Share this link via:

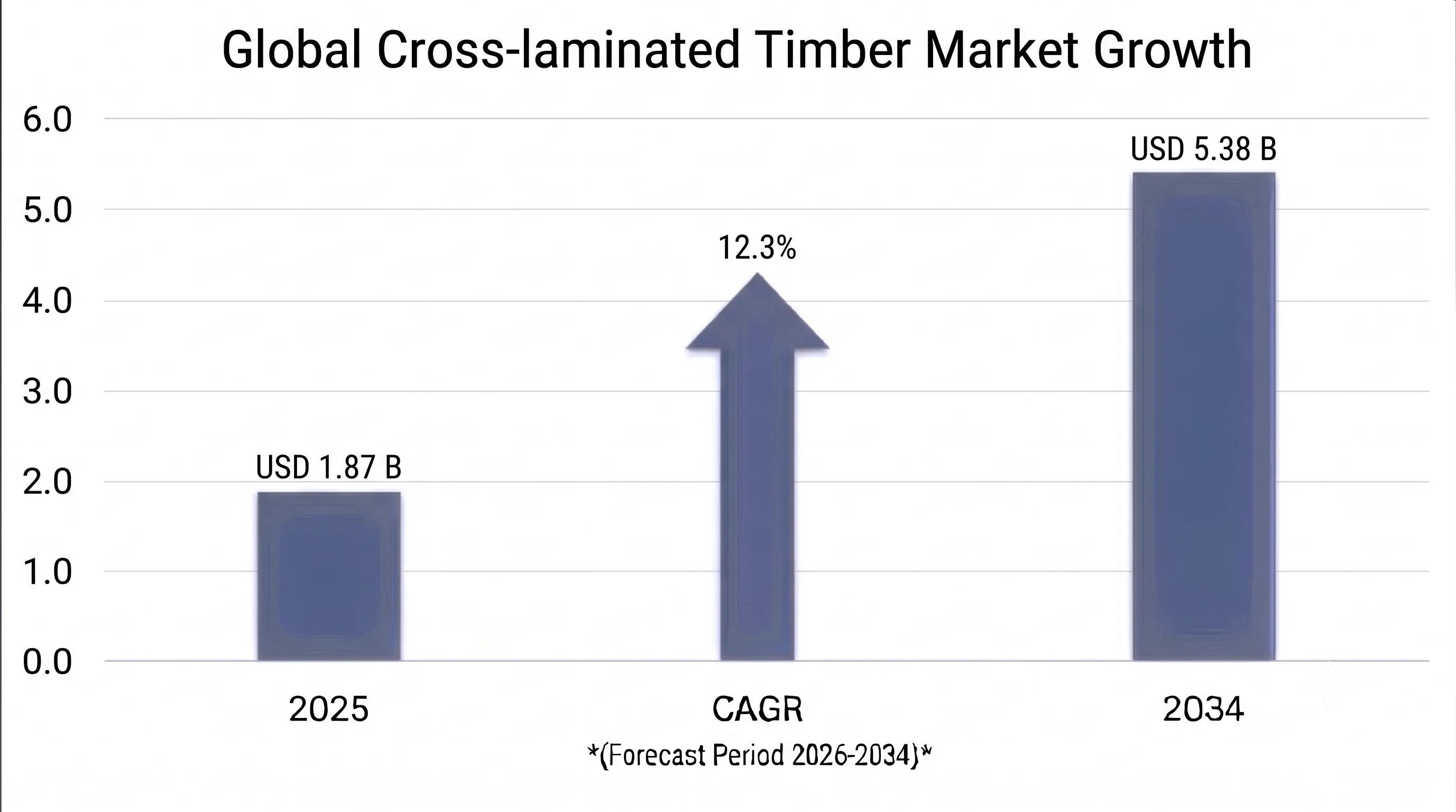

The global cross-laminated timber market size was valued at USD 1.87 billion in 2025 and is projected to reach USD 2.12 billion in 2026, expanding to USD 5.38 billion by 2034, growing at a CAGR of 12.3% during the forecast period (2026–2034).

Cross-laminated timber (CLT) is one of the most revolutionary engineered wood products which has changed the way modern buildings are constructed as it allows timber to rival other materials such as concrete and steel in mid- and high-rise structural constructions. Cross-laminated timber is manufactured using a unique process which involves careful layering of cut pieces of wood at alternating perpendicular angles in 3-ply, 5-ply, 7-ply or 9-ply configurations joined together under pressure with the help of structural glues such as polyurethane, melamine formaldehyde or bio-based binding.

