Share this link via:

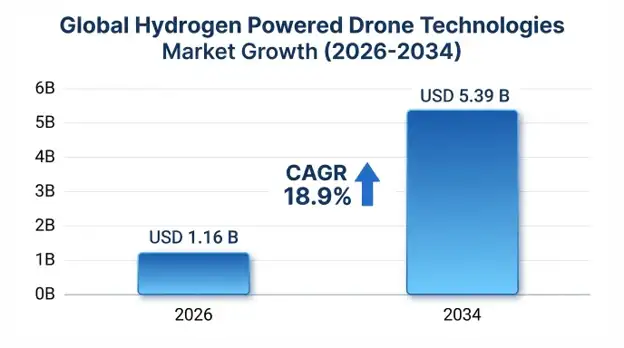

The global hydrogen powered drone technologies market was valued at USD 950 million in 2025 and is projected to reach USD 1.16 billion in 2026, expanding to USD 5.39 billion by 2034, growing at a CAGR of 18.9% during the forecast period (2026–2034).

Hydrogen powered drone technologies are an innovative leap in the field of unmanned aerial systems, using cutting-edge fuel cell technology to overcome the inherent energy density limitations of battery-electric technologies. These complex systems combine proton exchange membrane fuel cells with hydrogen storage systems using high pressure carbon composite tanks that have a gravimetric energy density of 600-1200 Wh/kg compared to 150-250 Wh/kg for advanced lithium-ion battery packs. This compelling energy density benefit directly drives improved flight endurance by 300–800%, opening new operational possibilities that significantly increase the commercial potential of unmanned aircraft in various industry verticals.

The core technology is based on the electrochemical conversion of compressed hydrogen gas into electrical energy using fuel cell stacks, generating only water vapor and minimal heat as by-products, while providing flight endurance of 2–12 hours, depending on platform configuration and mission profile. This on-site zero-emission operation with a quick refueling time of 5-15 minutes versus multi-hour battery charging positions hydrogen propulsion as the catalyst for Beyond Visual Line of Sight (BVLOS) operations, persistent surveillance missions, long-range logistics delivery, and extended-duration industrial inspection applications that are categorically impossible with battery-electric systems.

The market includes a variety of platform configurations that have 2-4 hours of endurance for precision agriculture and building inspection, and 8-15 hours continuous flight time for border security and maritime patrol missions. Fuel cells can be combined with buffer battery systems to achieve optimal power delivery characteristics and still benefit from the endurance properties of hydrogen propulsion, allowing dynamic flight profiles with high power availability during takeoff, aggressive maneuvers, and emergency response operations.

The commercial potential extends beyond the traditional UAS market but also includes hydrogen propulsion through new business models that include the ideas of persistent aerial services, automated logistics networks and complete area monitoring that results in sustainable business opportunities not possible due to battery limitations. The combination of maturing fuel cell technology, decreasing the cost of green hydrogen production, increasing regulatory authorizations for commercial BVLOS flight, and an increasing demand for ZE aviation solutions leads to a compounding growth dynamic for hydrogen drone platforms as the most prevalent architecture for professional long endurance UAV applications throughout the forecast period.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 950 Million |

| Forecast Value | USD 5.39 Billion |

| CAGR | 18.9% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Drone Type, Power System, Payload Capacity, Application, End-User, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Doosan Mobility Innovation, Intelligent Energy, HES Energy Systems, Ballard Power Systems, H3 Dynamics, Hylium Industries, Boeing Aurora Flight Sciences, ZeroAvia, Plug Power, Honeywell Aerospace |

Get more details on this report - Request Free Sample

The primary growth driver is the significant performance advantage that hydrogen fuel cell systems offer with respect to lithium-ion battery systems in terms of energy density, there is a significant performance gap that makes the difference in certain uses where flight duration is not a luxury but a necessity. When converting to practical system level, after accounting for the weight of the fuel cell stack, pressure vessel, and balance-of-plant components, hydrogen still offers a 4-12-fold increase in endurance when compared with battery electric systems of similar total system mass.

The endurance advantage translates into measurable operational cost savings in various commercial applications. Linear inspection operations (LIN), such as pipeline corridors, power transmission lines and railway networks, hundreds of kilometres long, demand either multiple battery drone deployments with frequent landings and battery swaps or hydrogen platforms to fly over the entire corridor segment without a single landing. Economic modeling of major utility operators shows that hydrogen drones can lower inspection costs by 35-52% when compared to battery drone fleets that complete the same coverage, due to fewer opportunities for mobilization, less labor needed for inspections, and robust data continuity without the need for battery swaps.

