that upkeep constant control of the sensor state, processing system integrity, decision-making algorithm resilience, and general system fitness that is needed to feel safe using the autonomous mode. Robotic cars rely on multiple sets of sensors such as cameras, radar, lidar, and ultrasonic devices, which should be correctly calibrated and active to provide safe manoeuvrational performance and failure of any of the sensors can impair the functionality of the autonomous system and its security.

Remote diagnostics systems offer real-time confirmation of sensor correctness, identify degeneration trends suited to recalibration interventions, ensure that perception systems perceive the environment correctly, as well as checking the performance of processing systems to guarantee that autonomous algorithms have access to correct input data to make their decision-making process. The regulatory regimes being developed around the implementation of autonomous vehicles all feature extensive data logs, and remote monitoring, to assist in investigating accidents, affirming the safety-related systems overall and responding to the detected software or hardware shortcomings that will impact the safety of a fleet.

The National Highway Traffic Safety Administration and European Union type approval regulators have already formulated preliminary autonomous vehicle data recording and monitoring requirements, which will increase significantly when the scale of deployments is greater, requiring an obligatory need of complex remote diagnostics facilities that continuously monitor the state of autonomous system health, and give verifiable records of operational parameters to fulfill regulatory compliance requirements.

The automotive remote diagnostics market is undergoing a fast pace of integrating sophisticated artificial intelligence and machine learning neural networks that can analyze past history of failures across entire car fleets to forecast component wear with more and more accuracy and provide actual predictive maintenance response. Conventional diagnostic systems are mostly based on using threshold-based alerts by defining the limits at which a parameter of interest should not be, leading to false positive alerts due to natural fluctuations in the operation of a system, and failure to alert at the early stages of an emerging issue that is not caused by the violation of an absolute threshold.

The machine learning models that are trained on millions of years of operation history of vehicles can detect complex failure patterns that give a warning of component failures up to weeks or months before failure occurs and therefore, maintenance can be performed within the optimal timing windows that reduce both operational interruption and repair expenses. These systems understand that a particular response of engine temperature pattern, vibration frequency, fuel usage variations, and operational load factors are all signs of an imminent component failure in the occurrence of which other parameters may not be out of the normal operating limits.

The technology keeps on increasing the accuracy of prediction because more failure cases in their training datasets will generate a network effect where diagnostic ability increases with the market penetration and the amount of data. Top implementations show 72% accuracy in predicting component failures 30+ days prior to failure versus 31% accuracy in predicting component failures of traditional threshold-based systems.

The performance metrics of AI diagnostics are illustrated using the following metrics:

A paradigm shift has been taking place as automotive remote diagnostics is no longer an active form of passive monitoring, but rather an active form of intervention which is resolved through software updates performed over-the-air which fix certain recognized problems without necessarily performing physical service visits and/or interacting with the dealer. The software code present in modern cars counts 120-180 million lines of code spread across dozens of electronic control units that provides complexity which is bound to create software bugs, security bugs, and optimization opportunities realized after production and customer delivery of cars.

The remote diagnostic infrastructure has made possible over-the-air update capabilities that are allowable to the manufacturers to provide software fixes, security patches and performance improvements to vehicle fleets within days after the problem is detected, instead of the weeks to months of dealer visits that traditionally reduced compliance rates on non-safety-related campaigns to 62-73 per cent.

Such functionality has risen beyond infotainment systems to include safety-related features such as brake control algorithms, battery management optimization, powertrain calibration changes, and autonomous driving feature enhancements. The technology generates recurring revenues by way of subscription based feature activation, performance upgrade, and extended capability deployment that make vehicles more valuable during lifecycles of ownership and diminishes liability to manufacturers due to the ability to fix issues easily.

