Share this link via:

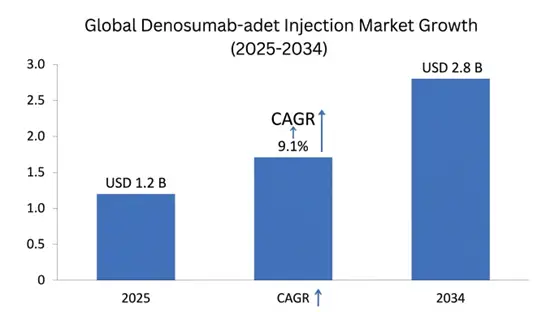

The global Denosumab-adet Injection Market size was estimated at USD 1.2 billion in 2025 and is projected to reach USD 1.4 billion in 2026, expanding to USD 2.8 billion by 2034, growing at a CAGR of 9.1% during the forecast period.

Denosumab-adet is a kind of biosimilar monoclonal antibody, made to target and stick very specifically to the receptor activator of nuclear factor kappa-B ligand RANKL, that cytokine that controls how osteoclasts develop and work and survive in the process of bone renewal. By neutralizing RANKL with strong binding, it stops the meeting between RANKL and its receptor RANK on osteoclast precursors and on mature osteoclasts, so it breaks the molecular chain that causes bone loss and gives a marked antiresorptive effect that quickly raises bone mineral density in both the dense cortical and the spongy trabecular parts of bone.

The uses of denosumab-adet cover two main clinical areas with different dosing plans to deal with bone problems across the spectrum. For metabolic bone disease, the 60 mg subcutaneous shot given every six months is a core therapy for postmenopausal women at high fracture risk, for men with primary or secondary osteoporosis, and for people who lose bone because of long term corticosteroid treatment. For cancer supportive care, the 120 mg monthly subcutaneous schedule is used to prevent skeletal related events such as pathological fractures, spinal cord compression, high calcium from cancer, and the need for radiation or surgery in patients with bone metastases from breast, prostate, lung and other solid tumors, and in multiple myeloma patients with lytic lesions.

Commercially denosumab-adet matters beyond simple drug sales, it fits into the wider health care ecosystem by creating value through biosimilar competition which can cut treatment costs while keeping similar effects to the original biologic. As health systems around the world face rising costs for specialty biologics, the biosimilar denosumab-adet offers important ways to save money and at the same time keep patient access to modern bone changing treatments that have shown better results than older oral bisphosphonates in high-risk groups. The market meets big unmet needs in aging populations where osteoporosis affects over two hundred million women worldwide and bone metastases happen in about seventy percent of advanced breast and prostate cancer patients, so demand stays high for accessible effective bone protection approaches.

The biosimilar status of denosumab-adet brings market effects, with patent expiry timing for original products, regulatory routes for complex biologics, and health system actions that push biosimilar use through formularies and competitive tenders. Clinical trials have shown equivalent exposure and similar pharmacodynamic markers of lowered bone turnover and bone mineral density gains compared to the reference denosumab, giving the regulatory basis for market entry and helping doctors feel confident about switching. The subcutaneous route, needing only two injections a year for osteoporosis, gives clear adherence benefits versus daily pills while the strong clinical evidence for reduced fracture risk and prevention of skeletal related events makes denosumab-adet an important piece of current bone health care plans.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 1.2 Billion |

| Forecast Value | USD 2.8 Billion |

| CAGR | 9.1% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Europe |

| Fastest Growing Market | North America |

| Segments Covered | By Application, Strength & Formulation, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Sandoz Group AG, Samsung Bioepis, Celltrion Inc., Fresenius Kabi, Biocon Biologics, Teva Pharmaceutical Industries |

Get more details on this report - Request Free Sample

The primary structural force pushing the denosumab-adet market to grow is the fast rise in osteoporosis and low bone mass related fragility fractures among aging populations worldwide, with the International Osteoporosis Foundation estimating one in three women and one in five men over age 50 will have an osteoporotic fracture sometime in the rest of their life. The move toward older age structures in developed markets combined with longer life spans creates a compounding effect where the absolute count of people at high fracture risk keeps growing even when age specific fracture rates stay about the same. Hip fractures are the worst clinical and economic outcome of osteoporosis, they carry about 20–24% one year mortality in women and 32–37% in men and more than half of survivors end up with lasting disability, with direct hospital costs averaging around USD 44,000 per admission.

