Share this link via:

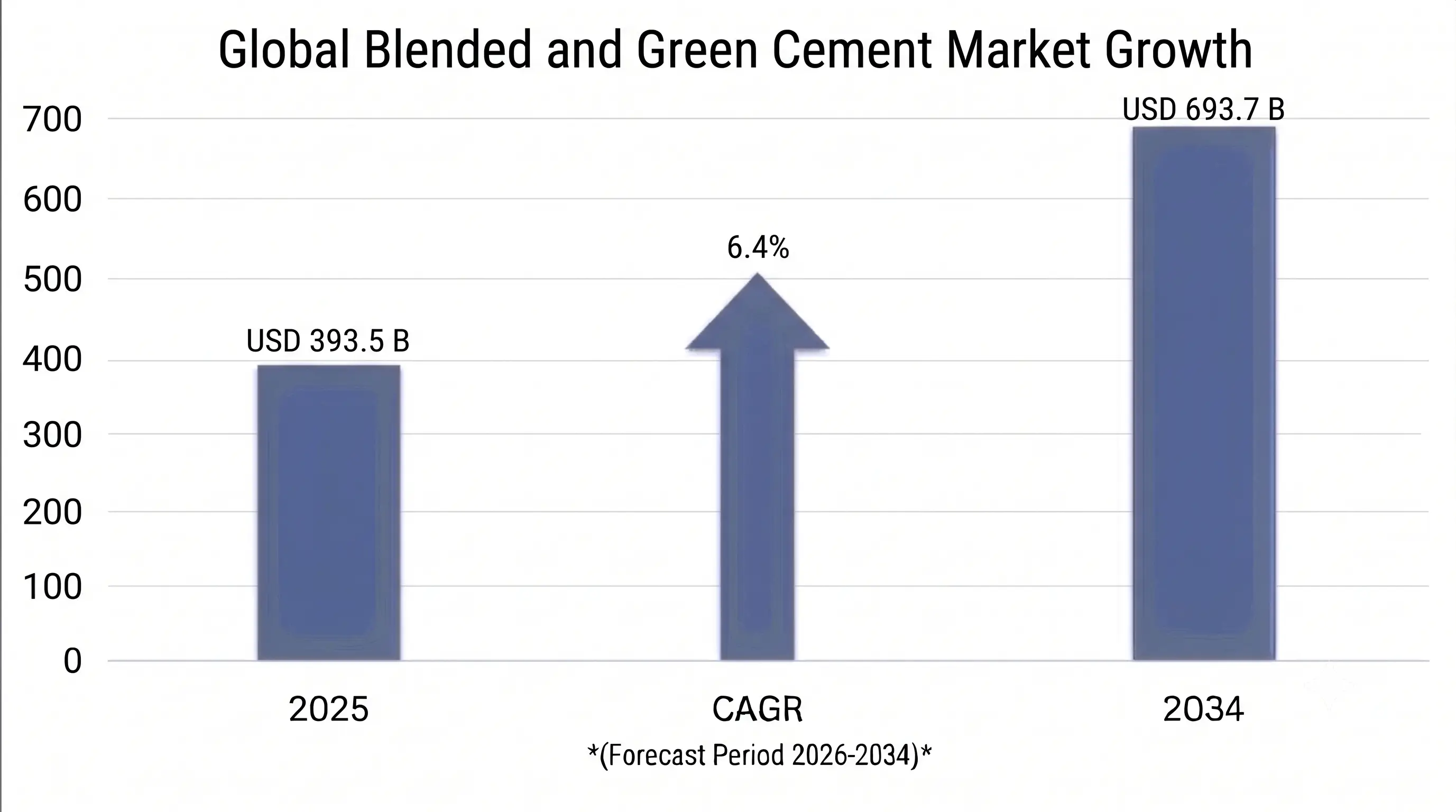

The global blended and green cement market size was valued at USD 393.5 billion in 2025 and is projected to reach USD 421.8 billion in 2026, expanding to USD 693.7 billion by 2034, growing at a CAGR of 6.4% during the forecast period (2026–2034).

