Share this link via:

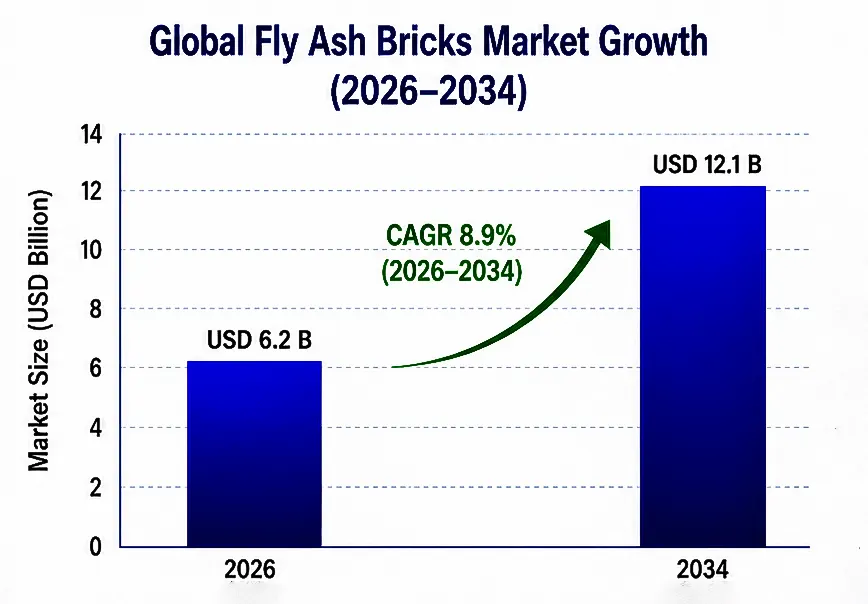

The global fly ash bricks market was valued at USD 5.6 billion in 2025 and is projected to reach USD 6.2 billion in 2026, expanding to USD 12.1 billion by 2034, growing at a CAGR of 8.9% during the forecast period (2026-2034).

Fly ash bricks are a modern form of sustainable building material which are manufactured by blending fly ash generated from coal combustion in thermal power plants with additives such as lime, cement, gypsum, and sand using compression molding followed by ambient or steam curing. As opposed to regular fired bricks made using topsoil from agriculture and requiring high energy usage through burning at high temperatures in kilns, fly ash bricks employ waste material from industries and possess improved mechanical properties, including better compressive strength from 75-200 kg/cm² and low water absorption less than 15%.

The basic manufacturing method capitalizes on the pozzolanic activity of fly ash grains made up of amorphous silicon and aluminum oxide substances that react with calcium hydroxide in the presence of water to produce calcium silicate hydrates and calcium aluminate hydrates, the binding substances like the components found in concrete. Due to the pozzolanic activity, fly ash bricks can gain strength gradually over time through curing, such that quality bricks produced can attain compressive strength values that satisfy international specifications such as those stipulated in IS 12894, ASTM C55, and EN 771-3.

Environmental benefits of fly ash bricks can be assessed on several planes in the context of green building materials. Every ton of fly ash used in brick manufacturing helps prevent industrial waste from being dumped into landfills or ash ponds, where it could potentially leach trace amounts of heavy metals to the water table, creating pollution hazards for power companies. Moreover, the fly ash brick manufacturing process does not require energy-intensive kiln firing, which saves 1.0-1.4 kg of coal equivalent (equivalent to 1,000 standard bricks), lowering the amount of energy consumed by 60-80% and cutting down greenhouse gas emissions by 40-60%.

