Share this link via:

The Europe AI-powered industrial robot market is experiencing significant acceleration because of three factors that include extreme labor shortages and advanced manufacturing needs and safety and sustainability requirements established through complete regulatory systems which control industrial operations. The market provides AI-based robotic solutions which serve manufacturing automation needs and precision assembly work and logistics tasks and various industrial applications that use artificial intelligence for autonomous system optimization and predictive maintenance and operational efficiency improvements beyond what traditional industrial robots can achieve.

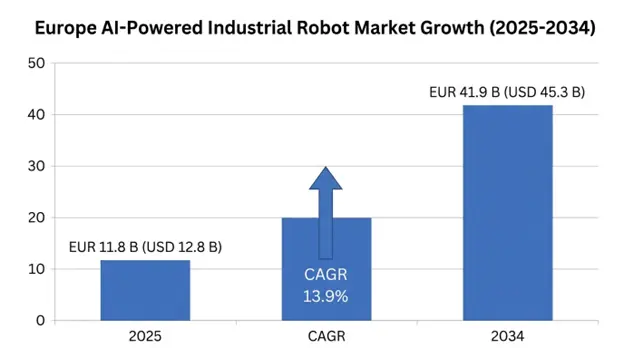

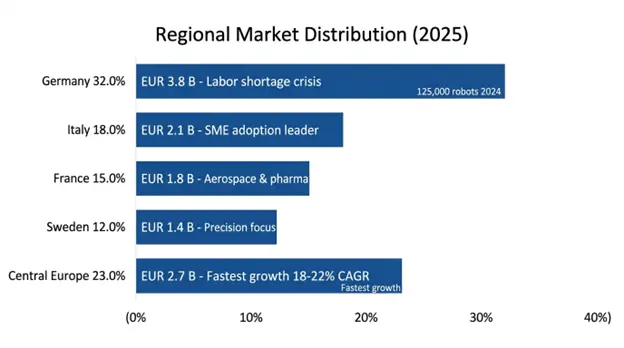

The market valuation begins at USD 12.8 billion in 2025 but will expand to USD 45.3 billion by 2034 which results in a 13.9% compound annual growth rate during the entire forecast duration. The operational stock of industrial robots in Europe reached over 580000 units in 2024 which resulted in a 7% year-over-year increase. Germany holds the top position in European robotics with a 32% share of the regional market while Italy follows with 18% and France has 15% and Sweden possesses 12% and Central European markets that are developing hold 23% of the market. The adoption of technological breakthroughs at Siemens with their AI-powered manufacturing control systems and ABB with their robotic advancements and KUKA with their collaborative automation systems received acceleration because of these major technological breakthroughs. Siemens declared an investment of EUR 8 billion for AI-powered industrial automation until 2027 while ABB expanded its European manufacturing capacity by 40% after SoftBank acquired its robotics division for USD 5.375 billion in October 2025. The industrial sector in Germany reached 125000 robot installations during 2024 which resulted in 28% growth from the previous year because businesses needed to solve their labor shortages and implement Industry 4.0 solutions.

The European AI-driven industrial robot market comprises advanced robotic systems and platforms that integrate artificial intelligence technologies for manufacturing automation, logistics optimization, and specialized industrial applications. European industrial robots operate through pre-set programs which limit their adaptability, while AI systems use machine learning algorithms and computer vision and predictive analytics and real-time decision-making to enhance manufacturing operations and handle production changes and improve their operational efficiency through knowledge gained from their performance data.

European AI robots use advanced engineering mechanisms which consist of multiple sensor systems that include vision systems and force sensors and industrial IoT connectivity, edge computing processors that support immediate autonomous decision-making, proprietary machine learning models which were developed through training on millions of manufacturing hours, and safety systems which guarantee compliance with CE marking, ISO 13849-1, and EN ISO/IEC 80001 standards. Collaborative robots incorporate force-limiting technology for workplace safety per ISO/TS 15066, intuitive programming interfaces, and AI-enhanced task adaptation enabling deployment alongside human workers. Advanced research perception systems enable autonomous mobile robots to execute materials handling and their operations within warehouse environments. Predictive maintenance systems which work with AI algorithms achieve maintenance schedule optimization while reducing unplanned downtime between 30-50%.

