Share this link via:

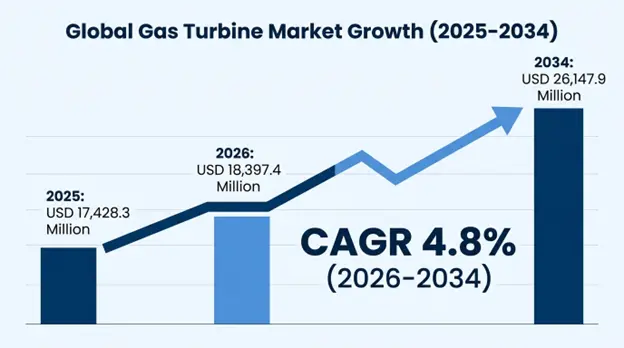

The market size of gas turbines in the world is estimated to be USD 17,428.3 million in 2025 and estimated to grow to USD 18,397.4 million in 2026 and to USD 26,147.9 million by 2034 with a CAGR of 4.8% over the period of forecasting (2026-2034)

Gas turbines are the most advanced thermodynamic machines in the world energy system, transforming chemical energy in combustible fuels to rotational mechanical energy via the Brayton cycle, and with advanced designs operating at very high temperatures, of over 1,600°C. This is the backbone of the modern electricity grids. These critical systems generate baseload power, peak shaving, grid stabilization services, and provide a critical backup power source, but are also used as mechanical drivers in oil and gas processing plants, pipeline compression plants and liquefied natural gas production plants around the world.

The fundamental change in the market is mainly due to the three convergent forces that have altered the global energy landscape: the rapid retirement of coal-fired power plants that creates immediate replacement demand of cleaner dispatchable generation, the swiftly growing variable renewable energy that needs rapid ramping backup capacity to maintain grid stability, and the emergence of the hydrogen economy that makes gas turbines an essential transition resource that can evolve to operate on zero-carbon hydrogen The current gas turbines have combined cycle thermal efficiency of up to 64%, which is a quantum leap in the performance and the carbon dioxide emission per megawatt-hour is 50-60% lower than the conventional coal generation.

The strategic significance of technology has escalated as countries walk a fine line between ambitious decarbonization targets and energy security needs, where gas turbines are considered key transition technologies that can supply reliable dispatchable energy whilst adapting to increased utilization of intermittent renewable energy sources. Newer designs of turbines now have quick startup times of 10-30 minutes of combined cycle units and less than 10 minutes of aeroderivative units, allowing grid operators to deal with renewable energy variability without compromising system reliability and frequency stability.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 17,428.3 Million |

| Forecast Value | USD 26,147.9 Million |

| CAGR | 4.8% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

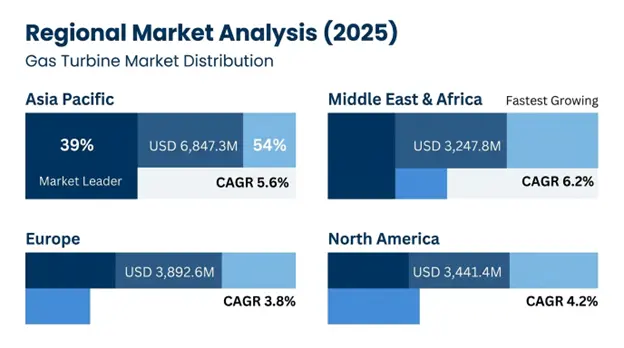

| Largest Market | Asia Pacific |

| Fastest Growing Market | Middle East & Africa |

| Segments Covered | By Capacity, By Technology, By Design, By Fuel Type, By Application, By End-User Industry |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Spain, Italy, Netherlands, Russia, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | General Electric Company, Siemens Energy AG, Mitsubishi Power Ltd., Ansaldo Energia, Kawasaki Heavy Industries, Solar Turbines |

Get more details on this report - Request Free Sample

The main driver of the strong growth in the gas turbine market is the concomitant acceleration of coal-fired power plant closures and the urgent requirement of quick responsive, flexible generation capacity to back up unprecedented renewable energy implementation. By 2024-2025, global coal retirement announcements of over 180 GW will create an immediate replacement demand on technologies that provide dispatchable generation services capable of providing grid stability services that the intermittent renewable sources cannot deliver on their own.