Endurance requirements are especially relevant to defense and security requirements, for example, the persistent surveillance missions over border regions, maritime exclusive economic zones, and tactical area monitoring that requires the operator to be on-station for hours instead of minutes. The 4–8-hour requirement for endurance at operationally relevant payloads is a military specification increasingly being imposed on small UAS that categorically rules out battery electric options and makes hydrogen fuel cell systems the technology driver for next generation tactical UAS systems.

A key barrier to commercial drone adoption, namely the regulatory limitation on their operations, is being systematically phased out in the largest aviation markets, allowing hydrogen drone operations to generate commercial value. The BVLOS Aviation Rulemaking Committee suggested recommendations that have been adopted in progressive regulatory steps such as Part 107 waivers and type certification pathways, allowing for commercial BVLOS operations along new corridors and throughout BVLOS regions for infrastructure inspection, precision agriculture, and logistics delivery applications.

The economic benefit of the BVLOS regulatory unlocking is directly proportional to the capability of the drone in terms of endurance, as the wider the geographic area flown in a single sortie, the more money can be generated while reducing the operational costs as a function of area flown per unit. Hydrogen drone operators in markets where BVLOS permissions have already been approved generate some 4.5-7.2 times higher revenue per platform than comparable battery drone operations that are restricted to VLOS operations, justifying the cost of the hydrogen system, which is typically 2.5-4.2 times the cost of a battery drone system.

The adoption of U-Space across EU member states by the European Union Aviation Safety Agency (EASA) has set the airspace management protocols standard, while similar efforts in Australia, Canada and advanced Asian markets have laid the groundwork for a level of operational permission that will allow hydrogen drone commercialization to operate meaningfully at scale.

The primary technical barrier is the safety certification of onboard high-pressure hydrogen storage systems., which is very expensive, time-consuming, and restrictive, and is difficult to clear the way for the deployment of hydrogen drones in a wide range of commercial and regulatory contexts. Compressed hydrogen storage at 350-700 bar requires composite pressure vessels that are certified to meet very high structural integrity requirements within aviation regulatory certification programs, such as hydrostatic burst testing, drop impact assessment, fire exposure evaluation, long-term fatigue cycling, etc., and which can take up to USD 3-12 million and 24-42 months to fully test a vessel design.

Unlike battery electric systems, handling high-pressure hydrogen needs specific knowledge for maintenance workers, special storage facilities with safety distances and monitoring, and complex emergency response protocols, which make the use of hydrogen-based power generation more complex than battery electric systems when it comes to operation. These needs pose workforce development issues and facility infrastructure costs that limit the rate of commercialization, especially for smaller operations that do not have specific technical resources.

Aviation authorities across various markets have different certification requirements and operating rules for hydrogen pressure vessels, making the regulatory landscape even more complex, as manufacturers have to apply for parallel certification in key markets such as the FAA, EASA, CAAC and national aviation authorities in Asia-Pacific markets.

Defense modernization programs in NATO countries, Indo-Pacific allies, and military powers are leading to significant spending on endurance unmanned aerial systems for ISR, border security, maritime awareness, and force protection applications, in which hydrogen power endurance is key in addressing existing operational gaps in capability. The current requirements by the military are for a minimum of 6-12 hours endurance of unmanned aircraft systems, and hydrogen fuel cell power is the only available solution for that challenge.

Persistent tactical ISR capabilities have been identified as a high priority requirement by the US Department of Defense unmanned system roadmap, where the hydrogen fuel cell S-UAS is an enabling technology that will help to achieve such capabilities at the company and battalion level of persistent surveillance missions. Such needs within allied forces provide a large addressable market for hydrogen drones.

Stable defense budgets support hydrogen drone procurement and continued technology development. that defense budgets are insulated from commercial prices and therefore allow the procurement process to occur at affordable price levels that can be sustainable in terms of profit and funding further research for development of hydrogen drones to suit harsher environments. A closely related area would be the use of hydrogen drones in counter-drone operations.

An important technological trend reshaping the hydrogen drone industry is the steady shift from the compressed gas form of hydrogen storage to the more efficient storage form of cryogenic liquid hydrogen, in addition to hybrid fuel cell and battery technology to achieve optimal power supply characteristics. The storage of liquid hydrogen at temperatures below -253° C provides energy density of 2.37 kWh/L compared to 1.33 kWh/L in 700 bar gas tanks.

Hybrid architecture of current generation systems employs buffer systems using high discharge lithium-ion or supercapacitors to manage peak power demands during takeoffs, aggressive maneuvers, and emergency situations, whereas fuel cells supply continuous baseline power while charging the buffer batteries during flight. This arrangement facilitates the size reduction of fuel cells for achieving efficient cruise performance, yet delivering peak power for dynamic flight conditions, leading to 15 to 22% reduction in total system weight relative to all fuel cell-powered systems.