The applications range from automotive production assembly to precision component machining and electronics assembly and food and beverage processing and pharmaceutical production and metalworking processes and logistics automation and specialized inspection work. European manufacturing requires AI robotics solutions which differ from global market standards because it needs precise products which meet quality standards and regulatory requirements.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | EUR 11.8 Billion (USD 12.8 Billion) |

| Forecast Value | EUR 41.9 Billion (USD 45.3 Billion) |

| CAGR | 13.9% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Segments Covered | By Application Type, By Robot Type, By Technology Component, By Enterprise Size, By Region |

| Countries Covered | Germany (32.0%), Italy (18.0%), France (15.0%), Sweden (12.0%), Central Europe (23.0%) |

| Key Market Playes | Siemens, ABB, KUKA, Stäubli, Universal Robots, Bosch Rexroth, Techman Robots, Fanuc Europe, Yaskawa Europe |

Get more details on this report - Request Free Sample

Structural Labor Shortages Forcing Automation Adoption

The labor shortage in Europe has developed into a serious structural problem because of fast demographic aging and decreasing industrial workforce participation which causes ongoing manufacturing sector supply-demand shortages. Countries such as Germany experience major labor shortages because more than 20% of their population currently exceeds 65 years and this number will reach almost 28% by 2034 along with 35–45% of skilled jobs remaining unfilled. Central and Eastern European countries deal with migration-based labor shortages which force more than 40% of their manufacturers to enter critical shortages. The economic rationale for automation has changed because AI industrial robots now operate in factories to guarantee production continuity instead of serving as cost-saving solutions. The European Union industrial strategies together with national AI programs which provide funding support, lead to industrial automation being recognized as critical infrastructure, which creates persistent demand for robotics throughout the economy.

Industry 4.0 Accelerating Intelligent Automation

European manufacturing systems are experiencing faster adoption of AI-powered industrial robots because Industry 4.0 technologies are succeeding in their implementation across the continent. The transition to smart factories which shows 65% of major manufacturers executing digital changes by 2025 enables manufacturers to monitor operations in real time and perform predictive maintenance and create precise products. The new system produces measurable results which lead to 35%-50% less downtime and 25%-30% more production efficiency and major cost savings. Manufacturers now pursue energy-efficient robotic systems which decrease electricity usage and improve resource management to meet their sustainability requirements. Industry 4.0 technologies improve operational efficiency through their strong regulatory system and their quality standards which make AI-based automation essential for modern European manufacturing businesses.

High Costs and Regulatory Complexity Limiting Adoption

The driver base has expanded significantly but European industrial sectors face obstacles that hinder their adoption of AI-driven industrial robots because of the expensive implementation costs and their intricate regulatory requirements which particularly affect small and medium-sized enterprises. The European business landscape faces major financial obstacles because initial investments of EUR 200,000 to EUR 2 million require additional costs for integration and software and training and maintenance expenses which SMEs need to pay. The time to implement safety standards and data protection requirements and emerging AI policies increases by 6-12 months because these regulators need to verify compliance with the safety standards. the compliance requirements of safety standards and data protection measures and emerging AI policies extend deployment periods by six to twelve months while increasing project expenses by thirty%. The robotics and AI development field suffers from a critical shortage of skilled workers who can fill more than 40,000 available positions which causes execution delays and project risks. The combination of financial obligations and regulatory requirements and talent shortages continue to hinder widespread adoption particularly in regions with lower levels of technological development.

Market Opportunity:

Collaborative Robotics and Human-Centric Manufacturing

The most important market opportunity exists through collaborative robotics and human-centric manufacturing because these systems transform European manufacturing by offering safe human-robot collaboration for operations that require precise and high-quality output. The development of force-limiting technology along with advanced perception systems and intuitive programming tools has established new opportunities for deploying collaborative robots which enable businesses to quickly increase their workforce without decreasing their need for skilled workers.