Blended cement and green cement are a revolutionary development in the science of construction materials that are designed to solve the biggest environmental problem faced by the cement industry and provide the best performance properties for contemporary use in construction. These energy-efficient hydraulic binders systematically replace energy-intensive Portland clinker with supplementary cementitious materials such as fly ash from coal combustion, ground granulated blast furnace slag from steel production, silica fume from silicon manufacturing, calcined clays, natural pozzolans and limestone fines, resulting in dramatic carbon footprint reduction. The basic environmental advantage is the reduction in the clinker factor, and it is a direct reduction in CO₂ emissions because the production of one ton of clinker, by the normal calcination of limestone at temperatures greater than 1,450°C, releases about 0.87 tons of CO₂ per ton of clinker.

The technical basis of the performance of blended cement is based on pozzolanic and latent hydraulic reactions, where amorphous silica and alumina in the supplementary cementitious material react with calcium hydroxide released during Portland cement hydration to form more calcium silicate hydrate and calcium aluminate hydrate gels. The secondary reactions occur slower than primary cement hydration and result in an increase in the degree of concrete density and impermeability, which improves resistance to sulfate attack, chloride intrusion, alkali-silica reaction and chemical degradation. The resulting concrete possesses greater resistance to the long-term effects of corrosive exposure conditions such as marine structures, underground structures, and industrial facilities, and has reduced heat-of-hydration, minimized the possibility of thermal cracking when used in large mass concrete projects such as dams, foundations and other large structural elements.

The market includes the growing range of formulations that contain only one supplementary material at 15-40% replacement rate, advanced ternary and quaternary systems with multiple supplementary materials providing a synergic reactivity profile, and innovative technologies that eliminate the use of clinker, such as geopolymer binders and Limestone Calcined Clay Cement - LCC, which feature clinker factors below 50% and perform as well as Portland cement. The current commercial transformation of the market, which is fueling the growth of the market, is driven by the convergence of stringent environmental regulations, carbon pricing schemes, green building certification programs, and infrastructure investment programs, all of which require embodied carbon reduction as a measurable metric for construction materials, while also maintaining structural performance and durability standards for built environments.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 393.5 Billion |

| Forecast Value | USD 693.7 Billion |

| CAGR | 6.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Europe |

| Segments Covered | Product Type, Supplementary Cementitious Material, Application, End-Use, Distribution Channel, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, Poland, China, Japan, India, Australia, South Korea, Indonesia, Vietnam, Thailand, Brazil, Argentina, UAE, Saudi Arabia, South Africa, Nigeria |

| Key Market Playes | Holcim Group, HeidelbergMaterials, CEMEX S.A.B., UltraTech Cement, CRH plc, Buzzi Unicem, Votorantim Cimentos, Dangote Cement, Ambuja Cements, China National Building Material Group |

Get more details on this report - Request Free Sample

A key factor transforming the market for the global blended and green cement industry is the fast adaptation to decarbonization policies and carbon pricing schemes that greatly influence the economics of conventional cement manufacturing processes. Cement production, accounting for about 8% of worldwide CO₂ emissions generated by limestone decomposition and fossil fuel burning, is being increasingly challenged due to national climate targets, industry sector plans to achieve net zero, and carbon border adjustment measures that penalize the use of carbon-heavy products. The EU Carbon Border Adjustment Mechanism that will be enforced starting 2026 entails carbon pricing at rates equal to the current prices within the EU Emission Trading System – about EUR 60-85 per metric ton of CO₂, placing conventional cement at an immediate economic disadvantage compared to its low-carbon counterpart.

The adoption of green procurement policies at both national and sub-national levels is hastening market transformation through the imposition of the highest allowable levels of embedded carbon content for publicly financed construction initiatives. The US Infrastructure Investment and Jobs Act has provisions known as Buy Clean which demand Environmental Product Declarations and carbon intensity standards for the procurement of construction material in federal construction projects. Similarly, France, Netherlands, and Denmark have enacted compulsory whole life carbon assessment for their publicly financed buildings and infrastructure. Such policies facilitate the implementation of mandatory criteria that promote blended cements, which can be between 20-50% less carbon intensive than alternatives.

The single most important structural constraint in expanding blended cement sales lies in the geographical distribution, reliability of supply, and consistency in quality of conventional supplementary cementing materials, especially considering the process of decarbonizing those industries as well. The rapid phasing out of coal-based electricity production in advanced economies coincides with the increasing need for fly ash within the cement industry, leading to problems of supply falling short of demand at a time when costs cannot be controlled.