Development of advanced cryogenic management systems including vacuum insulated cryogenic tanks, cryogenic pumps, and intelligent boil off management techniques is increasingly rendering liquid hydrogen suitable for unmanned aircraft systems across medium and large aircraft segments. Persistent observation and logistical operations by the military and civilian customers necessitate research and development efforts in liquid hydrogen powered platforms for 12 to 24 hours of endurance capability.

North America had the largest market share of USD 380 million in 2025 and continues to retain its projected CAGR of 18.2% until 2034. Market dominance is driven by large-scale investments in high-endurance unmanned aircraft systems. with high endurance capabilities, an evolved regulatory environment through approval of BVLOS by FAA, significant venture capital investment in hydrogen aviation ventures, and development of hydrogen infrastructure.

The United States constitutes 89% of the regional market value thanks to Department of Defense hydrogen drone research efforts covering persistent tactical ISR, maritime patrol, and logistics missions for the Army, Navy, Air Force, and Special Operations Command. The commercial industry growth relies on infrastructure inspection services operating vast pipelines totaling 3.8 million km, high-voltage transmission lines stretching up to 850,000 km, and telecommunications systems requiring periodic evaluation in multiple locations spread out geographically.

Regulatory factors contribute to innovation within FAA initiatives such as BEYOND project, Integration Pilot Program results, and development of Unmanned Aircraft Systems Traffic Management system which altogether reduce time-to-market while ensuring safety of operations. The healthcare industry represents an emerging application area in medical deliveries, using hydrogen drones for delivering supplies to remote hospitals and transportation of emergency medical care in geographically distributed areas.

The fastest-growing region was Asia Pacific, expected to witness a CAGR of 21.4% over the forecast period till 2034 with an estimated value of USD 285 million in 2025. Regional growth is driven by China’s leadership in drone production globally, Japan’s established hydrogen-based economy, South Korea’s experience in the manufacture of fuel cells, which enables the development of cost-effective systems, and vast agricultural regions in Southeast Asia and Australia.

China has the highest growth in the region, having 48% market share due to the presence of local drone suppliers such as DJI, EHang, as well as suppliers of hydrogen platforms. Support by the government through its industrial policy that favors development of hydrogen technologies in various transport sectors includes funding for research and production of fuel cell drones.

Japan offers unique advantages for the commercial deployment of hydrogen drones through extensive hydrogen retail infrastructure including more than 180 hydrogen filling stations and supply chain developed for automobiles using fuel cell technologies and increasingly extended to aviation. Hydrogen drone tests have been extensively carried out by Japanese utility companies for transmission line inspections.

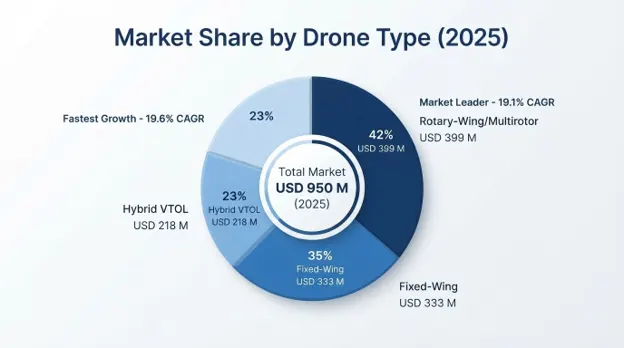

Rotary-Wing/Multirotor Drones form the leading segment by platform with a 42% share accounting for USD 399 million in 2025 and a 19.1% CAGR from 2026 to 2034. Rotary-wing/multirotor drones dominate the market due to the important take-off and landing ability that is necessary in many industrial applications, logistics in urban areas, and agriculture when runways are not available. Hydrogen fuel cells address the key limitation of battery-powered multirotor drones-limited flight endurance. for battery powered multirotor drones with flight times increasing from 25-40 min to 2-4 hrs.

The Fixed-Wing Drones will hold a 35% market share in 2025 and have a value of USD 333 million and 18.8% CAGR. Fixed-wing drones are preferred for applications requiring maximum endurance and range capabilities rather than vertical takeoff capabilities. The aerodynamic design enables continuous flight for 8–15 hours using hydrogen power.

The Hybrid VTOL Platforms will be valued at USD 218 million and will hold a market share of 23% in 2025 and have a CAGR of 19.6%. They are used in applications which need to perform operations with flexibility without compromising on endurance capabilities. These drones are being increasingly adopted in commercial, logistical, military, and other emergency operations.