The commercial ecosystem includes integrated supply chain logistics linking thermal power plants to brick factories, testing and certification facilities that guarantee consistent product functionality, as well as comprehensive policies that include obligatory fly ash use policies, which guarantee minimum demand levels for investments in productive capacities.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 5.6 Billion |

| Forecast Value | USD 12.1 Billion |

| CAGR | 8.9% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Raw Material, Application, End-Use, Distribution Channel, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, India, China, Japan, Australia, Germany, UK, France, Poland, South Africa, UAE, Saudi Arabia, Brazil, Indonesia, Bangladesh |

| Key Market Playes | UltraTech Cement Ltd., Boral Limited, LafargeHolcim Ltd., NCL Industries, Wienerberger AG, Jindal Panther Cement |

Get more details on this report - Request Free Sample

The primary factor driving market growth of the fly ash brick market is the increased regulation by governments whereby thermal power companies are mandated to utilize 100% of the fly ash produced in their operations while limiting the production of clay bricks due to environmental reasons. The Indian Environment Protection Act requires brick manufacturers located within 300–500 km from thermal power plants to utilize certain percentages of fly ash and prohibits the use of topsoil from agriculture lands for clay bricks manufacturing in several states like Uttar Pradesh, Bihar, and West Bengal, which together constitute more than 40% of the total number of bricks produced in India.

The Industrial Emissions Directive of the European Union establishes strict emission standards that are difficult for the brick kiln operators using the conventional brick kilns, and this compels a shift to brick plants using fly ash bricks in place of the traditional bricks. China has stringent rules concerning coal fly ash that categorize the pond ash as major pollution risk, hence motivating power stations to deliver fly ash to the brick making factories through subsidized prices.

Recycled industrial waste content and low carbon footprint credits offered by green building rating systems such as LEED, BREEAM, GRIHA, and Green Star can be earned through the use of fly ash bricks, allowing builders to secure top-level certifications which carry an 8-23% premium in commercial property rentals and sales markets.

The adoption of fly ash bricks is driven by their numerous technical and economic advantages, which are the reasons for their use by contractors, developers, and government agencies responsible for developing infrastructure. The high dimensional accuracy of machine-made bricks reduces up to 20-30% of mortar as well as decrease labor expenditures for masonry up to 15-25% due to higher productivity in bricklaying as well as absence of necessity to render surfaces to create even surfaces of walls. Due to low bulk weight (1,700-1,900 kg/m³ as against 1,900-2,100 kg/m³), this reduces foundation and column design costs.

Eliminating high-temperature kilns helps reduce direct energy expenses by up to 60-80%, while fly ash used as a raw material can often be procured at little expense from power generation companies trying to dispose of their waste. Economic gains resulting from improvements in product quality, such as a reduction in breakage rates from 10-12% for traditional clay bricks to under 2% for fly ash bricks, contribute towards balancing higher prices where there is transport expenses related to obtaining fly ash.

The primary constraint on market expansion is is due to variations in the physical and chemical properties of the fly ash obtained from various power plants, resulting in inconsistencies in terms of product quality. Fly ashes obtained from different types of coal vary significantly in their fineness, loss on ignition, calcium oxide content, and the content of harmful chemicals such as sulfates and heavy metals.

Fly ash with LOI values above 6–8%, particularly some Class F fly ash,, implies that there is significant unburned carbon in the material, which absorbs water, affects the pozzolanic activity of fly ash, and affects strength gain, necessitating either pretreatment or mixing with better fly ash. Changes in the quality of fly ash based on seasons in the same station are attributed to changes in the quality of coal used.

Dependence on coal-fired power generation creates a risk of supply shortages due to a transition in the energy matrix towards renewables. In North America and Western Europe, increased plant shutdowns have led to regional shortages of fly ash, with producers having to ship material longer distances or use expensive processing of legacy pond ash.

Significant market growth opportunities exist through the adoption of various Industry 4.0 technologies such as computer-controlled hydraulic press machines, automatic batch mixing, robotic processing, and quality control through near-infrared spectrometry and strength testing. Implementation of these technologies leads to better process standardization, reduced labor expenses, and ability to adjust in the process due to variations in raw materials.