Siemens Launches AI Manufacturing Control Systems (2025)

Siemens announced EUR 8 billion industrial AI investment through 2027, prioritizing AI-powered manufacturing control systems enabling real-time production optimization. The investment project aims to implement collaborative robot systems throughout European manufacturing operations, which will provide small and medium enterprises with access to cloud-based AI services that deliver enterprise-level automation solutions. The Siemens solutions provide 25-30% productivity improvement together with 20-30% cost reduction and predictive maintenance which decreases unplanned downtime by 40-50%. The deployment operation focuses on three specific sectors which include automotive suppliers, precision metalworking companies and pharmaceutical manufacturing facilities.

ABB Expands European Robotics Manufacturing (2024-2026)

ABB Robotics which SoftBank acquired in October 2025 announced its European expansion plan which will extend manufacturing capabilities by 40% through new production facilities in Germany Italy and Sweden that will manufacture collaborative robots. The IRB 1100 cobot platform from ABB enabled companies to deploy their robots 35% faster while achieving 25% lower operating costs compared to standard industrial robots. The investment will reach its goal of 50,000 units annual production capacity by 2027 which will make collaborative automation accessible to small and medium-sized enterprises throughout Europe.

KUKA Develops Industry 4.0 Integration Solutions (2024-2025)

KUKA developed an all-inclusive Industry 4.0 integration platform to link its AI-driven robotic systems with manufacturing execution systems for real-time production optimization. The solutions utilize predictive maintenance algorithms which decrease unplanned downtime between 45%-50% while increasing overall equipment effectiveness (OEE) between 15%-25%. KUKA expanded its manufacturing capacity in Germany by 30% to increase its production of collaborative robots and AI systems.

German Government Expands Industrial AI Subsidies (2025)

The German federal government now provides manufacturing automation subsidies which reach EUR 5 billion each year to provide financial support for small and medium enterprises that want to implement 25-35% of their AI robotics projects. The program helps mid-market manufacturers who want to start their Industry 4.0 transition between established roboticists and new AI specialists. The subsidy programs provide small and medium enterprises with funding which decreases their actual costs for AI robot implementation by between 25-35%.

By Application Type:

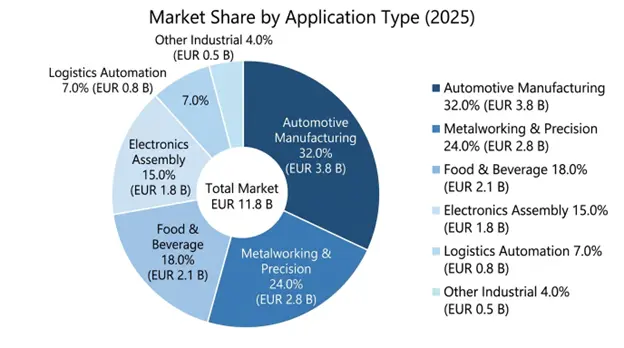

The automotive manufacturing field operates as the biggest industry sector with a 32.0% share which includes assembly automation and precision welding and component handling and quality inspection activities. The market value of metalworking and precision manufacturing stands at 24.0% which includes CNC machine tending and component machining and specialized fabrication services. The food and beverage processing industry holds an 18.0% market share through its packaging and sorting and quality control operations. The electronics and component assembly sector produces 15.0% of its work through its activities that involve precision placement and verification of electronic components. The logistics and warehouse automation sector includes material handling and order fulfillment operations, which make up 7.0% of its total activities. The industrial sector encompasses 4.0% of its operations through various applications which include pharmaceuticals and chemical processing and specialized manufacturing.

