Share this link via:

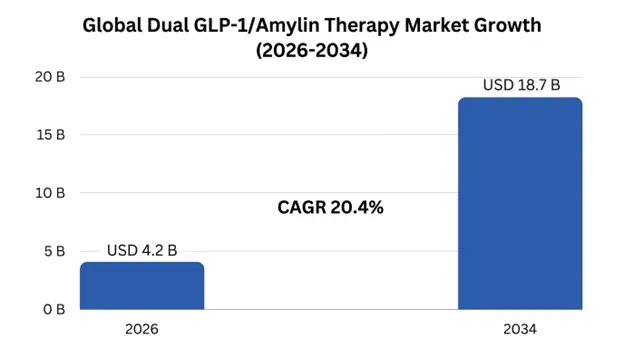

The global dual GLP-1/amylin therapy market size was valued at USD 2.8 billion in 2025 and is projected to reach USD 4.2 billion in 2026, expanding to USD 18.7 billion by 2034, growing at a CAGR of 20.4% during the forecast period (2026-2034).

Dual GLP-1/Amylin therapy is the latest revolutionary innovation in metabolic science where a dual mode of hormonal action is utilized to produce unprecedented results in the treatment of diabetes and weight loss. Using the innovative approach of GLP-1 and Amylin analogs therapy in combination, the positive impact of GLP-1 receptor agonists and the benefits of Amylin analog treatment are used to target deficiencies that are common among people with type 2 diabetes and obesity. The basis for this novel combination therapy lies in the fact that both GLP-1 and Amylin hormones are secreted by pancreatic beta cells in the body upon food ingestion; however, their concentrations are depleted in people with type 2 diabetess and are entirely missing in people with type 1 diabetes.

The GLP-1 receptor agonists operate via several mechanisms that include increasing glucose-stimulated insulin secretion from the pancreatic beta cells, inhibiting the secretion of inappropriate glucagon in cases where blood glucose is high, slowing down gastric emptying to help control the glucose excursions, and activating brain centers such as the hypothalamus and brain stem to enhance satiety and suppress food intake. Amylin, a peptide hormone composed of 37 amino acids, operates in conjunction with GLP-1 to achieve similar objectives using unique yet complementary pathways that include enhanced inhibition of glucagon secretion, further modulation of gastric emptying by vagal nerve activity, and activation of area postrema receptors in the brain stem to induce satiety by pathways that are relatively independent of GLP-1 pathways.

The clinical utility of dual GLP-1/amylin administration is not limited to mere additive actions of each drug separately, as synergy has been observed, resulting in weight loss outcomes comparable to bariatric surgery while maintaining effective glucose metabolism and avoiding muscle atrophy. The administration of cagrilintide, an extended-release amylin analog, in combination with semaglutide has shown average weight loss of 22.7% after 68 weeks of treatment in obese subjects compared to 15.7% weight loss with semaglutide alone, marking a 44% increase in weight loss efficacy compared to monotherapy, and putting it into a category of bariatric surgery alternatives.

The therapeutic ecosystem is focused on addressing critical unmet medical needs among the global population in which more than 1.1 billion people are considered obese, while about 537 million suffer from diabetes; diabesity has become one of the largest public health challenges in the 21st century. Target patient populations include people who have shown inadequate response to traditional treatment based on the use of GLP-1 receptor agonists monotherapy, people that require stronger metabolic treatments for the purpose of reversing the disease or prevention of related cardiovascular diseases, and people looking for alternatives to bariatric surgery for overcoming obesity and related diseases such as sleep apnea and non-alcoholic steatohepatitis.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 2.8 Billion |

| Forecast Value | USD 18.7 Billion |

| CAGR | 20.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By Product Type, Indication, Route of Administration, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Novo Nordisk A/S, Eli Lilly and Company, AstraZeneca PLC, Zealand Pharma A/S, Boehringer Ingelheim GmbH |

Get more details on this report - Request Free Sample

Unprecedented global obesity and type 2 diabetes epidemic along with their accelerating growth rate are the key drivers of the expansion of the market for dual GLP-1/amylin therapies, especially in emerging economies that are rapidly urbanizing and transitioning to a new diet. According to the International Diabetes Federation, 537 million adults were living with diabetes in 2025 and by 2045, the number is projected to increase to 783 million, and the World Health Organization estimates that global obesity prevalence has almost tripled since 1975, and that more than 1.1 billion adults are now considered obese globally. These coepidemic conditions result in a huge patient population that can be reached, with around 85-90% of the type 2 diabetes cases being attributed to excess body weight/central adiposity.

