Share this link via:

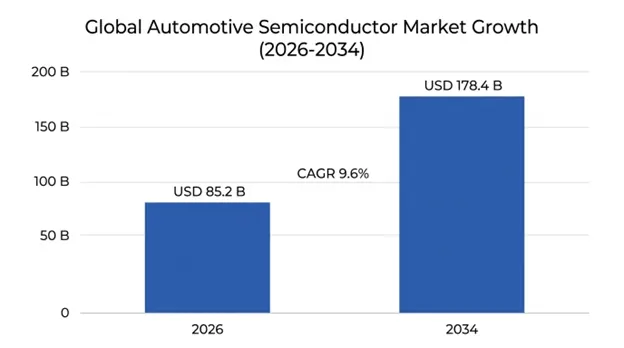

The global automotive semiconductor market size was valued at USD 76.5 billion in 2025 and is projected to reach USD 85.2 billion in 2026, expanding to USD 178.4 billion by 2034, growing at a CAGR of 9.6% during the forecast period (2026-2034). This market transformation has been fundamentally shaped by the unprecedented chip shortage crisis of 2021-2023, which caused an estimated USD 210 billion in automotive industry revenue losses and forced the production of 11.3 million fewer vehicles globally, catalyzing a permanent restructuring of automotive semiconductor supply chains, procurement strategies, and vehicle architectures.

The automobile semiconductors sector is an extremely strategic and dynamic component of the worldwide semiconductor market. This growth has been driven by factors such as the rise in electric vehicle adoption, innovations in autonomous driving technologies, and lessons learned from the global semiconductor shortage. Modern vehicles, unlike traditional vehicles that contained 300-500 semiconductor components primarily based on mature nodes, have developed into computing machines containing 1,500-3,000 semiconductor parts, ranging from power devices and high-performance computing chips to sensing and communication components.

The semiconductor shortage fundamentally transformed relationships between automotive manufacturers and semiconductor producers, ending decades of efforts to optimize inventories using just-in-time processes, in lieu of investing in resilience, forming direct partnerships with the foundries, and adopting end-to-end visibility tools along the entire supply chain. Automakers increasingly reduced dependence on traditional Tier-1 suppliers and instead developed direct relationships with foundries through capacity reservations, joint investments in dedicated automotive fabs, and collaborations on custom silicon solutions, joint investments in dedicated automobile fabs, and cooperation on custom silicon optimized for vehicle designs as opposed to merchant semiconductor chips used in consumer electronics.

Market architecture is increasingly not just about traditional revenues for semiconductor products but also large investments in the infrastructure of supply chain resiliency, including sophisticated inventory management systems, cutting-edge analytics for supply chains, alternate sources of supply development, and capacity expansions driven by groundbreaking government policy action. The global semiconductor foundry companies have invested over $350 billion in automotive-related capacity expansion until 2030, while automobile manufacturers have made drastic changes to their car electronics design and architecture, which include minimizing chip diversification, consolidation of electronic control units, and moving towards a software-driven platform.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 76.5 Billion |

| Forecast Value | USD 178.4 Billion |

| CAGR | 9.6% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | North America |

| Segments Covered | By Chip Type, Vehicle Type, Application, Technology Node, Supply Chain Strategy |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, Germany, France, UK, Italy, Spain, China, Japan, South Korea, Taiwan, India, Australia, Brazil, UAE, South Africa |

| Key Market Playes | Infineon Technologies, NXP Semiconductors, STMicroelectronics, Renesas Electronics, Texas Instruments, TSMC, ON Semiconductor, Qualcomm, NVIDIA |

Get more details on this report - Request Free Sample

The primary structural element driving automotive semiconductor market growth is the substantial rise in chip content per car resulting from the adoption of battery electric vehicles and advanced driver-assistance systems, resulting in semiconductor content per vehicle increasing from USD 450 in conventional vehicles to more than USD 1,200 in premium EVs by 2025., with further forecasts estimating semiconductor content to exceed USD 1,800 in 2030, as Level 3-4 autonomy becomes commercially feasible. The growing requirement for power electronics and control units, including silicon carbide-based inverters, battery management systems, onboard chargers, DC-DC converters, and thermal management units, has resulted in a significant increase in semiconductor content.

Advanced Driver Assistance Systems (ADAS) also represent a major growth driver that is equally important, whereby modern ADAS designs necessitate the need for very powerful SoC processors which will be able to perform real-time processing of sensor fusion involving several cameras, LiDARs, radars, and ultrasonic sensors. Moving from conventional driver assistance towards autonomous driving will entail very high computation capabilities, which requires computing performance in the range of hundreds of tera-operations per second. This implies moving from mature node microcontrollers to advanced node HPC, which should be done on the 7nm process node and below.

Software-defined vehicle design principles exacerbate demands for semiconductors, since vehicle makers switch from designs based on distributed electronic control units, which use dozens of different microprocessors, to central domain or zonal controllers that run high-performance application processors equipped with the ability to run hypervisors and multiple virtual machines, and over-the-air software updates enabling post-sale feature enhancements and over-the-air capability upgrades.

