Share this link via:

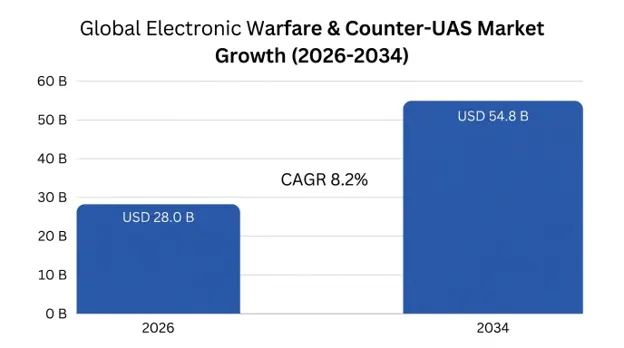

The global electronic warfare and counter-UAS market was valued at USD 25.6 billion in 2025 and is projected to reach USD 28.0 billion in 2026, expanding to USD 54.8 billion by 2034, growing at a CAGR of 8.2% during the forecast period (2026-2034).

Electronic warfare and counter unmanned aircraft systems are two major defense fields which have become vital in contemporary military operations and national homeland security. Electronic warfare entails control of the electromagnetic spectrum using three major aspects, namely Electronic Attack (EA) where jamming, spoofing and directed energy are used to attack the adversary’s systems, Electronic Protection (EP) which involves resilience of friendly forces against any adverse electromagnetic interference and Electronic Support (ES) whereby there are signals intelligence, threat detection and electromagnetic situational awareness.

Counter-UAS capabilities have become an urgent requirement due to the proliferation of low-cost drones., thus changing the asymmetrical nature of the enemy attacks. With such commercially available UAVs, which may cost as little as USD 1,000, it becomes possible to load them up with explosives, carry out reconnaissance missions or even swarm attacks that will cripple expensive air defense systems. Recent battles have shown that these low-cost drones can cause significant harm to expensive armored vehicles, command centers and critical infrastructure with favorable cost exchanges.

Modern joint EW and counter-UAS capabilities utilize highly advanced sensor fusion systems consisting of passive radio frequency sensing, active electronically scanned array radar technology, electro-optical/infrared sensors, and acoustic sensing, thereby producing a full air picture for identifying low, slow, and small air targets that are otherwise invisible to conventional air defense radars. The effector options include precise radio frequency jamming, GPS spoofing, and even laser-based weapons and high-power microwaves with unlimited magazine capacity and significantly lower cost per engagement than traditional kinetic systems.

The strategic importance of controlling the electromagnetic spectrum has elevated these technologies from auxiliary capabilities to fundamental warfighting necessities., with large military institutions aware that an opponent who is able to deny access to GPS guidance, interfere with communication systems, and blind sensors is able to render technologically advanced conventional forces useless. The awareness of such a problem has led to massive spending on procurement, the rapid development of cognitive electronic warfare systems utilizing artificial intelligence and increasing interest in EM spectrum management capabilities.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 25.6 Billion |

| Forecast Value | USD 54.8 Billion |

| CAGR | 8.2% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By EW Capability, Counter-UAS Technology, Platform, End-User, Technology |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Israel, Poland, China, Japan, India, Australia, South Korea, UAE, Saudi Arabia, Brazil |

| Key Market Playes | Lockheed Martin, Northrop Grumman, Raytheon Technologies, BAE Systems, L3Harris Technologies, Thales Group, Elbit Systems, Leonardo |

Get more details on this report - Request Free Sample

The strongest structural force driving market growth stems from the increased rivalry between great powers and the substantial investments made by China, Russia, and the United States to gain electromagnetic spectrum superiority, a critical factor for projecting military power in the contemporary era. In particular, the Chinese People's Liberation Army has used Military-Civil Fusion initiatives that merge the technical knowledge from civilian communications with military electronic warfare systems to develop anti-access/area-denial networks posing a threat to existing military technology dominance.