Automated fly ash brick plants can increase labor productivity by up to 200–280% by producing 80,000-120,000 bricks per shift using 12-18 employees, while traditional brick plants can only manufacture 30,000-50,000 bricks by employing 35-55 workers, thus ensuring high economic efficiency at a time of increasing construction labor costs.

Fly ash bricks are increasingly being integrated into modular construction in modular construction by developing panels from fly ash brick materials. The use of such panels, as well as other fly ash brick products, including block interlocks and precast concrete, ensures that there are many economic advantages, as well as speed in terms of fabrication of components off-site. Fly ash brick panels fabricated in a factory environment exceed the quality and dimensional accuracy of field-constructed masonry structures.

The global market for modular construction worth USD 98.4 billion by 2025 is experiencing a rising trend of incorporating sustainability features that are provided by fly ash-based products, especially as big modular companies try to earn their green credentials.

Asia Pacific accounted for an estimated 68% of the global market of USD 3.8 billion by 2025, retaining a consistent CAGR of 9.4% up until 2034. The region dominates the market because it has the world’s leading markets for construction industry, high volumes of fly ash production, and the most advanced regulations that promote fly ash usage. India and China together make up 74% of the market value of the Asia Pacific region.

India’s policy requiring thermal power plants to supply fly ash supports market growth fosters structural strength in the growth of the market, with an annual production of 220 million tons forecast to continue being significant until 2034 even with advancements in renewable energy. The fast-growing demand in Southeast Asian countries like Indonesia, Vietnam, and Bangladesh is attributable to urbanization and enhanced technological awareness.

Middle East and Africa is expected to be the fastest-growing market, growing at a CAGR of 11.7% from 2023 to 2034, valued at USD 0.72 billion in 2025. The region is expected to grow due to significant infrastructure investments in GCC nations under their vision 2030 initiatives, significant fly ash availability in South Africa, and accelerated construction activity due to rapid urbanization in Sub-Saharan Africa.

The UAE and Saudi Arabia have integrated fly ash bricks in their green building initiatives based on their sustainable development principles with Dubai Green Building Regulations and Abu Dhabi Estidama Pearl Rating System granting credit to recycled content. The South African electric power company Eskom produces about 38 million tons of fly ash per year with utilization levels at just 12% in 2025, hence a lot of available raw material.

Solid Fly Ash Bricks occupy the largest market share with 54% at USD 3.0 billion in 2025, expected to grow at 8.6% CAGR during 2025-2034. Solid Fly Ash Bricks are the dominant product segment in terms of both load-bearing and non-load-bearing walls on account of the familiarity of this construction method.

The Hollow Fly Ash Bricks occupy 26% market share, estimated at USD 1.5 billion in 2025, growing at a 10.2% CAGR to emerge as the fastest growing product among all segments. Their hollow structure reduces material usage due to the hollow structure, resulting in lower dead load and enhanced insulation performance.

The Cellular Lightweight Concrete Block is estimated to grow at an 11.8% CAGR during 2025-2034, and is forecasted to be worth USD 0.67 billion in 2025, accounting for 12% market share.

