Share this link via:

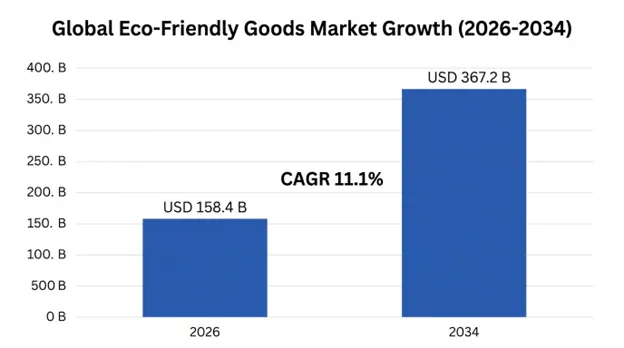

The global eco-friendly goods market size was valued at USD 142.8 billion in 2025 and is projected to reach USD 158.4 billion in 2026, expanding to USD 367.2 billion by 2034, growing at a CAGR of 11.1% during the forecast period (2026-2034).

Eco-friendly products form an innovative class of goods and services produced, processed, and marketed in a manner that causes minimal environmental impact during each phase of the product’s life cycle, beginning with raw material procurement and continuing until the end of the product lifecycle and eventual disposal or recycling. Such products incorporate sophisticated concepts of sustainability by adopting renewable, recycled, and biodegradable materials, avoiding the use of harmful chemicals, minimizing packaging waste, ensuring minimal environmental impact such as water or carbon footprint during production processes, and circularity principles such as design for longevity, reparability, and infinite recyclability.

The science behind eco-friendly product manufacturing is based on lifecycle assessments, which measure environmental impacts across multiple parameters such as global warming impacts measured through carbon dioxide equivalent emissions, water usage and contamination, impact on biodiversity, and material depletion. Superior eco-friendly products can deliver environmental improvements of 25–70% when compared to their non-green counterparts. The best eco-friendly products attain zero carbon footprint or achieve positive environmental results due to regeneration of materials used in production.

The market is driven by changing global consumption habits because of the rising awareness about climate change, stringent environmental policies around the world, and the rising prominence of sustainability as a crucial parameter in purchasing decisions among an increasing number of consumers. The commercial significance extends beyond product sales and encompasses the transformation of global supply chain systems, ESG performance metrics for companies, and branding systems based on sustainability.

Modern eco-friendly goods range from simple sustainable ones such as recycled paper and biodegradable cleaners to advanced products like bioplastics made of plants, waterless concentrates, refillable packaging, and regeneratively produced items that help restore ecosystems. The premium pricing of eco-products, which is mathematically shown as:

$$ ext {Green Premium} = frac{P_{ ext{eco}} - P_{ ext{conventional}}} {P_{ ext{conventional}}} imes 100%$$

where sustainable products command average premiums of 12-28% across major categories, is gradually narrowing as manufacturing scale increases and conventional product costs increasingly internalize environmental externalities through carbon pricing and regulatory compliance requirements.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 142.8 Billion |

| Forecast Value | USD 367.2 Billion |

| CAGR | 11.1% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

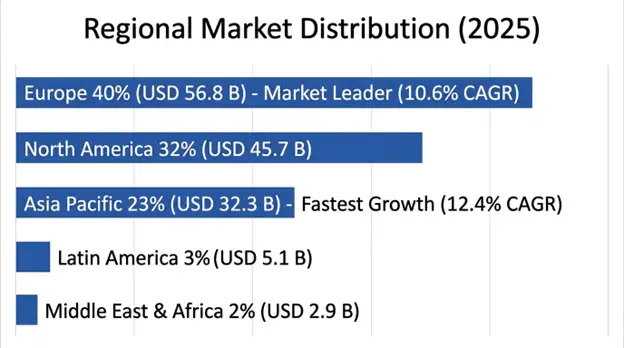

| Largest Market | Europe |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Material Type, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Unilever PLC, Procter & Gamble Co., Patagonia Inc., Seventh Generation Inc., The Honest Company, Natura & Co, Grove Collaborative, Method Products, Ecover, Dr. Bronner’s |

Get more details on this report - Request Free Sample

The key structural force driving the growth of the market for eco-friendly products is the radical shift in the value system of consumers regarding their environmental awareness, especially among young generations of Millennials and Gen Z that make up most of the most influential consumer segments globally. This generation shows unique consumer behavior as consumption becomes more of an expression of people’s value systems, with a particular emphasis on their environmental responsibilities. Research shows that 73% of global consumers are willing to change their consumption behavior to limit the environmental footprint, and 66% of consumers include sustainability in their purchasing decisions.

Value changes have resulted in real business benefits by enhancing the propensity to spend more on environmentally friendly goods, resulting in green premiums being accepted in up to 67% of the population in developed nations. Sustainable buying behavior is not only a result of environmental consciousness but also an expression of individual identity and social status, leading to brand loyalty that can withstand the challenges posed by economic turmoil and competition from regular products.