Metrics of Impact of Over-the-Air Update:

Regional Insights

The biggest market share of USD 7.2 billion is directed at North America in 2025 and the CAGR projected up to 2034 is 11.4%. Geographical leadership is due to the localization of the centers of automotive technology innovation, large commercial fleet operation, strong consumer acceptance of connected vehicle services, and sympathetic regulatory incentives to permit the operation of data-driven vehicle management in the manner without unreasonable privacy limitation that constrains functionality.

The United States reflects 82% of regional market value with significant adoption in commercial trucking operations in which hours-of-service compliance, routing optimization, fuel management and profitable preventive maintenance are generating legalistic diagnostics system adoption. The Electronic Logging Device requirement has provided the basis of telematics infrastructure on which fleet operators have built comprehensive diagnostic functionality which has produced demonstration impacts that fuel adoption throughout other commercial vehicle categories.

There are developed telematics provider ecosystems, a well-established relationship between automotive manufacturers and technology firms, well-developed telecommunications infrastructure that remains connected at high-speed data transmission, and consumer knowledge of connected services in other product categories which makes the barrier to adopting automotive applications lower in North American market.

Key Performance Indicators:

Asia Pacific became the most rapidly growing region with a predicted CAGR of 13.2% until 2034 and will hit USD 5.8 billion in 2025. The locations where the company is expanding are driven by the high prevalence of electric vehicle manufacturing and uptake, the size of the automotive infrastructure, the government policies regarding the development of connected vehicles infrastructure, and the high rate of urbanization that creates need in effective transportation management systems and an ability to integrate a city.

The development in China is regional, with a market share of 58% through 12.8 million electric vehicles sold in 2025, which have the natural characteristics of the availability of remote diagnostic tools to monitor batteries and state compliance with government regulations. The national monitoring platform of New Energy Vehicles mandate by the Chinese government provides that all electric vehicles should transmit real-time data, establishing regulatory foundation to standardize the remote diagnostics infrastructure of all electric vehicle manufactures and provides data collection framework to support the advanced analytics development.

The area enjoys combined tech ecosystems where automotive firms, telephone firms, cloud computing firms and government departments collaborate on connected automobiles platforms with unified growth activities that hastens the implementation timelines and lowers the expenses of implementation in contrast to disjointed Western market frameworks.

Regional Growth Drivers:

Europe had USD 5.9 billion market value in the year 2025 with a forecasted CAGR of 10.8 percent to 2034. The region is on the forefront of regulatory development of connected vehicles, such as the creation of comprehensive frameworks such as eCall emergency response requirements, General Data Protection Regulation setting the data privacy framework, and new regulations on autonomous vehicle data recording requirements creating structured demand on diagnostic capabilities and creating consumer protection frameworks.

The European car manufacturing companies focus on the high-end segments of the car market where sophisticated diagnostic features become competitive advantages and customers are ready to spend money on interconnected services that can improve ownership experiences and improve the performance of their cars. The structural requirements on advanced battery diagnostics, charging optimization and lifecycle management systems are driven by the region being committed to electrification by more and more stringent emissions regulations and phase-out timelines of internal combustion engines.

The European market is characterized by the high level of focus on the protection of data privacy and rights of consumers in relation to the access of information about vehicles, which introduces more specific requirements in designing a diagnostic system and practices of data handling, as well as contributes to the formation of trust frameworks that will facilitate the further adoption of the system as more consumers get confident in the measures of privacy protection and the transparency of data use.