CLT’s importance from an engineering standpoint goes way beyond the realm of standard wooden construction material, as CLT provides a strength-to-weight ratio that is about five times better than reinforced concrete, natural fire protection through its char layer, great seismic resistance due to its flexible connections, and enhanced thermal mass characteristics contributing to energy-efficient buildings. CLT manufacturing enables the production of precisely machined panels with openings for doors, windows, mechanical systems, and connections; this leads to a complete change in the construction process from field fabrication to prefabrication with an estimated 25-40% reduction in construction schedule time.

Such impressive growth of the market is due to the alignment of the pressing need for decarbonization, regulatory developments supporting higher wooden buildings, and revolution in the construction industry towards prefabricated buildings. As such, the construction industry generates approximately 38% of global CO2 emissions considering both operational and embodied carbon, while structural materials contribute approximately 11% of all global emissions due to the energy-intensive nature of their production. Cross-laminated timber acts as a carbon sink, storing approximately 0.9 tons of CO₂ per m³ of timber through photosynthesis. In addition, CLT uses 80% less energy during production than concrete-based construction materials of the same volume, making it a truly climate-positive building material.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 1.87 Billion 12.3% |

| Forecast Value | USD 5.38 Billion |

| CAGR | 12.3% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Europe |

| Fastest Growing Market | North America |

| Segments Covered | Product Type, Layer Configuration, Species, Application, End-Use, Building Type, Treatment Type, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, Austria, Switzerland, France, Italy, Sweden, Norway, Finland, Netherlands, China, Japan, Australia, New Zealand, South Korea, Singapore, Brazil, Chile, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Stora Enso, Binderholz GmbH, KLH Massivholz, Structurlam Mass Timber, Nordic Structures, Mayr-Melnhof Holz, SmartLam North America, Mercer Mass Timber, Hasslacher Norica Timber |

Get more details on this report - Request Free Sample

The most disruptive force behind CLT market growth is the fast rollout of compulsory standards for embodied carbon regulation, whole life carbon assessment, and climate-conscious building policies in which low-carbon building materials take priority over traditional carbon-intensive concrete and steel options. As the contribution of the building industry to CO₂ emissions, reaching roughly 38% in terms of total anthropogenic CO₂ emissions from both operations and material manufacturing processes, becomes a key objective of national and municipal climate action plans, CLT takes a prominent position within those policies.

The regulatory regime of the European Union, comprising the EU Taxonomy for Sustainable Activities and other national legislation like the RE2020 regulation in France and the Future Homes Standard in the UK, sets declining carbon intensity standards, which increasingly makes timber structures the economically rational solution toward compliance. In the United States, there has been a fast-moving uptake of legislation, including the Buy Clean Act in California and Local Law 97 in New York City, among other federal government regulations, which altogether governs trillions of dollar worth of construction annually.

Systematic advancements in international building codes have gradually increased the allowed maximum heights of mass timber buildings from past restrictions of up to 4-6 stories to present regulations of up to 12-18 stories based on prescribed requirements with the use of performance-based design techniques allowing mass timber buildings over 20 stories. The International Building Code 2021 revision has allowed three new types of constructions allowing the construction of mass timber buildings up to 18 stories, being the greatest advancement of timber construction regulations in over a hundred years.

The global pipeline of tall timber projects has grown significantly, with the number of structures having CLT building systems that are taller than 8 stories going from 47 projects being completed in 2020 to 318 projects completed or currently being built in 2025, marking a massive 576% increase in the number of projects, all with much larger average areas per floor. Some examples of landmark tall timber buildings are Brock Commons Tallwood House in Vancouver, Mjøstårnet in Norway, and HoHo Vienna.

The primary factor restricting market growth is of the CLT market includes limited manufacturing capacity on a global basis, confined to manufacturing centers in Europe. The limited capacity of manufacturers in Europe, especially in Austria, Germany, and Scandinavia, supplies substantial amounts of CLT for North America, Australia, and other developing regions using international shipping, thus adding between 8-18 weeks of lead time and an additional cost of USD 200-380 per cubic meter of CLT shipped.

CLT manufacturing is capital intensive, since one requires an investment of around USD 25-45 million in setting up advanced manufacturing plants that include a drying kiln system, finger jointing, hydraulic pressing systems, and CNC machines. Involves third-party product certification, manufacturing audits, and traceability systems.

Significant opportunities exist in the development of smart hybrid structural systems that will allow the effective combination of CLT together with concrete, steel, and smart connections, allowing for the use of the best properties of each material while limiting the disadvantages of each. Concrete-timber composites made by combining CLT panels with concrete toppings provide equal floor span and sound performance as conventional concrete structures but at 40-55% less embodied carbon and 50-65% less building weight.