By Robot Type:

The market for collaborative robots or cobots has grown to become the fastest developing sector which holds a market value of EUR 4.8 billion in 2025 and experiences an annual growth rate of 18% according to ISO/TS 15066 standards for human-robot workstations. The market value of traditional industrial robots with AI integration reaches 35.0% because these robots bring intelligent control capabilities to existing systems. The market for autonomous mobile robots that handle materials operates at an 18.0% capacity because their advanced perception systems enable them to move through active manufacturing spaces. The market for specialized robots that perform inspection and quality control functions plus hazardous operation tasks reaches 9.0%.

By Technology Component:

The market value of AI and machine learning software amounts to 38.0% which includes predictive analytics and computer vision and autonomous decision-making systems. Hardware and advanced sensor systems comprise 36.0% which includes collaborative force-limiting mechanisms and industrial IoT connectivity. The company provides 18.0% of its revenue through integration services and consulting which help clients with deployment and workforce training and Industry 4.0 system integration. The company spends 8.0% of its budget on ongoing maintenance and technical support services.

By Enterprise Size:

The AI robot market value shows that large enterprises which have more than 250 employees create 62% of the market value because they have access to financial resources, and their staff members possess technical skills. The market share of small and medium enterprises which employ between 50-249 workers currently stands at 28% and their market share expands because of government financial support and easier installation methods. Micro enterprises, which have between 10-49 employees, hold a 10% market share, but their growth remains restricted because of their financial restrictions and their lack of technical skills.

Germany: The European AI-powered industrial robot market is divided into 32% for Germany which stands as the leading market player in Europe. German manufacturing employment exceeds 7 million with industrial workforce declining 15% since 2015, creating acute automation imperative. The automotive industry and precision engineering businesses and robotics manufacturers which include Siemens and KUKA and Bosch and Daimler, have built their operations in Bavaria and Baden-Württemberg. The total number of industrial robots installed in Germany passed 125,000 units during 2024 which marked a 28% increase from the previous year. The German federal government provides subsidies which cover 25-35% of AI robotics investments to help small and medium enterprises adopt these technologies. German manufacturing facilities spend more than EUR 500,000 each year on their automation systems.

Italy: Italy's Precision Manufacturing Hub holds an 18% market share in Europe through its three specialized fields which include precision manufacturing and luxury goods production and metalworking techniques. The Italian manufacturing sector faces an urgent crisis because its workers now have an average age of 52 years in established industrial areas. The industrial region of Northern Italy which includes Emilia-Romagna and Lombardy and Piedmont contains multiple concentrated industrial facilities which manufacture machinery and operate precision engineering businesses and produce textile equipment. Italian SMEs demonstrate rapid AI robotics adoption, with 35% of small and medium enterprises deploying automation by 2025. The Italian government provides subsidies which cover 20-30% of automation expenses to help micro and small businesses implement automated systems.

France: France controls 15% of the European AI robot market through its industrial diversification across automotive aerospace pharmaceutical and food processing manufacturing sectors. The French manufacturing industry currently deals with a shortage of specialized technicians who make up 20-25% of its workforce. The Paris-Lyon-Marseille corridor contains the two primary locations which house both manufacturing facilities and distribution centers. The three largest industrial automation investors in France are Renault and PSA which operates under the Stellantis brand and Michelin. The French government programs provide financial support to small and medium enterprises by covering 20-25% of their AI robotics investments which helps to promote technology adoption throughout different regions.

Sweden: Advanced Manufacturing Pioneer Sweden holds 12% of the European market through its advanced automotive supply and precision manufacturing and forest products processing expertise. Swedish manufacturing focuses on producing high-value precision-engineered products which prioritize quality instead of producing large quantities. Major automation investors include Volvo Scania and SKF. Manufacturing industries in Sweden face workforce shortages between 30 and 40% which forces companies to increase their automation efforts. The Swedish government and industrial partners work together to support quick technology implementation and large-scale innovation development.