The largest market segment in terms of revenue, Proton Exchange Membrane Fuel Cells hold a 71% market share, worth USD 675 million in 2025 and having a CAGR of 19.2% over the period until 2034. PEM fuel cells have an optimum blend of fast start-up, high power density, low operating temperatures, and load following that is required for drone applications requiring variable levels of power generation. PEM technology has benefited from significant fuel cell developments in the automotive sector, reaching stack power densities of 4.2 kW/kg and thereby allowing lightweight fuel cell systems for different platform architectures.

Hybrid Hydrogen-battery Systems hold a market share of 21%, worth USD 200 million in 2025 and having a CAGR of 18.4% during the forecast period until 2034. These systems combine fuel cell efficiency during cruising conditions with the peak power capacity of batteries to ensure best flight performance in all dynamic operating scenarios.

Defense and Military is the biggest application segment with 36% market share worth USD 342 million in 2025 and is projected to grow at a 18.6% CAGR through 2034. Military organizations leverage hydrogen-powered drones for such as ISR (intelligence, surveillance, and reconnaissance), border surveillance, maritime domain awareness, and communication relay missions wherein the on-station presence is directly proportionate to mission effectiveness and protection of forces.

The Infrastructure Inspection segment holds 26% market share valued at USD 247 million in 2025 and 19.8% CAGR, providing comprehensive structural inspections for the pipeline industry, electrical utilities, telecommunications firms, and transportation infrastructures with widespread geographic presence. The economic case for hydrogen in this segment is clear from the cost savings that have been realized compared to other methods of inspection.

Commercial Logistics and Delivery is the 19% market segment, valued at USD 181 million in 2025 and 21.2% CAGR, which is the fastest-growing commercial application segment owing to e-commerce growth, middle-mile economics, and evolving regulatory environment.

The Military & Defense segment is the most significant end-user segment constituting a 36% market share worth USD 342 million in 2025 due to consistent surveillance needs, modernization of ISR programs, and force protection applications, wherein hydrogen endurance helps in addressing the capability gap that exists in existing unmanned system portfolios.

Energy & Utilities constitutes 28% market share worth USD 266 million in 2025 with a 19.4% CAGR including pipeline companies, electricity transmission corporations, renewable energy companies, and oil & gas exploration companies where hydrogen endurance helps in covering dispersed infrastructure assets.

Logistics & E-Commerce Corporations make up 18% market share worth USD 171 million in 2025 with a 21.8% CAGR as the fastest-growing end-user segment, which includes regional delivery networks, last-mile automation services, and medical supply chain applications.

The hydrogen-powered drone technologies industry features a unique pattern of competition, where partnerships are formed between traditional fuel cells producers and manufacturers of drones, with no single company holding more than a 14% market share.. There is a wide range of competitors including traditional hydrogen drone producers who manufacture their own drones, traditional aerospace and defense companies who implement hydrogen propulsion into their drones, and companies that supply components of propulsion systems for various drone manufacturers.

Competitive differentiation is based on flight endurance performance backed by third-party testing, certification for wide application in targeted markets, maturity of hydrogen storage systems and their safety certification, and software solutions for operational applications of drones in both business and military spheres. Collaborations among experts in fuel cells and airframes have become more frequent lately as hydrogen drones cannot be designed without knowledge of fuel cell technology, aerospace engineering, and software systems.

April 2026: Fourth-generation hydrogen fuel cell power pack from Doosan Mobility Innovation became available on the commercial market with 5.2 kW of continuous output at 1.3 kg of system weight allowing for 6 hours of flight time for 12 kg payload multirotor airframes; the product is being delivered to infrastructure inspection service providers in South Korea, Japan, Australia, and North America.

March 2026: Intelligent Energy has been granted EASA type certification for its hydrogen fuel cell propulsion system – making the company’s hydrogen drone power system the first one in Europe to be completely certified by the regulatory authority.

February 2026: Boeing Aurora Flight Sciences conducted a 12-hour endurance test flight of its hydrogen-powered fixed-wing ISR air vehicle during the evaluation phase conducted by the US Army, securing an operational range of 850 km along with full sensor payloads for EMD contract win.

January 2026: Ballard Power Systems has signed partnership agreements with four drone manufacturers from Europe for the supply of next-generation FCair fuel cell modules designed specifically for unmanned aviation platforms, whereby total supply agreements for 3,200 units up to 2029 equate to USD 128 million in contracted revenue.

December 2025: H3 Dynamics has conducted a successful demonstration of its liquid hydrogen storage system for its 18-hour endurance flight featuring 8 kg payload capacity and setting the world endurance record for rotary-winged unmanned aerial vehicles.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

08 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.