Share this link via:

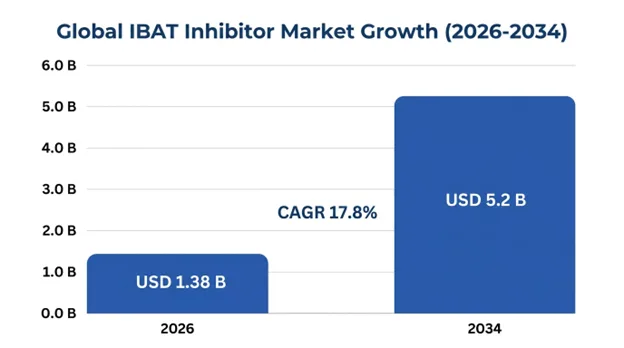

The global ileal bile acid transporter (IBAT) inhibitor market size was valued at USD 1.08 billion in 2025 and is projected to reach USD 1.38 billion in 2026, expanding to USD 5.2 billion by 2034, growing at a CAGR of 17.8% during the forecast period (2026–2034).

Inhibitors of ileal bile acid transporters (IBATs) or apical sodium-dependent bile acid transporter (ASBT) inhibitors constitute a novel class of oral medications that specifically impairs the reabsorption of bile acids from the terminal ileum to disrupt their enterohepatic cycle. The pharmacological approach not only addresses the pathophysiology but also treats cholestatic liver diseases by enhancing bile acid excretion, decreasing systemic and hepatic bile acid levels, and thus minimizing hepatocyte damage and alleviating symptoms like pruritus caused by cholestasis.

The IBAT protein, which consists of SLC10A2-encoded receptors, actively transports around 95% of bile acids from the terminal ileum back into the portal bloodstream. Cholestatic liver diseases are characterized by the accumulation of cytotoxic bile acids in the hepatocytes and cholangiocytes due to their inability to secrete the same, causing oxidative stress and mitochondrial damage, leading to chronic inflammation, fibrosis, and eventual cirrhosis.

First-wave IBAT inhibitors such as odevixibat and maralixibat have already proven their clinical and commercial viability through their ability to provide significant decreases in serum bile acid levels, clinically relevant relief from cholestatic pruritus, and positive impacts on growth metrics and liver biochemistry in children suffering from progressive familial intrahepatic cholestasis and Alagille syndrome. This has firmly established that the IBAT inhibition approach is a viable disease-modifying therapy for rare pediatric cholestatic diseases with high unmet medical need, scarce treatment histories, and high likelihood of requiring liver transplantation during childhood or adolescence.

The therapeutic and commercial applicability of IBAT inhibitors expands far beyond the initial ultra-rare conditions into larger cholestatic patient populations including primary biliary cholangitis, primary sclerosing cholangitis, biliary atresia, intrahepatic cholestasis of pregnancy, and specific metabolic liver disease presentations. The market is characterized by premium orphan drug pricing, extensive patient identification initiatives, and physician specialization within hepatology centers with the global treatable patient population for current indications numbering in the tens of thousands while offering lifetime per-patient revenue opportunities worth hundreds of thousands of dollars.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 1.08 Billion |

| Forecast Value | USD 5.2 Billion |

| CAGR | 17.8% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By Drug Type, Indication, Patient Type, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, Saudi Arabia, UAE, South Africa |

| Key Market Playes | Mirum Pharmaceuticals, Ipsen (Albireo Pharma), GlaxoSmithKline, EA Pharma, Intercept Pharmaceuticals |

Get more details on this report - Request Free Sample

The primary catalyst driving growth of the IBAT Inhibitors Market is the approval of groundbreaking medicines in terms of regulatory approval and commercialization which have validated their clinical concept and mechanism of action, and established specialized commercial infrastructure to cater to the rare cholestatic conditions. For example, odevixibat, initially manufactured by Albireo Pharma but now taken up by Ipsen, was FDA-approved in July 2021 to treat pruritus in children and adults aged six months and above suffering from progressive familial intrahepatic cholestasis, later followed by EMA approval and labeling for Alagille syndrome. Similarly, another agent, maralixibat, manufactured by Mirum Pharmaceuticals, was approved by the FDA in September 2021 to treat cholestatic pruritus in children aged one year and above suffering from Alagille syndrome.

