Share this link via:

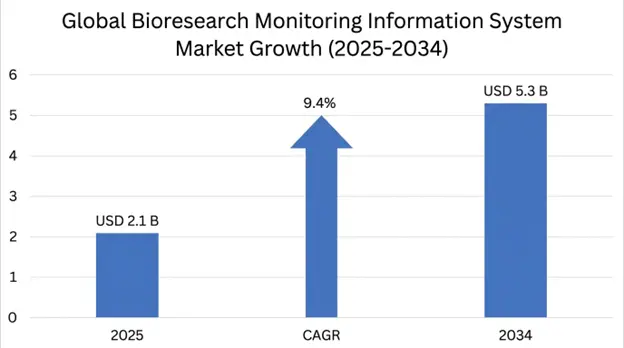

The Bioresearch Monitoring Information System Market size is projected to grow from USD 2.1 billion in 2025 projected to reach USD 2.4 billion in 2026, expanding to USD 5.3 billion by 2034 at a CAGR of 9.4% over the forecast period.

Bioresearch monitoring information systems are complex, integrated digital platforms and regulatory compliance frameworks built to oversee, record and manage the whole life cycle of bioresearch activities under regulatory authority oversight. These systems make sure clinical investigations, preclinical studies and lab research operations fit with applicable federal rules, Good Clinical Practice guidelines, Good Laboratory Practice standards and institutional compliance demands, while dealing with the problems of modern drug research environments.

The base architecture goes further than simple document management, it includes workflow automation that arranges inspection prep activities, follows up on corrective and preventive actions after audit findings, keeps investigator qualification records, watches protocol deviation reporting windows and secures audit-ready documentation that meets evidentiary standards needed during FDA inspections, European Medicines Agency audits and other regulator site visits. Modern platforms mix in risk-based monitoring frameworks, key risk indicator panels, central statistical checks for data quality and fraud spotting, deviation tracking systems, automated alerts and broad reporting across studies, programs and portfolios.

The regulatory landscape for bioresearch monitoring has become much more demanding in the last ten years, with the FDA’s Bioresearch Monitoring Program doing over 1,200 clinical investigator inspections a year across the United States, plus sponsor and monitor inspections that together review thousands of regulated research operations annually. The fallout from compliance failures has grown a lot, with warning letters, clinical holds, import alerts and consent decree actions causing study data rejections, delayed regulatory filings and big remediation bills averaging USD 4.2-6.8 million per case, which creates strong economic reasons for organizations to put money into advanced information systems to avoid compliance breakdowns before inspection.

Today’s bioresearch monitoring information systems use AI-driven risk scoring that looks at several data streams including patterns of protocol deviation, monitoring visit notes, data query rates and investigator site performance measures to flag rising compliance risks before they become inspection findings or data integrity problems. These predictive features mark a move from reactive compliance handling to proactive risk-based monitoring approaches that regulators worldwide support, letting sponsors shift monitoring effort to sites in proportion to their risk, instead of using the same monitoring level for every site regardless of how they perform.

The market includes standalone compliance management tools, integrated clinical operations suites that combine bioresearch monitoring with clinical trial management and electronic data capture, regulatory intelligence services giving timely updates on changing compliance rules, and full professional services like system rollout, validation, staff training and ongoing compliance advice that together cover the range of needs organizations have to stay compliant across complex global research programs.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 2.1 Billion |

| Forecast Value | USD 5.3 Billion |

| CAGR | 9.4% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Segments Covered | By Component, Deployment Mode, Application, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Switzerland, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Veeva Systems, Oracle Health Sciences, Medidata Solutions, IQVIA Holdings, Parexel International, MasterControl Inc., IBM Watson Health |

Get more details on this report - Request Free Sample

The main moving force pushing the market for systems that monitor bioresearch is the steady ramp up of regulatory oversight, targeting clinical investigators, study sponsors, contract research groups and institutional review boards, all working inside the regulated research space. The FDA Bioresearch Monitoring Program has, over time, broadened its inspections with clinical investigator visits topping about 1,200 a year in the United States while the official action indicated results have gone up a lot as reviewers apply tougher tests to informed consent forms, records of sticking to protocols, completeness of adverse event reporting and inventories of investigational products.