The phenomenon known as social amplification through digital media platforms leads to significant network effects where sustainable information is more likely than other content types to create buzz on social media and influencer marketing can impact hundreds of millions of consumers worldwide. Such social amplification has the power to make sustainability much more approachable for people who may not have sought it out otherwise.

The The global regulatory framework initially began as a voluntary initiative with sustainability initiatives and now encompasses stringent regulatory laws on issues such as plastic pollution, chemical safety, and corporate greenhouse gas emissions, thereby compelling companies to adopt eco-friendly products. The EU Green Deal Initiative has been among the most prominent regulatory changes that have brought about binding rules such as single-use plastics ban, mandatory recycling for packaging, sustainable textiles, and corporate sustainability reporting among others.

Producer Responsibility Schemes covering 67 countries around the world demand that companies pay to collect, sort, and recycle packaging materials and products after the products’ useful life has expired. This arrangement creates strong economic incentives to develop environmentally friendly products since EPR fees can be lowered with better product designs.

The regulation not only affects products directly but is also extended through sustainability reporting regulations where companies must demonstrate improvements in environmental performance, hence creating procurement regulations on eco-friendly products by corporations in supply chains dealing with companies committed to sustainability.

The primary factor limiting mass-market adoption with eco-friendly products is the continuing price gap between sustainably made products and traditionally manufactured items making such products unaffordable for many cost-conscious consumers who make up most of the buying population worldwide. The price premium for eco-friendly products ranges from 12–35% due to higher costs of raw materials and manufacturing, certification fees, and logistical challenges involved in keeping things sustainable.

These premiums create accessibility challenges in which the concept of sustainability remains an elitist option that only people who earn more money have the means to pay for. For the poorer people, sustainability is not an option regardless of their attitude towards environmental conservation. In times of economic instability and inflationary pressures, many sustainability-conscious consumers shift back to conventional products.

Though the price difference is steadily decreasing due to manufacturing efficiency and policy measures such as pricing of carbon to incorporate environmental costs of traditional products into their prices, full price convergence will take 8-15 more years.

A transformational opportunity in establishing business models within the circular economy which extend product value via repair, refurbishing, reselling, and renting, while minimizing environmental impact. In 2025, the total second-hand global market volume reached USD 197 billion and by 2030 it is expected to reach more than USD 350 billion, expanding three times faster than traditional retail owing to a greater consumer awareness of circular economic principles.

Models of Product-as-a-Service allow businesses to retain ownership yet make products accessible, thereby ensuring there are incentives to design for longevity and recyclability, thus aligning corporate goals with environmental considerations. The concept of regenerative products, which restore ecological balance through manufacturing processes, is what lies ahead of us in terms of development past sustainability into regenerative products.

Rapidly evolving trends are emerging toward zero-waste packaging and waterless product formulations that reduce or eliminate packaging requirements while cutting down on transport emissions and difficulties related to storage. This trend involves creating concentrated powder, solid bar and tablet formulations that eliminate up to 90% of the water content found in conventional liquid products.

Refill networks, standardized packaging-free containers, and refill services by subscription have been scaled up from pilots to being incorporated into regular retail operations, with significant investments in the logistics infrastructure by consumer goods manufacturers like Unilever, P&G, and Nestlé.

Digital technologies such as blockchain supply chain tracing and product passports are transitioning from their experimental usage to their full-scale adoption within leading product categories. Such digital platforms allow consumers to verify sustainability claims via supply chain traceability, combating the problem of greenwashing while allowing premium pricing for sustainable products.

QR code-enabled product information systems offer detailed environmental information such as calculations regarding the carbon footprint, sourcing materials, and instructions concerning proper disposal of the products after their use, which results in competitive advantages for firms with transparent processes.

Europe leads the market in terms of market share in 2025 with a value of USD 56.8 billion. It enjoys a projected CAGR of 10.6% between 2025-2034 owing to the presence of the most robust environmental regulatory policies, supported by high sustainability awareness among consumers across Northern and Western Europe. The Green Deal and Circular Economy action plan and sustainable products regulation of the European Union mandate market transformation.

Sustainability commitments related to product offerings and allocated retail spaces for sustainable products have been made by European retailers such as IKEA, H&M, and Carrefour. The presence of a developed recycling infrastructure, Extended Producer Responsibility, and carbon pricing policies in Europe leads to an economic environment that is more favorable toward sustainable products than conventional alternatives.

Asia Pacific is projected to be the fastest-growing region of 12.4% CAGR up to 2034, attaining USD 42.3 billion by 2025. China’s commitment to carbon neutrality represents the region’s largest growth opportunity due to annual growth rate of 28% for eco-friendly products in the Chinese domestic market during 2023-2025.