The availability of European fly ash witnessed a reduction of 42% during the period 2015-2025 due to the early shutdown of coal-fired power plants prior to their commitment to climate change. The same is true in North America, where fly ash supplies are being affected by increased competition with natural gas use and expansion of renewable energy sources. Similarly, ground granulated blast furnace slag is subjected to similar problems as steel manufacturers move towards producing steel through electric arc furnace and direct reduced iron processes.

A revolutionary market development can be seen in the fast-track commercialization and globalization of Limestone Calcined Clay Cement technology, where the use of calcined clay with abundant availability of kaolinitic clays and limestone allows for reducing the clinker factor to around 50% without having to rely on any by-products from depleting coal-powered electricity generation and steel production plants. The LC3 technology ensures mechanical performance and durability comparable to ordinary Portland cement through the combination of reactive alumina and silica derived from the calcined clay, as well as carboalumination phase formation with limestone fines.

The strategic importance of LC3 is not limited to CO2 emissions reduction; it also lies in securing raw materials because the deposits of kaolinitic clay are found all around the world in regions that experience the highest cement demand growth and shortages of conventional supplementary materials. Countries such as India, Cuba, Ethiopia, Brazil, and various countries in Africa have rich sources of clay that can be used to produce LC3, allowing cement manufacturers to expand into these markets using LC3 technology.

The blending cement sector is witnessing an ongoing revolution from conventional two-component blends to more complex blends involving three and four components using combinations of supplementary cementitious materials based on compatible particle size distribution, reactivities, and chemistry to obtain synergies of performance which go beyond the properties of any single constituent material. Modern blending technology employs computer simulations of cement hydration reactions and microstructure formation to formulate desired blends meeting specific performance objectives.

Technologies such as artificial intelligence-powered mix designs, real-time process monitoring, and predictive performance models for quality control are contributing to more precision in terms of control of the blending of the cements and applications, eliminating the performance variability that used to play a role in the conservative approach to specifications. By analyzing large amounts of data about concrete performance and training machine learning programs on these bases, engineers can predict the performance of the blended cements under varying curing and exposure conditions.

Asia Pacific controls 68% of the world’s consumption of blended cement and green cement which has been estimated to be worth USD 267.6 billion in 2025 because of its status as the biggest market for construction globally and the largest producer of cement in addition to having favorable policies that favor the use of industrial by-products and decreasing carbon intensity. China and India contribute to 58% of the world’s production of cement, with the blended cement penetration ratio standing at 67-82% respectively.

India’s cement industry is the world leader in terms of adoption of blended cement, with 82% of total output in 2025 accounted for by Portland Pozzolana Cement and Portland Slag Cement products due to BIS standards advocating supplementary materials use and Bureau of Energy Efficiency campaigns providing economic motives for clinker proportion reduction. India’s total annual amount of fly ash from coal-fired power stations at 240 million metric tons ensures a steady supply of supplementary materials necessary for affordable blended cement production, supplemented by government regulations mandating fly ash utilization in construction projects.

China’s blended cement industry is undergoing rapid transformation with the introduction of environmental policies aimed at by-product utilization and lowering carbon footprint, with the Ministry of Ecology and Environment setting obligatory supplementary materials quotas and restricting production capacity of conventional clinker-based cement. Chinese cement producers have managed to bring average clinker ratio of their output to 0.61 in 2025, compared to higher figures globally, due to systematic usage of fly ash, slag, and limestone blends.

Europe is considered the world’s most environmentally advanced blended cement market, where carbon prices are set based on the Emissions Trading System, and where it is compulsory for companies to provide Environmental Product Declarations. Europe boasts highly advanced decarbonization plans and therefore a very fast development of low carbon cement. The blended cement market value of Europe stood at USD 51.7 billion in 2025, and the market share of blended cement was 76%.

European cement industry net-zero plan aims at reducing carbon intensity from 620 kg CO₂/metric ton in 2020 to under 280 kg by 2050 through a series of interim goals that include reducing the average clinker factor to 0.65 by 2030 and 0.55 by 2040. Such a trend will result in binding industrial commitment leading to enhanced blended cements’ adoption, innovations in alternative materials to deal with limitations on fly ash and slag sources, and investments in breakthrough technologies including LC3 and carbon capture innovations.