Organizations that get an official action indicated find themselves facing serious regulatory fallout, including possible dismissal of study data used in pending marketing filings, required corrective steps under agency watch, and damage to reputation that can complicate future study programs. The money at risk from a single data integrity problem that can void a pivotal trial dataset can climb into 100 million of dollars once you add delayed approval, the price of repeating studies and losing time to competitors in the market. Warning letters tied to data integrity at FDA rose from 12 in 2012 to 87 in 2024, and clinical research organizations picked up about 23% of the citations, showing enforcement is moving beyond the old focus on manufacturing.

The growth of FDA remote assessment abilities, which sped up during the pandemic and now are part of the normal inspection toolkit, has created new compliance needs for organizations to keep electronic records always available and aligned with 21 CFR Part 11 requirements for electronic records and signatures. Systems built specifically to make remote inspection readiness easier have seen strong demand, because many groups realize the old style of heavy pre-inspection paperwork, is not compatible with the short notices of remote assessments.

Key performance signals show the rising regulatory squeeze feeding market demand. FDA clinical investigator inspections held high official action indicated rates around 22% of completed inspections in 2025, and warning letters mentioning bioresearch monitoring shortcomings rose about 34% between 2020-2025. The typical bill to respond to an FDA warning letter for clinical investigation problems reached roughly USD 4.2-6.8 million including remediation, legal help and regulatory affairs work, creating big pressure inside organizations to adopt systematic compliance management through dedicated information systems.

The progressive sophistication of clinical research programs, pushed by the rise of complex adaptive trial blueprints, decentralized trial approaches and platform protocols that test several interventions at once, and by the globalization of investigatory site networks across many countries with different regulatory rules, has made information management messy, manual compliance steps and disconnected old systems just can’t keep up. Modern drug development programs now routinely involve hundreds of investigator locations across 30-50 countries at the same time, creating compliance monitoring needs that grow much faster as you add sites and more geographic variety.

Global clinical trial site numbers went past 380,000 active sites in 2025, that was about a 42% jump from 2018, driven largely by pushing into emerging markets, while the typical number of countries in a global Phase III program rose from 18 in 2015-31 in 2025, so there are many more regulatory authorities to manage at once. This growth calls for technology platforms that can pull together, analyze and report on compliance status across far flung operations while fitting different regulatory frameworks language needs and cultural factors that change how sites work.

Decentralized trial models, which really took off during pandemic era changes and stayed, have become a permanent piece of the clinical research picture, and they bring new monitoring issues tied to remote consent practices, digital health device data capture, shipping investigational products directly to patients and telemedicine based clinical checks. By 2025 decentralized approaches were used in about 67% of newly started Phase II and III studies, creating new infrastructure needs for compliance oversight that the old site-based monitoring setups weren’t built to handle.

The rising use of adaptive trial designs that include planned interim looks, response adaptive randomization, and smooth Phase II-III handoffs produces documentation needs that are a lot more complex than fixed design studies. These require information systems that can record and sort extra protocol amendment histories, tweaks to statistical analysis plans, and the records around blinding procedures that adaptive designs create during the study life cycle. Such complex operational settings need advanced information systems that provide a single view across distributed networks while keeping up with regulatory standards comparable to traditional centralized research models.

The pharmaceutical and bio research industries are going through a prolonged data integrity crisis that has pushed information system quality from an operational detail to a strategic business must, with regulators worldwide issuing unusually large numbers of enforcement actions about data integrity against organizations whose electronic systems do not produce reliable attributable contemporaneous original and accurate records that meet evidence standards. FDA and MHRA and EMA together have sent hundreds of warning letters, import alerts and GMP noncompliance notices over the last ten years, and clinical research outfits are being targeted more often, as inspectors move data integrity focus into the bioresearch area.

Organizations that put in validated systems for monitoring bio research saw a 64% drop-in audit finding rates versus groups still using manual compliance workflows, and modernization of electronic records management made up about 38% of regulatory tech spending among the top twenty drug firms in 2025. The cost gap between buying compliant information systems and dealing with the fallout from data integrity failures usually favors the proactive buy, since a single import alert or a clinical hold can create remediation bills and business disruption losses that often top the full price of deploying enterprise level compliance systems.

Monitoring systems for bioresearch include strong audit trail features, access controls that stop unauthorized data changes, time stamped logs that let you rebuild all system interactions, and validation approaches proving ongoing fitness for use, addressing the main data integrity needs regulators now expect to see during inspections. These systems act as centralized stores bringing together monitoring plans, risk assessments, deviation logs, corrective and preventive actions, investigator and site performance records and study related monitoring outputs across countries and across silos, building comprehensive audit trails that help defend with regulators and show a systematic oversight approach.