Modern gas turbines have distinctive operating features that are vital in the integration of renewable sources such as the fast start-up times, high rates of ramping 15-50 MW/min, and the capability to be operated efficiently at low loads in the 30-40% range of rated output. These features allow gas turbines to offer important grid services such as frequency regulation, spinning reserves, and voltage support and act as back up generation in times of low renewable output, forming a symbiotic relationship that provides grid reliability as renewable penetration rises.

F-class, H-class and J-class combined cycle gas turbines with the technology have environmental benefits that further increase the adoption rate, with net thermal efficiencies of 58–64%, which equates to 50-60 % lower carbon dioxide emissions than subcritical coal plants and 35-45 % lower than supercritical coal technologies. This efficiency benefits, together with dramatically lower air pollutant emissions such as particulates, sulfur dioxide, and nitrogen oxides, place gas turbines as temporary solutions to decarbonization as renewable energy infrastructure builds up.

According to International Energy Agency data coal-to-gas switching in power generation avoided some 500 million tons of CO₂ emissions in the world in 2024-2025, of which 78% of the replacement capacity of retired coal units was covered by gas turbines. According to grid operators, every 1 GW of variable renewable capacity integrated into electrical systems must be matched with a 250-400 MW of flexible gas turbine capacity to ensure the reliability and frequency stability of the systems within acceptable operating limits. Installed advanced gas turbines in 2025 reached average combined cycle efficiencies of 61.8%, a 2.3 % higher than those of units installed in 2020-2022 and give levelized costs of electricity that are competitive with coal generation in 89 of the world markets in the absence of carbon pricing mechanisms.

The greatest limitation to the growth of gas turbine markets is the radical cut in costs through renewable energy technologies, especially solar photovoltaic and onshore wind generation which have dropped to levelized costs of electricity at USD 30-50 per megawatt-hour in favorable sites, which exert significant economic pressure on gas-fired generation. This cost advantage has fundamentally changed the pattern of power generation investment, with renewable capacity additions of 507 GW to the world in 2024 versus 52 GW of gas-fired capacity, and 9.7:1 ratio that is growing as the cost of renewable power falls 6-10%/year due to technological progress and scale effects of manufacturing.

Renewable energy growth has pushed the capacity factors of gas turbines down in the high-penetration markets to narrow the historical averages of 4,500-5,500 hours of annual operating time to 2,800-3,800 hours in such locations as California, Germany, and South Australia. This paradigm shift in operation transforms gas turbines into cycling and peaking units with non-persistent operation patterns, which fundamentally changes the economics of the project and the payback period of investments, which currently range between 18-25 years, in the current market structures in the absence of proper capacity market compensation mechanisms.

The analysis of United States Energy Information Administration illustrates the weighted-average levelized costs of USD 35.42 per megawatt-hour of utility-scale solar photovoltaic installations in 2025, versus USD 61.78 per megawatt-hour of new combined cycle gas turbine facilities with fuel costs at USD 3.75 per MMBtu natural gas prices. Factors of European gas turbine fleet capacity fell to 36% in 2025, which is a direct result of the consequences of displacement of renewable energy, as compared to 51% average in 2019, and the German combined cycle plants referenced had 3,180-hour average annual operation versus 6,000-6,500-hour design assumptions. The volatility of natural gas prices also contributed to economic difficulties in operation since at a time in 2024-2025, the price at Henry Hub ranged between USD 2.10-8.90 per MMBtu, which led to operational uncertainty and made it necessary to maintain higher reserve margins and lower the frequency of dispatching gas turbines during high-fuel price periods.

