Share this link via:

The global beta-2 adrenergic receptor agonist market was valued at USD 21.8 billion in 2025 and is projected to reach USD 23.1 billion in 2026, expanding to USD 34.2 billion by 2034, growing at a CAGR of 5.4% during the forecast period (2026-2034).

Beta-2 adrenoceptor agonists are a very important category of bronchodilator drugs that act only upon the selective beta-2 adrenoreceptors found primarily on airway smooth muscles of the lungs. These sophisticated drugs act by binding to seven-transmembrane G-protein-coupled receptors leading to activation of intracellular cascades involving adenylyl cyclase activity, increased cyclic adenosine monophosphate levels, and protein kinase A activation, thereby causing smooth muscle relaxation, bronchodilation, and immediate relief of bronchial obstructions. Some of the categories of this drug are the short-acting beta-2 agonists comprising of salbutamol and terbutaline providing instant relief in bronchodilation, the long-acting beta-2 agonists comprising of salmeterol and formoterol providing 12-hour bronchodilation, and the ultra-long-acting beta-2 agonists comprising of indacaterol, olodaterol, and vilanterol providing once-a-day dose schedule.

Modern beta-2 agonists have pharmacological advantages not only due to their ability to induce bronchodilation but also because of additional modes of action, such as mast cell stabilizing, which results in decreased inflammatory mediator release, improved mucociliary clearance via increased ciliary beat frequency, microvascular leakage reduction, and neurotransmitter release modification from airway nerves. Their pharmacological diversity explains their established status as the first-line medication recommended in all current respiratory disease treatment guidelines. Due to the anatomical and physiological properties of the respiratory system, medications must be delivered through specialized methods, which, in the case of beta-2 agonists, would be inhalation, because this method enables obtaining maximum concentrations within target airway smooth muscle while avoiding systemic distribution.

Beta-2 adrenergic receptor agonists are no longer merely available in the form of mono-inhaler formulations but have diversified into combination inhalers that combine beta-2 agonists with other medications, such as inhaled corticosteroids for asthma or long-acting muscarinic antagonists for chronic obstructive pulmonary disease management. The combinations result in a synergetic mechanism of action with the added advantage of using only one inhaler as opposed to two or more different inhalers, which improves patient compliance and results in high-value commercial opportunities far exceeding the price of each constituent separately. This market focuses on managing chronic respiratory disorders affecting over 650 million people worldwide suffering from asthma and chronic obstructive pulmonary disease collectively.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 21.8 Billion |

| Forecast Value | USD 34.2 Billion |

| CAGR | 5.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Route of Administration, Formulation, Indication, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | GlaxoSmithKline plc, AstraZeneca plc, Boehringer Ingelheim, Novartis AG, Teva Pharmaceutical Industries |

Get more details on this report - Request Free Sample

The primary driver of the beta-2 adrenergic receptor agonist market is the growing global burden of chronic obstructive airway diseases, with asthma affecting approximately 339 million people worldwide while chronic obstructive pulmonary disease is experienced by roughly 384 million people as the biggest burden of chronic respiratory diseases to be faced by any health care systems irrespective of their economic status. The burden of asthma continues to increase, especially in urban settings because of higher air pollution, indoor allergens, occupational sensitizers, and the effects of the way of life with childhood asthma rates between 5 % and 21% in various nations and adult-onset asthma as a problem at both the occupational and environmental levels. Economic burdens of asthma are huge with total cost estimates being more than USD 82 billion annually.

Chronic obstructive pulmonary disease is the third most significant cause of death in the world and is responsible for the deaths of 3.23 million people every year. Prevalence forecasts indicate a continued rise in COPD incidence through 2034 due to historical tobacco smoking trends in aged populations, biomass fuel burning in the rural population especially in developing countries, occupation-related dust and chemical exposure in the mining, building, and manufacturing industries, and increasing cases of non-smoking COPD from exposure to indoor air pollution. The irreversible nature of COPD necessitates lifelong bronchodilator therapy, with beta-2 agonists being the basis of pharmacotherapy for all disease severity classes according to the Global Initiative for Chronic Obstructive Lung Disease guidelines.

The key business restriction for existing beta-2 agonist companies is the continuous impact of generic competition after patents expire for large-volume branded medications, with generics of salbutamol, salmeterol, and formoterol, and their combinations gaining high market shares and causing price erosion in the range of 35-65% from pre-generic levels. The inhaled medications industry is characterized by special requirements in the process of developing generic drugs as compared with normal oral preparations, which include the need to prove similar lung deposition using bioequivalence studies, aerodynamic analysis of particle sizes of the active ingredient in vitro, and other clinical endpoints, which increase development complexity but do not hinder access to the market.

