Share this link via:

Press Release

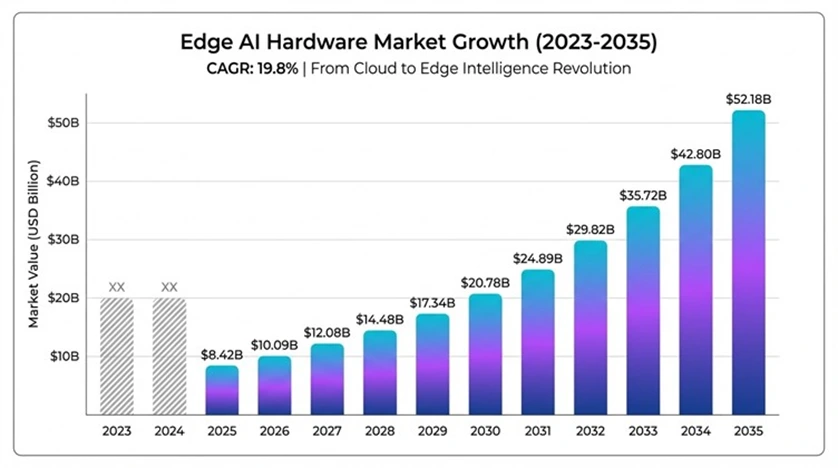

The Edge AI Hardware market is undergoing a paradigm shift in the way we process artificial intelligence. Instead of relying on centralized cloud data centers, we are now taking the processing of AI to the end-user or "edge" of the network, on devices that can process data in real-time and make decisions instantly. The Edge AI Hardware market will be worth approximately USD 8.42B in 2025 and is projected to reach a staggering USD 52.18B in 2035, representing an overall compound annual growth rate (CAGR) of 19.8%.

The rapid growth of this market is greatly influenced by converging technological and market dynamics that support the movement of AI away from the traditional model of being cloud dependent to the autonomous operation of edge intelligence. Edge AI Hardware includes specialized processors, accelerators, and integrated systems built to run machine learning inference, neural network calculations, and AI workloads directly on or next to where the data is created, thus providing a millisecond or less time for response for autonomous vehicles, industrial robots, healthcare monitoring and smart city applications.

Edge AI hardware comprises advanced semiconductor architectures designed for running AI workloads in environments that have strict requirements regarding power limitations, heat dissipation and size due to their location being near where they are being used. While cloud-based AI software requires data to be sent to a Data Centre for processing, Edge AI Hardware conducts inference computations locally which allows for real-time decision making with low latency, less bandwidth usage and better data privacy.

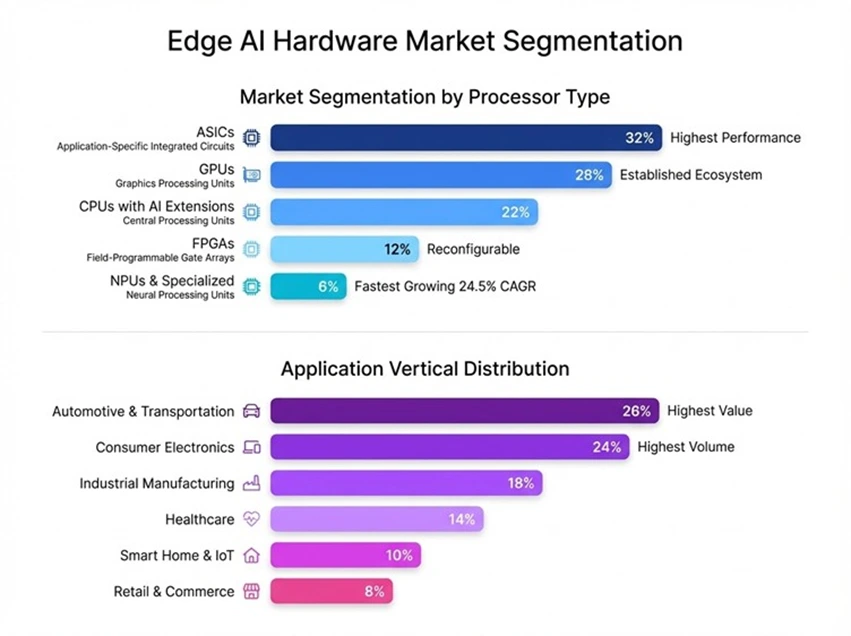

The edge AI technology ecosystem is made up of many different custom Processor Architectures used to process AI and includes Application Specific Integrated Circuits (ASICs) that have been designed for the exclusive purpose of running neural networks, Graphics Processing Units (GPUs) that have been adapted to perform parallel computations for AI, Field Programmable Gate Arrays (FPGAs) that have re-programmable hardware acceleration capabilities, as well as custom Neural Processing Units (NPUs) or Tensor Processing Units (TPUs) that have been optimized for processing machine learning inference workloads.