The most radical chance redefining gas turbine market is the strategic development towards hydrogen-capable combustion systems that would allow both current and new turbine assets to be deployed as long-term decarbonization infrastructure, and not as transitional fossil fuel technology. Large equipment manufacturers have produced combinations of combustion systems that can operate with an increment of 30 per cent to 100 per cent of hydrogen blend with commercial units certified as being able to operate with 50 per cent hydrogen and 100 per cent hydrogen operation planned in 2025 and 2027-2028 respectively.

Such technological development brings about two value propositions: short term revenue of hydrogen-ready premium pricing on new equipment sales, and long-term large aftermarket potential in retrofitting existing global gas turbine fleets of more than 15,000 operating units. The process of retrofitting that has been adopted is the updating of fuel delivery systems, combustion parts and control systems to suit the higher flame speed and temperature properties of hydrogen, which would possibly extend the life of assets by 15-20 years and allow zero-carbon operation as the infrastructure of hydrogen supply evolves.

At the same time, the growing infiltration of variable renewable energy opens premium pricing prospects to gas turbines that offer the much-needed grid stabilization services such as frequency regulation, voltage support, spinning reserves, and the black start capability. These ancillary services attract between USD 8-18/kilowatt-year capacity payments in organized wholesale electricity market, and frequency regulation services can fetch USD 15-32/megawatt-hour, such that gas turbines can earn 30-45% of total revenue on grid services, not on energy sales.

By 2030, the world's capacity of hydrogen production is expected to reach 180 million metric tons per year, and power generation will be 28-34% of the aggregate demand, which will present an opportunity to address the market gap of hydrogen able gas turbines. Equipment manufacturers give a 12-18% premium on new turbine sales with hydrogen-ready certification, and retrofit market is projected to reach USD 6.8 billion yearly by 2030 to upgrade existing fleet. PJM Interconnection, the largest grid operator in North America, raised capacity market clearing prices between USD 76.53/megawatt-day in 2023 to USD 269.92/megawatt-day in 2025-2026, that is, the cost of increasing the value of dispatchable generation attributes. By 2030, the requirements of grid balancing services by European transmission system operators will have grown 280% over the current level, and the EUR 16-22 billion of annual addressable market by flexible generation assets capable of delivering quick response and sustained output in times of renewable generated power will become a reality.

One such paradigm shift that changes the way gas turbines are operated entails the extensive adoption of digital twin technologies developing advanced virtual representations of the physical turbine assets, constantly updated with real-time sensor data of the more than 8,000-12,000 measurement points on temperatures, pressures, vibrations, combustion dynamics, and the signs of component degradation. These new digital models allow predictive maintenance plans that can maximize inspection cycles, decrease the number of unplanned outages by 38-52 %, and increase the major overhaul cycle of 24000-hour duration in traditional models to 32000-42000 hours due to the ability to monitor degradation accurately and timely replace the components before failure.

With artificial intelligence and machine learning algorithms that examine large volumes of historical operational performance, weather, and fuel quality fluctuations, and grid demand profiles, autonomous optimization of turbine operation is possible. Advanced control systems adjust in real-time firing temperatures, compression ratios, fuel-air ratios, and cooling flows to achieve maximum efficiency and minimum emissions and component thermal stress, yielding 1.4-2.9 %age point improvements in efficiency and saving USD 2.1-3.7 million of fuel each year at USD 4.25 per MMBtu natural gas prices at 400 MW combined cycle facilities operating 4,000–6,000 hours annually, while simultaneously extending maintenance intervals and improving overall plant reliability and availability.