Investing in robust compliant systems reduces inspection findings and lowers regulatory and business risk while creating a single place for evidence, although some organizations still hesitate, thinking short term costs matter more than the bigger potential losses.

The biggest barrier slowing wider use of bioresearch monitoring information systems, especially at small and medium sized research groups and new biotech outfits, is the large resource outlay needed for computer system validation activities that regulators require for systems that make or keep records under FDA rules. Validation under 21 CFR Part 11 and related Good Practice guidance needs a long string of documents user requirements, functional specs, design qualification, installation qualification, operational qualification and performance qualification activities.

The validation lifecycle for enterprise grade bioresearch monitoring systems usually takes six to eighteen months from choosing the system to finishing validation, it demands dedicated project teams with regulatory affairs and quality assurance know how, big IT infrastructure spends, and deep vendor cooperation to get the docs needed for the validation package. Average system validation projects for enterprise bioresearch monitoring systems were about 11.4 months in 2025, while validation related implementation costs made up roughly 28-42% of total deployment spend for groups without a validation setup.

Organizations that don’t have internal validation skills must hire specialist consultants who charge high fees, total spending to validate large company systems can run from USD 350,000 up to USD 1.2 million, and that’s before you add the regular checks and re-validation that come when systems get upgraded or guidance from regulators changes. Small and mid-sized research groups said the validation burden was the main thing blocking adoption in about 71% of surveys done in 2024-2025, this shows the out of proportion hit of compliance requirements on groups with limited money for infrastructure investment.

A transformative market opportunity exists by building and selling AI and machine learning tools made just for bioresearch monitoring, to predict compliance risk, letting groups spot new weak points before they turn into inspection problems, deviations from protocol or issues with data integrity. Right now, most bioresearch monitoring systems work after the fact, they organize and report compliance events once they happen, while the next wave of platforms that use predictive analytics can look at patterns across many data streams to point out sites, studies and processes that show early signs of things getting worse

Algorithms that learn from past inspection results, patterns of findings on monitoring visits, how often protocols are broken, and site performance numbers can produce risk scores. Those scores let sponsors send monitoring effort where it’s needed most, instead of using the same visit timetable everywhere which might give too much attention to low risk places and not enough to sites with real problems. In pilot projects run by three top 10 drug companies between 2023 and 2025, AI-based compliance scoring cut unexpected inspection findings by 41%, and natural language processing used to review monitoring reports matched human expert review about 89% of the time, while processing documents some 340 times faster than manual review.

Global investment into AI tools for regulatory compliance hit USD 680 million in 2025, with bioresearch monitoring being the fastest growing part at roughly 34% yearly growth. The FDA has started using risk-based inspection timing, with its Site Selection Model, which shows regulators are backing predictive risk methods, this brings regulators expectations closer to what the new generation of bioresearch monitoring systems can offer by combining advanced analytics with machine learning integration.

Substantial growth opportunities exist in emerging pharmaceutical markets, where the rise of clinical research activity and the building up of regulatory authorities, and the more common use of harmonized international research rules are making a need for more advanced compliance information systems among local research groups and multinational sponsors who are setting up regional research operations. Countries like India, China, Brazil, South Korea and several Southeast Asian places, have in the last ten years, strengthened their clinical research rules, they adopted ICH guidance’s and put in place Good Clinical Practice rules aligned with global standards and even started active inspection programs that bring similar compliance management needs to those that drove market growth in older pharmaceutical markets.

Site activations for clinical trials in the Asia Pacific went up about 67% between 2020 and 2025, mostly because of more work in China, India and Southeast Asia, and regulatory inspections in the region rose about 89% from 2018-2025, creating a sense of urgency for compliance management among the regional research organizations. India’s Central Drugs Standard Control Organization has notably increased its oversight for clinical research, doing routine GCP inspections of investigator sites and asking sponsors to keep full monitoring records that show ongoing oversight of how investigations are run.

China’s National Medical Products Administration has changed its clinical research rules too, bringing in new drug registration rules that set strict bioresearch monitoring compliance needs for both local and foreign sponsors running clinical studies in China, this has produced urgent demand for compliant information systems among the growing number of organizations aiming for Chinese regulatory submissions. The regional market for bioresearch monitoring information systems grew at about 18.4% annually from 2020 to 2025, well ahead of global market growth, which signals strong momentum for more expansion as rules mature, and trial volumes go up across emerging markets.

