Share this link via:

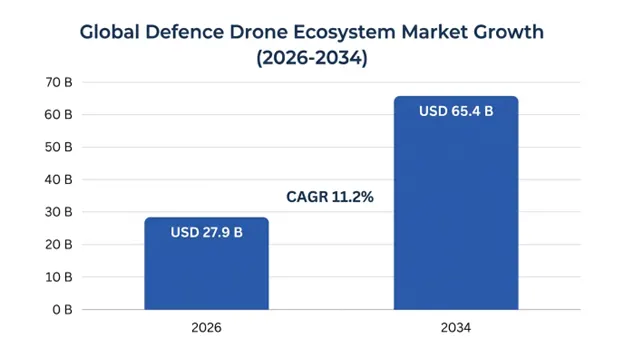

The global defence drone ecosystem market size was valued at USD 24.8 billion in 2025 and is projected to reach USD 27.9 billion in 2026, expanding to USD 65.4 billion by 2034, growing at a CAGR of 11.2% during the forecast period (2026-2034).

Defence drones constitute a vast, inter-dependent grid of unmanned aerial systems, secure communication networks, ground control stations, and autonomous AI software, all designed to execute critical military missions across modern warfare domains. This ecosystem has grown to include integrated systems for combat, including persistent surveillance, precision strikes, electronic warfare, and collaborative autonomous operations, all integrated into multi-domain command-and-control frameworks.

In recent wars, unmanned systems have proven to be pivotal in their ability to engage high-value targets, saturate enemy air defense systems and deliver persistent situational awareness on the battlefield at a lower cost and risk than manned platforms. The Ukraine conflict, in particular, has made the world aware of the effectiveness of drone warfare with Loitering munitions and tactical UAVs have effectively destroyed millions of dollars’ worth of tanks and armored vehicles at a tenth of the cost.

Increasingly, the technological foundation of this ecosystem is software-defined, using AI and machine-learning algorithms that enable swarms ranging from dozens to hundreds of platforms to navigate in GPS denied environments autonomously, identify and classify targets in real time, and coordinate swarm operations under unified command structures. Modern defence drones use electro-optical/infrared sensors, synthetic aperture radar, signals intelligence packages, electronic warfare payloads and kinetic effectors in modular, open-architecture systems for quick capability insertion and mission adaptation.

This is not just about platform purchase, but also comprehensive lifecycle support, such as software updates, hardening against cyber threats, payload modernization, training services and maintenance contracts that can last for decades and yield recurring revenues. Acquisition models are shifting from traditional procurement models to capability-as-a-service frameworks across defense ministries around the world, with blurred lines between manufacturers, integrators, and service providers, and steady technology advancements to address the challenges of a changing threat landscape.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 24.8 Billion |

| Forecast Value | USD 65.4 Billion |

| CAGR | 11.2% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Platform Type, Component, Application, Operation Mode, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Italy, Israel, Turkey, Ukraine, China, Japan, India, Australia, South Korea, Taiwan, UAE, Saudi Arabia, Brazil |

| Key Market Playes | General Atomics Aeronautical Systems, Northrop Grumman, Lockheed Martin, AeroVironment, Elbit Systems, Israel Aerospace Industries, Turkish Aerospace Industries, Anduril Industries |

Get more details on this report - Request Free Sample

The battlefield success of unmanned systems as force multipliers across modern warfare domains has validated UAS platforms as indispensable weapons systems. Massive volumes of operational data have been collected during the current conflict in Ukraine to illustrate the effectiveness of using drone systems from the simplest commercial quadcopters modified for munition strikes to the more sophisticated loitering munitions, which can neutralize armored vehicles at standoff distance. The Ukrainian and Russian forces have launched hundreds of thousands of UAS, with tangible battlefield effects that have reshaped threat scenarios and acquisition agendas for NATO allies and partner countries around the world.

The cost-effectiveness ratio has been found to be strategically important; loitering munitions cost USD 30,000–80,000 while the cost of kills against armored systems is USD 2–6 million, which is a paradigm shift from the traditional force-on-force economics. The geopolitical threat environment has been the impetus for emergency procurement programs led by European countries, with the NATO members alone having collectively allocated more than USD 8.4 billion for extra funding in their drone procurement programs for 2023–2025. Fighter aircraft designs are also undergoing a radical shift as the use of unmanned systems becomes a core rather than an ancillary part of the strike force, and as air forces plan to have increasingly more missions flown by autonomous strike and reconnaissance platforms.