Digitally enabled fleets with advanced monitoring and predictive analytics have recorded 99.2% availability in 2025, versus 96.4% with conventional units, according to leading gas turbine manufacturers, and 21-28% lower maintenance costs through optimization of inspection schedules and predictive component replacement programs. Digital twin-powered combined cycle power plants reported 95-162 BTU per kilowatt-hour heat rate improvement compared to baseline performance, which corresponded to 1.6-2.8% point efficiency improvements and 28–47-pound reductions in carbon dioxide emissions. The total number of gas turbines in the installed base with comprehensive digital monitoring systems has crossed to 52% market penetration in 2025, up from 31% in 2022, with the number of retrofit installations growing 41% annually as operators aim at maximizing the use of their assets and extending their economic lifespan as existing capacity factor and higher cycling duty demands are experienced in their existing fleets.

The highest market share of USD 6,847.3 million is commanded by Asia Pacific, amounting to 39% of global market value with a forecasted CAGR of 5.6 up to 2034. The market leadership is indicative of aggressive demand growth in electricity of 4.8% per year, huge infrastructure development projects, coal-to-gas fuel switching projects necessitated by air quality improvement requirements and large liquefied natural gas importation infrastructure which allows competitive pricing of gas-fired generation.

China constitutes 46% of regional market value of USD 3,149.8 million which is driven by strategic decision of the National Development and Reform Commission to bring up the gas-fired generation capacity to 195 GW by 2030 compared to 118 GW in 2025 as a part of overall air pollution reduction efforts in major metropolitan regions such as Beijing-Tianjin The gas turbine plants in the country focus on high efficiency combined cycle designs with thermal efficiencies of 59-62% that would enable much-needed load-following capacity to supplement 1,400 GW of proposed wind and solar generation, replacing older coal-fired generation.

The gas turbine market in India was USD 1,438.7 million in 2025 with a forecasted 6.4% CAGR to 2034 due to a capacity enhancement program by the ministry of power to add 32 GW of gas-fired generation by 2032 to facilitate renewable energy integration and the substitution of the old liquid fuel-fired generation. The market focuses on turbines with dual-fuel capability that allows them to operate on natural gas, naphtha, and diesel fuels, to allow flexibility in operation when there is limited domestic natural gas availability and when there is fluctuation in the international LNG prices.

The market size in Japan was USD 967.4 million in 2025 with its high levels of hydrogen-capable turbine purchasing to comply with the government Green Growth Strategy of 15 GW of hydrogen-capable gas turbine capacity by 2030. The southeast Asian countries such as Indonesia, Thailand, Vietnam, and the Philippines take up 26% of the regional market value, as a result of the electrification program that needs 52 GW of new generation capacity by 2030, with gas turbines supplying 38 % of the planned capacity increases as a consequence of utilizing rapid deployment plans and operational flexibility to support the economic development agenda.

Middle East and Africa: The greatest growth and resource monetization.

Middle East & Africa was the region with the highest growth rate with the projected CAGR of 6.2% till 2034, which is USD 3,247.8 million in 2025. The fast growth rate in the region is a reflection of the growth rate of electricity demand (5.1 per annum on average), massive scale desalination needs (19-24% of the total power generation), diversification efforts in the economy to decrease the reliance on petroleum exports, and the presence of natural gas resources within the country to allow the region to provide competitive fuel costs in the power generation sector.

Saudi Arabia is a 36 % of the regional market value at USD 1,169.2 million with the Saudi Vision 2030 economic transformation agenda necessitating 64 GW of new generation capacity by 2030, with gas turbines contributing to the baseload and intermediate power required to meet the 58.7 GW of planned renewable capacity additions. The procurement of the kingdom focuses on high-technology H-class and J-class turbines combined with multi-stage flash desalination plants, and with combined cycle efficiencies of over 62 % with 8.4 million cubic meters of desalinated water per day.

The United Arab Emirates market is expected to reach USD 724.6 million in 2025 with implementation of ultra-high efficiency gas turbine technologies with 64% combined cycle performance in support of the UAE Net Zero by 2050 Strategic Initiative and dispatchable generation capacity to ensure energy security. The market in Qatar amounted to USD 398.4 million due to the North Field LNG expansion projects which needed an increase in the generation of power capacity of 4.2 GW to be used in liquefaction facilities and petrochemical complexes.