Approval of these regulatory milestones marks a turning point for patients that have relied on symptom management via low effectiveness therapeutic drugs such as cholestyramine, rifampicin, and naltrexone, or needed more invasive surgeries like partial external biliary diversion and liver transplantation. Statistical proof of significant efficacy of clinical trials, involving lowering of serum bile acid levels, use of validated pruritus scoring tools, indicating 40–60% responses compared to 10–20% for placebo, leading to improvement in sleep and quality of life negatively affected by severe itching.

Seven years of market exclusivity in the US and ten years in the EU market granted with the orphan drug designation supported premium pricing models ranging from USD 250,000 to 400,000 per year in patients. The disease burden of progressive familial intrahepatic cholestasis has an incidence of one per 50,000–100,000 live births globally, with around 15,000 to 20,000 patients. While for Alagille syndrome, the incidence is one per 30,000 live births, with about 25,000 to 35,000 patients globally.

The most commercially promising growth driver would be the clinical pipeline of research on IBAT inhibition among large patient populations encompassing conditions such as primary biliary cholangitis, primary sclerosing cholangitis, and other adult cholestasis disorders. Primary biliary cholangitis is an orphan indication that affects about 130,000 Americans and nearly 400,000 individuals worldwide. About 40% of patients respond poorly to the primary therapy of ursodeoxycholic acid, and 70- 80% suffer from pruritus associated with cholestatic disorders without any pharmacological interventions.

Linerixibat developed by GlaxoSmithKline has advanced to Phase III clinical trials for primary biliary cholangitis-related pruritus via the GLISTEN program, with over 200 patients enrolled and likely to serve as a pivotal dataset for potential registration purposes for a much larger commercially viable indication than those currently available. The underlying basis for the use of IBAT inhibition in primary biliary cholangitis-induced pruritus is very strong as the high concentration of bile acids within the systemic circulation as well as in the skin is the cause of intense itchiness.

Volixibat developed by Mirum Pharmaceuticals is undergoing clinical investigation in relation to primary sclerosing cholangitis and further indications of primary biliary cholangitis by way of the VISTAS and VANTAGE clinical studies. These programs aim at reducing pruritus and altering liver biochemistry and fibrosis progression. Success in these clinical studies will transform the use of IBAT inhibitors into mainstream treatments used in hepatology, rather than orphan treatments in the field of pediatrics.

An important future growth factor will be the incorporation of genetic profiling and therapy approaches that use biomarkers for better patient selection and higher efficacy, resulting in premium prices because of the high clinical value in genetically selected patient groups. For instance, by determining whether specific genetic mutations such as JAG1 or NOTCH2 cause Alagille syndrome or ATP8B1, ABCB11, or ABCB4 cause different types of progressive familial intrahepatic cholestasis, it becomes possible to predict which patients will respond favorably to IBAT inhibition therapy.

Response to IBAT inhibitors occurs in patients with a functioning bile acid transport system but dysfunctional secretion, whereas patients lacking all proteins are likely to have reduced efficacy of therapy, hence the ability to choose the right treatment and avoid wasting money on the wrong medication. Besides improving patient outcomes, the precision-medicine strategy is important in improving the business case for reimbursement due to effectiveness in targeting the right patients.

The increased scope of newborn screening tests to include genetic testing for liver diseases that cause cholestasis, coupled with decreasing cost for next-generation sequencing, results in the early detection of affected individuals, thereby enabling early therapeutic intervention, such as inhibition of IBAT, which can be most effective at certain stages of development.

One of the primary restraints limiting growth of the global IBAT inhibitor market is the extremely high cost of treatment with the therapy being priced at more than USD 350,000-400,000 annually per patient in the developed markets and thus creating significant barriers to treatment access in the underdeveloped countries as well as leading to rigorous evaluation from the HTA bodies even in the well-resourced healthcare systems.

