Share this link via:

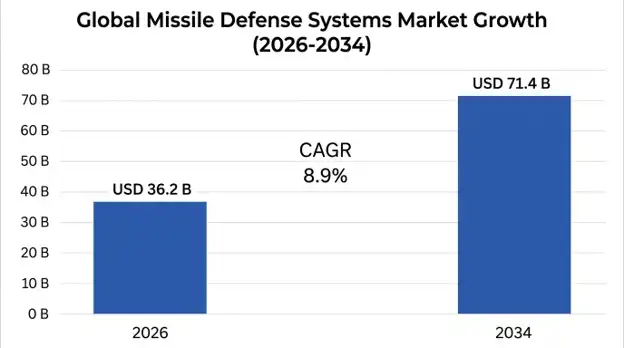

The global missile defense systems market size was valued at USD 32.8 billion in 2025 and is projected to reach USD 36.2 billion in 2026, expanding to USD 71.4 billion by 2034, growing at a CAGR of 8.9% during the forecast period (2026-2034).

Missile defense systems are the most highly technologically advanced and strategically vital segment of contemporary military architecture, comprising sensor arrays, interceptor platforms, command structures, and battle management facilities tasked with locating, identifying, discriminating, and intercepting inbound ballistic missiles, cruise missiles, hypersonic glide vehicles, and other advanced maneuvering weapons throughout all segments of their flight paths. Such missile defense systems must overcome the inherent difficulty of engaging targets that move at speeds of 3-25 kilometers per second, employing complex countermeasures such as decoys and maneuvering re-entry vehicles, as well as electronic jamming, in an effort to defeat missile defense systems.

The modern missile defense system has undergone numerous technological changes since the first emergence of radar-based surface-to-air guided missiles. Missile defense architectures comprise terminal defense systems, midcourse intercept systems, and boost-phase interception systems depending on the phase at which the missiles can be intercepted using different techniques. Terminal defense systems include platforms such as Patriot Advanced Capability-3 (PAC-3), THAAD, and Iron Dome. These are designed to protect targets during terminal phases of flight by intercepting the missiles. Midcourse interception systems include Ground-Based Midcourse Defense (GMD) and Aegis Ballistic Missile Defense systems that protect against missiles in predictable phases.

The strategic importance goes beyond the technical aspects into implications that can be described as far-reaching for the stability of nuclear deterrence, alliances, arms control architecture, and balances of power geopolitically. Effective missile defense could affect the doctrine of mutually assured destruction behind nuclear deterrence as it implies that the first-strike attack can still survive, generating some interesting strategic issues involving offense-defense relations and affecting procurement choices of adversaries.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 32.8 Billion |

| Forecast Value | USD 71.4 Billion |

| CAGR | 8.9% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By System Type, Technology, Platform, Range, Component, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Poland, Israel, Japan, South Korea, Australia, India, China, UAE, Saudi Arabia, Turkey |

| Key Market Playes | Lockheed Martin, Raytheon Technologies, Northrop Grumman, Boeing Defense, L3Harris Technologies, Rafael Advanced Defense Systems, MBDA |

Get more details on this report - Request Free Sample

The driving force behind the increased focus on missile defense systems at the global level is the growing missile capabilities among both peer and regional powers, thereby transforming the global security environment from the relatively predictable bipolar structure of the Cold War era to an environment filled with multi-vector threats and necessitating defensive measures on all fronts. Since 2016, North Korea alone has tested its missiles more than 100 times, with ranges extending up to 13,000 kilometers, including submarine-launched ballistic missiles and MIRV-capable systems.

The hypersonic threat represents one of the most significant technological challenges, as the hypersonic glide vehicles moving at speeds more than Mach 5 and conducting unpredictable maneuvers create engagement scenarios that cannot be effectively addressed by current midcourse interception systems. Examples of systems using this technology include the Russian Avangard, Chinese DF-17, and DF-ZF systems, and the North Korean Hwasong-8 systems. These systems operate within flight profiles that significantly complicate detection and tracking by existing sensor architectures and move in an unpredictable fashion.