Europe: Technology Leadership and Hydrogen Transition

Europe had USD 3,892.6 million market value in 2025 with estimated 3.8% CAGR to 2034, high levels of emissions regulation, extensive hydrogen infrastructure development initiatives, high levels of turbine technology deployment, and complex capacity market mechanisms that compensate the flexibility of the dispatchable generation. The area is the international laboratory of hydrogen-enabled gas turbine technologies, with 28 demonstration projects running or being built proving the commercial feasibility of hydrogen combustion systems.

Germany has a European market value of USD 1,206.7 million, which represents 31% of the European market value, driven by the coal phase-out initiative that necessitates 19 GW of gas-fired capacity additions by 2030 as a bridge technology that supports 400 GW of the planned renewable energy capacity and does not compromise grid stability and energy security. The German gas turbine procurement requirements are hydrogen-ready with at least 50% volumetric blending capacity, which has become a global standard in technology that affects global equipment standards.

The market in the United Kingdom was USD 823.4 million in 2025 which was facilitated by capacity market mechanisms which guaranteed 15-year revenue assurance with capacity agreements of GBP 18-42 per kilowatt-year payments to new combined cycle plants. Hydrogen integration The Netherlands is a leader in hydrogen integration, with six utility-scale gas turbine plants already operating on 25-35% hydrogen blends by 2025, enabled by national hydrogen backbone infrastructure linking 1,400 kilometers of re-purposed natural gas transmission lines.

North America: Fleet Modernization and Maturity.

North America had a USD 3,441.4 million market value in 2025 with a forecasted 4.2% CAGR until 2034 due to fully developed infrastructure, a large network of natural gas pipelines that offer competitive fuels and continued shift of coal-fired to gas-fired power generation to ensure integration of renewable energy. The area is blessed with a natural gas production of 118 billion cubic feet per day on average, which allows fuel costs of USD 2.80-4.20 per MMBtu, and which has kept gas turbine economic competitiveness despite renewable energy cost savings.

The United States controls 83% of the North American market share at USD 2,856.4 million with gas turbines contributing 41% of the total electricity generation in 2025. The market focuses on coal-fired capacity replacement, with 42 GW of coal retirements between 2025-2030 demanding dispatchable generation options, and a growing use of aeroderivative turbines with better cycling ability and quick response functionality needed to integrate renewables in states such as California, Texas, and New York.

The Canadian market is USD 448.7 million in 2025 and is projected to grow at a CAGR of 4.6 per cent to 2034 with Alberta and Ontario capacity addition as per the commitments to phase-out coal and as a backup reserve to hydroelectric systems during drought periods that affect the water level and generation capacity.

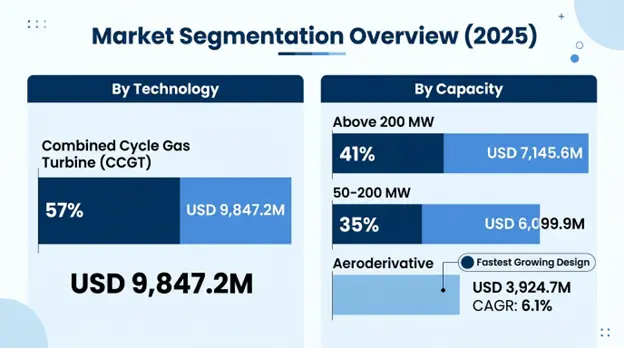

Above 200 MW segment has majority market share of 41% of total revenue amounting USD 7,145.6 million in 2025 which is used to represent large-scale utility installations, and industrial cogeneration facilities. This segment includes highly developed H-class and J-class turbine technologies with combined cycle efficiencies of 62-64% and firing temperatures more than 1,600 C with single crystal nickel superalloy materials and enhanced thermal barrier coating systems.