The bioresearch monitoring information system area is going through a deep architectural shift as organizations move away from local installed systems that need internal IT upkeep and big version upgrades, toward cloud-native SaaS platforms that push continuous feature updates, elastic capacity to handle variable workloads and built-in disaster recovery that tackles business continuity needs without extra hardware investment. Cloud models have reached widespread buy-in in the regulated life sciences after early worries about data sovereignty security certification and validation approaches for continuously updated systems were mostly resolved.

Cloud-hosted bioresearch monitoring systems made up 58% of new deployments in 2025, up from 31% in 2020 while groups shifting from on site to cloud-native reported a 44% cut in total cost of ownership over 5-year spans, covering infrastructure maintenance and upgrade expenses. The typical rollout time for cloud-natives reached 4.2 months compared to 11.8 months for local deployments accelerating time to compliance value and lowering the validation load through infrastructure qualification patterns and automated software test frameworks.

The regulatory picture for cloud systems has matured a lot, with FDA direction on data integrity and electronic records, plus industry advice from bodies like the Pharmaceutical Inspection Co-operation Scheme and the International Society for Pharmaceutical Engineering, setting out what firms should do to validate and sustain cloud-hosted solutions while meeting records rules. Cloud deployment also enables near real-time collaboration across geographically spread compliance teams allowing sponsors, CROs and investigator sites to work inside shared compliance environments that keep consistent audit trails across all parties, removing document version control headaches and communication gaps that are used to create compliance risks in distributed research work.

The research monitoring info system landscape is moving toward merged platforms that bring together old-style on-site visit management with central statistical checking that keeps looking at clinical trial data, to spot oddities, data points that stand out, and patterns that don’t fit real data generation. This coming together lets risk-based monitoring methods, that regulators have supported in several guidance papers including the FDA note on risk-based monitoring and the Trinucleate BioPharma risk-based quality approach, show a clear shift from systems that only handled compliance paperwork into bigger quality management solutions addressing both rules and data quality sides.

Central statistical checking methods look at clinical data across many things at once, like whether visit dates seem real, lab value spreads, patient reported outcome answer patterns, and clusters of protocol departures, to make site level risk flags that help decide when to schedule visits and to target on-site checking at specific data areas and processes showing statistical oddness. When these analyses are woven into research monitoring info systems, their outputs become part of the monitoring file, showing inspectors that sponsors used organized risk-based ways to allocate oversight resources rather than using the same monitoring routine for every site, regardless of the site-specific risk picture.

North America held the biggest slice of the region, about USD 890 million in 2025 and is expected to expand at roughly 8.9% CAGR through 2034. That lead comes from how much pharma and biotech research and development is packed there, with the United States running the largest clinical research operation in the world, counting more than 85,000 active clinical investigators, around 3,200 institutional review boards and thousands of drugs, biotech and medical device firms that fall under FDA Bioresearch Monitoring oversight. The regulatory set up is quite advanced, with detailed guidance papers, active enforcement programs and clear expectations for compliance which push organizations to buy information systems that can show they manage compliance in a systematic way.

The US alone makes up about 84% of the North American market value, helped by the FDA’s busy inspection program which did 1,847 inspections across investigators, sponsors, monitors and IRBs in fiscal 2025, the big financial risks when compliance fails in the world’s largest drug market and the fact that many global pharma headquarters and research teams are located there, so North American rules become de facto global norms for multinationals. Pharma and biotech R and D spending in North America hit about USD 312 billion in 2025, keeping pressure on the need for compliance management systems, and among the top fifty North American drug companies, adoption of bioresearch monitoring information systems reached 94% in 2025, while growth now is more from mid-market and newer biotech players.

The market also benefits from a mature network of regulatory affairs people, compliance advisors and tech vendors who know FDA bioresearch monitoring inside out, so firms can set up sophisticated compliance programs backed by specialist services. Public payer spending on clinical research oversight and regulatory work grew to notable levels, supporting the infrastructure investments needed to roll out comprehensive bioresearch monitoring information systems at academic medical centers and research institutions that take part in federally funded trials.