These hybrid systems facilitate CLT entry into applications that were deemed inappropriate for timber-based structures such as long-span floors in commercial projects, structures in earthquake-prone regions, and buildings that require superior sound performance. The technological complexity of hybrid system design enables manufacturers to differentiate themselves through an integrated solution versus a generic panel product.

The CLT industry is undergoing rapid digital transformation, thanks to total digitalization from parametric design tools, artificial intelligence-optimized algorithms, and CNC machines capable of manufacturing with extreme accuracy and customization potential. Leading CLT manufacturers are utilizing fully digitalized production lines whereby 3D architectural designs are converted into cutting files, connection details, and logistics plans, making possible the production of customized structures for intricate architectural projects without the usual extra costs.

The availability of digital manufacturing technologies will allow CLT fabricators to cater to the rising demand in the design-oriented architectural sector by producing customized buildings characterized by unique geometrical shapes and integrated building systems that can justify the increased expense of using CLT materials due to their premium value and construction efficiency. Machine learning techniques applied to databases containing information about building structure performance will optimize the production process.

Europe dominates the global CLT market with 56% of total demand worth USD 1.05 billion in 2025, resulting from several decades of steady development of CLT technology, production and regulation, which have made CLT a widely used building material in the residential, commercial, and institutional sectors. Europe’s market advantage stems from the high level of integration in its supply chain, which links sustainably managed boreal and alpine forests to advanced manufacturing plants having combined production capacity of more than 2.1 million cubic meters.

Austria and Germany are the global hubs of CLT production, with factories boasting the world’s most advanced and large-scale production lines capable of producing up to 180,000-220,000 cubic meters of CLT panels per annum. This level of efficiency and quality in the manufacture of CLT products has been accomplished through many years of innovation and advancements in processes, machinery, and adhesives that are hard for new players in the industry to match without significant investment.

The UK market is experiencing strong growth because of evolving regulations to allow higher buildings using timber and housing delivery objectives from the government that require new ways of construction. Brexit has allowed greater independence in construction regulations to facilitate the adoption of CLT, which, along with the constant shortage of houses, creates demand for CLT.

North America emerges as the most rapidly expanding market for CLT globally, with expected CAGR of 15.8% up until 2034, attributed to revolutionary changes in building codes, growth in domestic manufacturing capacity, and compelling sustainability motivations such as corporate real estate pledges and green building initiatives. The North American region is estimated to have a market value of USD 458 million in 2025, of which the USA has 74%, while Canada accounts for 26%.

The adoption of the 2021 IBC, permitting mass timber buildings up to 18 stories, has resulted in numerous commercial, residential, and institutional projects involving commercial, residential, and institutional buildings where large technology companies, university organizations, and developers are specifying CLT as a sustainability strategy in their flagship projects. The manufacturing capability domestically was increased by 312% from 2020 to 2025 to a capacity of 720,000 cubic meters per year by adding manufacturing plants by Structurlam, SmartLam, Mercer Mass Timber, and DR Johnson.

The Asia Pacific region serves as an emerging market for CLT worth USD 267 million by 2025 at a growth rate of 13.6% CAGR to 2034. It is being driven by strong CLT adoption in Japan and Australia via different approaches of development, which are based on their respective construction traditions, legal framework, and availability of timber resources. Japan’s adoption of mass timber construction, combined with its long tradition of timber building, combined with favorable policies towards domestic timber consumption and earthquake-proof buildings, has led to CLT adoption.

Australia shows strong market dynamics due to the progressive development of building codes, culture of green building certifications, and successful implementation of show-case projects. Regulations permitting multi-story timber buildings of the National Construction Code, and policy on timber use first implemented by states like Victoria and Queensland, provide a friendly regulatory environment for CLT applications. Geographical proximity of Australia to timber-growing regions of New Zealand provides favorable conditions for further market development.

The largest long-term potential lies in China due to governmental policies favoring wood building construction in specified pilot cities along with rising awareness of the environmental impacts amongst urban construction companies and plantation forests available to produce CLT within the country. Though there is still limited implementation due to complex regulations and conservative nature of the construction sector, pilot projects have established groundwork.

The Adhesive-Bonded CLT leads the world in terms of consumption, accounting for 89% of market share in 2025 valued at USD 1.66 billion due to its outstanding structural performance and dimensional stability. The use of structural adhesive systems such as polyurethane, melamine formaldehyde, and other bio-based adhesives provides equal distribution of loads and makes it possible to manufacture large-scale panels.