The use of advanced electronic warfare systems by Russia in Ukraine has provided a real-world demonstration of their effectiveness., as the latter has been using highly developed jamming systems, which reduce the accuracy of GPS guided weapons, interfere with various military communications on several frequency channels, and create complex electromagnetic situations. This trend has led to rapid development of procurement plans by NATO members, as the European defense communities increased their electronic warfare expenditures by an average of 34% between 2022-2025.

In 2025, the U.S. Department of Defense had spent four point eight billion U.S. dollars on its electronic warfare programs. This demonstrates the realization by the U.S. military that electronic warfare programs of the adversary present an existential threat to the principles of networked warfare on which American warfare strategies are based. Electromagnetic Spectrum Operations doctrine advocates that supremacy in the electromagnetic spectrum is critical for multi-domain operations.

The proliferation of armed unmanned aerial systems stands out as the key catalyst for the growth of the anti-UAS market, owing to the rapid conversion of commercial drones into their militarized versions across the globe. Modern battles have shown that inexpensive quadcopters could easily be turned into lethal weapons to carry explosives and help gather real-time battlefield intelligence, thus eliminating the conventional advantages of well-equipped, high-tech military forces.

The advent of loitering weapons and swarm attacks presents significant threats to existing air defense structures that have been designed to handle conventional fighter planes. Using surface-to-air missiles costing USD 100,000–500,000 per interception is too costly to use when dealing with cheap drones that cost only hundreds of dollars. The favorable cost exchange ratio encourages the adoption of counter-drone technology based on electronic warfare.

The major limitation that affects the deployment of electronic warfare and counter-UAS measures is the comprehensive set of regulations that control the usage of electromagnetic spectrum, especially within the civil environment where the jamming of signals might interfere with other legitimate signals used for communication purposes. The FCC and FAA regulations explicitly prohibit any person other than those employed by the federal government from conducting any activities related to radio frequency jamming and GPS signal spoofing due to serious collateral damage.

These regulations drastically hinder the ability of commercial anti-drone solutions providers from entering the market in anything beyond mere detection/tracking devices; active interdiction technology is simply too limited by the export and regulatory environment. Exporting electronic warfare capabilities is heavily regulated under ITAR and EAR, which have tight licensing rules that prevent the sale of many high-end technologies except through congressional approval via FMS channels to key allies within an 18–36-month timeframe.

Complex electronic warfare systems and UAS countermeasures have faced immense technical hurdles posed by the demands of Size, Weight, Power, and Cooling, combined with heavy development expenditure which constrains fast adoption and deployment. The incorporation of high-powered jamming equipment, directed-energy systems,, and advanced sensor fusion systems into existing military platforms involves major physical and electrical integration that goes beyond the capabilities of the platform itself, especially in case of airplanes and lightly armored vehicles.

Development of advanced cognitive electronic warfare capabilities is extremely capital-intensive, involving expenditures of several billion dollars to develop algorithms to differentiate between legitimate targets and unwanted clutter, as well as prevent fratricide incidents against friendly communications infrastructure. This has made their development extremely expensive, constraining countries from acquiring them in large numbers, and precluding non-military users from purchasing such defense systems.

A major market opportunity lies in directed-energy weapon technology, including the development of high-energy lasers and high-power microwaves in counter-unmanned aerial systems as well as general air defense operations. In contrast to conventional kinetic interceptor technology, directed energy weapon technology provides limitless ammunition based on the availability of power on board the launch platform, thus providing a paradigm shift in economics of air defense operations from favoring the attacker to favoring the defender. The cost of engagement for laser technology is less than USD10 per shot in electricity versus USD150,000 for standard SAM technology.

The advantages of the high-power microwave technology over drone swarms include generating an electromagnetic cone that can incapacitate numerous unshielded civilian electronics at once. Those companies who manage to scale down their directed energy weapons to fit on conventional military trucks will benefit from huge market share due to the unlimited ammunition capacity of directed energy systems.

The use of space for electronic warfare is one such development that offers benefits in terms of worldwide electromagnetic spectrum monitoring and electronic warfare signal gathering. Advances in commercial small satellites have made it possible to insert such capabilities quickly while keeping the cost of doing so extremely low by leveraging technology that involves payloads under 50 kg costing between USD 5-15 million.