Modern edge AI hardware is manufactured using advanced semiconductor process nodes at 7nm, 5nm, and emerging 3nm or smaller geometric technologies, utilizing specialized processor instruction sets designed for matrix multiply operations, quantized methods of reducing the size and power consumption of a model, and heterogeneous processor architectures that combine different types of processors to maximize performance per unit of power consumed in doing so.

Edge AI hardware is being used for the highest value and most complex application in the automotive industry as this industry transforms into autonomous driving.

Autonomous vehicles can generate roughly 4 terabytes daily from various sensor systems (cameras, LiDAR, radar, and ultrasonic sensors), requiring near real-time processing for object detection, path planning, and decision making where latency is measured in milliseconds. Waymo, the technology developer of autonomous driving systems, has accrued over 20 million autonomous miles on public roadways and completed billions of miles of simulated driving; each vehicle contains many edge AI processors to carry out complex neural network executions related to perception, prediction and planning functions. Tesla's Full Self-Driving computer was developed internally and can produce 144 TOPS of processing performance due to a dual redundant system, processing eight surrounding cameras at 36 frames per second.

Over USD 15 billion has been invested in the ai automotive market across all leading automotive manufacturers, technology companies and semiconductor companies that develop specialized processors for applications related to autonomous driving since 2020. Leading global manufacturers of automotive semiconductors include NVIDIA, Qualcomm, Mobileye (Intel) and new companies emerging such as Horizons Robotics™ to produce automotive grade edge AI processors that comply with all requirements for safety, reliability and temperature.

The global deployment of 5G networks has brought major changes to edge computing systems which operate through economic systems and technological operations. The worldwide investment in 5G infrastructure by telecommunications operators has reached more than USD 1 trillion which will continue until 2025. Multi-Access Edge Computing (MEC) architecture positions computing resources at cellular network edges, enabling AI workload execution with minimal latency while maintaining connectivity to cloud resources.

Verizon and AT&T and Deutsche Telekom and China Mobile have launched commercial MEC platforms which use edge AI technology for their applications in augmented reality and industrial automation and smart city infrastructure. The combination of 5G connectivity with edge AI hardware has opened doors to fresh application types which are used to face network restrictions.

The European Union's General Data Protection Regulation (GDPR) together with California Consumer Privacy Act (CCPA) and China's Personal Information Protection Law (PIPL) have established strict data privacy rules which push organizations to adopt edge AI processing for their compliance needs. The established regulatory systems limit personal data handling through collection and transmission and storage operations while they impose severe penalties when organizations fail to comply with these rules.

The Edge AI hardware system performs privacy-based computing operations because it processes all sensitive information within local environments which prevents data from reaching cloud-based servers. Smart camera systems perform facial recognition and object detection and behavioral analysis through built-in processing capabilities which send out only non-identifiable data instead of complete video footage.

The Internet of Things (IoT) devices have rapidly increased their deployment which produces new data at network edges while global IoT device numbers should surpass 29 billion by 2030. Industrial IoT has seen major growth because manufacturing plants now use thousands of sensors to track their production lines through equipment monitoring and product quality assessment and operational performance evaluation.

The transfer of huge data amounts from billions of edge devices to central cloud systems creates network bandwidth problems which block time-sensitive applications from achieving their required fast response times. Edge AI hardware solves these problems through its ability to process data on-site while it sends only important information and keeps its ability to respond instantly.

High Development Costs and Technical Complexity

Specialized edge AI hardware development requires large financial investments because ASIC manufacturing needs more than USD 50-100 million for advanced production nodes together with all required mask production and engineering and testing expenses. The semiconductor industry must increase its financial investments because it produces 7nm and 5nm and 3nm nodes through its manufacturing operation.

Power Consumption and Thermal Management Constraints

Edge AI systems need to function with minimal power because their battery-operated devices must operate at milliwatt levels while industrial installations show poor cooling abilities. The high computational needs of AI systems force systems to select between their performance objectives and their available power resources.

Standardization and Interoperability Challenges

The edge AI hardware ecosystem operates without any standardized framework which defines hardware interfaces and software frameworks and model deployment formats. The AI industry operates through multiple frameworks which force developers to build different model versions for every hardware platform that they want to support because of TensorFlow and PyTorch and ONNX and proprietary solutions.

Healthcare and Medical Diagnostics Applications

Healthcare systems now operate through Edge AI hardware which enables all medical data processing requirements for real-time data handling and patient privacy and regulatory monitoring. Medical professionals use Portable ultrasound devices which contain edge AI processors to perform fast image analysis and detect medical conditions and generate clinical recommendations right at the treatment location.