Generic inhaler market share amounted to 34% of overall beta-2 agonists prescription volumes by 2025, owing to several companies obtaining approval for the sale of generics to salbutamol MDI inhalers, budesonide-formoterol DPIs, and fluticasone-salmeterol combinations. Price pressures have seen the average selling price of such products fall by 40-60% within two years from launch of the generics, forcing brand-name manufacturers to concentrate their efforts on next generation combination therapies, superior device technology, and value-added services.

An emerging market limitation is the increasing regulation aimed at discontinuing hydrofluorocarbon propellant inhalers because of the significant global warming potential presented by these inhalers. Specifically, hydrofluorocarbon propellant inhalers have approximately 1,430 times the global warming potential of carbon dioxide compared to carbon dioxide over a period of 100 years. The United Kingdom’s National Health Service has introduced guidelines encouraging physicians to transition away from pressurized metered dose inhalers to greener options such as dry powder inhalers and soft mist inhalers.

The shift towards sustainability generates considerable product reformulation challenges for the manufacturing companies, forcing them to invest in next-generation inhalers with low GWP propellants or even those that do not use propellants at all, making it a costly endeavor in terms of capital investments and even market disruptions as well. The changes in regulations primarily apply to high volume products where calculation of the environmental effect indicates considerable implications, obliging companies to ensure efficacy while maintaining environmental standards.

The Asian Pacific region, Latin America, the Middle East, and Africa offer considerable opportunities due to the presence of large populations with chronic respiratory diseases; however, the incidence of diagnosis and treatment along with the cost of medicines present considerable challenges. According to World Health Organization data, about 80% of asthma fatalities occur in low-income and middle-income nations, where even the most fundamental bronchodilation is not always accessible, highlighting the urgent need for affordable beta-2 agonist therapies in these regions.

Investment in the healthcare infrastructure within these areas such as increasing primary care services for respiratory diseases, training community healthcare workers for managing chronic ailments and adding beta-2 agonists to national essential medicines lists is improving treatment access and contributing towards market volume growth. In China, the country’s reform within healthcare insurance that included respiratory drugs within the national reimbursement list contributed to an increase in prescriptions by 34% from 2022-2025 whereas in India, Ayushman Bharat, with a population of 500 million, made inhaled bronchodilator therapy more accessible.

Advancements in respiratory pharmacogenomics are driving a shift toward individualized beta-2 agonist therapy, as genetic markers are employed to determine the most effective treatment choice according to the extent to which patients exhibit polymorphisms in their ability to respond to bronchodilation, the duration of effect, as well as predisposition towards tolerance formation through exposure to agonists. The Arg16Gly mutation is an example of such a marker, as Patients with the Arg16 homozygous genotype demonstrate reduced responsiveness to repeated inhalation of short-acting beta-2 agonists relative to Gly16 homozygotes.

Given the decreasing cost and increasing accessibility of pharmacogenomic tests, there is an opportunity for the development of companion diagnostics along with the advancement of second-generation beta-2 agonists to facilitate precision medicine strategies that can optimize patient benefits while reducing negative side effects. This concept has been implemented in the practice of clinical respiratory therapy by way of asthma specialty centers and integrated health systems, with promising results indicating that genetic testing can improve response to treatment by 20-30%.

North America leads in terms of market leadership with an estimate of USD 8.7 billion in 2025, contributing 40% to the worldwide beta-2 agonists market value, due to the high prevalence of chronic respiratory diseases impacting 25.3 million Americans with asthma and 16 million Americans with chronic obstructive pulmonary disease, well-established coverage of insurance from Medicare, Medicaid, and commercial insurers ensuring the availability of superior combination inhalation medicines, and developed pulmonology subspecialties enabling complex disease management. The U.S. healthcare system demonstrates strong adoption of innovative respiratory therapies, and the brands still hold a strong market presence despite the competition from generics through differentiation.

Market forces within the region receive assistance from the presence of strong research and development facilities located in pharmaceutical centers, regulations that favor fast-track approvals of novel respiratory treatments via FDA’s breakthrough designation scheme, and payers who are prepared to cover the costs of expensive yet more efficacious treatment modalities with improved exacerbation reduction effects. The Medicare Part D expenditures related to inhaled respiratory drugs, such as beta-2 agonists, amounted to USD 4.8 billion in 2025, while commercial insurance still holds favorable formulary status for effective combination therapies.

