Share this link via:

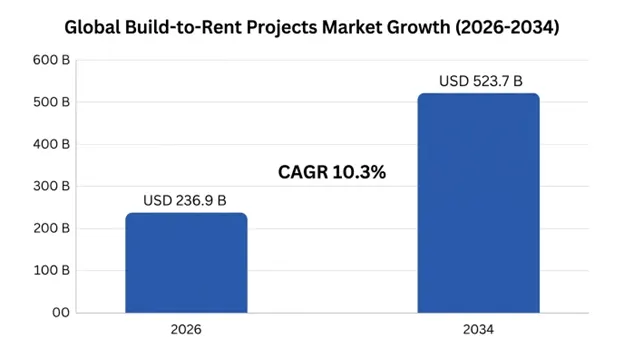

The global build-to-rent projects market size was valued at USD 210.4 billion in 2025 and is projected to reach USD 236.9 billion in 2026, expanding to USD 523.7 billion by 2034, growing at a CAGR of 10.3% during the forecast period (2026-2034).

Build-to-Rent is a transformative residential real estate concept in which housing units are specifically designed, built, and managed for long-term institutional rental purposes rather than for the sale of individual units, as seen in conventional residential developments. This model creates professionally managed residential communities characterized by high service standards as well as efficient integration of amenity offerings like those in commercial real estate. Contrary to conventional residential development, build-to-rent developments are institutionally owned and therefore offer asset management and capital reinvestment opportunities to preserve standards and deliver hospitality services at the highest levels possible.

The design of build-to-rent communities is based on a sophisticated understanding of modern renter lifestyles. This includes design features and amenities created specifically for renter households and not modifications of residential properties intended for homebuyers. Build to rent developers put in considerable effort in providing communal spaces that include co-working facilities with high-speed internet, gyms, roof decks with kitchen facilities, dog parks, and pet-washing stations, concierge services, integration of smart home features, and other features that create quality lifestyle experience in residential communities.

Modern build-to-rent properties increasingly incorporate advanced technology systems for property management, communication with tenants, coordination of maintenance tasks, and revenue maximization using artificial intelligence and machine learning. Technology ecosystems help property operators provide a seamless experience through virtual tours, online leases, maintenance requests via apps, and even management of community events, but at the same time generate insightful information on which decisions can be made regarding maintenance, pricing strategies, and tenant retention programs.

The market’s investment thesis is supported by several attractive fundamentals such as the undersupply of housing within key urban markets around the world, lower homeownership rates as a result of unaffordable housing and changes in lifestyle preferences, rising investor interest in defensive income-producing properties with cash flows that track inflation, and changing demographics leading to ongoing demand for rental housing among various groups.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 210.4 Billion |

| Forecast Value | USD 523.7 Billion |

| CAGR | 10.3% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Property Type, Investment Model, Management Model, Price Segment, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Netherlands, Ireland, Spain, Australia, Japan, Singapore, China, India, UAE, Brazil |

| Key Market Playes | Greystar Real Estate Partners, Blackstone Inc., Invitation Homes, Cortland, Grainger plc, Legal & General, Quintain |

Get more details on this report - Request Free Sample

The primary driver of the rapid growth of the BTR market is the worsening global housing affordability crisis, which has resulted in the complete decoupling of homeownership from middle-class economics in major urban centers, where median house prices are between 12 and 18 times higher than annual incomes in metropolitan areas such as London, Sydney, Toronto, Vancouver, and many others on the US coasts. Housing unaffordability requires homebuyers to save between USD 100,000 and USD 200,000 for down payments and spend 45-55% of their salaries on mortgages, which is not sustainable and excludes increasingly greater numbers of working-age individuals from homeownership.

The growing population of long-term renters has created sustained demand for quality rental housing beyond what fragmented private landlords can provide. Developed economies have experienced consistent declines in homeownership rates, with America's percentage dropping from 69.2% in 2004 to 65.6% in 2025, that of the UK dropping from 71% in 2003 to 62.8% in 2025, and similarly declining homeownership levels in Australia as prices rise beyond increases in wages in major urban areas. These broader trends demonstrate affordability issues but are also driven by a change in the preferences of younger generations towards geographic mobility to support careers, the flexibility of not being locked into property ownership, and the lack of maintenance obligations associated with rentals.

This demographic shift is driven not only by affordability constraints but also by lifestyle preferences among millennials and Generation Z, who have different views about living and prefer urban environments that facilitate community-based residential areas and provide curated amenities to improve their living experience. The concept of build-to-rent focuses on addressing these preferences by providing professionally managed communities with an apartment-style rental environment that offers hotel-like amenities and service levels.

The growth of the build-to-rent sector is fundamentally supported by a major shift in institutional capital toward residential real estate because of the asset class’s resilience across economic cycles, its link to inflation, and its strong return profiles compared to commercial real estate, which is increasingly being affected by trends toward remote work and online shopping. Institutions managing more than USD 120 trillion of investments have raised their allocation targets for residential real estate from around 3-4% to 8-12%, reflecting their need to match liabilities to investments that provide inflation-linked income over the long term.