Although the high prices for treatment are justified considering the rarity of the disease, huge costs involved in the development of therapies, as well as highly beneficial effects of treatment on clinical outcomes, which include avoiding organ transplant, such costs have led to the fact that market penetration for the therapy has been restricted primarily to the developed healthcare markets with established orphan drug reimbursement systems.

The need for lifelong therapy creates an even greater financial burden for the healthcare system because young children will undergo decades of treatment with the costs accumulating over years and potentially reach USD 5-8 million per patient for the entire period of treatment.

The pharmacologic basis of action of IBAT inhibitors naturally predisposes patients to gastrointestinal side effects, which not only represents a therapeutic challenge but also a commercial hindrance to market growth. Through the inhibition of bile acid uptake in the distal ileum, IBAT inhibitors are designed to elevate bile acid levels entering the colon, where elevated bile acid levels cause excessive fluid secretion, motility changes, and diarrhea, abdominal pain, and bloating occurring in 20-45% of patients during clinical trials.

Although such gastrointestinal side effects are generally mild to moderate and amenable to dose adjustment and diet changes, serious gastrointestinal upset may force patients to discontinue the drug in 8-15%, thus limiting the fraction of the target population who would be able to endure long-term therapy. Among pediatric patients prone to malabsorption, poor growth, and nutrition problems, gastrointestinal complications necessitate special skills from clinicians and might restrict the use of this medication to hepatology departments in tertiary hospitals and not general practice.

The potential use of IBAT inhibitors in the treatment of MASH (formerly NASH) and other metabolic disorders of the liver, which are associated with disruption of bile acids and lead to inflammation and fibrosis in the liver, is one of the transformative market opportunities. Increased fecal bile acid excretion triggers compensatory by increased production of bile acids in the liver from cholesterol, which may have positive impacts on lipid metabolism in the liver and blood cholesterol content.

Pre-clinical data show that IBAT inhibition leads to lower levels of fatty liver infiltration, inflammation, and fibrosis in animal models of metabolic liver diseases via pathways involving the activation of farnesoid X receptor signaling, modulation of fibroblast growth factor 19 activity, and enhanced insulin sensitivity. Although previous drug discovery efforts to target hypercholesterolemia have been limited by poor gastrointestinal tolerability relative to statins, advances in our knowledge regarding bile acid physiology and combination therapy options present opportunities for IBAT inhibitors in metabolic conditions based on optimal dosing schemes and patient selection criteria.

The total number of patients that could potentially be treated with MASH and metabolic liver diseases is in the millions worldwide, representing a commercial opportunity that could far surpass today’s rare diseases if clinical development efforts prove effective and well-tolerated.

IBAT inhibitor treatments have rapidly adopted precision medicine strategies through the requirement for genetic testing to establish the appropriateness of patients for such therapy and in the development of biomarkers that ensure optimal patient selection and treatment outcomes. Genetic testing for genetic variations associated with transport proteins of bile acids, enzyme synthesis, and regulatory factors have become common in the guidelines for treatment of IBAT inhibitor therapies.

Individuals with PFIC type 1 and type 2 due to mutations in the ATP8B1 and ABCB11 genes, respectively, exhibit the strongest biochemical and clinical responses to inhibition of IBAT function, whereas patients with PFIC type 3 due to mutations in the ABCB4 gene exhibit highly variable responses due to the heterogeneity of their molecular pathophysiology. The genotypic-phenotypic correlation allows physicians to select the best treatment options, anticipate the probability of success, and advise patients on the anticipated outcomes, as well as facilitate economic justifications for therapy because treatment is directed at the most appropriate candidates.