European companies dominate global leadership in advanced blended cement formulations, which includes research in ternary and quaternary blends, geopolymer technology, and carbon capture innovations. The construction industry in Europe shows exemplary practice in terms of blended cement specifications. Europe is also a pioneer in performance standards, which help develop green building concepts based on innovative cement formulations.

The North American region shows the fastest growth in terms of blended cement adoption due to the infrastructure spending programs by the government, the Buy Clean procurement policy and sustainability efforts taken voluntarily by construction companies, thus providing specifications that push for the use of low-carbon cement. The region’s market valuation stood at USD 42.3 billion in 2025.

USD 1.2 trillion investment of the Infrastructure Investment and Jobs Act provides a huge procurement leverage for setting the embodied carbon standards, as federal agencies create specifications favoring increasingly low-carbon cement mixtures when building transportation, water, energy, and broadband infrastructure. In the United States, such state-based policies that set a mandatory requirement for an Environmental Product Declaration and maximum global warming potential levels are enacted in California, New York, Washington, and Colorado, thus directly encouraging blended cement specification.

Blended cements are seeing major growth investment in North America by manufacturers to meet market demands. There is an ample amount of fly ash supply due to operational coal-fired power stations in the area, an efficient infrastructure of imported slag, and increasing calcined clay production capacity to deploy LC3 technology.

Portland Pozzolana Cement is the most consumed in the world with a 35% market share, valued at USD 137.7 billion by 2025, due to its high usage in India, Southeast Asia, and Africa, as there is an abundance of fly ash in these regions due to the high consumption of coal power, thereby resulting in cost-effective production of the cement along with durable properties due to tropical climatic conditions. It offers better performance against sulfur attacks, alkali-silica reactions, and chloride intrusions, when compared to ordinary Portland cement.

Portland Slag Cement holds a market share of 28% with sales worth USD 110.2 billion by 2025, being used in premium infrastructure constructions such as marine and underground constructions, which require the use of concrete with high durability because of the density of slag cement and its low hydration rate. The ground granulated blast furnace slag with a substitution rate of 40%-70% enhances the strength development and serviceability of concrete.

Limestone Calcined Clay Cement is the highest-growing cement type at 16.8% CAGR through 2034 but from a smaller base of USD 18.9 billion in 2025, owing to increasing commercial adoption, as technology moves from demonstrative to full-scale production phase on multiple continents. The LC3 formula reduces CO2 emissions by 30-40% per tonne as compared to traditional cement with the use of abundant raw materials irrespective of availability of industrial wastes.

Geopolymer cement exhibits immense growth prospects at 18.2% CAGR through 2034 with an estimated market value of USD 12.4 billion in 2025, propelled by increasing commercial interest for zero-clinker cement with near-zero carbon footprint when made using industrial waste material and activated with optimized alkaline solutions. Activator cost, workability issues, and standardization problems still pose major hurdles to its wider adoption.

Fly Ash continues to be the most used supplementary material at 42% of total consumption worth USD 165.3 billion in 2025 in cement use, although there are concerns over availability in developed regions due to reduced production of coal for electricity purposes. The Class F fly ash obtained from the combustion of bituminous coal has excellent content of silica and alumina providing high reactivity. Class C fly ash obtained from sub-bituminous has self-cementing properties that allow high usage in blends.

Ground Granulated Blast Furnace Slag constitutes 32% of the total consumption of supplementary materials worth USD 125.9 billion in 2025, and commands high prices owing to its latent hydraulic properties which provide high replacement capacity without compromising its performance as compared to pozzolanic supplements. Slag cement exhibits high durability in both marine and harsh chemical environments.

Calcined Clay is the quickest growing segment within supplementary materials, with a CAGR of 24.7%, owing to commercialization of LC3 technology and increased awareness regarding use of calcined kaolinite as a reactive supplementary material not reliant upon the availability of industrial by-products that may be constrained within developed nations.

Natural Pozzolan & Limestone Fines are the two segments that together constitute 18% of consumption but have seen rapid growth due to evolving cement specifications for increasing limestone content within blended cements.