The unmet clinical need is significant, and dual GLP-1/amylin therapy has the potential to address several of these gaps. There is consistent real-world data that conventional treatment approaches leave less than half of type 2 diabetes patients with their A1C readings below 7.0% and less than one-quarter of patients with combined A1C, BP, and lipid targets. The amount of weight lost from the use of the most effective weight loss GLP-1 receptor agonists (2.4 mg semaglutide) usually reaches 14-17% of the individual's pre-treatment body weight, with a large percentage of patients with severe obesity failing to reach the 20-25% of their body weight to be considered for diabetes remission and a significant cardiovascular risk reduction.

The dual GLP-1/amylin mechanism approaches this therapeutic ceiling by multiple and non-overlapping pathways that do not involve compensatory mechanisms that limit the efficacy of single-hormone therapy. The clinical results from the REDEFINE and COMBINE trial programs prove that, with CagriSema, weight loss of up to 22–25% in obese patients with type 2 diabetes is possible, in regions where bariatric surgical intervention was previously the only way.

The growing clinical trial data in Phase III showing efficacy of dual GLP-1/amylin co-activation over current GLP-1 monotherapy are a game-changer for the market, delivering the clinical evidence required to support FDA regulatory approval, positive payer coverage decisions, and physician adoption in the increasingly competitive diabetes and obesity treatment landscape. The landmark REDEFINE clinical program designed to investigate the efficacy of CagriSema will yield unprecedented efficacy data, elevating CagriSema to a therapeutic class on its own and not simply an incremental step over current treatments.

In adults with obesity but without diabetes, REDEFINE-1 Phase III showed a mean body weight loss of 22.7% with CagriSema compared to 15.7% seen in the semaglutide alone group, demonstrating 44% greater weight loss efficacy. But more significantly, the percentage of patients reached the clinically relevant weight loss milestones significantly more rapidly; 40.6% of CagriSema patients lost ≥20% weight compared to 18.3% of those taking semaglutide monotherapy. CagriSema was shown to achieve reductions in HbA1c of 2.2 percentage points, compared with 1.8 percentage points with semaglutide alone, and superior weight loss of 15.6%, versus 8.2%, in the type 2 diabetes patient population studied in COMBINE-1.

These results provide strong evidence that dual GLP-1/amylin therapy may be practice-changing, potentially providing a way for clinicians to replicate bariatric surgery results in terms of weight loss and glycemic control without the invasiveness or irreversibility of surgery. The clinical implications are especially interesting because, although GLP-1 receptor agonists have been shown to benefit patients, they often do not produce sufficient metabolic improvement to achieve diabetes remission or to prevent major cardiovascular events among high-risk patients.

The shift in practice toward more holistic care and treatment of cardiometabolic risk factors, instead of treating diabetes or obesity alone, creates significant market potential for dual GLP-1/amylin therapy, which could be used to treat multiple aspects of metabolic syndrome at once and offer cardiovascular and renal protective benefits. The new joint consensus recommendations from the American Diabetes Association and the European Association for the Study of Diabetes assert that cardiovascular outcome benefits are primary considerations when selecting therapy, independent of glycemic control; this creates an environment in which superior metabolic interventions can get preferred formulary positioning, not just based on glucose-lowering, but on comprehensive risk reduction.

The large cardiovascular outcomes trials of GLP-1 receptor agonists (LEADER, SUSTAIN-6 and REWIND) have confirmed that this class of medication can lower major adverse cardiovascular events by 12-14% in high-risk individuals, and the link between percent weight loss and cardiovascular risk reduction has led to the expectation that higher percent weight loss will yield greater incremental cardiovascular benefits if this class of drug can be used in combination with amylin receptor agonists. The current REDEFINE-3 cardiovascular outcomes trial, which is evaluating CagriSema in 12,500 patients with obesity and established cardiovascular disease, is intended to assess the ability to achieve better cardiovascular event reduction than standard care with superior weight loss.