The Build-to-rent properties possess unique characteristics that appeal to institutional investors, such as predictable monthly rental cash flows generated from diversified tenant bases consisting of hundreds of leases within a single property; inherent protection against inflation risk due to yearly rent revisions based on market factors and consumer price index increases; low correlation with stock market movements; and true scarcity as it is difficult to develop in highly constrained urban areas with limited availability of land and restrictions on planning. Build-to-rent property proved to be remarkably resilient during the COVID-19 pandemic and subsequent inflationary cycle with lower fluctuations in residential rents compared to other commercial real estate.

The process of maturation of build-to-rent into an accepted investment asset class has been hastened due to the availability of standardized benchmarking of performance, clear transaction markets providing pricing information, and a professional investment management infrastructure which has enabled institutions to confidently invest in large-scale operations through capital deployment. Forward-funding investment structures, whereby institutions finance developments during construction to acquire buildings at discounted prices on completion have emerged as key forms of capital deployment, thus providing certainty in terms of supply and allocation of risks.

The primary constraint affecting build-to-rent project expansion is the sharp increase in construction costs combined with rising interest rates that have affected the profitability of developments within several markets. Average annualized cost growth of the construction industry during 2021-2024 was 8.4%, due to high material prices, shortage of skilled labor, and disruption in the supply chain process. Meanwhile, interest rates have increased from 2-3% to 6-8% among major markets.

As a result, narrowing margins between achievable rents and total development costs have delayed many planned projects either under planning or pre-construction stages, especially if the development was already planned based on lower cost assumptions for the construction phase. For many developers, there needs to be an increase in rents of 6-8% each year to achieve their target yield rates.

Build-to-rent developments face significant regulatory challenges due to planning policies that are not geared towards the development of purpose-built rental accommodation, hence making it difficult and impractical to apply residential property regulations which include having too much parking space and requirements for unit mixing which might be inappropriate to the rental demographic population. The process of acquiring planning permission to develop build-to-rent projects usually takes around two to three years on average.

Single-family build to rent stands out as the most viable avenue for growth in terms of addressing the unmet needs of families and aging individuals who require larger spaces that cannot be offered by multi-family developments. Single-family rental communities offer a combination of the space offered in suburban homes along with professional management and communal facilities. These properties offer suburban-style living through rental arrangements rather than homeownership.

Operational performance metrics for single-family build-to-rent communities are stronger than those of multifamily developments as occupancy is around 96-98% while the length of stay ranges from 3.5-5 years due to growth in rental prices, which is enabled through limited supply of quality family housing in suburbia. The movement of this segment towards the UK, Australia, and Europe indicates that the need for family housing is universally applicable since multifamily housing cannot meet the same requirements.

Environmental, Social, and Governance (ESG) considerations are no longer optional marketing tools but essential requirements for institutional capital raising, thereby presenting a wealth of opportunities for build-to-rent businesses that adopt sustainability as a key aspect of their business and operating practices. Net-zero carbon build-to-rent projects that use renewable power, high-performing building shells, and electric building services can earn rent premium margins of 5-8%.

The build-to-rent industry is diversifying its offerings from classic apartment buildings to co-living projects that provide small-sized units coupled with abundant shared facilities, flexible tenure conditions suitable for different rental demands, and community activities designed to meet social connectivity needs among city tenants. Co-living projects generate better rent per square foot than apartments and help resolve severe affordability problems in tight urban markets by utilizing space efficiently.

Advanced artificial intelligence applications are transforming build-to-rent operations through predictive analytics that help in maintaining optimal schedules for maintenance and energy management, apart from managing tenants’ requirements in an effective manner to increase rental income. Applications of machine learning algorithms help identify behaviors and trends regarding tenants as well as the environment around them to enable decision-making.

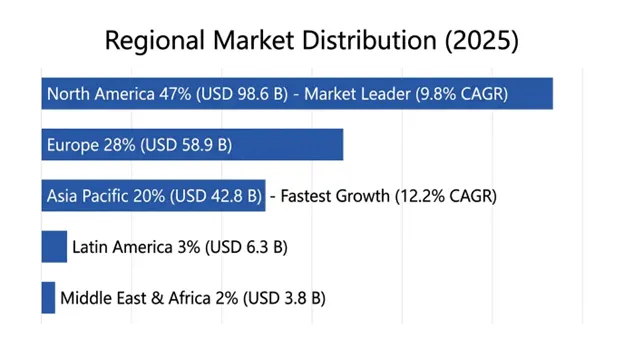

North America held the largest market share, valued at USD 98.6 billion in 2025, and is projected to grow at a CAGR of 9.8% through 2034. The US holds the value of 91% in North America due to its advanced institutional rental housing market, property management systems, and flourishing single-family rental industry which has witnessed robust growth since 2012. The US market enjoys deep capital markets, standardized lease agreements for easy and cost-effective management of properties, and cultural norms supporting the concept of renting.