Asia Pacific came out as the fastest growing regional market with a projected CAGR of 11.2% through 2034 and reached USD 380 million in 2025. The regional expansion is pushed by a very quick rise in clinical research activity across China, India, Japan, South Korea and Southeast Asian countries combined with stronger regulatory authorities that build compliance management needs like those in mature markets. The region has an enormous diversity of patients, a heavy disease burden, including many conditions high on the list of global clinical programs, and cost‑ competitive research infrastructure, that together have drawn big multinational clinical programs, bringing international compliance norms and the related information system needs into local research organizations.

China is at the front of this regional growth, with about 38% market share, driven largely by the National Medical Products Administration’s overhaul of the clinical research rules through new drug registration regulations, which put strict study oversight tracking requirements on both local and foreign sponsors running clinical investigations in China. The expansion of China’s clinical research market, backed by government moves to push pharmaceutical innovation and to align rules more with international standards, has created big demand for bioresearch monitoring information systems able to handle compliance paperwork that fits both Chinese and international rules within single global compliance setups.

In 2025 Asia Pacific diabetes prevalence hit 206 million adults, that is roughly 38% of the world burden, and this produces strong demand for clinical research in metabolic conditions, while uptake of anti-vascular endothelial growth factor treatments rose 156% between 2020 and 2025, showing fast adoption of advanced therapies that need sophisticated trial oversight. The area benefits from large ophthalmology hospital networks and clinical research groups pioneering high-volume delivery models that keep quality yet reach cost levels that allow access in price sensitive markets, creating need for scalable study oversight tracking information systems supporting efficient compliance management across wide site networks.

Component Insights

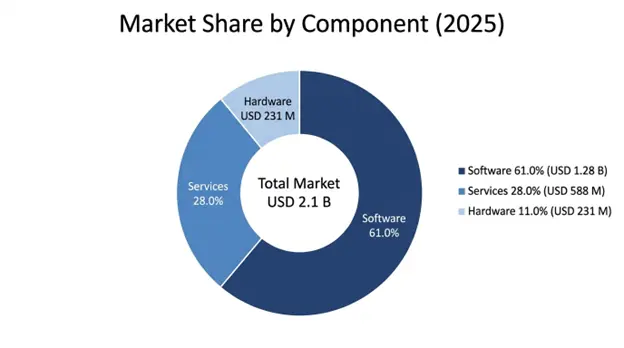

Software tools make up the main part, about 61% of the market, worth USD 1.28 billion in 2025 and they keep growing at a compound annual growth rate of 9.8% through 2034. This part covers platforms for managing compliance, apps to be ready for inspections, systems that keep audit trails, modules to track corrective and preventive actions, regulatory intelligence services and combined suites for clinical quality management, which together are the tech base of organizational bioresearch monitoring programs. The part benefits from subscription-based income that repeats, giving predictable streams, continuous growth of capabilities via regular platform updates and strong customer stickiness because switching is costly with validated regulated systems.

The software area includes main bioresearch monitoring information system platforms that give centralized compliance management, analytics and dashboard pieces that let you see compliance status in real time across global research operations, integration and API layers that let them talk to electronic data capture systems and clinical trial management platforms, plus reporting and document control modules that produce audit ready papers meeting inspection rules. Newer platforms increasingly bring in artificial intelligence and machine learning for predicting risks, natural language processing for automated review of monitoring reports, and workflow automation, which cuts down manual compliance tasks, though sometimes the pieces don't fit perfectly.

Services account for 28% of the market share at USD 588 million in 2025, and include system implementation, validation of computer systems, staff training and consulting for compliance, managed services and ongoing support that help organizations to roll out and keep bioresearch monitoring information systems running effectively. The services segment shows strong growth driven by rising system complexity, expanding regulatory demands that need specialized know-how and the increasing preference among mid-market organizations for managed service setups that shift day to day responsibility to specialist vendors. Implementation and configuration work tackles the technical and regulatory needs for putting validated systems into regulated settings while validation and compliance work makes sure systems meet rules for electronic records and data integrity.

Hardware parts represent 11% of market share at USD 231 million in 2025, mostly covering secure server infrastructure, dedicated audit trail devices and peripheral equipment that support bioresearch monitoring operations, although growth is limited by the ongoing move toward cloud-based deployment models that reduce the need for premise hardware. Organizations that keep on premise deployments need dedicated infrastructure that supports high availability operations, full data backup and disaster recovery plans and security controls that meet regulatory requirements for protecting clinical trial data and personal health information.