Artificial Intelligence and Machine Learning are the most technologically significant growth drivers which, when integrated into defense drones, make them increasingly autonomous and capable of navigating, identifying targets, assessing threats and operating in coordination with other platforms without constant human supervision. This technological advancement overcomes critical operational constraints such as bandwidth limitations; operator workload associated with multiple concurrent platforms and mission continuation in the event of electronic warfare scenarios where communication links could be degraded or lost.

Autonomous navigation using computer vision, sensor fusion and terrain-relative navigation allow drone operations in GPS-denied areas, which mitigates and neutralizes a key operational vulnerability of early-generation drones that rely on GPS navigation. The miniaturization of edge-computing hardware enables onboard processing of sensor data for target recognition, collision avoidance and other tactical functions in real time without the need for communication links with the ground-based processing infrastructure, thus significantly enhancing operational resilience and minimising signature exposure.

Autonomy is expected to remain the most heavily funded R&D capability area and will be the first to be implemented in swarms, with programs such as DARPA's Offensive Swarm-Enabled Tactics and collaborative combat aircraft efforts, frameworks for coordinated autonomous flight being developed, to enable dozens to hundreds of individual platforms to act together in response to changing threat scenarios such that an individual human operator cannot handle.

The continued erosion of the post-Cold War security environment has led to defense budget growth in all major economies, with unmanned systems receiving a disproportionately large share of rising defense budgets due to their proven effectiveness in operation and attractive cost-benefit ratios in comparison to manned systems. Strategic competition across Indo-Pacific countries is creating distinct procurement drivers, with China's seemingly fast and aggressive development of military drones such as Wing Loong and CH-series strike drones, naval unmanned systems and rumored swarm initiatives sparking significant investment across the region by its allies and partners.

In fiscal year 2025, the United States Department of Defense (DoD) Replicator Initiative made a specific USD 1.8 billion investment in the procurement of autonomous systems, with a focus on fast fielding thousands of attritable systems to offset the numerical advantage of potential adversaries. Since the Ukraine conflict, European defense transformation has increasingly focused on drones, while collective European Union spending on unmanned systems on unmanned systems is increasing by 94% from 2022-2025.

The biggest challenge facing the defense drone market is that these systems are extremely susceptible to advanced electronic warfare (EW) and cyber-attack that can lead to loss of platform or compromise mission effectiveness. Defense drones possess significant attack surfaces, such as communication links between drones and ground stations, as well as among interconnected control systems, and between drones and other networked systems; data links carrying drone sensor data and mission data; navigation systems relying on satellite data that can be jammed and spoofed; and the growing networked architectures in which drones are linked to bigger command and control networks.

The Ukraine conflict provided a clear example of the effects of Electronic Warfare on drone operations, with both sides implementing advanced jamming equipment which interfered with GPS navigation, communication links and in some cases resulted in autonomous return-to-home missions that made it difficult to achieve mission success and secure the platform. These vulnerabilities require ongoing investment in quantum-encrypted communications, anti-jam navigation systems, and cybersecurity protection that can be costly and difficult to develop and use.

Leading platform and technology providers are subject to complex export controls and export-controlled international arms transfer agreements that limit market access and hinder global market growth, especially in the development of more sophisticated autonomous systems and precision strike systems. The Missile Technology Control Regime (MTCR) provides multilateral export controls for systems more than 300 km in range and greater than 500 kg in payload weight, limits transfers to approved recipient countries, and mandates long and complex authorization processes.

American exports of defense drone systems and components are regulated by the United States International Traffic in Arms Regulations, which provide for approvals to be made within 12-36 months for key platform transfers, and limit technology transfer for autonomy algorithms, electronic warfare systems and precision navigation capabilities. These limitations allow for competitors from countries with less restrictive technology transfer policies to gain market share in countries where delivery speed and more favorable terms are significant commercial advantages in emerging markets.

The increasing number of military and commercial drones in the airspace in conflict zones and sensitive airspace is generating a growing market for the C-UAS technologies, which are an interlinked growth opportunity within the defense drone market. The counter-drone market refers to detection systems such as radar, radio frequency sensors, and electro-optical cameras; identification and tracking systems; and defeat systems, such as electronic jamming, directed energy weapons, kinetic interceptors, and net capture systems.

However, the global counter-drone market is valued at USD 5.2 billion in 2025 and is expected to expand to 24.1% CAGR through 2034, well outpacing the primary drone market growth because of threat recognition lag and the continued threat will lead organizations to recognize their vulnerabilities before implementing proper protection measures. Military counter-drone procurement accounts for about 71% of the total market value, and critical infrastructure protection, border security, and other areas are increasing.