TinyML and Ultra-Low-Power Applications

TinyML technology allows machine learning operations to function on microcontrollers which possess memory between kilobytes and megabytes and operate with power consumption that stays within milliwatts. The market now allows for extensive distribution of affordable AI hardware which connects to more than a billion normal devices that include environmental sensors and wearable technology and smart devices for home automation.

Application-Specific Integrated Circuits - ASICs (32% market share, highest performance)

The ASICs function as specialized edge AI hardware units which operate neural network inference tasks with their purpose-built architectures that deliver maximum energy efficiency. Google Edge TPU operates with 4 TOPS of inference capacity at 2 watts power consumption and Tesla's Full Self-Driving computer operates through customized ASIC units which produce 144 TOPS of performance through their two redundant processing systems.

The ASIC segment commands premium pricing because it offers specialized design elements which produce superior performance characteristics so automotive-grade processors cost between USD 200 and 500 per unit. The system experiences growth because applications need their systems to operate at peak efficiency while running autonomous vehicles and industrial robotics and datacenter edge servers.

Graphics Processing Units - GPUs

The development of GPUs has gone beyond graphics rendering and become multifunctional AI accelerators that take advantage of parallel processing architectures that are more than capable of performing matrix operations, which neural networks heavily rely on. NVIDIA controls the under 572 GFLOPS edges AI GPU market with its Jetson platform (ranging 472 GFLOPS, 5-10 watts) to high performance Jetson AGX Orin (275 TOPS, 15-60 watts).

Central Processing Units - CPUs with AI Extensions

Modern CPUs include dedicated AI workload instructions and accelerators, such as Intel versions Deep Learning Boost, AMD versions Zen architecture optimizations and ARM versions Machine Learning extensions. The Core processors of the 12th and 13th generation produced by Intel also provide AI acceleration with 10-30 TOPS through optimized instruction sets.

Field-Programmable Gate Arrays - FPGAs

The reconfigurable hardware architecture provided by PGA has special benefits with changing AI model’s needs. Arria and Stratix FPGA lines of Intel, and Zynq and Versal systems of AMD have hard IP blocks designed to make AI calculations such as DSP slices and high-bandwidth memory interfaces.

Neural Processing Units and Specialized Accelerators

The latest category of processors is dedicated neural processing unit, which is specially designed to execute neural network inference. The Neural Engine of Apple provides 15-17 TOPS, which provides on-device AI services in iPhones, iPads, and Mac computers. The Qualcomm AI Engine is a hexagon DSP, Adreno graphics and Kryo CPU with the ability to provide up to 75 TOPS on flagship devices.

Automotive and Transportation (26% market share, highest value)

The automotive industry is a high value application industry, as it is being fueled by the implementation of ADAS and the development of autonomous vehicles. The Full Self-Driving computer of Tesla is the biggest implementation of custom edge AI hardware with more than 3 million units deployed. The autonomous vehicles at Waymo use several edge AI processors that perform sensor fusion, perception, and planning.

Consumer Electronics (24% market share, highest volume)

The largest volume segment is consumer electronics, where billions of smartphones, tablets, and wearable devices every year have edge AI processors built in. Apple sells about 230 million iPhones every year, with each model having Neural Engine processors, which support Face ID, computational photography, and machine learning that protects privacy.

Industrial Manufacturing and Automation

The edge AI hardware is used in industrial applications of predictive maintenance, quality inspection, process optimization, and collaborative robotics. Factories provide thousands of sensors that check the health of the equipment with edged AI processors that process patterns and detect anomalies, and the device is going to fail.

Healthcare and Medical Devices

Healthcare apps are fascinating sectors that are developing rapidly due to handheld diagnostic tools, patient trackers, and AI-based medical imaging. Portable ultrasound systems include edge AI processors that help in automatic organ identification and diagnostics support.

Smart Cities and Infrastructure

Municipal governments have applied smart city initiatives using edge AI hardware to control traffic, offer civic security, track the setting, and enhance infrastructure. Smart Nation project in Singapore consists of over 110 thousand cameras and sensors with edge AI.

Retail and Hospitality

Customer analytics, inventory management, automated checkout and loss prevention are all examples of retail environments that apply edge AI hardware. The Amazon Go stores have enormous edge AI systems that enable clients to walk out of the store without scanning them with the traditional point-of sale machines.