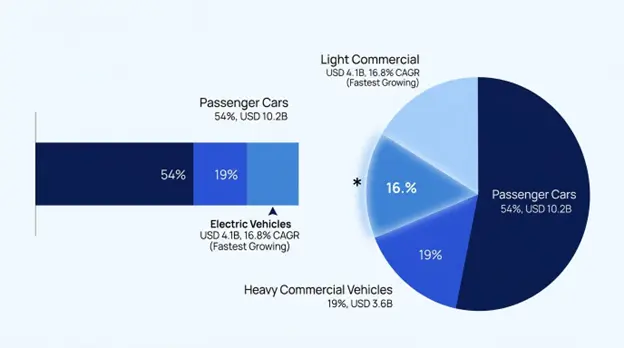

Passenger Cars lead with 54 percent market share worth USD 10.2 billion in 2025 due to large production volumes, rising rates of connectivity standard equipment in each price bracket, and demand by consumers of convenience features such as remote vehicle tracking, maintenance alert systems, stolen vehicle tracking, and built-in smartphone applications. The segment also enjoys the effects of economies of scale in the hardware production and software development which have made the unit price below USD 165 in volume production vehicles with comprehensive diagnostic facilities.

The EV Vehicles are the highest growth and vehicle type at 16.8% CAGR till 2034 with a worth of USD 4.1 billion in 2025. Growth acceleration displays intrinsic diagnostic need to battery health checkout, thermal administration scrutiny, battery optimization, and high-voltage system safety examination that breeds 2.8-3.6 times the diagnostic system value than the traditional inner combustion vehicle. The advanced battery monitoring algorithms, predictive maintenance, and the safety-critical system validation all necessitate electric vehicle diagnostics which are priced at USD 380-520 per vehicle.

In the year 2025, Heavy Commercial Vehicles will be 19-percent market share at USD 3.6 billion, with high adoption and fleet economics where diagnostic systems will provide high returns on investment by reducing downtimes, providing better maintenance schedules and regulatory compliance support. The segment has the most diagnostic system use rates where the mean data transmission is 5-7 times the passenger vehicles because it is needed to operate constantly to monitor the operation and analyze the behavior of the driver and ensure that the emissions are taken care of.

The highest component segment with a 46 per cent share worth USD 8.7 billion in 2025 will be software which will include diagnostic applications, cloud analytics platforms, machine learning algorithms, user interface systems and over-the-air update management platforms. The software segment exhibits the highest growth rates of 13.4% CAGR up to the year 2034 because of the constant improvements in features, improvement of algorithms and subscription services models generate recurring streams of revenue with gross margins of more than 72 percent in case of established platforms.

Services take 34% of the market share in USD 6.4 billion in 2025, such as diagnostic data analysis, predictive maintenance, technical support, system integration, and managed services to fleet operators. The services segment enjoys the returns of recurring revenue models where the average duration of lifetime customers would pay an average of USD 2,200 per vehicle in comprehensive diagnostic services subscriptions and average project revenues of USD 38,000-150,000 per fleet and complexity of integration of the diagnostic system.

Hardware includes 20% market share of USD 3.8 billion in 2025, hardware includes telematics control units and embedded connectivity modules, sensors, edge computing processors, and diagnostic interface equipment. Commoditization pressures and an expanding trend towards integrating diagnostic functions into the mainstream vehicle electronic architecture limits hardware segment growth, but is offset by growing content per vehicle as more vehicle systems become subject to diagnostic monitoring, and by the rising 5G connectivity demands compelling hardware upgrades.

Vehicle Health Monitoring also takes the lead in the application segments with USD 7.8 billion in 2025 and expected to grow at 12.1% CAGR through 2034, and includes engine diagnostics, transmission monitoring, brake system analysis, emission system validation and comprehensive system status reporting. The app is the basis of any other diagnostic service and proves to be the best adopted in all car segments as it is universally applicable and benefits directly through reduction of maintenance costs.

Predictive Maintenance is the most rapidly growing application with a USD 4.2 billion valuation in 2025 with 14.7 percent CAGR. The growth acceleration represents the development of artificial intelligence features that will allow predicting failures with high accuracy 30-45 days beforehand and allow fleet operators and individual car owners to maximize the timing of maintenance, minimize the emergency repair rate, and minimize disruptions in the operation of the vehicles by timely arranging preventive intervention.

