Share this link via:

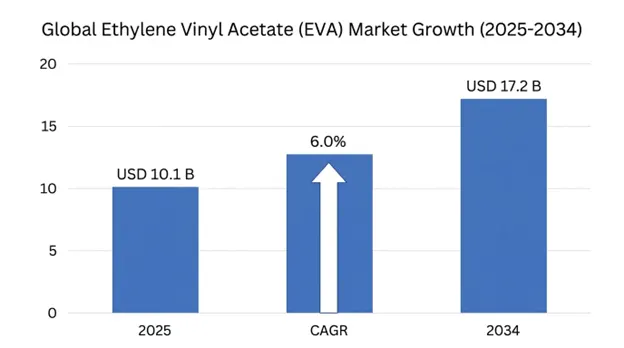

The ethylene vinyl acetate (EVA) market size reached USD 10.1 billion in 2025 and is expected to increase at a CAGR of 6.0% to USD 10.8 billion in 2026 and USD 17.2 billion in 2034 during the forecast period.

Ethylene vinyl acetate is a high-grade thermoplastic copolymer produced through the copolymerization of ethylene and vinyl acetate monomers, the content of vinyl acetate is the key factor that determines the properties of ethylene vinyl acetate. Typically, the concentration of vinyl acetate ranges from 5% to 40% by weight, and thus the materials range from rigid (like polyethylene) to highly flexible (like rubber). This compositional flexibility allows EVA to close the performance gap between conventional rigid thermoplastics and elastomers without the need for vulcanization processes, allowing it to be handled on standard thermoplastic processing equipment and exhibit rubber-like properties.

During the polymerization of EVA, the incorporation of a polar vinyl acetate group along the polyethylene chain disrupts the crystalline structure of polyethylene chains, introducing free volume into the structure, which increases chain mobility. Such structural changes make materials more flexible in low-temperature applications, with exceptional clarity and gloss, excellent resistance to stress cracking, strong adhesion to a variety of substrates and outstanding toughness when subjected to mechanical stresses. The combination of processability and performance has made EVA a must-have in a variety of high-value applications such as photovoltaic module encapsulation, athletic footwear production, flexible packaging systems, hot melt adhesive formulations, and special wire and cable insulation.

Beyond its conventional polymer applications, EVA plays an important role in the broader global efforts towards energy transition and sustainable materials. EVA is the most widely used encapsulant material for shielding silicon solar cells from environmental degradation, is optically clear and provides electrical insulation for solar cells for an operational lifetime of 25–30 years in the fast-growing solar photovoltaic industry. Its reliability in outdoor exposure and strong adhesive bond with glass and backsheet materials after thermal crosslinking renders it the industry standard for the crystalline silicon modules, accounting for more than 85% of global solar installations.

EVA has a strong commercial ecosystem, as evidenced by the involvement of petrochemical feedstock suppliers, specialised resin manufacturers, compounders and converters, and end-use industries that are leading innovations in renewable energy infrastructure, high performance consumer products, and advanced packaging solutions. Policies supporting the structural growth of the market, such as the transition toward renewable energy sources for global energy transition, rising demand for lightweight and durable materials, and growing applications in electric vehicle components and medical device manufacturing, drive the demand fundamentals to meet critical industrial requirements across a wide range of sectors.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 10.1 Billion |

| Forecast Value | USD 17.2 Billion |

| CAGR | 6.0% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

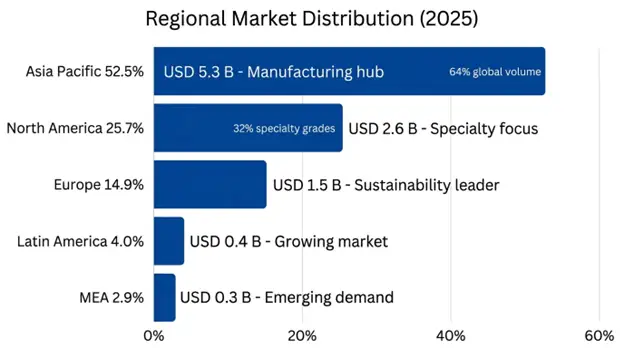

| Largest Market | Asia Pacific |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Type, Form, Application, End-Use Industry, Processing Technology |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Dow Inc., ExxonMobil Corporation, LyondellBasell Industries, Hanwha Solutions, Celanese Corporation, Braskem S.A., Sinopec Group, Formosa Plastics |

Get more details on this report - Request Free Sample

The world's largest structural influence on the global EVA market is the unprecedented pace at which solar PV installations are continuing to increase around the world, as a result of national decarbonization goals, falling PV manufacturing module prices, and the increased need for energy security which is seeing solar energy become the fastest-growing electricity generation technology in the world. EVA encapsulant films are among the most essential materials in the PV module and play a key role in ensuring module performance and reliability over 25-30 years, by providing electrical insulation, mechanical bonding of the glass cover to the PV cells, moisture barrier protection and optical clarity.