Advancements in software-defined satellite payloads by the commercial space industry ensure quick adaptability in response to emerging threats in electronic warfare along with continuous global coverage that is not possible using any terrestrial system. Space-based systems hold several benefits in the detection of electronic warfare activities by an adversary, warning against their activation, and communication relay support for networked electronic warfare.

Developments in gallium nitride semiconductors and efficient batteries are allowing significant miniaturization of EW/counter-UAS systems, making their use possible at tactical levels North America holds a dominant market position, accounting for USD 11.5 billion in 2025.. Gallium nitride-based amplifiers can function at higher temperatures and voltage levels, making it possible for smaller and lighter systems to be developed, which can then be employed in portable systems.

Miniaturization will allow EW payloads to be deployed on miniature tactical drones and create distributed electronic attack capabilities that are highly mobile and deployable into contested areas without any danger to crewed vehicles. Portable counter-drone systems in handheld form factors can conduct directional radio frequency jamming for infantry soldiers, whereas mounted versions can provide protection for armored units from drone attacks.

Software-defined radio technology has become an essential component of electronic warfare technology because it can reprogram itself to respond to threats using software updates. Electronic warfare systems make use of wideband antennas and the fast conversion of signals from analog to digital before applying sophisticated algorithms to the signal.

The concept of cognitive EW is based on software-defined technology but integrates machine learning algorithms to provide autonomous analysis of threats and develop countermeasures without any human intervention. Such a system maintains its own library of threats using experience gained during actual operations and lessens the cognitive workload of the operator.

North America holds a dominant position in terms of market leadership, having USD 11.5 billion in 2025, accounting for 45% of total market share owing to the procurement policies of the US Department of Defense. The procurement policies of the United States Department of Defense reflect the necessities and requirements of strategic competition and modernization initiatives. Procurement projects such as Next Generation Jammer, Surface Electronic Warfare Improvement Program, and Terrestrial Layer System constitute multibillion dollar investments.

The regional market benefits from exceptional R&D capabilities, which is well represented at defense contractor facilities, national labs, and universities that benefit from significant funding by the government. The next generation of cognitive electronic warfare programs at the Defense Advanced Research Projects Agency and electromagnetic spectrum initiatives at the Air Force Research Laboratory will define future trends in the market up to 2034. The counter-UAS market development is especially strong through the Army Indirect Fire Protection Capability and Department of Homeland Security initiatives.

Europe is expected to register the highest CAGR of 11.2% through 2034., The region accounted for USD 6.8 billion in 2025, driven by a renewed assessment of defense requirements. after Russia invaded Ukraine and proved that Europe’s current electronic warfare technology is ill-equipped to deal with modern-day adversaries. Defense spending for NATO countries has been increasing comprehensively, with electronic warfare and counter-UAS capabilities being one of the main focuses.

Consolidation of Europe’s defense sector is leading to the emergence of more formidable national competition through such firms as Thales, Leonardo, Airbus Defense and Space, and HENSOLDT, forming a competitive industrial base that diminishes European reliance on US technology regarding their electronic warfare technology. The European Defense Fund supports cross-border consortia that create sovereign electronic warfare technology capability, whereas regulations require installation of drone detection technology in key infrastructures.

The Asia-Pacific market will contribute USD 5.4 billion by 2025 due to the presence of various geopolitical complexities, disputes, and security at borders resulting in the requirement for continuous electronic warfare capabilities. The modernization of China’s People’s Liberation Army, especially the anti-access/area-denial network, has led to investments by other countries in the region such as Japan, South Korea, India, and Australia to keep pace technologically.

Naval electronic warfare provides a promising area of growth as countries purchase electronic support systems and decoys for shielding their surface fleet against modern anti-ship cruise missiles. The needs of India to monitor its lengthy borders make integrated sensors for countering unmanned aerial vehicles critical to prevent them from crossing the borders for intelligence gathering and smuggling.