Key Performance Metrics:

The automotive semiconductor industry is benefiting from major procurement strategy changes that emerged following the shortage crisis. Automakers are now prioritizing resilience over just-in-time inventory optimization through investments in foundry capacity allocation, multi-sourcing strategies, and strategic inventory reserves. amounting to billions of dollars more spent on semiconductors annually but with assurance of supply which makes the higher costs worthwhile. More than 65% of leading automobile makers were able to forge direct procurement deals with the semiconductor foundries by 2025, cutting out the intermediary role of Tier-1 suppliers for essential chips.

The evolution in procurement has led to investment in a supply chain visibility platform that would enable real-time tracking of demand and supply of semiconductors, bottlenecks through predictive analytics, and planning capabilities that ensure demand visibility of foundries for two to three years compared to quarterly orders. The new inventory management strategy will require that strategic inventories be kept for weeks or months instead of days, thereby incurring more working capital, but at the same time avoiding shutting down production lines, which has costs associated with it, averaging USD 50,000 hourly for automakers.

Supply agreements of an indefinite nature are now a norm when it comes to automotive semiconductors, where there are purchase obligations and technology joint ventures which provide semiconductor suppliers with annuity type of revenues and ensure that automotive producers enjoy secure supplies and participation in product roadmap decisions tailored to automobile needs and not those of consumer electronics.

Supply Chain Transformation Metrics:

The primary limitation on the growth potential of automotive semiconductors is the inherent shortage of capacity at mature process nodes since automotive applications are highly reliant on mature 28nm-90nm processes for microcontrollers, analog chips, and power management integrated circuits which suffer from an ongoing shortage of capacity as a result of the semiconductor industry’s focus on advanced process nodes to support more profitable consumer electronics and cloud data centers. The establishment of capacity at mature process nodes necessitates an investment of USD 15-25 billion along with a three to five-year period, after which qualification for use by automotive manufacturers adds another one to two years to the time frame.

The reality about economics that limits growth in capacity is the fact that node manufacturing at more mature technology nodes is less profitable than node manufacturing at advanced technology nodes, without incentives by governments or contractual assurances from automotive consumers that make private investments attractive. This limits the automotive industry’s ability to migrate commodity semiconductors to smaller process nodes.

Qualification practices in the automotive semiconductor industry create significant impediments to fast supplier diversification, where the automotive electronics council’s AEC-Q100 qualification standards mandate thorough stress testing and long-term reliability testing, making any fast supplier switch impossible in case of supply shortages. Although such qualifications are necessary from the point of ensuring safe and reliable vehicles, they essentially tie automotive manufacturers to specific suppliers for up to 5-10 years of a given vehicle platform's lifecycle.

Opportunities in the market transformation can be seen in the development of SiC and GaN power semiconductors, where SiC power semiconductors have created the possibility for the creation of 800V electric vehicle architecture which offers an additional range of 5-8% when compared to standard silicon-based power semiconductors. This is complemented by the ultra-fast charging capability of over 350kW, greatly enhancing consumer acceptance of electric vehicles. The market size for automotive SiC semiconductors was USD 1.8 billion in 2025 and is forecast to grow at a CAGR of 34% through 2030.

Supply of silicon carbide substrates is a major bottleneck and potential source of huge investments, considering that manufacturing processes involve expensive machinery and long lead times of up to several weeks, even with increasing demands. Companies that vertically integrate operations from SiC substrates, devices, all the way to automotive qualification will reap huge profits thanks to their strategic location in the transition to electricity.

The shift to software-defined architecture in cars results in many opportunities for providers of high-performance computing semiconductors since automotive companies will have to combine several separate control units into a single domain controller, which would require a sophisticated node system on chip technology fabricated using 7 nm process nodes or even smaller. Thus, this will match automotive semiconductor demand with the capabilities of top-notch foundries and will allow for over-the-air feature upgrades.

Vertical integration into the development and design of semiconductors is taking place in the auto industry on an unprecedented level, with top manufacturers such as Tesla, GM, Volkswagen, and Toyota developing their chip designs directly and forming relationships with foundries to create these components without going through third-party automotive semiconductor suppliers. The development of Full Self-Driving computer chips by Tesla proved that designing silicon chips specifically for auto applications could be done at costs impossible to achieve with commercial semiconductor products.

The pattern reflects a serious disruption in the value chain of automotive semiconductors, presenting a chance for foundries and design services, as well as posing a threat to the existing suppliers of automotive chips, who were offering turnkey solutions for customers lacking knowledge of semiconductors.