Solar PV capacity additions worldwide are forecast to total 450 gigawatts in 2025, and to go beyond 580 gigawatts per year by 2030. Global PV capacity will exceed 4.2 terawatts by 2034 under current national energy transition pathways. The energy transition is directly linked to EVA demand growth with each GW of solar PV installed equating to 4,200 to 4,800 MT of EVA encapsulant film -resulting in substantial EVA demand growth. China alone took up 260 gigawatts of new solar installations in 2025, which was the highest demand origin for PV-grade EVA in the world.

Solar-grade EVA differs from commodity grades by having a more precisely controlled vinyl acetate content (usually between 28 and 33% VA), certain crosslinking agent packages, UV stabilizers, and optical clarity (light transmittance > 91%). This technical specificity has enabled the development of a premium market segment which is represented by solar encapsulant grades, the growth of the market value varies by a price premium of at least 18-25% compared to the growth of the volume of standard grades of foam and film, making a significant increase in the value of the market.

Key Performance Metrics:

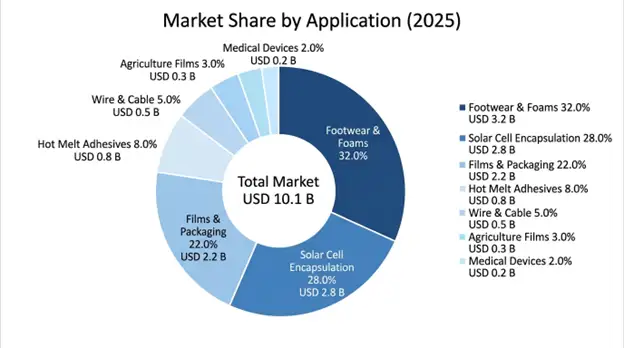

The footwear industry is the largest single application volume for EVA, using about 32% of the world's EVA production in the form of foam midsoles, outsoles, insoles and upper parts in athletic, casual, safety and specialty shoes. Since the 1980s, EVA foam has been used as the standard material for the midsole of athletic shoes, and new developments in EVA foam chemistry and processing have extended its competitive edge over other natural- and manmade-based materials, such as polyurethane foam and thermoplastic rubber compounds.

In 2025, global production of shoes surpassed 25 billion pairs per year, with Asia Pacific accounting for about 86% of global production, with China, Vietnam, Indonesia, and India accounting for the majority of the production. The premium athletic footwear category, which experienced a 7.8% CAGR growth due to the increasing popularity of athleisure fashion trends, sports participation growth and consumer willingness to pay for performance-ready footwear, requires more advanced EVA foam formulations, with higher energy return, lower weight and extended durability as opposed to standard grades. Major athletic footwear manufacturers such as Nike, Adidas, New Balance, and ASICS have invested heavily in proprietary EVA foam technology, with some technologies such as supercritical fluid foaming allowing for EVA foam densities of less than 0.08 grams per cubic centimeter and still having good structural integrity and energy return characteristics.

The mid-tier footwear market is experiencing volume growth as the middle class continues to grow in India, Southeast Asia and Latin America, where the performance of EVA foam components is acceptable and the cost is low enough for mass-market accessibility. With a rapidly expanding footwear consumption market in India, an increasing urban population, enhanced disposable income and the rise of organized retail, there is significant incremental demand for EVA from the second largest footwear production and consumption market in the world.

Key Performance Metrics:

As the packaging industry evolves with record e-commerce sales, demanding food safety laws, sustainability initiatives, and automation of packaging lines, EVA-based Hot Melt Adhesives and EVA packaging films are still experiencing growth. Hot melt adhesives offer rapid setting properties, can be used on a wide range of substrates, and have good resistance to temperature and are compatible with high-speed automatic packaging equipment that operates at speeds exceeding 800 units per minute, so they are used as hot melt adhesives for carton sealing, case and tray forming, labeling and flexible packaging lamination applications, making them more widely used than alternative adhesive technologies.

In 2025, global e-commerce packaging volumes hit 320 billion units with each unit needing adhesive bonding, labelling and sealing; EVA hot melt adhesives deliver reliable performance at competitive cost structures. EVA's oxygen barrier properties, heat sealability and food contact compliance are increasingly making it the packaging of choice for the food packaging sector for use in vacuum packaging, modified atmosphere packaging and retort applications, to ensure shelf life and food safety performance demanded by modern retail distribution systems.