Asia-Pacific is the fastest-growing regional market, projected to register a CAGR of 7.8% through 2034, valued at USD 6.2 billion by 2025, due to large population sizes, in excess of 4.7 billion, and rapidly increasing incidence of respiratory diseases associated with urbanization, air pollution, and lifestyle modifications, which are especially evident in major cities in China, India, and Southeast Asia, along with increased healthcare insurance coverage that facilitates access to drugs for a growing number of middle-income individuals. China emerges as the leader of the regional market owing to its high incidence of asthma (45 million) and COPD cases (99.9 million), the highest among any country, due to national reforms in healthcare, particularly the inclusion of drugs on the national reimbursement list.

The regional market expansion can be facilitated by the development of domestic pharmaceutical manufacturing capability, where the generic inhalers manufactured in India contribute 28% to total world consumption in 2025, cooperation between multinationals in pharmaceuticals and their domestic counterparts allowing them access to the markets at reasonable prices, and healthcare investments that would facilitate subspecialty training programs and advanced diagnostic capability. There is significant growth potential in the region for cost-effective generic combination medications, intelligent inhalers that leverage technological savvy of younger consumers, and telemedicine respiratory treatments.

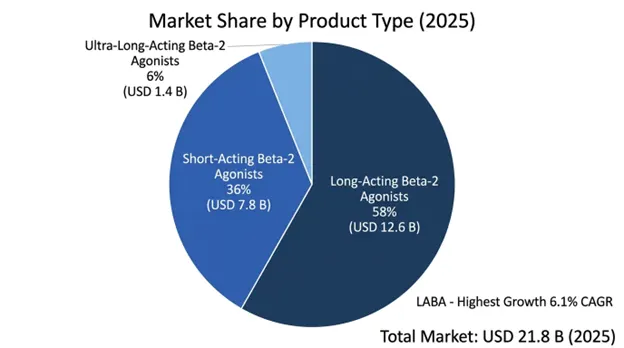

The Long-Acting Beta-2 Agonists are the highest-selling product type in 2025, accounting for 58% and worth USD 12.6 billion, experiencing a 6.1% CAGR until 2034. The category comprises salmeterol, formoterol, indacaterol, olodaterol, and vilanterol, which are mostly sold in fixed-dose combinations with inhaled corticosteroids or long-acting muscarinic antagonists for maintenance treatment in moderate-to-severe asthma and COPD. The category enjoys premium pricing due to its excellent performance, guideline-based recommendation, and easy-to-follow treatment protocols that help increase patients' compliance as compared to the repeated intake of the medicines.

The asthma treatment segment is leading to the indication segments with USD 11.8 billion revenues in 2025 and anticipated 5.6% CAGR up to 2034, due to the large global patient population exceeding 339 million, requirement of a combination therapy per guidelines for chronic asthma, and high-cost brands sustaining their market positions by providing clinical differentials to patients. This segment gains from higher awareness about severe asthma and use of biologics in its management.

The Retail Pharmacies end-use segment accounted for the highest revenue share of 54%, estimated to be worth USD 11.8 billion in 2025. This dominance is attributed to the outpatient management requirements of chronic respiratory diseases, which involve frequent prescription refills The growth in this segment is supported by the growing availability of pharmacy-based clinical services such as medication therapy management.

The global beta-2 adrenergic receptor agonist market is moderately concentrated, with the top six firms accounting for approximately 64% of the total value of the branded market share in relation to a broad respiratory portfolio comprising several beta-2 agonists, various inhaler technologies, and successful fixed-dose combinations backed by significant clinical evidence and commercialization efforts in multiple geographic regions. The competitive positioning of these firms involves innovation regarding inhaler technology that enhances usability and proper administration, superior clinical evidence showing reductions in exacerbations and improving quality of life, digitized health technology enabling connected health management, and strong patient support initiatives.

March 2026: AstraZeneca reported promising results from Phase III trial for novel generation of budesonide-formoterol soft mist inhalation showing similar efficacy with conventional dry powder preparations but with better lung deposition efficiency in patients with poor peak inspiratory flow.

February 2026: GlaxoSmithKline obtained FDA approval for digitalized variants of fluticasone-salmeterol combination inhalation therapy featuring a built-in Bluetooth sensor allowing immediate monitoring of treatment compliance and inhalation technique using app for smart phones, thus being first smart inhalation device approved for existing combined medication.

January 2026: The Phase II clinical development of an ultra-long-acting beta-2 agonist drug, which showed effectiveness for a period of 48 hours in pre-clinical trials, was started by Boehringer Ingelheim with the aim of administering the drug twice weekly as a treatment for chronic obstructive pulmonary disease (COPD).

November 2025: Teva Pharmaceutical Industries released its generic version of the budesonide and formoterol inhalation dry powder in the United States after FDA approval, thus making entry into a lucrative market worth over USD 800 million per year.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.