Use-Based Insurance Support to USD 2.8 billion in 2025 at a CAGR of 13.9 percent through 2034 will provide claims to insurance companies willing to design risk-based pricing models to match actual driving patterns and vehicle condition instead of relying on demographic indicators. The application generates a value to both the insurers of enhanced accuracy of risk assessment and the consumers of customized pricing to reward safe driving and appropriate vehicle maintenance.

Over-the-Air Updates in USD 2.1 billion in 2025 with 15.2% CAGR up to 2034, will allow manufacturers to provide software updates, feature enhancements, and security patches remotely without needing to visit service centers. The application provides recurrent revenue streams by the means of subscription-based services, and eliminating the expenses incurred by manufacturers in recalling products and enhancing customer satisfaction by delivering updates smoothly.

The automotive remote diagnostics world in the market has moderate level of concentration with the top seven firms holding about 48-56% market value based on a combination of proprietary technology platform, mature relations with automotive manufacturers, detailed network of services and vertical integration strategies of hardware, software, and services. The focus of competitive differentiation is diagnostic algorithm accuracy, level of integration with vehicle electronic architectures, scalability of cloud platforms, artificial intelligence, and the range of supported vehicle makes and models in global markets.

The major players are pursuing both original equipment manufacturer ties to install systems in the factories and aftermarket solutions to serve independent repair shops, fleet operators, and individual owners of vehicles willing to have the diagnostic capability of the older vehicles. The strategic positioning can be exhibited by traditional automotive suppliers based on the knowledge of embedded systems, telecom companies offering the infrastructure of connectivity and data management platforms, specialized telematics providers that specialize in fleet management applications, and technology companies that introduce the idea of cloud computing and artificial intelligence to automotive applications.

Car makers and cloud computing technology alliances have gotten more competitive with the help of technology as the amount of diagnostic data and the processing needs surpass core competencies, providing ecosystem competition between integrated and best-of-breed component strategies which enable customers to choose the best combinations of hardware, software, and service providers.

March 2026: Robert Bosch GmbH also declared USD 285 million investment in artificial intelligence diagnostic platform, where the machine learning models are trained using 72 million years of operational data, which achieves 79% accuracy in component failures 40 or more days early. The platform will be incorporated throughout the Bosch automotive electronics portfolio that caters to 34 vehicle manufacturers worldwide, with the business implementation commencing in Q4 2026.

February 2026: Continental AG finalized the purchase of special electric vehicle battery diagnostics company at USD 160 million to add capabilities in the state-of-health assessment algorithms, thermal management optimization, and charging behavior analysis. The acquisition will enhance the capabilities of Continental in the electric vehicle diagnostic systems with the estimated annual contribution to the revenue of USD 380 million in 2028.

January 2026: Verizon Connect announced next-generation fleet diagnostic platform that incorporates 5G connectivity, edge computing and real-time coach capabilities of drivers. The platform cuts the diagnostic data latency of 12-25 seconds to less than 1.8 seconds, which allows critical systems failures to be alerted of and helps support up to 98,000 commercial vehicles within the North American fleet operations.

December 2025: Geotab Inc. declared that it would cooperate with a large European car manufacturer to incorporate the telematics hardware and diagnostics software into their factories and would install it on 1.8 million vehicles per year starting the 2027 model year. The alliance is the first original equipment manufacturer integration by Geotab which goes beyond the traditional aftermarket positioning to include factory installed diagnostic functionality.

November 2025: Modular diagnostic architecture to allow retrofitment of vehicles with advanced monitoring abilities, installed by Harman International, on vehicles produced after 2016. The system will cover 145 million vehicles around the world that do not have factory telematics installed by dealers or aftermarket with an installation cost that ranges at USD 340-495 depending on the nature of the vehicle and the features that are installed.

List of Key Players in Global Automotive Remote Diagnostics Market

Global Automotive Remote Diagnostics Market Segments

By Vehicle Type:

By Component:

By Technology:

By Application:

By Connectivity:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

13 Jul 2022

Intellectual Market Insights Research © 2026. All rights reserved.