Key Performance Metrics:

The price volatility of ethylene and vinyl acetate monomer (VAM), which are the primary raw materials for EVA production, all of which are directly affected by fluctuations in crude oil prices, natural gas prices and ethylene cracker supply-demand balance in the region, is the most crucial structural limitation affecting the stability and profitability of EVA markets. The economics of ethylene production are closely related to the price of the feedstocks, naphtha and ethane, and the cost of these feedstocks can fluctuate by 45-65% for a given calendar year in the event of oil market volatility, geopolitical unrest in producing areas, or unplanned outages of crackers that impact regional ethylene supplies.

Vinyl acetate monomer pricing is influenced by ethylene prices as well as exposure to natural gas prices due to the dependence on natural gas to produce the acetic acid that is feedstock to produce ethylene and ultimately vinyl acetate. A volatile feedstock market as seen between 2021 and 2025 further highlighted the impact of feedstock volatility in EVA markets, with ethylene prices in APAC varying from USD 680 to USD 1520 per metric ton within 24 months, which narrowed EVA producer margins and caused pricing instability affecting downstream customer planning and procurement strategies.

Impact Metrics:

In addition, competition is increasing in the PV encapsulant segment from other encapsulant materials such as polyolefin elastomers, thermoplastic polyurethane and polyvinyl butyral film that possess certain performance benefits in challenging module configurations and operating conditions. Polyolefin elastomer encapsulants have become more popular recently for use in bifacial and high efficiency module applications because they offer excellent moisture resistance, lower potential induced degradation susceptibility and do not create acetic acid during thermal aging that can corrode metal contacts in EVA encapsulant modules.

Polyolefin PV module encapsulant market share has seen a gradual rise by major module manufacturers such as LONGi, Jinko Solar and Canadian Solar in their higher-quality module product lines, increasing from 14% in 2020 to 31% in 2025. Despite maintaining a dominant 65% share of the PV encapsulant market in 2025, the developments towards higher efficiency modules, longer warranties and more extreme installation environments puts structural pressure on EVA's PV encapsulant market share.

Competition Metrics:

There is a transformative market opportunity to commercialize bio-based ethylene vinyl acetate, with the establishment of circular recycling ecosystems through sustainability commitments made by major brand owners, regulatory action to reduce fossil-derived plastics, and consumer demand for lower carbon footprint products. Bio-based EVA produced using sugarcane ethanol from Braskem's renewable feedstock platform, Brazil's leading producer, allows production of EVA with the same technical performance as the petroleum-based EVA grades, and provides a carbon footprint reduction of 75-85% on a cradle-to-gate basis.

The development of chemically recyclable EVA formulations is another complementary pathway for innovation, as there are challenges associated with the conventional EVA foam recycling due to the presence of crosslinked polymer networks that cannot be thermally processed. New chemical depolymerization technologies that are able to break EVA crosslinks to produce monomer-level feedstocks are progressing to pilot scale and are predicted to be commercially viable for EVA foam recycling applications by 2029-2031.

Opportunity Metrics:

The electrification of the global automotive fleet presents a major opportunity for EVA in electric vehicle battery systems of the global automotive fleet, which also opens up major prospects for thermal management systems and cable insulations. EVA's proven insulation performance in wire and cable is directly applicable to electric vehicle high-voltage cable systems, where the electrical insulation, flame resistance (when compounded properly) and flexibility at low operating temperatures are required to satisfy automotive qualification requirements.

By 2034, the global electric vehicle fleet is expected to exceed 420 million with an annual demand of 950,000-1,400,000 metric tons of EVA needed for automotive electrification alone, due to EVA's use as cable insulation, battery assembly, and interior applications.

EV Opportunity Metrics:

Move to high vinyl acetate content production.

Structural change in the global EVA industry is towards the manufacture of high VA content resins with more than 28% VA. The change is driven by the wide range of uses in hot melt adhesives, solar encapsulants, and specialty wire and cable compounds that demand the high fillers acceptance, high VA, and high polarity properties only found in high-VA compounds. High-VA EVA is a capital-intensive, technically complex process that is manufactured in a high-pressure tubular or autoclave reactor, which can act as barriers to entry and justify premium pricing for qualified manufacturer.

Trend Metrics:

Enhance and optimize advanced processing technologies.

Advances in EVA processing technology, such as the supercritical fluid foaming process with carbon dioxide and nitrogen as blowing agents, allow EVA foam structures to be fabricated with never before seen characteristics of low density, high energy return and durability. Supercritical CO₂ foaming processes produce EVA foam with densities less than 0.08 grams per cubic cm, which is 40% less dense than the conventional expanded EVA foam, and achieve energy return values exceeding 68% versus the 48-58% range of regular EVA foam grades.