Single-family build-to-rent has become the primary growth driver in North America, with large players such as Invitation Homes, American Homes 4 Rent, and Tricon Residential owning portfolios with more than 50,000 properties in Sun Belt regions, where the combination of population and employment growth along with affordable housing creates an environment that favors operations. Purpose-built communities have become favored over scattered sites owing to efficiency gains and the ability to maintain consistency in tenant experience through larger portfolios.

Asia Pacific emerged as the fastest-growing regional market, registering the fastest CAGR of 12.2%, up to 2034, to hit USD 42.8 billion in 2025. The reasons behind regional growth are the urbanization of emerging nations, the development of institutional property investing platforms in Australia and Japan, as well as increasing awareness of build-to-rent as an affordable housing option in large cities such as Singapore, Seoul, and Shanghai.

Australia is leading the way with regards to regional market development through rapid expansion in the build-to-rent pipeline in Sydney and Melbourne, thanks to tax reform that has stripped managed investment trusts of their disadvantages, as well as incentives from state governments to develop residential housing for rent on a large scale. The Japanese rental housing market has been moving towards institutional housing, while Singapore and South Korea are building regulatory frameworks to support build-to-rent investments.

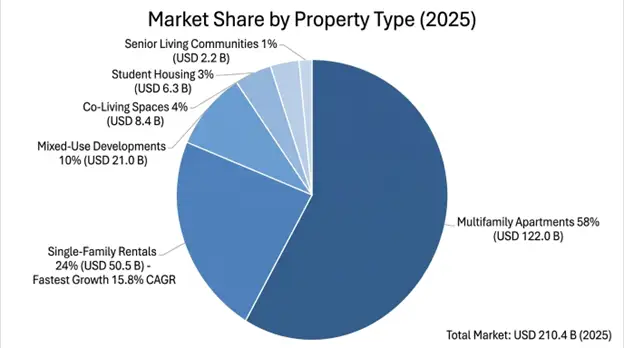

Multifamily Apartments account for the highest share of the market, amounting to 58% worth USD 122.0 billion in 2025, recording a 9.4% CAGR between 2026 and 2034. This dominance is supported by its well-established investment model, effective use of land in urban areas, and scalability, making it possible to professionally manage large numbers of units at once. Multifamily Apartments gain momentum due to high demand among young professionals and couples.

The category experiencing the fastest growth is Single Family Rentals with a 15.8% CAGR due to family needs for space and privacy in conjunction with institutional awareness of improved metrics such as increased tenure, reduced turnover expenses, and better growth through renting. Single family purpose-built rental communities are revolutionizing the suburbs by offering management and amenity services not previously available in scattered private rentals.

Forward Funding takes the lead with 44% share, owing to institutions’ desire for development risk transfer to experts in the development process while assuring delivery of the pipeline at pre-agreed prices. Joint Ventures follow suit with 28%, thanks to the combination of international capital sources and local expertise in development.

The Mid-Market Segment is leading with 52% market share, which focuses on customers whose income is 80-120% of the area median income, people requiring quality rental homes yet unable to opt for homeownership. The Premium/ Luxury Segment shows strong growth potential with 13.2% CAGR owing to their search for hotel-quality homes.

The build-to-rent market in the world is moderately concentrated, with the operators and institutions having significant shares in developed build-to-rent regions, but with fragmentation still prevailing in developing build-to-rent regions. Competitive advantages include the ability to deliver high-quality operational platforms that provide better experiences for tenants, brand identity among the targeted segments, technological advantage that improves efficiencies, and pipeline size that gives visibility to institutions.

Platform operators seek to capitalize on growth through organic growth, portfolio acquisitions, and management contracts by third parties to create scale efficiencies that will help make technological investments economically viable. Increasingly, competitive advantage is obtained using data analysis to enhance revenue management, PropTech to promote tenant retention, and ESG status to attract capital and tenants.

April 2026: Greystar Real Estate Partners reported build-to-rent commitments worth USD 4.2 billion in Europe, focusing on 12,000 units in the United Kingdom, Ireland, and the Netherlands that will be delivered from 2027-2030.

March 2026: The Blackstone Group concluded its purchase of a 7,500-unit single-family build-to-rent property portfolio in Sun Belt markets at a total deal value of USD 2.8 billion, thus bringing its residential property portfolio to more than 55,000 units.

February 2026: Legal & General announced the launch of a GBP 1.5 billion build-to-rent investment scheme aimed at regional UK cities such as Manchester, Birmingham, and Leeds, due to rising rental demands beyond London as well as the viability created by falling land prices.

January 2026: Cortland has introduced its centralized AI-based property management system, powered by machine learning algorithms, across its 85,000 units portfolio worldwide.

November 2025: Invitation Homes partnered with a North American home builder in forming a strategic joint venture to develop 5,000 single-family rental properties worth USD 1.8 billion in the US Sun Belt cities over a period of three years.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.