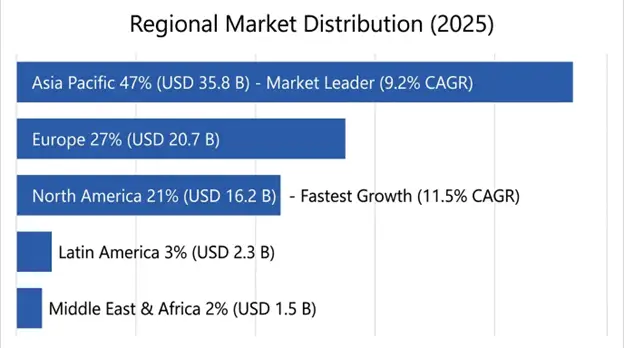

The Asia-Pacific region accounted for the highest market share with USD 35.8 billion in 2025, sustaining an anticipated CAGR of 9.2% until 2034. The reason behind regional leadership is the presence of most global semiconductor fabrication capacities. Taiwan, South Korea, and Japan account for more than 75% of global automotive semiconductor production capacity due to Taiwanese firms such as TSMC, South Korean firms such as Samsung, and several Japanese semiconductor manufacturing companies. China holds the largest automotive market in the world, besides being a leader in EVs.

Regional domination also indicates the major supply chain risk for the occurrence of global shortage effects because disruptions from single factories in the major foundry regions can remove millions of cars from the global market. Although regional car manufacturers have been increasing their capacities to avoid such risks, the issue of geographic concentration still exists.

North America stands out as the most rapidly growing regional market with a forecast CAGR of 11.5% to reach USD 16.2 billion by 2034. Increased growth is associated with significant investments by the government through CHIPS Act and other programs which have spurred over USD 200 billion in private semiconductor investments within Arizona, Texas, Ohio, and New York. North America boasts of its leadership in autonomous vehicle software engineering and artificial intelligence, thereby generating a need for high-performance computing semiconductors and cooperation between technology firms in Silicon Valley and traditional automotive firms.

Automotive firms in the region are leading in direct foundry engagement strategies and customized chip production that reduces reliance on Asia-based semiconductor supplies and exploits advantages from chip innovations.

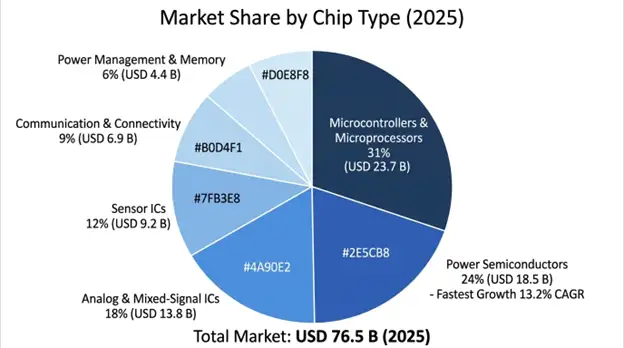

Microcontrollers and Microprocessors take up a major position of 31% in the market with the market value of USD 23.7 billion in 2025 with an 8.4% CAGR over the forecast period till 2034. This type of technology acts as the backbone of computation for all automotive electronic systems ranging from simple body electronics to advanced assistance applications.

Power Semiconductors is the most rapidly growing category at a 13.2% CAGR to reach USD 18.5 billion by 2025, thanks mainly to the increasing demand for electric vehicles with the need for efficient power conversion, battery management systems, and motor controls. The silicon carbide power semiconductors in this category are experiencing growth rates above 30% per annum.

Electric Vehicles remain the fastest-growing category with a 14.8% compound annual growth rate, though with lower volume than ICEV vehicles. The semiconductor consumption in EVs is twice as high as that in internal combustion vehicles owing to the requirement for power electronics, battery management system, and thermal management in such vehicles.

Passenger Vehicles remain the largest category with a share of 68%, valued at USD 52.0 billion in 2025, due to high production volumes around the world and adoption of ADAS and Infotainment systems.

The global market for automotive semiconductors is moderately concentrated within the ranks of existing integrated device manufacturers, where the top 5 players collectively account for about 48% of the revenue derived from automotive-oriented chips, But the competitive landscape in the industry is evolving very fast because of the emergence of fabless tech firms like Qualcomm, NVIDIA, and Mobileye into the high-performance computing markets, along with the influence wielded by foundries via capacity commitments and OEM partnerships.

Competitive advantage today is increasingly becoming contingent on long-term access to foundry capacity, capabilities in wide bandgap semiconductor processing, integrated hardware/software platforms, and direct partnerships with automakers.

April 2026: Taiwan Semiconductor Manufacturing Company (TSMC) started its operation from its specialty technology semiconductor fabrication plant in Dresden, Germany, co-financed by the European Chips Act to manufacture 28nm-16nm car-certified processes for the benefit of carmakers in Europe.

March 2026: Infineon Technologies expanded its manufacturing plant of 200mm silicon carbide wafers in Malaysia and inked deals worth USD 4.5 billion with North American and European manufacturers of electric cars for SiC power devices.

February 2026: NXP Semiconductors introduced its new centralized vehicle compute solution that includes powerful processors together with real-time microcontrollers, allowing car makers to substitute up to 40 of their existing electronic control units with one computing unit.

January 2026: General Motors increased its direct semiconductor sourcing by establishing partnerships with five more foundries and reduced intermediary purchases from Tier-1 suppliers from 78% to 54% while gaining priority capacity.

December 2025: Texas Instruments opened its new factory facility in Sherman, Texas, focused on producing 300mm wafers with mature-node analog and power management semiconductors used in automotive batteries and power conversions.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.