China’s expanding missile capabilities represent one of the most significant long-term threat drivers on a sustained basis, as the PLA Rocket Force fields over 1,250 missile launchers with ranges exceeding 500 kilometers, including DF-41 intercontinental missiles that carry up to ten multiple independently targetable re-entry vehicles (MIRVs) with ranges of 14,000 kilometers. Coupled with growth in nuclear weapon stockpiles expected to number 1,000 warheads by 2030, this provides continuous incentives for improved defensive systems in the Indo-Pacific region.

Unlike systems evaluated solely through controlled testing programs, missile defense systems which have been employed in areas of active warfare have generated substantial operational data confirming the viability of such systems while simultaneously pointing out capability deficiencies compelling urgent procurement decisions. In particular, the Israeli Iron Dome system has achieved hit ratios more than 90% against short-range rockets since 2011, while the Arrow-2 and Arrow-3 missile defense systems intercepted Iranian ballistic missiles in April and October 2024.

Patriot, NASAMS, and IRIS-T systems' consistent use in Ukraine against persistent Russian missile strikes have highlighted the requirements of high-tempo defensive operations, including an average interceptor consumption rate of 3.2 missiles per engagement; radar degradation under electronic warfare conditions; and the crucial necessity to resupply interceptors, leading to a 340% increase in interceptor production capacity across Western defense manufacturers.

The operational experience gained by Saudi Arabia in terms of using Patriot and THAAD missile defense against Houthi missiles and drone strikes has reaffirmed concepts of layered defense while underscoring the financial difficulties of dealing with low-cost asymmetric threats through expensive interceptors, spurring further research in affordable laser and shorter-range kinetic weapons systems.

One of the biggest factors restricting the proliferation of missile defense systems is the extremely high cost associated with the development, acquisition, and maintenance of interceptor systems that individually range between USD 3.5 million for Patriot PAC-3 MSE and USD 24.5 million for Standard Missile-3 Block IIA, resulting in serious cost-exchange challenges, whereby defensive interceptors are five to fifteen times more expensive than offensive missiles worth between USD 500,000-2 million, respectively. Costs associated with the Ground-Based Midcourse Defense (GMD) program exceed USD 67 billion.

Reliance on high-cost interceptor systems makes it possible for the enemy to employ saturation attacks by employing cheap weapons intended to destroy the defenders' supply of interceptors, forcing defense planners to make difficult decisions regarding asset protection priorities. The problem is made even harder by the fact that the environment requires more advanced systems and bigger magazines.

High-energy lasers and high-powered microwave devices as directed energy weapons offer transformative potential by fundamentally changing the cost-effectiveness of anti-missile technology from the current expensive and complex missile interceptions to a much simpler system where engagement costs are measured in dollars rather than millions of dollars. For example, the High Energy Laser Mobile Demonstrator from the US Army has successfully destroyed drones and mortars within 1-5 kilometers.

The transition from experimental prototypes to operational systems represents an estimated market opportunity of USD 12-18 billion and covers weapons design, power supply systems, heat management systems, and beam control systems that allow for the successful interception of ballistic missiles and cruise missiles at operationally relevant ranges.

Missile defense operations are undergoing rapid digital transformation by integrating AI and ML into Command and Control, Battle Management, and Communications systems. With increasing numbers of sensors and speeds of threats, human operators will be unable to process the increasing volume of data that need to be analyzed within seconds to make optimal interception decisions. AI software will analyze the data collected by land, naval, and satellite sensors.

The operational lines that demarcate air and missile defense have blurred in recent times due to the evolving nature of cruise missiles, hypersonic weapons, and unmanned aircraft, leading to situations where an integrated sensing system, battle management system, and weaponized system become essential in dealing with any kind of threat. The new architecture uses common data links and a joint tactical ground station.

The North American region held the largest market share at USD 15.2 billion in 2025, expected to grow at a CAGR of 8.4% from 2025 to 2034. The supremacy of the US is a result of the fact that it has one of the best missile defense shields in the world comprising Ground-based Midcourse Defense with 44 interceptors, Aegis Ballistic Missile Defense with 48 missile-defense enabled surface ships, THAAD and Patriot defense systems.