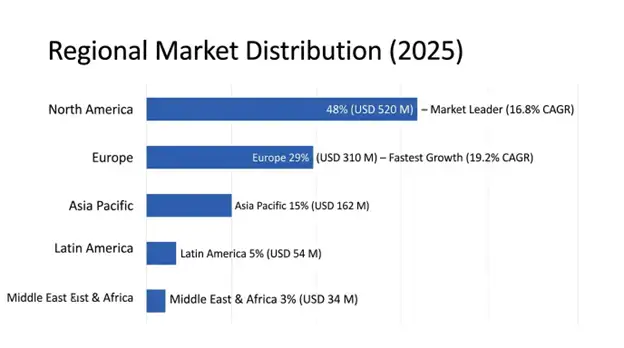

North America holds the leading market share with a valuation of USD 520 million in 2025, forecasted to exhibit a CAGR of 16.8% during 2025-2034. The US holds the top market share owing to advanced regulatory approvals creating a precedent, advanced rare disease drug development and delivery systems including patient identification and genetic screening programs, and a robust reimbursement system for rare diseases in children.

Breakthrough Therapy designation, Priority Review pathway, and Rare Pediatric Disease priority review voucher system have been used by the FDA to promote the development of IBAT inhibitors by offering lucrative financial rewards to drug companies. The existing system of pediatric hepatology clinics, genetic counselors, and patient advocacy groups creates an ecosystem that facilitates patient identification and recruitment for trials and post-marketing uptake of the treatment is facilitated.

Medicare and Medicaid systems offer essential coverage for approved IBAT inhibitors, complemented by the drug manufacturers' patient assistance programs for individuals without adequate insurance or high out-of-pocket costs. The use of highly specialized centers for prescribing allows for the successful implementation of risk evaluation and mitigation strategies (REMS), patient monitoring program, and outcomes-based contract, thereby supporting premium pricing.

Europe will experience the highest CAGR at 19.2%, growing up to USD 310 million by 2034. The regional market growth will be driven by incremental national reimbursement authorizations after EMA centralized approval, with the key players in this market being Germany, France, and the United Kingdom from 2022-2023. Additional countries such as Spain, Italy, the Netherlands, and Nordic nations are expected to follow until 2024-2025.

Ten years of market exclusivity along with efficient development pathways is provided by the European regulatory pathway that has led to fast clinical development and approvals. The pediatric hepatology centers of Europe, especially those located in the UK, Germany, and France, are considered centers of excellence in the management of rare liver diseases and have generated substantial real-world evidence backing their clinical utility and use in payer negotiations.

The European HTA process requires the demonstration of clinical effectiveness and cost-effectiveness against the current standard of care that has been effectively demonstrated through cost savings of transplants, quality-adjusted life years, and reduced family caregiver burden justifying premium pricing.

Odevixibat retains its position as the market leader with a market share of 48%, valued at USD 518 million in 2025, and will register a 17.2% CAGR until 2034. This drug enjoys the advantage of being the pioneer molecule for progressive familial intrahepatic cholestasis, approval for use by individuals in a wider age range up to six months old, and the global commercialization platform of Ipsen owing to its acquisition of Albireo Pharma.

Maralixibat represents 35% of the market with USD 378 million market valuation in 2025, growing with CAGR of 18.6% to 2034, exhibiting strong performance in line with the targeted rare disease business model and broader patient pool in the Alagille syndrome indication. The oral once-a-day formulation and well-established safety profile for the treatment of children enhance prescribing confidence for the drug used by patients of all ages within the Alagille syndrome population, with further label expansion being sought for additional cholestatic indications.

Linerixibat and Volixibat among pipeline products show the fastest growth prospects with an estimated CAGR of 45.2% until 2034, starting from a market size of USD 89 million in 2025, depending on successful completion of phase three trials and subsequent regulatory approval in primary biliary cholangitis and other adult indications beyond pediatric rare diseases.