Japan’s advanced consumer culture supports the adoption of high-end environmentally friendly products, whereas South Korea’s increasingly stringent environmental policies and growing consumer consciousness promote rapid growth in green products. India possesses the greatest growth potential due to its governmental sustainability efforts and alignment of consumer values with environmental sustainability.

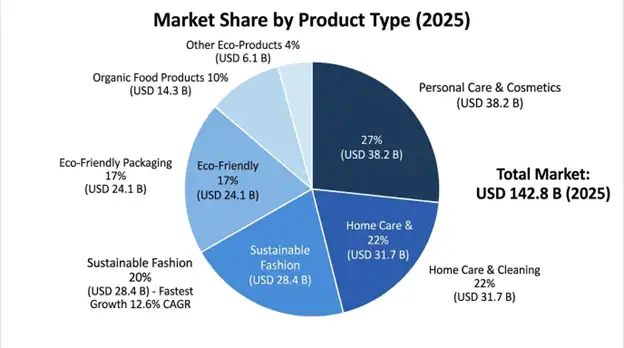

Product Type Insights: The Personal Care & Cosmetics segment is the largest with estimated revenues of USD 38.2 billion in 2025 growing at CAGR of 11.8% till 2034 due to increasing consumer preferences towards clean and non-toxic formulations as well as eco-friendly packaging options. Home Care & Cleaning Products are expected to have revenues of USD 31.7 billion with CAGR of 10.9%.

Sustainable Fashion & Apparel are valued at USD 28.4 billion at a CAGR of 12.6%, being the fastest-growing segment because of the evolution towards sustainable fashion practices and implementation of the circular economy concept. Eco-Friendly Packaging is worth USD 24.1 billion at a CAGR of 11.3%.

Material Type Insights: Recycled materials hold the highest market share of 36% worth USD 51.4 billion due to established recycling infrastructure and commercial adoption. Biodegradable & Compostable Materials have 28% share worth USD 40.0 billion with a CAGR of 13.2%, and this is the fastest-growing material type.

Organic & Natural Materials account for a 22% share, valued at USD 31.4 billion, comprising food and personal care segments. Bio-Based Plastics account for 9% market share with high CAGR of 15.1%. Upcycled Materials constitute a share of 5%, having the greatest potential for future growth.

Distribution Channel Insights: Supermarkets & Hypermarkets is the biggest distribution channel, with a market share of 44%, worth USD 62.8 billion, owing to integration into the retail mainstream of green goods and services from leading grocers. Online Retail/E-Commerce forms 29% of the market share worth USD 41.4 billion with a CAGR of 14.7%.

Specialty eco-stores capture a 15% market share among sustainability-focused consumers about sustainable products due to the special selection of products offered by these retailers. Direct-to-consumer channels constitute an 8% market share and have a 16.2% CAGR as this model allows sustainable brands to reduce retailer-related costs. Zero-Waste and refill stores make up 4% market share and have the highest CAGR at 18.9%.

The eco-friendly products market at an international level is moderately fragmented since traditional consumer goods companies compete against mission-driven sustainable brands. Multinational corporations such as Unilever, Procter & Gamble, and Nestle among others have been seen making efforts towards formulating their existing product brands and acquiring other sustainable brand firms.

Competitive distinction is based on factors such as third-party sustainability certification, product performance comparable to conventional alternatives compared to non-sustainable products, values-based branding which mirrors consumers' environmental beliefs, and an effective balance between capturing a premium price for sustainable products while remaining accessible to consumers. Businesses that demonstrate sustainability through their operations and reduced environmental impact can leverage considerable brand equity and customer loyalty premiums.

The innovation focuses on advanced material development, implementation of a circular economy business model, digital transparency and traceability solutions, as well as regenerative product innovation that can provide positive environmental impacts. The strategic collaborations between traditional consumer goods firms and the new generation of sustainable materials providers are fostering market growth due to their complementary strengths.

April 2026: Unilever PLC announced the completion of the transition to sustainable packaging across all European products, with the entire range of 400 brands now having recyclable/reusable packaging, thereby setting a new industry benchmark for large-scale sustainable packaging conversion.

March 2026: Procter & Gamble Company introduced its refill program across North America with 2,800 refill stations in cooperation with major retail partners, targeting a 40% reduction in packaging.

February 2026: Patagonia Inc. extended its Worn Wear circular economy platform into 28 new countries and expanded repair and resale capabilities that cater to 4.2 million people around the world, proving that circular business models can be commercially viable at scale.

January 2026: Grove Collaborative made its entire private label range plastic-free, making it the first big player in the household products category to achieve this feat and set a new industry benchmark in the process.

December 2025: The European Commission adopted its Sustainable Products Regulation implementation guidelines, which include mandatory ecodesign rules for 23 product categories and are estimated to create EUR 145 billion of substitution demand in the region by 2030.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

27 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.