The Infrastructure & Civil Engineering application segment is leading the market with a 39% market share worth USD 153.5 billion in 2025, including transportation systems, water supply systems, energy generation plants, and urban infrastructure, which make use of blending cement’s longevity in highly hostile environments. The Infrastructure & Civil Engineering segment has the highest relevance to government initiatives in terms of funding infrastructure developments and procuring low-carbon cements.

The Residential Construction application segment accounts for a 32% market share worth USD 126.0 billion in 2025 owing to increased volume demand due to urbanization in emerging countries with Portland Pozzolana Cement and slag cement being common requirements for the construction of residential buildings, as well as growing adoption of green building certifications in developed countries.

The Commercial Construction segment accounts for an estimated 19% market share at USD 74.8 Billion in 2025 due to faster adoption driven by sustainability policies by corporations, mandatory certification programs for green buildings, and tenants' preference for low embodied carbon building materials.

The Industrial Construction segment holds a market share of 10% and is valued at USD 39.4 billion in 2025 due to the specific applications of cement in industries such as chemical plants, factories, and energy infrastructure that benefit from blended cement chemical and physical attributes.

Ready-Mix Concrete is the leading end-use segment, accounting for 52% of market demand as it is the primary delivery channel for blended cement to the market where specifications and performance are crucial for successful completion of projects.

New Construction makes up 68% of the total demand, while Repair & Rehabilitation contributes 32%. It is important to note that the Repair & Rehabilitation product line shows remarkable growth due to the need to refurbish older infrastructure using durable materials.

The global market for blended cement and green cement is fragmented, and the top ten companies hold around 42-48% of the global production capacity, which is strongly dependent on the region as transportation economics restrict trade distance and local production meets regional demand. Carbon intensity, supplementary cementitious material sourcing, technical service support, verified Environmental Product Declarations (EPDs), and third-party sustainability certifications are key competitive differentiators.

Holcim Group is the market leader in low-carbon concrete solutions, through its ECOPact low-carbon concrete platform, with a comprehensive range of EPDs, covering 85% of production facilities, and through the industry-leading net-zero roadmap with verified intermediate targets. HeidelbergMaterials is differentiated by its world’s first commercial-scale carbon capture project, Brevik, and its EvoBuild low-carbon product range, which reduces carbon intensity by 30-50% in various markets.

The regional leaders such as UltraTech Cement (India), Dangote Cement (Africa) and China National Building Material Group are also doing well by their scale benefit, presence in markets with adequate distribution systems and their strategic position in markets with high growth potential, where the markets for blended cement are gaining momentum due to policy support and infrastructure investment programs.

Advanced technology deployment, such as LC3 commercialization, geopolymer development, carbon capture integration and digital quality control systems for consistent performance delivery under different application conditions and customer requirements, are the strategic differentiations that are increasingly emphasized.

April 2026: ECOPact ZERO ultra-low carbon cement, which features 60 percent supplementary cementitious material content with proven carbon intensity of less than 320 kg CO2 per metric ton, was unveiled by the Holcim Group, aiming to be used in infrastructure projects in Europe and America, where mandatory Environmental Product Declarations are required.

March 2026: The first successful commercial capture of CO2 occurred in the Brevik plant by HeidelbergMaterials, as they were able to capture 380,000 metric tons of CO2 annually, confirming economic feasibility of integrating carbon capture in blended cement production plants.

February 2026: UltraTech Cement established an LC3 plant in Gujarat with a production capacity of 1.5 million metric tons per year of 1.5 million metric tons per annum using locally available kaolinitic clays at costs 12% lower than those for production of Portland Pozzolana Cement.

January 2026: CEMEX formed an alliance with a carbon utilization technology firm in a move aimed at integrating the use of captured CO₂ into precast concrete curing process, with plans to formulate carbon-negative cement for sustainability-oriented projects in North America.

December 2025: The International Organization for Standardization (ISO) introduced ISO 52000-1 for an innovative classification framework of low-carbon cements such as LC3, geopolymer, and multicomponent blends, to overcome specification constraints of advanced blended cement production on the global construction scene.

November 2025: CNBM made an investment worth USD 420 million in supplementary cementitious materials in Guangdong, Jiangsu, and Shandong provinces with a plan to achieve an average reduction in clinker factor of 45% through systematic use of fly ash and slag in China by 2030.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.