Clinical data for denosumab based therapy shows strong reductions in fracture risk at several parts of the skeleton. The landmark FREEDOM study found roughly 68% fewer vertebral fractures, 40% fewer hip fractures, and about 20% fewer other non-vertebral fractures versus placebo over three years. These solid efficacy results, together with the convenient twice yearly, subcutaneous dosing that helps with adherence problems seen with daily oral bisphosphonates, make denosumab-adet, especially the biosimilar forms, a good therapeutic option for patients at high risk of fracture. The gap in getting treatment for osteoporosis is still big, with less than 25% of eligible patients worldwide on drug therapy despite clear fracture risk, representing over 375 million people undertreated who could benefit from more accessible biosimilar denosumab-adet therapy.

The financial burden of osteoporotic fractures keeps rising, with direct health care costs in the United States over USD 57 billion per year in 2025 and forecasts up to USD 95 billion by 2040 because of population aging. Health systems are increasingly aware that early drug intervention with proven antiresorptive agents like denosumab-adet can produce big cost savings by preventing fractures, and economic models show favorable cost effectiveness that improves further when biosimilar pricing lowers acquisition costs while preserving the therapeutic effects.

Key Performance Metrics:

The cancer area is becoming a fast-growing vector for denosumab-adet, driven by rising cancer rates and better survival, which means longer times managing bone mets and more focus on bone health as part of whole cancer care. Bone mets happen in about 65-75% of people with advanced breast cancer, 65-80% of those with advanced prostate cancer, and 30-40% of patients with advanced lung cancer creating a large and expanding group that needs long-term bone modifying therapy to avoid skeletal related events that hit quality of life and use a lot of healthcare resources.

Clinical data show denosumab better than IV bisphosphonates at delaying the first skeletal event, with studies reporting an 18% risk reduction versus zoledronic acid in patients with bone mets from solid tumors. Subcutaneous dosing gives practical benefits over IV alternatives, it removes the need for long infusion appointments, reduces kidney toxicity worries that limit bisphosphonate uses in those with poor renal function, and fits into outpatient chemo schedules without extra chair time.

Treatment related bone loss in cancer is another high-growth area, it affects those on androgen deprivation therapy for prostate cancer, aromatase inhibitor therapy for breast cancer and several chemo regimens that speed up bone loss by direct and indirect paths. The growing interest in survivorship care and keeping quality of life long-term pushes more attention to maintaining bone health across extended treatment courses, creating ongoing demand for effective bone-protective approaches like denosumab-adet.

Oncology Market Expansion Indicators:

The third key growth factor is the rising worldwide attention to using biosimilars as a strategy to control specialty drug spending while keeping wide patient access to advanced biologic treatments, and this is getting more intense, more quickly than before. Health systems in richer and developing countries are under steady strain from increasing biologic drug costs; bone-targeting drugs take up a big slice of budgets for osteoporosis and cancer supportive care, and competition from biosimilars can cut those costs a lot. The launch of denosumab biosimilars in parts of Europe showed price drops around 25-45% versus the original product pricing, which gave quick budget breathing room and let more patients get treatment who previously were limited by cost.

Regulatory trust in denosumab biosimilars has risen after in-depth analytical and clinical comparison studies that showed they match the reference products on drug levels in the body, on how they lower bone turnover markers, and on clinical effectiveness. The European regulator and other authorities have cleared several denosumab biosimilars based on solid evidence, and the FDA pathway for complex biologics keeps moving forward with earlier examples for monoclonal antibody biosimilars, creating a generally supportive review environment.

Payers are adding biosimilar preferences into formularies, step therapy rules, and competitive bidding processes that favor lower cost treatment options. Medicare and private insurers are changing coverage to help biosimilar use by putting them on preferred tiers and lowering what patients pay, while hospital systems set up substitution rules for biosimilars that aim to keep clinical results the same, and at the same time make better use of pharmacy budgets.

Biosimilar Adoption Momentum Metrics:

The main clinical limit that keeps denosumab-adet from spreading more, is the known risk of a quick loss of bone mineral density and a rise in vertebral fractures after stopping treatment, when there is no proper follow-up therapy. Studies, both clinical and in real life, have shown that denosumab’s antiresorptive effect goes away fast once you stop, with bone turnover markers coming back to baseline or even above, usually within six to twelve months of the last shot, and that comes with faster bone loss, sometimes falling to levels lower than before treatment.