50-200 MW segment has 35 % market share of USD 6,099.9 million in 2025, which includes mid-scale utility projects, industrial cogeneration projects, and distributed generation installations. This power scale provides the best tradeoff between economies of scale and operational flexibility, with turbines having combined cycle efficiencies of 58-61% and having rapid startup and load-following allowing the turbine to operate with renewable support.

The most market uses are a combined Cycle Gas Turbine (CCGT) technology, which will account USD 9,847.2 million in 2025 and make 57 % of the total market worth. CCGT schemes combine gas turbine topping cycles with steam turbine bottoming cycles, utilizing turbine exhaust waste heat to produce more electricity, which has a total thermal efficiency of 58-64% versus 36-42% when operated as a simple cycle.

Aeroderivative Gas Turbines is the fastest growing design segment with 6.1% CAGR forecast up to 2034 with the 2025 value USD 3,924.7 million. Based on aircraft jet engine technology, they have a better power / weight ratio, fast start values of 8-12 minutes and modular maintenance strategies of full engine replacement in 24-36 hours so that they are ideal in peaking applications and renewable integration support.

The gas turbine industry is highly monopolized worldwide with five main manufacturers that own about 82-87 % of the total global production capacity and aftermarket services revenue. Competitive differentiation focuses on the thermal efficiency leadership, hydrogen combustion capability, digital monitoring and optimization systems and lifecycle service offerings include maintenance, parts supply and performance optimization services over 15–25-year contracts.

Major corporations have vertically aligned business processes that include research and development, high-tech materials production, precision machining, assembly, project implementation, and long-term service contracts that create continuous stream of revenues amounting to 48-55% of total company income. The competitive environment focuses on technological leadership in progressive cooling system, optimization of combustion, materials science, and digital twin integration to support predictive maintenance and autonomous performance optimization.

Hydrogen-ready development of combustion systems with roadmaps to 100% hydrogen capability by 2028-2030, service business growth through remote monitoring, performance optimization, and increasing the service life of assets through additive manufacturing technologies are strategic focus areas. Firms are spending a lot of money on artificial intelligence and machine learning to use predictive maintenance, autonomous optimization, and improved customer services.

March 2026: General Electric Company reported a successful test of the 100% hydrogen-fueled gas turbine, the first commercial-scale, at a 520 MW combined cycle plant in the Netherlands, indicating that a zero-carbon gas turbine could be operated technically, and that advanced combustion system changes to allow pure hydrogen combustion without increasing nitrogen oxide emissions were feasible.

February 2026: Siemens Energy AG wins USD 3.4 billion contract with Saudi Electricity Company to supply sixteen H-class gas turbines with a total capacity of 8960 MW to support the program of expansion of the power sector in the kingdom, with equipment that has hydrogen-ready combustion lines that can blend hydrogen by 50 % at commencement and 100 % by 2030, aligning with Saudi Arabia’s long-term decarbonization and energy transition goals.

January 2026: Mitsubishi Power Ltd. acquired European gas turbine services provider with USD 1.2 billion to expand aftermarket services across 420 installed turbines in 22 countries to enhance competitive advantage in the high-margin maintenance and parts supply business with recurring revenue streams, and EBITDA margins of 34-41.

December 2025: Ansaldo Energia released GT36-H2 Advanced gas turbine with 65.2% combined cycle efficiency on natural gas and 62.8% efficiency on 100% hydrogen fuel, the highest-efficiency hydrogen-capable turbine on the market, with first deployment planned in 2028 at Italian utility facility to support coal phase-out.

November 2025: Solar Turbines (Caterpillar Inc.) won USD 420 million contract to deliver 32 industrial gas turbines with total output of 960 MW to Qatar petroleum processing facilities to supply mechanical drive to LNG compression and power generation with dual-fuel capability to run on either natural gas or liquid fuels.

List of Key Players in Global Gas Turbine Market

Global Gas Turbine Market Segments

By Capacity:

By Technology:

By Design:

By Fuel Type:

By Application:

By End-User Industry:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 Apr 2026

Intellectual Market Insights Research © 2026. All rights reserved.