Technology Innovation Metrics:

Asia Pacific: Market Leadership Through Manufacturing Scale and Integration

Asia Pacific is the leading region in the global EVA market in terms of market value with USD 5.3 billion at 52.5% of the global market value due to the overwhelming dominance of the region in terms of manufacturing PV modules, footwear and manufacturing of EVA polymer capacity. 72% of the world's PV module production, 62% of the world's footwear production, and around 48% of the world's EVA polymer production capacity is in China, with the three processes of polymer production, conversion, and consumption occurring in near geographic proximity.

Chinese producers such as Sinopec, CNOOC, and Formosa Plastics Taiwan enjoy massive scale advantages in EVA production, with their world-scale EVA plants (above 220,000 metric ton per year) benefiting from feedstock integration, operational scale advantages and regional cost structures, which allow them to achieve unit production costs that are 18-25% lower than North American/European equivalent capacity.

Regional Performance Metrics:

Innovation Leadership and Specialty Applications in North America

The second largest regional EVA market is North America with value projected at USD 2.6 billion in 2025, where the premium specialty grade dominates and is well advanced in application development. The advanced packaging, medical devices and aerospace industries are sophisticated end-use industries that require high-performance EVA formulations with stringent quality requirements and regulatory compliance specifications, which support the regional value.

The announced capacity additions to increase to > 50 GW by 2027, due to the Inflation Reduction Act's domestic content requirements and manufacturing incentives, are creating a growing demand for EVA encapsulant films manufactured in the USA, and signaling increased investments in EVA manufacturing capacity in North America.

North American Market Metrics:

Type Insights

With 44% market share and a valuation of USD 4.4 billion in 2025, medium VA Content EVA is the leading product in the global market, as it provides a balance of flexibility, adhesion and processability that makes it suitable for a wide variety of applications, such as footwear foams, packaging films and hot melt adhesives with different requirements.

The product segment with the highest VA content (above 28%) is expected to be the fastest-growing segment in 2025–2034 with a market share of 38% and a projected CAGR of 8.4% in terms of USD 3.8 billion. These grades are primarily used in encapsulant and specialty applications where high clarity and adhesion are essential to get the highest clarity and adhesion, and PV applications are leading to high price levels and fast volume growth.

Low VA Content EVA (<18% vinyl acetate) will hold an 18% market share of USD 1.8 billion in 2025 and will grow at 4.8% CAGR until 2034, used for wire and cable insulation and for applications that require moderate flexibility enhancement compared to polyethylene (PE).

Application Insights

The fastest-growing application segment is Solar Cell Encapsulation with 8.8% CAGR and will be worth USD 2.8 billion by 2025. The application market is growing in direct proportion to global PV installation rates and energy transition policies; technical requirements such as precise gel content control, UV stability and optical clarity (transmittance > 91%) offer differentiation opportunities to the application.

At 32% market share in 2025 and projected at USD 3.2 billion, the biggest application segment by volume is footwear & foams, which is expected to grow at a solid rate of 6.4% CAGR, fuelled by global footwear production growth, athletic footwear premiumisation and safety footwear demand in industrial applications.

In the year 2025, Films & Packaging will account for 22% market share, valued at USD 2.2 billion, with the growth fuelled by e-commerce packaging and modernization in food packaging in emerging markets.

End-Use Industry Insights

Structural energy transition dynamics are expected to drive the higher growth of Solar & Photovoltaics end-use at 9.2% CAGR till 2034. Footwear accounts for the highest volume share at 32% and Electronics & Electrical is the second largest share, contributing 16% of the market value and growing steadily due to the electrification of infrastructure and electric vehicle adoption.

The specialty grade EVA market is moderately concentrated, while the commodity grades are highly competitive, with the top eight producers accounting for about 62-68% of the world's production capacity. The commodity footwear, commodity packaging, specialty encapsulant, and medical segments differ significantly, with cost/scale as the primary driver for Asian competitive dynamics and technical differentiation, regulatory compliance and customer qualification relationships giving sustainable competitive advantages.

Other major integrated petrochemical players like Dow, ExxonMobil, LyondellBasell and Celanese are specializing in specialty grades through backward integration into ethylene and vinyl acetate monomer; Asian players like Hanwha Solutions, Sinopec and Formosa Plastics have been competing across both specialty and commodity grades based on operational scale and geographical proximity to market.

List of Top Companies of Ethylene Vinyl Acetate (EVA) Market

Global Ethylene Vinyl Acetate (EVA) Market Segments

By Type:

By Form:

By Application:

By End-Use Industry:

By Processing Technology:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

13 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.