In addition to cardiovascular benefits, dual GLP-1/amylin therapy is now being studied in various obesity-related conditions like nonalcoholic steatohepatitis, obstructive sleep apnea, chronic kidney disease, and heart failure with preserved ejection fraction, suggesting that these drugs could be used as a cornerstone therapy for the management of comprehensive metabolic syndrome rather than for just one indication. This more global therapeutic perspective underpins higher prices and greater access to the market as payers begin to appreciate the economic benefits of early intervention with powerful metabolic drugs and avoiding downstream complications.

Technical difficulties in manufacturing two separate peptide drugs or engineered dual-agonist drugs of high purity, stability, and consistency needed for subcutaneous injection make the development and commercialization of dual GLP-1/amylin combination drugs a significant manufacturing challenge. The major manufacturing challenges associated with amylin analogs stem from the intrinsic tendency of the native amylin peptide to aggregate into amyloid fibrils in physiological conditions, which requires comprehensive chemical modifications to develop stable, soluble amylin analogs with favorable shelf life and patient tolerability to be manufactured commercially.

To get the two peptides to co-formulate in a single injection device with both equally optimum dosages while ensuring compatibility between them and stability during storage, advanced pharmaceutical development was required for co-formulation of cagrilintide with semaglutide in CagriSema. This complexity further prolongs the development process by 18–24 months versus single-agent programs and raises manufacturing expenses by an estimated 35-45% relative to manufacturing expenses of GLP-1 monotherapy, which can be a challenge in price-sensitive regions.

Peer industry manufacturing capacity is limited, despite shortages in 2022-2024, as USD 4.2 billion is being invested across the industry to expand capacity for peptide manufacturing between 2023-2026. Extensive customization for dual peptide products could also introduce new production constraints that will impact commercial availability in the early stages of product launch, especially where the product is expected to be launched concurrently with multiple competing products.

Dual GLP-1/amylin therapies will be priced at higher levels, likely at USD 18,000-25,000 per year, which is 40-60% higher than the market price of GLP-1 receptor agonist monotherapy. The high costs present significant reimbursement issues, especially when healthcare systems around the world are facing budget pressures due to increasing use of GLP-1 agonists worldwide, where global spending on this therapeutic area is projected to exceed USD 42 billion per year in 2025.

Payers are likely to have restrictive coverage criteria to restrict initial access to patients with highest clinical need, including BMI greater than 35 kg/m², multiple obesity-related comorbidities, and poor response to GLP-1 monotherapy. Limited coverage for obesity indications versus diabetes, step-therapy protocols requiring GLP-1 monotherapy trials, and prior authorization requirements could be a major limitation for market entry in early commercialization.

The global population of people with type 1 diabetes is estimated to be about 8.4 million and they have a complete loss of both insulin and amylin, which current insulin replacement therapy is unable to address, thus a significant market opportunity exists to expand the use of dual GLP-1/amylin treatment to type 1 diabetes. Type 1 diabetes patients do not have amylin treatment and, therefore, have unphysiological postprandial glucagon secretion, fast gastric emptying, and impaired satiety signaling, all of which are factors that can contribute to glycemic variability, postprandial hyperglycemia, and weight gain in intensive insulin therapy.

Early clinical trials on use of long-acting amylin analogs as adjuncts to optimized insulin therapy in type 1 diabetes have shown reduction in HbA1c levels of 0.4-0.7 percentage point and weight loss of 3-6 kg when added to optimized insulin therapy, and the convenience of once-weekly administration is especially significant compared to the 3 times/day injections of pramlintide, which limited the use of first generation amylin analogs. The type 1 diabetes market is seen as largely unexploited and the efficacy of pramlintide has been demonstrated, which has achieved 4-7% market penetration.

The cardiovascular outcomes data expected from dual GLP-1/amylin therapies offers a great opportunity for differentiation of the product in the market on a basis of greater cardiovascular risk reduction than the current GLP1 monotherapy standards. Because established relationships exist between degree of weight loss and cardiovascular event reduction, the greater weight loss with dual agonism raises intriguing hypotheses for greater cardiovascular protection, which could profoundly influence treatment guidelines and coverage policies.