Central Europe: The Central European countries of Poland and Czech Republic and Hungary account for 23% of the market while experiencing annual growth rates between 18 and 22% which surpasses the overall growth rate of Europe. European Union funds support the region by financing automation projects which receive cost assistance between 30-35%. Central European manufacturers now require faster automation implementation because they need to shift their business model from low-cost labor to high-quality and innovative production methods. The region faces economic pressure to automate work because its labor costs which start at EUR 12-18 per hour exceed the expected market rates.

Siemens Announces EUR 8 billion Industrial AI Investment (2024-2025): Siemens announced comprehensive EUR 8 billion investment in AI-enabled industrial automation through 2027, prioritizing AI-powered manufacturing control systems and collaborative robot ecosystem development. The investment will fund manufacturing facility upgrades which will take place in Germany and Poland and Italy and will provide cloud-based AI services which SMEs can access and workforce training programs. Through its predictive maintenance capabilities Siemens solutions enable 25-30% productivity gains and 40-50% reductions in unplanned downtime.

ABB Robotics Expands European Production (2024-2026): SoftBank acquired ABB Robotics for 5.375 billion dollars in October 2025. The company announced its plan to increase European production capacity by 40% based on their existing manufacturing sites. The investment will establish new production plants across Germany and Italy and Sweden which will produce more than 50000 collaborative robots every year by 2027. ABB's IRB 1100 cobot platform enables organizations to deploy systems 35% faster and achieve 25% lower operational costs compared to conventional methods.

KUKA Develops Industry 4.0 Integration Solutions (2024-2025): KUKA launched its complete Industry 4.0 integration system which allows AI robots to establish links with manufacturing execution systems for ongoing process enhancement. The system enables predictive maintenance which decreases unexpected equipment failures by 45-50% while increasing overall equipment efficiency by 15-25%. KUKA increased its German manufacturing capacity by 30% to enhance its production capabilities for collaborative robots.

German Government Expands Manufacturing Subsidies (2025): The federal government has increased automation subsidy programs from their previous funding level to EUR 5 billion per year which supports small and medium enterprises with 25-35% of their AI robotics expenses. The programs enable mid-market manufacturers who are implementing Industry 4.0 to work together with roboticists and AI specialists who use newly developed technology.

Italian Manufacturing Digitalization Initiative (2024-2025): The Italian government established a digitalization program which includes a budget of EUR 3 billion to support AI and robotics implementation in small and medium enterprises through financial aid that covers 20 to 30% of implementation expenses. The program focuses on Northern Italy's small and medium-sized manufacturing businesses to provide them with access to advanced technology which will help them compete against multinational corporations.

European Union Industry 4.0 Directive (2025): The European Commission introduced a complete Industry 4.0 regulation which establishes fundamental automation requirements together with cybersecurity standards and workforce training initiatives. The directive requires all AI-based industrial robots to obtain CE marking certification which manufacturers must implement between 2027-2028.

Manufacturers of robotics in Europe which include Siemens, ABB (which SoftBank has acquired), KUKA, and Stäubli, use their existing manufacturing abilities and distribution systems and customer connections to create AI-driven products. The AI robotics market features competitive platforms which Universal Robots and Techman Robots and European AI startups use to create innovative solutions and tailored offerings for their clients.

Siemens gives companies its extensive expertise in manufacturing automation together with its worldwide service network and its ability to integrate Industry 4.0 platforms. ABB brings 3 decades of robotics innovation and its established OEM partnerships plus SoftBank's AI technology access which became available after the acquisition. KUKA provides a manufacturing solution which combines precision manufacturing capabilities with its European operational network and its development of new collaborative technology. Universal Robots invented the collaborative robotics industry through its user-friendly programming system which includes safety features that prevent force overloads. Techman Robots and Dobot supply Chinese companies with affordable solutions which particularly benefit small and medium enterprises that face budget limitations. Bosch which operates as a German automotive supplier focuses on vertical integration by creating its own automation systems which enable factories to operate while providing limited services to clients.

The competitive landscape shows that European manufacturers use their established ecosystems and their unique service offerings to secure their market position against two types of opponents which are companies that develop disruptive technologies and developing markets that provide lower operational expenses.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

11 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.