Representing the convergence of traditional aerospace capabilities with autonomous systems technologies is a transformative market opportunity for developing collaborative combat aircraft and loyal wingman systems that fly in close coordinated formations with manned fighter aircraft as force multipliers. The United States Air Force Collaborative Combat Aircraft program, Australia's MQ-28 Ghost Bat, and the United Kingdom's Future Combat Air System (Future Air Sea Lanes) are projects of at least semi-autonomous platforms that can perform suppression of enemy air defense, electronic warfare, sensor extension, and weapons carriage missions.

The platforms are at a significantly lower capability and lower cost level than traditional surveillance drones, featuring low-observable airframes, sophisticated electronic warfare packages, and A.I. autonomy stacks that allow the drone to operate autonomously within given mission parameters set by a human commander. The USAF is seeking to acquire more than 1,000 collaborative combat aircraft through 2030, totaling a procurement of more than USD 6 billion.

The defense market is seeing an accelerated development and procurement of low-cost, attritable autonomous systems that are expendable in a high threat environment and provide meaningful combat effects through mass and coordinated tactics. An attribute of an attritable system is that it is designed to be expanded, giving the operators operational persistence from a limited number of elements and a superior number of systems to overload enemy defenses.

This is accelerating the shift towards more sophisticated production methods such as 3D printing airframes, using commercial off-the-shelf components, and software-defined capabilities which allow for production to scale quickly and at lower costs. The operational concept includes distributed decision making among swarm members, allowing a collective response to a changing threat environment and coordinated engagement tactics that outperform that of a high value platform.

Naval forces around the world have been rapidly moving towards the integration of unmanned aerial, surface and undersea systems into the naval architecture, thereby extending the boundaries of the defense drone market beyond air domain applications and building multi-domain unmanned ecosystems. Unmanned surface vessels with surveillance sensors, weapons systems, autonomous undersea vehicles for intelligence collection and mine countermeasures, and coordinated aerial-maritime operations are all growing areas of procurement of technologies that are key components of the drone ecosystem, such as autonomy algorithms, sensor payloads and communication architectures.

The United States Navy Task Force 59 showcased multi-domain unmanned system integration in operational environments, including coordinated surface and air platforms to support maritime domain awareness and threat response. Comparable initiatives from key naval forces signal increased capital flows into unmanned maritime systems, which are all part of the larger addressable market for defense drone ecosystem solutions and offer cross-domain operational synergies.

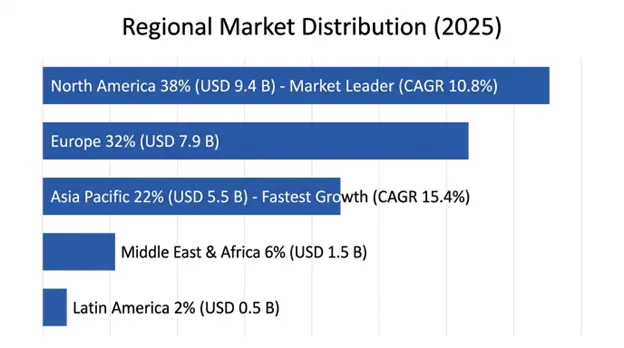

North America remained a leader in terms of market size at USD 9.4 billion in 2025, with a forecast CAGR of 10.8% till 2034. The United States' share within North American defense drones market accounted for 91%, supported by its largest defense budget, focus on development of next generation autonomous systems, and broad spectrum of missions involving global force projection and homeland security missions. The United States has the most versatile and advanced arsenal of military drones that cover strategic, tactical, and advanced autonomous cooperative combat systems.

The Department of Defense Replicator Initiative can be regarded as a doctrine change, focusing on accepting platform expendability in exchange for platform proliferation and operational persistence, thus leading to purchases of small-sized, low-cost autonomous platforms from traditional primes, and tech-focused defense companies. The Department of Defense initiative has diversified the industrial base, including not only aerospace firms but also software-focused tech companies developing AI and autonomy capabilities.

The Asia Pacific region is expected to grow at the fastest regional CAGR of 15.4%, attaining revenues of USD 6.1 billion by 2034. The drivers that influence regional growth include strong great power strategic rivalry where the drone development efforts of China form a key threat driver for procurement by competitors and are among the largest markets within the region. China had 45,000 military drones deployed across the various branches in 2025. The Wing Loong series, CH-series drones and the stealth combat drones formed the most advanced drones within the Chinese drone fleet.