The dual GLP-1/amylin therapy space is seeing a great deal of innovation to deliver the therapy orally, which may alleviate injection-related challenges that impact patient uptake and persistence. Technical challenges are still high with the efforts to achieve acceptable bioavailability of dual peptide combinations when administered orally, but if achieved, it could greatly increase the patient population that can be addressed by oral therapy, since the psychological barrier that exists with the use of injectable therapy are being responsible for eliminating a large number of patients who are eligible to use oral therapy.

The increasing knowledge regarding heterogeneity in metabolic phenotypes is leading to the establishment of precision medicine approaches to match individuals to appropriate therapeutic mechanisms, considering their own traits, such as appetite regulation behavior, postprandial glucose levels, and genetics associated with drug metabolism and effectiveness.

North America dominated the market with revenue of USD 1.2 billion in 2025, and is projected to grow at a CAGR of 19.8% through 2034, owing to the presence of a high number of obese and diabetic patients, along with well-developed insurance facilities that promote development of advanced metabolic treatments and regulatory frameworks that make it easier to obtain approval for hormonal combination therapies. The U.S., accounting for 84% of the total regional revenue, has FDA-approved precedents for such combinations that have proven superiority over monotherapy.

The fastest-growing regional market will be Europe, with expected CAGR of 22.1% up to 2034 due to healthcare technology assessments favoring treatments with improved cost-effectiveness, as well as a complete national health care system for implementing dual treatment modality. Europe’s long-term approach to preventing complications associated with type 2 diabetes is highly suitable for the use of dual GLP-1/amylin therapy.

Asia Pacific carries a disproportionate global diabetes burden, with the region accounting for a staggering 140 million people diagnosed with diabetes in China and 77 million in India, providing an immense target market for innovative diabetes treatments. This is due to the unique metabolic profile seen in the region, which develops diabetes even with lower BMI levels.

Product Type Insights: Fixed-dose combinations are most prevalent with 68% market share in terms of co-formulated formulations that consist of GLP-1 and amylin analogs in one injection device. Single dual-agonists occupy a share of 24%, which includes engineered peptides with receptor activity. Finally, coadministration has retained a market share of 8% for special indications and dose titration.

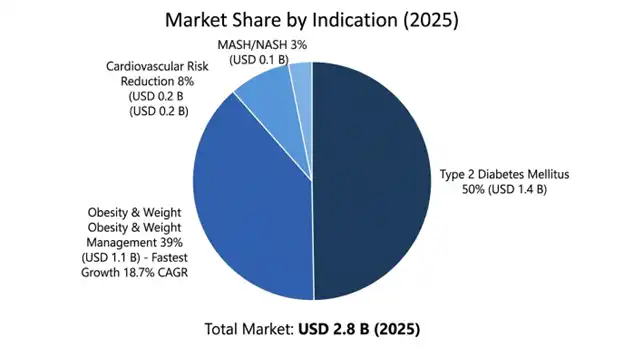

Indication Insights: The market segments are further bifurcated based on indication. Obesity and weight management is the leading segment, accounting for USD 1.1 billion in terms of revenue with 18.7% CAGR, based on effective weight loss results as key differentiators in the clinic. Type 2 diabetes holds a value of USD 1.4 billion with 16.2% CAGR.

GLP-1/Amylin dual-therapy is a moderately concentrated market worldwide due to CagriSema being the lead program of Novo Nordisk that enjoys the first-mover advantage. This segment is likely to see competition from Eli Lilly, AstraZeneca, and Zealand Pharma that have distinct methods such as dual-agonist monomers or non-amylin amylin analogues.

March 2026: REDEFINE-3 was enrolled by Novo Nordisk with 12,500 patients, initial findings anticipated in 2029.

February 2026: Zealand Pharma announced positive Phase II results for petrelintide alone that resulted in an 8.4% weight loss after 26 weeks of therapy.

January 2026: Novo Nordisk applied for CagriSema drug regulatory filings at FDA and EMA under priority review status.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.