There are multiple reports of vertebral breaks in people who stopped denosumab and didnt move to another antiresorptive treatment; observational work shows rates around seven to fourteen percent in the year to two years after stopping, versus about one to two percent background, in people who never got treatment. This rebound after stopping causes specific, practical clinical problems, it needs continued monitoring of patients, help to keep them on treatment and carefully planned stepwise therapy using bisphosphonates or other antiresorptive medicines to keep bone protection if denosumab-adet is paused or stopped.

Health care teams must set up strong follow-up systems to keep continuity of care and act quickly if there are gaps, for example when patients miss doses, insurance stops covering the drug, or there are medical reasons to pause therapy. The tricky management of these transitions may make some clinicians hesitate to start denosumab-adet, especially in patients who might not stick with long term treatment or who are likely to have interruptions.

Discontinuation Risk Impact Metrics:

Denosumab-adet treatment has built in risks of low blood calcium, especially for people who already have vitamin D lack, chronic kidney problems, low parathyroid function, or absorption problems that upset calcium balance and so it needs a full check before starting and continued checks, which makes beginning and keeping up the treatment more complex and costly. Very low calcium that needs emergency care happens in about 1.7% of patients on the oncology dose (120 mg each month) and about 0.3% of those on the osteoporosis schedule (60 mg every six months), with more cases seen when calcium and vitamin D are not enough or when parathyroid problems are missed.

Clinical management asks for baseline labs of serum calcium, 25-hydroxyvitamin D, parathyroid hormone and kidney function then proper calcium and vitamin D supplements before treatment and while it continues. Patients should be told about symptoms of low calcium and told to keep up good calcium intake from food and supplements, and providers must set up checks for high-risk people and steps to treat low calcium episodes if they happen.

These monitoring and supplement needs can limit use in primary care places with little lab access, or patient groups who miss follow ups, while adding costs and paperwork that change the treatment economics. In markets that are developing, where lab systems are weak and patient education is limited, the safety checks become real barriers to wide denosumab-adet use even though the drug profile is favorable.

A substantial and largely untapped market opportunity exists in treating bone thinning in men, a condition that affects about 200 million men around the world and is still very much underdiagnosed and undertreated although the clinical outcomes often are worse than those seen in women who have similar fracture risk. Men who break a hip, show one-year death rates of 32–37% which is much higher than the 20–24% seen in women, yet less than 15% of men with fractures from weak bones get drug therapy, compared with 35–40% of women with similar risks. This gap in treatment comes from biases in the health system inadequate screening, and not enough awareness among patients and doctors about how common and serious male bone loss is

Denosumab-adet has regulatory ok for treating osteoporosis in men at high fracture risk, and to prevent bone loss in men on androgen suppression therapy for prostate cancer, so there is a clinical and regulatory base to reach more patients in this neglected group. The ADAMO study showed a 62% drop in new spine fractures in men with osteoporosis who got denosumab versus placebo, giving evidence like results in postmenopausal women and backing guideline suggestions for managing osteoporosis in men

The market is wider than primary osteoporosis, it also covers secondary bone loss in men with low testosterone, long term steroid use, chronic kidney problems and other conditions that speed up bone loss, making a varied group of patients who could gain from easier to get biosimilar denosumab-adet therapy. Health system moves that focus on men’s bone health, like broader screening programs, fracture liaison services and education efforts for providers, open routes for market growth as awareness and diagnosis improve.

Male Osteoporosis Market Potential:

Emerging markets across Asia Pacific, Latin America, Middle East and Africa, are seen as big chance for growth as copycat denosumab-adet medicines allow price setups that fit local health care money and what patients can pay in places that together hold more than 60% of the world’s osteoporosis load but less than 20% of people getting drug treatment. The mix of fast aging populations, more diabetes adding to other forms of bone loss, and wider insurance coverage, creates several demand pushes that the arrival of copies could turn into real market share, even quite quickly.

China is the single biggest spot, with about 69 million people with full osteoporosis and another estimated 210 million with low bone density, yet treatment reaches under 8% of those who could take it, because cost has been the main barrier, and cheaper biosimilar pricing is addressing that systematically. The National Healthcare Security Administration, putting denosumab copies on the national reimbursement lists, removes the main access block for many who before could not afford the brand level prices.

India’s growing market benefits from local factories making denosumab-adet at cost levels that let prices sit 60-70% below the original products, mixed with expanding government insurance programs and doctors getting more aware of bone care protocols. Brazil and other Latin American countries show similar patterns, where the presence of biosimilars together with evolving health systems and an aging population create conditions favorable for bigger uptake.