Ultra-Low Power (Under 1 Watt)- Enables always-on AI in battery-operated devices including wearables and IoT sensors

Low Power (1-10 Watts - 35% market share, largest segment) - Addresses mainstream applications including smartphones, tablets, and smart cameras

Medium Power (10-50 Watts) - Serves autonomous robots, industrial vision systems, and edge servers

High Power (Over 50 Watts) - Supports autonomous vehicles, industrial edge servers, and telecommunications infrastructure

Asia-Pacific (38% market share, fastest growing at 21.3% CAGR)

Asia-Pacific is the biggest and most rapidly expanding regional market, with huge volumes of consumer electronics production, intensive smart city projects, and significant investments of governments in the sphere of AI. China is a leading producer of smartphones in the world with about 50 percent production and consumer electronics with 60 percent of the total worldwide.

The New Generation Artificial Intelligence Development Plan of China is aimed at CNY 1 trillion AI industry value in 2030, with much emphasis on AI chips and edge computing. Domestic firms such as Huawei (HiSilicon), Horizon Robotics, and Cambricon have also created competitive edge AI processors.

North America

The market share of North America remains a large market share based on concentration in the technology industry, high venture capital, and early adoption in the automotive and enterprise applications. Another important edge AI hardware maker, NVIDIA, Qualcomm, Intel, and AMD have their headquarters in the area, as well as dozens of startups.

Artificial intelligence has become a strategic priority of the United States government, and the CHIPs and Science Act is providing USD 52.7 billion towards domestic semiconductor production and research to support the development of edge AI hardware.

Europe

Europe retains strong presence owing to the dominance in the auto industry, the automation of industries, and the presence of extensive AI regulations. The automotive sector in Germany spends a lot of money on ADAS and autonomous driving systems, which advance the demand of automotive-grade edge AI processors.

Latin America, Middle East & Africa

There is a high potential of growth in emerging regions due to urbanization, development of infrastructure and the growing adoption of technology. Plans of the ambitious smart city projects announced in the Middle East have generated significant demand of the edge AI hardware.

NVIDIA Corporation

NVIDIA is a leader in edge AI GPUs with the Jetson platform, which makes its products available in entry-level up to high-performance processors used in robotics, autonomous machinery, and industrial applications. The CUDA ecosystem offered by the company offers highly competitive advantages due to software maturity and wide libraries of optimizations.

The Jetson product family will meet the wide range of needs, including Jetson Nano (472 GFLOPS, USD 99), and Jetson AGX Orin (275 TOPS, USD 1,999). The automotive business of NVIDIA has won design contracts with Mercedes-Benz, Volvo, Jaguar Land Rover, and many developers of autonomous vehicles. Fiscal 2024 revenue was USD 60 billion and due to automotive and embedded segments, USD 1 billion in revenue is made per quarter.

Qualcomm Technologies

Qualcomm has been leading mobile edge AI with Snapdragon processors that power more than 2 billion smartphones in the world with AI Engine capabilities at all the product levels of up to 75 TOPS in flagship products. The automotive, IoT, and XR applications have their own product lines that the company has spread beyond the mobile.

Snapdragon Ride automotive platform has already won design with General Motors, BMW, Honda and Volvo. The security of the automotive pipeline will translate into an excess of USD 30 billion revenue in future. The revenue in fiscal 2023 was more than USD 35 billion, and the estimate of IoT was USD 6 billion.

Intel Corporation

Intel is competing in various segments with Core processors that have Deep Learning Boost, Movidius VPUs and FPGAs. The company Mobileye subsidiary vehicle vision product leads car vision systems with more than 100 million EyeQ processors deployed worldwide. Edge AI revenue was more than USD 10 billion in fiscal 2023.

Apple Inc.

To enhance its vertical integration, Apple has integrated its own Neural Engine processors into all its products, providing 15-17 TOPS in modern generation processors. The company has shipments of 230 million iPhones, 60 million iPads, and 25 million Macs per year, the largest implementation of bespoke edge AI processors in the world.

AMD (Advanced Micro Devices)

After being acquired in the USD 49 billion deal, AMD competes in the markets using the Ryzen Embedded processors and Xilinx FPGAs. The unified portfolio would cover different needs including reconfigurable acceleration to general purpose computing with AI extensions.

In-Depth Company Profiling (15+ Leading Edge AI Hardware Market Players)

Market Valuation & Financial Intelligence

Regional Market Leadership & Growth Opportunities

Competitive Intelligence & Strategic Positioning

Technology & Innovation Assessment

Market Segmentation Leadership

Navigate the Intelligence Revolution at the Edge

While competitors are having a hard time figuring out the change from cloud, based to edge, native AI, you will have a strategic roadmap to leverage the fastest, growing segment in semiconductor history.It is not only market data but also your competitive advantage in the race to deploy intelligence where it matters most.

What You Get: Strategic Intelligence That Drives Billion-Dollar Decisions

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.