Deployment Mode Insights

Cloud based deployment commands 58% market share valued at USD 1.22 billion in 2025 growing at 11.3% CAGR through 2034 reflecting the accelerating move from on premise systems driven by lower total cost of ownership faster implementation timelines, continuous capability updates and improved disaster recovery capabilities. The segment benefits as regulatory guidance has matured supporting cloud deployment for regulated systems, and there is more comfort with software as a service models after successful projects in nearby life sciences areas, plus the operational gains of cloud platforms when managing research programs spread across regions.

Cloud deployment lets organizations scale system capacity up or down dynamically based on clinical program needs, avoiding the big upfront infrastructure costs that on premise setups require while continuous security updates automatic backups, and global access supporting international research. Cloud native platforms include built in integration features that make it easier to connect with other cloud based clinical ops systems, reducing the complexity and cost of keeping integrated compliance environments across many vendors and platforms.

On-premises deployment keeps 31% market share at USD 651 million in 2025, mainly serving big pharmaceutical companies, those with already established local IT setups and strict rules about where data must stay, or complex connections that are handled best by putting systems nearby. This area sees a slow loss of share as remote platform features get better and regulators gradually accept cloud like deployments across most markets, though firms that already put a lot into their own hardware may stick with local deployments to squeeze more value.

Hybrid models make up 11% of the market, they serve organizations that need the ability to keep some data and apps local while using remote platforms for certain tasks like worldwide teamwork, heavy analytics work or backup and disaster recovery. Hybrid approaches let organizations move step by step from local systems toward cloud-native platforms while still following rules about where data must live and the company's own policies for handling sensitive information.

Application Insights

Regulatory Compliance Management is the biggest application segment with 34% of the market, valued at USD 714 million in 2025 and growing at about 9.6% CAGR through 2034. It covers things like inspection readiness management, tracking of regulatory correspondence, monitoring compliance status and support for regulatory submissions applications that meet the basic organizational need to show systematic compliance with bioresearch monitoring requirements. This application sees universal demand across all types of organizations doing regulated research and has a direct tie to the financial fallout from compliance failures which can lead to study data being rejected, delays in approvals and large remediation costs.

Clinical Trial Monitoring applications make up about 27% of the market at USD 567 million in 2025, and they serve the operational management needs of overseeing clinical investigations including tracking protocol deviations, managing monitoring visits, maintaining investigator qualification records and handling the trial master file. This segment shows strong growth, driven by rising trial complexity, wider uptake of risk-based monitoring approaches that need more advanced data management capabilities and the spread of decentralized trial models which require better oversight of operations distributed beyond the traditional site-based monitoring frame.

Data Integrity and Quality Management software tools hold about 19% of the market share at USD 399 million in 2025, meant to cover the critical need to keep audit trails and stop people from changing data without permission and to show compliance with data integrity rules that regulators stress more during inspections. These tools include deep audit logging user access controls, capabilities for electronic signatures and validation frameworks that help keep systems in line with 21 CFR Part 11 and other related rules for managing electronic records.

Pharmacovigilance and Safety Monitoring systems make up around 12% market share at USD 252 million in 2025, they support adverse event reporting and the finding of safety signals, plus the regulatory safety reporting tasks that are core parts of clinical research compliance. These systems tie into clinical data management platforms to catch safety info, automate the reporting workflows and keep full documentation of safety oversight activities that regulators expect to see during inspections.

End-User Insights

Pharmaceutical and biotech companies make up the biggest group, about 52% of the market, valued at USD 1.09 billion in 2025 and growing at roughly 9.2% CAGR to 2034. This group covers large pharma firms, mid-size specialty drug makers, and newer biotech outfits that together run most of the regulated bioresearch under FDA and other global regulators. There is strong financial reason to spend on compliance systems, given how much revenue is at risk if approvals are blocked, a single data integrity issue can wipe out key clinical trial datasets worth hundreds of millions in development spend.

Big pharma creates heavy demand because of their complex worldwide research work, hundreds of trials at once, thousands of investigator locations, dozens of countries, they need enterprise level platforms that manage compliance at scale. New biotech companies are a growing slice, as venture and public money let smaller teams run advanced clinical programs, needing professional grade compliance tools that once only big pharma could afford.