Emerging Market Expansion Indicators:

The denosumab-adet delivery scene is changing by the rise of more user-friendly auto - injector devices and prefilled syringe systems meant to let patients’ self-administration or have caregiver help, without the need to go to a clinic for the twice-yearly osteoporosis shots or monthly oncology doses. New auto-injector tech brings in safety features like automatic needle retraction and dose confirmation mechanisms, plus ergonomic shapes that cope with limited manual dexterity common in older osteoporosis patients with arthritis or poor vision. Some devices also add digital links for dose tracking and adherence monitoring and automatic alerts to healthcare teams, supporting remote follow up and earlier steps when there are treatment gaps.

Connected injection hardware produces real world adherence data that can back outcomes-based contracting with payers, while giving clinical teams a view into how patients are taking therapy, enabling more personalized support actions. The move toward patient self-administration cuts system costs by removing facility-based injection appointments, and it tends to improve convenience and adherence through flexible dosing options that fit patient preferences and daily life.

Self-Administration Adoption Metrics:

Europe: Market Leadership Through Biosimilar Integration and Healthcare System Innovation

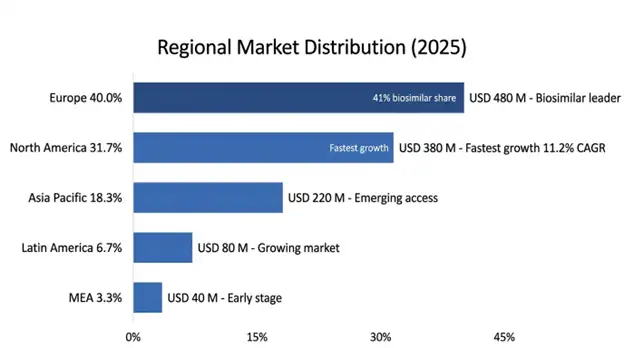

Europe holds the biggest regional slice at USD 480 million in 2025, and a projected CAGR of 8.4% through 2034, this is driven by broad osteoporosis management infrastructure and by established frameworks for biosimilar uptake and integrated health care systems that put cost saving specialty drugs first. The area benefits from mature regulatory routes for biosimilar approval competitive tender systems, that speed up biosimilar use and clinical guideline frameworks which back denosumab-based therapy as the first option for high-risk osteoporosis patients. European systems have brought biosimilar denosumab into formularies using evidence-based review processes that keep therapeutic standards while cutting costs on average 35-45% versus the reference product pricing.

Germany is the largest national market in Europe, with wide statutory health insurance coverage for denosumab-adet therapy and fracture liaison services running in more than 180 hospitals, plus systematic screening programs for people at high risk. The market profits from strong pharmacovigilance systems that track biosimilar safety and effectiveness, physician training programs to build confidence in biosimilars and patient support services that help with sticking to treatment and monitoring.

The UK shows a working mix of biosimilar use, via NHS procurement plans that favor cheaper biologic medicines first but still try to keep clinical quality standards, denosumab copies reached roughly 42% of the marketplace within a year and a half after first approval. France and Italy follow similar paths driven by hospital tender systems and regional health authority pushes to increase biosimilar use to help keep the health service sustainable, although adoption can vary a lot from region to region.

European Market Performance Indicators:

North America: Fastest Growth Through Biosimilar Market Entry and Access Expansion

North America became the fastest growing regional market with a projected CAGR of 11.2% through 2034 and it is expected to hit USD 380 million in 2025. This quickening reflects the recent arrival of follow-on denosumab versions into the United States market after FDA approvals, that set off competitive moves and some formulary reshuffles by pharmacy benefit managers and Medicare Part D plans. The region benefits from broad Medicare Part B coverage for doctors administered subcutaneous biologic medicines, established specialty pharmacy networks and integrated health systems with advanced bone health management routines.

The United States accounts for about 87% of the regional market value driven by high prices for the reference product which create big cost saving chances for biosimilar alternatives, comprehensive insurance through Medicare and commercial plans and a strong osteoporosis care setup including widespread access to dual energy X-ray absorptiometry and specialist knowledge in metabolic bone disease. The switch to biosimilars is producing complex rival dynamics as originator manufacturers react with patient assistance programs and outcome based contracting while biosimilar makers pour resources into market access and clinical support initiatives.

Canada shows a more gradual uptake of biosimilars through provincial formulary listing and doctor education efforts, with Health Canada’s regulatory approach giving confidence via thorough approval steps and post-market safety checks.