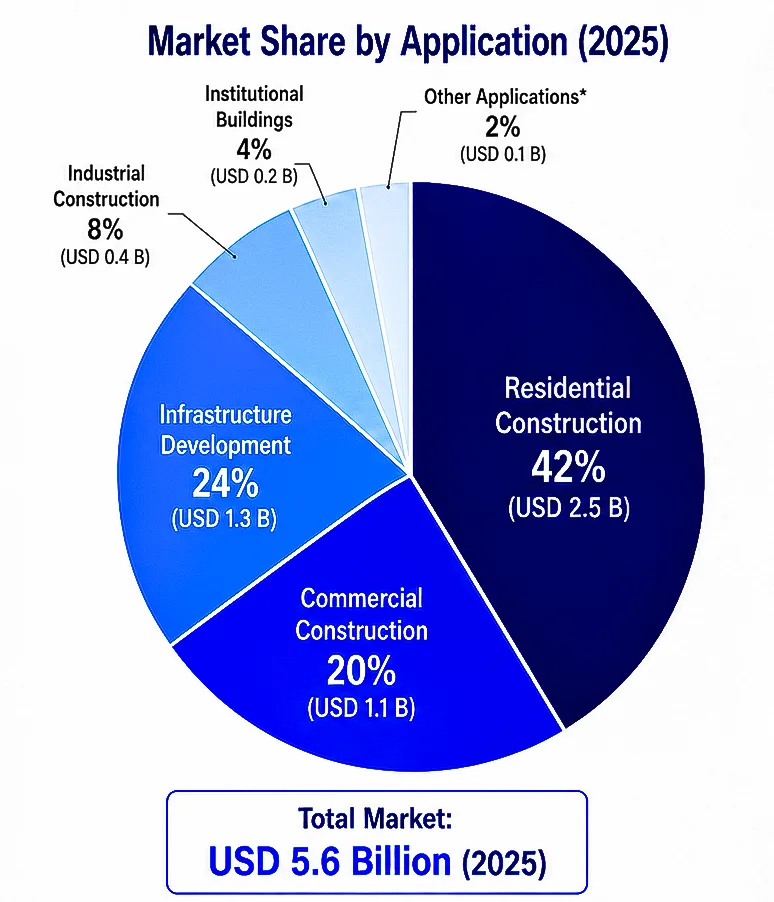

The Residential Construction segment holds a 44% market share valued at USD 2.5 billion, backed by government policies related to affordable housing schemes in India, China, and Southeast Asian countries owing to the use of fly ash bricks in such projects.

The Infrastructure Development segment holds a 24% market share valued at USD 1.3 billion and growing at a CAGR of 9.8%, covering applications like drainage structures, retaining walls, boundary walls, and other ancillary structures where fly ash bricks offer cost-effective options.

The Commercial Construction segment occupies 20% market share worth USD 1.1 billion, supported by green building certification policies and sustainability norms mandating recycled content products for office buildings and retail spaces.

The fly ash bricks industry is highly fragmented with concentration of the regional competition among bigger companies equipped with automation while there is a presence of many small and medium scale firms that operate locally. Transportation costs beyond 200–300 km create a regional competitive landscape in which competitiveness depends on geographic location regarding fly ash source and construction site. The top ten companies account for approximately 31% of the global market based on localized nature of market operations with customers’ loyalty dependent on existing relationships and quality products.

The basis of competitive advantage lies in cost effectiveness in production process due to unique technology of automation, quality assurance with use of effective quality control system, geographic locations close to fly ash sources and construction sites, technical assistance for contractors and certifications allowing access to government and green building projects. Competitive companies increasingly engage in vertical integration involving fly ash sourcing and horizontal integration related to other construction products such as concrete blocks and precast units.

June 2026: UltraTech Cement commissioned the establishment of three automated units to produce fly ash bricks in the eastern parts of India by making an investment of USD 52 million. The units have an aggregate annual capacity of production of 180 million bricks.

April 2026: The LafargeHolcim Company introduced the manufacture of geopolymer fly ash bricks with certification for reduced embodied carbon by 68 percent compared to traditional clay bricks and fire resistance of more than 4 hours through its ECOPact sustainable material range in India and Indonesia.

March 2026: The Boral Limited company was awarded ISCC PLUS certification for their fly ash brick manufacturing operations in Australia, allowing them to produce sustainable bricks for the commercial builders who need end-to-end traceability for their eco-friendly construction projects.

February 2026: A coalition of GCC-based construction firms formed a joint venture for producing fly ash bricks through the importation of fly ash from India to be used in projects related to Saudi Arabia's Vision 2030 initiatives as environmentally sustainable walling materials.

January 2026: Ministry of Environment, Government of India increased the radius for mandatory utilization of fly ash from 300 kilometers to 500 kilometers from power plants, greatly widening the geographical availability of raw material and thus increasing the availability of 35 million tonnes of fly ash per year.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.