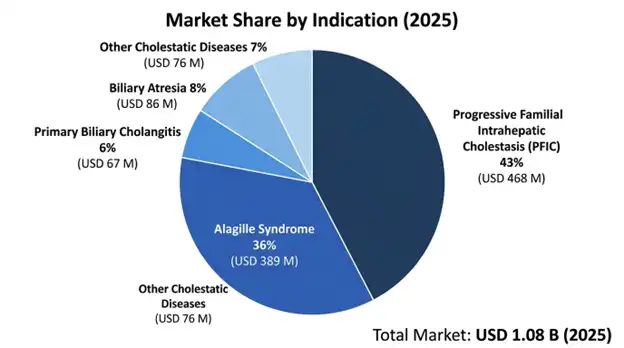

Progressive Familial Intrahepatic Cholestasis is the leading indication category valued at USD 468 million in 2025 with 16.8% CAGR, driven by robust commercial models, high uptake among diagnosed cases, and solid proof of effectiveness in modifying disease process apart from treating symptoms such as pruritus. This indication enjoys the advantage of well-defined criteria for diagnosis, testing, and clinical management, which ensures proper identification and initiation of therapy.

Alagille syndrome is the second-highest revenue-generating indication, with USD 389 million forecasted in 2025, growing at an 18.4% CAGR until 2034, attributable to its higher patient base, high prevalence of severe pruritus that impacts the quality of life adversely, and increasing awareness among pediatric experts that will result in higher detection and treatment.

The highest growth indication is the Primary biliary cholangitis with a forecasted CAGR of 52.3% till 2034, starting with a 2025 base of USD 67 million and depending upon positive Phase III trials of linerixibat and subsequent approval of the drug expected in 2027–2028. The indication has the largest number of patients out of all other cholestatic indications.

Pediatric patients will make up 78% of current market revenues at USD 842 million in 2025 owing to the approval of treatments for pediatric cholestatic disease as well as the long-term nature of the treatments needed for several decades starting in childhood through adulthood. The pediatric sector can benefit from established clinical management systems, hepatology centers specializing in the condition, as well as comprehensive reimbursement mechanisms for rare pediatric diseases.

The share held by adult patients will be 22% of the current market, worth USD 238 million in 2025, though they are anticipated to generate a much higher CAGR of 28.7% from 2025 through 2034 due to the progress made in the development of treatments for adult cholestatic disorders such as primary biliary cholangitis and primary sclerosing cholangitis and other related conditions.

The international IBAT inhibitor market is dominated by highly concentrated companies that produce rare disease drugs and innovative biotech companies, with the top five companies accounting for approximately 89% of the total revenue generated in the market. Competitive advantage is achieved through clinical trial data proving superiority over competitors regarding efficacy and safety, gaining approval and labeling expansion to new conditions, reliable manufacturing that ensures steady supply of the product, and extensive patient assistance programs.

Mirum Pharmaceuticals and Ipsen by way of its acquisition of Albireo have dominance in the commercial market by virtue of their approved drugs, while GlaxoSmithKline is emerging as the key competitor with its late-stage development programs for large adult indications. The competitive environment is changing quite quickly as the late-stage pipeline progresses towards approval and existing players focus on expanding indications that can dramatically change the market dynamics going forward during the forecast period.

The market reflects typical orphan drug dynamics with high barriers to entry involving significant investment in research and development, regulatory challenges, special skill sets needed in clinical trials, and infrastructure needs for patients, along with lucrative commercial prospects such as premium pricing, market exclusivity, and reduced competition in certain indications.

March 2026: GlaxoSmithKline released positive topline results of its Phase III GLISTEN trial in linerixibat for treating pruritus associated with primary biliary cholangitis with statistical significance observed for reducing itch scores against placebo, and with regulatory submission planned by the end of 2026.

February 2026: FDA granted approval of expanded maralixibat label to cover patients with biliary atresia who have undergone Kasai portoenterostomy, marking its entry into a major indication for pediatric liver transplantation.

January 2026: Ipsen released extended 24-month data of its odevixibat programs confirming sustained efficacy and safety while preserving native liver function in responders suffering from progressive familial intrahepatic cholestasis.

December 2025: Intercept Pharmaceuticals commenced its Phase II combination study of obeticholic acid in combination with its investigational IBAT inhibitor in primary sclerosing cholangitis to achieve superior biochemical responses compared with monotherapy.

November 2025: European Medicines Agency granted expanded label approval of odevixibat in covering Alagille syndrome, creating direct competition with maralixibat in Europe and broadening indication scope for both approved molecules.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

21 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.