North American Growth Acceleration Factors:

Application Insights

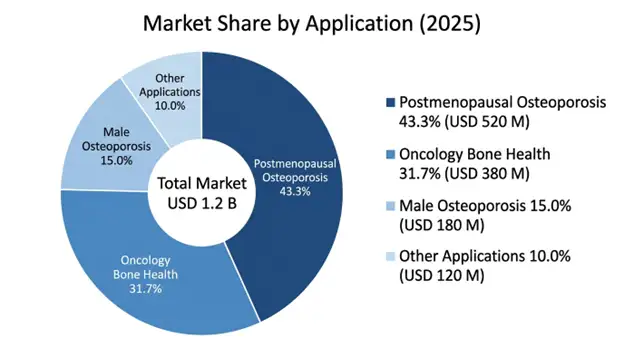

Osteoporosis after menopause dominates the application areas with a market value of USD 520 million in 2025 and a projected 8.7% CAGR through 2034, and it is the largest therapeutic indication because there is a substantial pool of eligible patients, plus established clinical evidence that supports lowering fracture risk and a growing recognition in health systems that osteoporosis is a preventable source of disability and healthcare costs. This area benefits from broad clinical guidelines that recommend denosumab based therapy for high-risk patients, expanding fracture liaison services that systematically identify who need treatment, and a patient preference for twice yearly subcutaneous injections compared with daily oral options.

Bone health in oncology makes up USD 380 million in 2025 with a 9.8% CAGR through 2034, covering prevention of bone metastases and management of cancer treatment induced bone loss, which gains from rising cancer survival, longer treatment times in metastatic cases and more awareness that bone health is part of full cancer care. The oncology area shows higher revenue per patient because of monthly dosing needs, and premium pricing for supportive care measures that help quality of life and cut skeletal complications.

Distribution Channel Insights

Hospital Pharmacies represent the largest dispensing channel at 48% market share valued at USD 576 million in 2025 encompassing oncology infusion centers, endocrinology departments and clinics for specialized care that provide broad patient monitoring adverse event management, and integrated laboratory services supporting safe administration of denosumab-adet. The hospital channel benefits from established reimbursement for facility based biologic administration and a concentration of complex patients who need specialized care.

Specialty Pharmacies make up 32% market share at USD 384 million in 2025 with a 10.1% CAGR through 2034, they are the fastest growing channel as home delivery programs, patient support services and self-administration capabilities widen access while lowering healthcare system use and reducing patient travel needs.

The global denosumab-adet injection market shows a shifting competitive layout, with the original reference product still strong but new biosimilars, from several approved makers, pushing into different regions. Competition is driven by when patents run out and the order of regulatory green lights and by how health systems buy and negotiate prices, which affects who gets market access.

Sandoz Group AG keeps a lead among biosimilar makers thanks to broad development programs, known biologic making skill and deals with hospitals and clinics that help get on formularies and encourage clinical use, they also had earlier entry in parts of Europe and solid clinical evidence for approvals in many places.

Samsung Bioepis holds a good spot with advanced factory methods, teaming up with big drug firms for selling, and a wide IP collection that shields their biosimilar work, their growth plan aims at markets where biosimilars are welcomed and worth more.

Celltrion Inc. uses an in-house model, it makes and distributes itself and uses pricing tactics that let it gain a foothold in wealthy and emerging markets focusing on making therapies more within reach and lower priced, aligns with health systems cost saving goals.

March 2026: Sandoz Group AG stated FDA approval for its denosumab biosimilar with launch planned for Q2 2026, becoming the second denosumab copy approved in the United States and that will add more pressure on the original product market share and on pricing.

February 2026: Samsung Bioepis got the European Medicines Agency ok for its denosumab copy, this one has a better auto-injector device with digital connection features for monitoring adherence and to link into patient support programs.

January 2026: The American Society for Bone and Mineral Research published updated clinical practice guidance recommending denosumab based therapy as first option for postmenopausal women with very high fracture risk, and they give explicit advice supporting use of biosimilars based on established bioequivalence data.

December 2025: Fresenius Kabi launched its denosumab copy in major European markets with price around 45% below the reference product, which triggered hospital tenders and, formulary reshuffling across several countries.

November 2025: A large real world evidence study in The Lancet confirmed similar safety and effectiveness for the biosimilar denosumab compared to the original product in over 15,000 patients, supporting ongoing biosimilar uptake and physician confidence.

List of Top Companies of Denosumab-adet Injection Market

Global Denosumab-adet Injection Market Segments

By Application:

By Strength & Formulation:

By Distribution Channel:

By End-User:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

12 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.