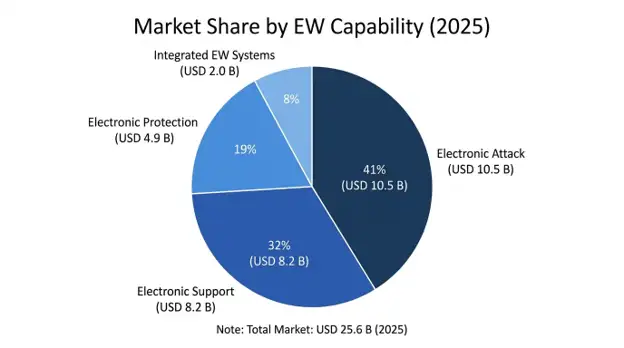

Electronic Attack leads the capability segments with a market share of 41%, worth USD 10.5 billion in 2025, which includes active jammers, anti-radiation missiles, directed energy weapons, and deception systems intended to deny, disrupt, or destroy an adversary's electromagnetic systems. The capabilities in this segment will gain significant traction from the high levels of funding due to great power competition needs and counter UAS applications.

The market share of Electronic Support is estimated at 32%, amounting to USD 8.2 billion. It consists of electronic support measures such as signals intelligence collection, electronic surveillance, threat warning, and electronic order of battle that form the basis of intelligence required for electronic attacks and protection. The market share of Electronic Protection is estimated at 19% through electronic warfare measures used to protect friendly assets against adversary electronic attack.

Counter-UAS technology is predominantly made up of RF Detection & Jamming Systems, which make up 37% of market share worth USD 9.5 billion in 2025, offering effective solutions by disrupting control link signals and GPS navigation of commercial drones. Multi-Sensor Fusion Network holds 28% market share responsible for creating a complete air picture using radars, electro-optical sensors, and acoustic sensors.

Directed Energy Weapons hold the largest growth potential due to 16% market share and 15.4% CAGR because of the benefits offered by their infinite magazine depth and maturity of the technology. The kinetic intercept systems have a market share of 19% owing to their use of interceptor technology against threats to electromagnetic systems.

The airborne platforms capture a major 41% market share worth USD 10.5 billion based on electromagnetic spectrum management from electronic warfare aircraft, electronic warfare pods, and electronic warfare payloads for unmanned aerial vehicles. The land-based platforms have 35% of the market share based on electronic warfare equipment mounted on vehicles and fixed installations for tactical force protection and base defense.

The naval platforms capture a 16% market share through self-protection suites for ships and electromagnetic spectrum management for naval fleets. The space-based platforms have an 8% market share through electromagnetic spectrum monitoring and signal intelligence satellites.

The global market for electronic warfare and counter-UAS is highly concentrated among defense contractors in terms of their presence and dominance, where the eight leading companies account for about 68% of the market in terms of total value through system development, access to classified programs, and domain expertise in integration. Market competition is based on proven performance in contested electromagnetic environment, software-defined design offering flexibility to update capabilities, and expertise in integration of electronic warfare systems into battle management systems.

Prime large contractors continue to enjoy a competitive edge because of vertical integration, classified technology capabilities, and pre-existing relations with the government, whereas the counter UAS niche has more fragmentation among dynamic defense technology firms using innovation cycles and capabilities as their point of competition. There is also an increased level of strategic acquisitions as prime contractors acquire specialty firms dealing with electronic warfare and counter UAS technology.

April 2026: The USD 1.8 billion modification contract was awarded to Northrop Grumman for Next Generation Jammer Mid-Band program to develop cognitive electronic warfare technologies that can provide self-adjustment to threats in extended frequencies to counter emerging threats of the enemy's radar systems.

March 2026: The L3Harris Technologies company successfully underwent an operational assessment on its integrated counter UAS system that was able to defend against swarming assaults utilizing radio frequency jamming and high-power microwaves, securing an initial production contract worth USD 340 million.

February 2026: A program between BAE Systems and Thales Group to develop European electronic warfare systems utilizing AI-driven spectrum management has been unveiled. for current and next-generation fighter jets’ needs.

January 2026: Elbit Systems launched a modular counter-UAV system utilizing passive RF sensing, multi-spectrum tracking, and jamming capabilities, weighing less than 80 kilograms..

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.