Japan underwent extensive defense reforms, leading to the acquisition of General Atomics MQ-9B system for maritime patrols, and developing programs to develop indigenous combat UCAVs. Japan was spending USD 2.4 billion on unmanned systems in fiscal year 2025, which represents a whopping 380% rise since 2020.

The Indian defense drone industry offers a significant growth opportunity in its own right because of the need to maintain security at borders and on the seas, along with efforts toward developing a local defense drone industry. Procurement of the MQ-9B Predator under a USD 3.99 billion deal helped lay the groundwork for future high-end usage.

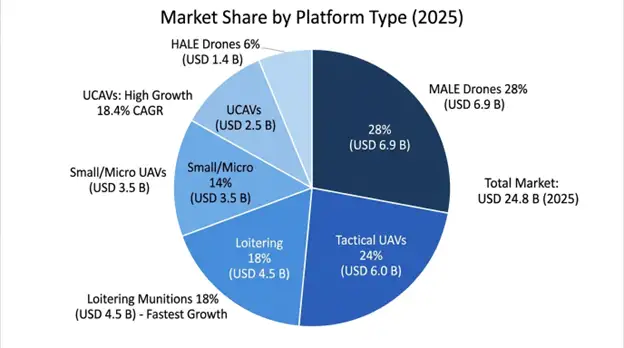

The Loitering Munitions category will be witnessing strong growth on account of the validation of cost-effective precision attack potential of these platforms on battlefields. This category of platforms integrates the ability to remain aloft for extended durations along with attack capability, which provides the operator with the advantage of lingering over the targeted area prior to deciding to attack. These platforms offer the flexibility of attack not available with traditional munitions.

Unmanned Combat Aerial Vehicles will continue to enjoy robust growth at a rate of 18.4% CAGR. Traditional strike platforms as well as collaborative combat aircraft, which work along with manned fighter jets as multipliers, comprise this category.

AI Software and Autonomy is the fastest-growing component segment with a CAGR of 26.1% up until 2034, owing to the shift from hardware-based to software-based functionalities. The segment includes software algorithms used for target detection, autonomous navigation technologies, and swarm management software.

Payloads & Sensors represent the biggest revenue in absolute terms at USD 7.8 billion by 2025, growing at 12.4% CAGR. Payloads & Sensors include electro-optic/infrared sensor packages, SAR, SIGINT payloads, and electronic warfare systems that decide the success of the platform mission.

Intelligence, Surveillance & Reconnaissance hold the largest application market share of 44%, amounting to USD 10.9 billion in 2025, signifying the essential nature of persistent aerial surveillance in modern warfare. This application involves integration of sensors with a variety of collection technologies on one platform.

Combat & Strike Operations hold the highest growth rate of 21.2% CAGR during 2025-2034, due to the widespread use of loitering munitions and development of collaborative combat aircraft that allow precision strikes.

The market for global defense drone ecosystems displays a concentrated landscape in terms of existing defense contractors, unmanned systems developers, and new technology companies exploiting artificial intelligence and software solutions. The leading ten firms in this market make up about 58–64% of the revenues earned from the market. Competitive advantage is built around experience in deploying systems, software sophistication in automation, payload capabilities, established government connections, and economies of scale to offer competitive pricing.

Conventional aerospace primes rely on their strength in systems integration, strong procurement networks, and capability to handle multi-billion-dollar programs, while new firms capitalize on their software-defined, AI-driven, and autonomous networking technologies, which compel existing aerospace primes to enter aggressive joint ventures and mergers.

March 2026: General Atomics Aeronautical Systems successfully integrated next-generation artificial intelligence target recognition software on all MQ-9B systems for autonomous target detection even without GPS and ground station links.

February 2026: AeroVironment was awarded a contract worth USD 1.1 billion by the U.S. Army for Switchblade 600 loitering munition systems in rapid fielding programs.

January 2026: Anduril Industries raised USD 500 million in Series F funding round; funds will be utilized for scaling Lattice autonomy software as well as increasing production capacity for attritable platforms.

December 2025: Turkish Aerospace Industries handed over the first set of Bayraktar TB3 carrier-borne systems to the Turkish Naval Forces that are capable of arrested landings on board the TCG Anadolu aircraft carrier.

November 2025: Shield AI performed BVLOS autonomous operations using its Hivemind software in a contested electronic warfare environment.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

22 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.