CLT with Mechanical Fastenings comprises 8% of the market value, accounting for USD 150 million in 2025 and is expected to grow at a CAGR of 16.4% up to 2034, owing to increased preference for completely recyclable structure systems that utilize wooden dowel, metal fastening, or hybrid system of fastening in place of chemical bonding.

Hybrid CLT systems account for 3% of the market yet enjoys the fastest compound annual growth rate of 22.8%. This rapid growth is due to the emergence of innovative technologies where CLT systems have been designed together with concrete toppings, steel joints, and composite materials.

5-Ply CLT represents the largest configuration segment with 44% market share valued at USD 823 million in 2025, providing optimal balance between structural capacity and material efficiency for floor and roof applications requiring spans of 5-8 meters with panel thicknesses of 160-200 millimeters. This configuration serves most residential and commercial applications while maintaining manageable panel weights for standard construction equipment.

3-Ply CLT represents a 26% market share of USD 486 million in 2025, suitable for wall panels, structures requiring relatively lower spans, and budget-sensitive projects in which panel thickness can meet the structural demands. The three-ply panels represent the most affordable choice for CLT and are widely used in residential buildings.

7-Ply CLT represents 19% of the market in 2025, amounting to $355 million by growing at a rate of 15.2% CAGR up to 2034 owing to increased demand in tall timber constructions that use large capacity panels for longer span lengths and load capacities in commercial tall structures. Seven-ply panels with thicknesses of 220–280 mm meet high structural requirements in buildings beyond eight stories.

9-Ply and Above Panel Structures constitute 11% of the market share catering to specific applications like long span roof structures and load-bearing transfer structures and seismic resistant designs.

Spruce accounts for 46% of species utilization because of Europe’s dominance in producing high-quality CLT panels where the Norway spruce offers an ideal balance of strength, dimensional stability, and adhesive qualities needed for CLT production.

Douglas Fir holds a 24% market share, mainly due to North America’s dominance in producing CLT panels made from the Pacific Northwest Douglas fir, which performs better in terms of density and strength compared to spruce.

Pine has a market share of 17%, being cost-effective in regional markets but still delivering enough structural strength to be used in domestic and low-complexity commercial construction.

Mixed Softwood has a 9% market share, allowing the producers to minimize the use of resources and keep structural integrity through engineered combinations of different wood species.

Hardwood CLT has a 4% market share but is forecasted to grow at a CAGR of 21.7% up to 2034 due to its development in the tropical areas and special applications that require increased surface hardness and/or acoustic insulation qualities.

The global CLT industry is moderately concentrated, with the European firms have a technological edge and strong exporting capacity, whereas the producers in North America and the Asia Pacific region quickly increase their production capacities for rising domestic consumption. The ten leading global producers account for about 54-61% of the total production capacities, with high concentration of Austrian and German firms that have developed manufacturing expertise and certification capabilities through decades of experience.

Stora Enso dominates market share leadership via diversified mass timber product lines, significant production capabilities in Europe, and smart investment in the North American market with increased production to address rising demand there. Binderholz offers the greatest single-site capacity for CLT panels in the world and leverages its strengths through low cost-volume and specialized technical support for advanced building projects.

Competitive advantage increasingly depends on digital fabrication capabilities that can work with advanced geometry designs, technical services to facilitate design integration, sustainable documentation to comply with green building standards, and full-service capabilities. Partnerships have been key to facilitating optimal mass timber structures and project delivery methods through integration of all partners in the process.

April 2026: Stora Enso made a USD 320 million investment in CLT capacity at its European plants, expecting an annual capacity boost of 240,000 cubic meters by 2028 to cater to the fast-growing commercial and tall timber sectors using automation technology.

March 2026: The International Code Council issued updated requirements for the 2027 International Building Code, allowing mass timber buildings to rise to 25 stories on a performance pathway basis. This is a major step forward in regulation for tall timber structures and has led to major pipeline development.

February 2026: Mercer Mass Timber has commissioned North America’s most modern CLT manufacturing plant in Washington, which can produce 160,000 cubic meters annually, with its own glulam facility and digital manufacturing capabilities serving the Pacific Coast construction market.

January 2026: The Japanese Ministry of Land, Infrastructure, Transport, and Tourism has ratified new building codes that allow for CLT to be used up to 14 floors high, thus making Japan the leading regulatory framework in Asia Pacific for mass timber.

December 2025: KLH Massivholz has made an important announcement about their successful innovation in hybrid CLT-concrete structures where they have been able to maintain the same structure integrity as any other concrete system but with 45% less carbon emission.

November 2025: The Australian Green Building Council introduced improved CLT credits under its Green Star rating program by offering additional points for structures built with mass timber that have verifiable carbon storage capacity and sustainable timber forest management.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.