Contract research organizations, about 24% share at USD 504 million in 2025 and the fastest growth, with 10.4% CAGR to 2034. CROs have special compliance headaches, juggling monitoring duties across hundreds of client programs at the same time, with mixed regulatory rules, so there is strong demand for scalable IT systems that let them handle compliance across multi-client, multi-program portfolios. This segment rides the trend of outsourcing clinical work, drug companies relying more on specialist providers for trial conduct, while keeping sponsor oversight.

Academic and research institutions are about 14% of the market, USD 294 million in 2025, including university hospitals, government labs, and non-profit research groups running clinical studies with federal funds or industry sponsors. They face rising regulatory inspection and compliance needs like commercial sponsors but often with tight budgets for infrastructure, so low-cost compliance solutions that can be run and kept up without big internal IT teams are in demand.

Medical device and diagnostic makers cover about 10% at USD 210 million in 2025, serving companies running clinical studies for device approvals, test validation, and combo product work that must meet FDA Quality System Regulation plus clinical research rules. These firms often run smaller trials than drug companies but face similar regulatory oversight, creating need for flexible platforms that can support different study types and approval routes efficiently.

The global bioresearch oversight information system market shows a moderate concentration, with six main firms controlling around 52-58 % of market value through broad product portfolios that cover many ways of delivery and rule applications and extensive clinical development experience, established ties with pharma company compliance groups, and capable implementation skills that help ensure product quality and meeting of regulations. Competitive difference comes from how complete a platform is, addressing several compliance areas inside one system, regulatory know how shown by successful inspection support, the ability to link with nearby clinical operations systems, quality of implementation help including validation assistance and help managing change, and how total cost of ownership is positioned which together shape customer choices in markets where switching costs, once systems are validated, keep customers for longer.

Competition is getting stronger as the usual clinical trial management system sellers move into bioresearch oversight features, by building internally and by buying other companies, while niche compliance management sellers widen their platforms to cover nearby clinical operation’s needs, making a convergence toward wide clinical quality management platforms that handle bioresearch oversight plus broader clinical operations management. This coming together gives chances to vendors who can deliver joined up solutions, but it also puts pressure on specialists that only focus on compliance functions.

Recent moves show the market evolving toward full platforms that include artificial intelligence features, cloud native designs, and joined compliance management across clinical operations, drug safety and quality management areas. Vendors who put money into predictive analytics, natural language processing and automated compliance monitoring are getting edges because they can offer proactive risk approaches not just reactive reports, which matches what regulators expect for systematic risk-based oversight.

March 2026: Veeva Systems said it released Vault BioPharma Monitoring, an AI assisted module for bioresearch monitoring built into the Vault Clinical platform that uses machine learning based risk scoring algorithms trained on inspection outcome data to produce predictive indicators of compliance for clinical investigator sites. The module also has automated regulatory intelligence updates that try to translate new FDA guidance into system configuration needs and includes natural language processing to do automated analysis of monitoring visit reports, so it kind of flags issues and trends.

February 2026: Oracle Health Sciences got an FDA acknowledgement for its cloud hosted clinical trial management platform compliance with the updated 21 CFR Part 11 guidance, this lets customers cite Oracle infrastructure qualification docs in their own validation packages and reduces the validation work customers need to do for cloud deployments substantially, supporting Oracles push to speed up cloud adoption with simpler validation paths.

January 2026: IQVIA Holdings completed the purchase of a specialized inspection readiness software firm for USD 215 million, folding in the company’s AI powered document review and inspection simulation features into IQVIAs wider regulatory affairs tech portfolio and growing its bioresearch monitoring information system to include predictive compliance risk assessment plus automated workflows for inspection preparation.

December 2025: Master Control Inc launched an updated bioresearch monitoring compliance suite that adds natural language processing for automated review of monitoring visit reports, enabling sponsors to pull out standardized compliance metrics from narrative monitoring documentation and generate near real time compliance trend analysis across global investigator site networks, the platform can integrate with existing quality management systems to provide a more unified compliance oversight.

November 2025: Medidata Solutions announced it added centralized statistical monitoring analytics into its Rave platform, allowing smoother data flow between clinical data management and bioresearch monitoring compliance functions and supporting combined risk-based monitoring workflows that are more in line with FDA and ICH E6(R3) expectations for systematic oversight approaches.

List of Top Companies of Bioresearch Monitoring Information System Market

Global Bioresearch Monitoring Information System Market Segments

By Component:

By Deployment Mode:

By Application:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

12 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.