The budget for the Missile Defense Agency in FY 2025 stood at USD 10.2 billion due to its priority in Congress under challenging environments. Some of the key programs include Next Generation Interceptor for a system replacement along with better kill vehicles, Hypersonic and Ballistic Tracking Space Sensor Constellation for constant tracking capability, and Glide Phase Interceptor for hypersonic defense.

The European region is projected to be the fastest-growing region with CAGR estimated at 11.8% during 2026-2034 and exceeded USD 7.4 billion in 2025. The increasing Russian threats have made missile defense a core defense issue rather than a secondary one and almost all NATO nations are investing heavily in missile defense procurement programs. The European Sky Shield initiative is the biggest multinational defense procurement deal in the alliance's history.

Germany is taking the lead in the initiative, making significant investments at home in its capacity as the largest European market. Poland, in its role on the frontlines, ensures continued procurement, while Baltic countries among other small member states make their first investments in advanced technologies.

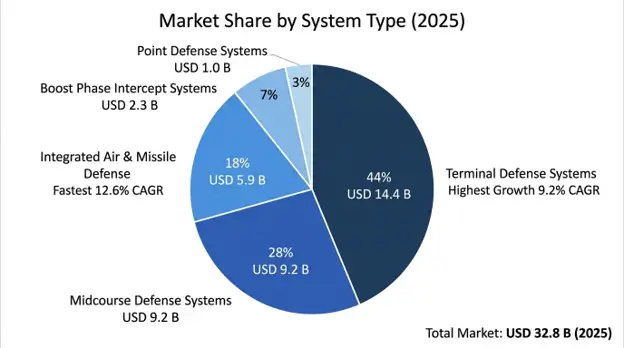

Terminal Defense Systems lead the market, accounting for 44% of total market share worth USD 14.4 billion by 2025, with a CAGR of 9.2%. This group comprises systems such as Patriot, Terminal High Altitude Area Defense System (THAAD), Iron Dome, and David's Sling, which remain market leaders due to wide allied adoption and their operational success record, coupled with ongoing enhancements to their capabilities.

Integrated air and missile defense systems have the highest growth rate of 12.6% CAGR. This growth is driven by demand for unified defense architectures that can target a variety of threat types from different types of sensors and interception options.

Hit-to-Kill Technology leads the market with a 52% share, supported by its integration into Patriot PAC-3, Terminal High Altitude Area Defense, and Ground-based Midcourse Defense systems. Directed Energy Weapon technology holds the second largest position, growing rapidly at a CAGR of 18.4%. This growth is attributed to high development investments and successful operational demonstrations and improved cost-effectiveness.

The Ground-based Systems constitute a 46% market share valued at USD 15.1 billion, comprising mobile land-based platforms that are considered the first line of defense for securing border areas and military establishments. The naval-based Systems contribute to the 32% market share driven by the popularity of the Aegis Combat System.

Missile defense system manufacturing companies in the global market operate within a highly concentrated market structure because the industry is dominated by leading manufacturers with systems integration capabilities, classified information technology, and strong government relations required to participate in such programs. These five companies have close to 72% of the total market revenue share.

Differentiation through competition relies on proven efficiency via combat experience, ability to integrate for effective allied operations, technical superiority in dealing with new threats, and manufacturing capability to ensure quick delivery of interceptors under increasing threat scenarios. Partnerships and cooperative efforts among firms are becoming more widespread due to sharing in development costs and access to export markets via governmental agreements.

April 2026: Contract modification valued at $2.8 billion was awarded to Lockheed Martin for production and capability improvements, including improvements to discrimination algorithms and cruise missile engagement range increases.

March 2026: Production capacity for Patriot Advanced Capability-3 MSE interceptors increased by 340% in response to European and Indo-Pacific partner countries' procurement needs and the need to increase inventory levels.

February 2026: The US Missile Defense Agency awarded a USD 1.4 billion contract for the Hypersonic and Ballistic Tracking Space Sensor, which is expected to provide persistent coverage for persistent threat tracking across a constellation of four satellites by 2027.

January 2026: Germany successfully delivered its first battery under the Arrow-3 program via emergency procurement, providing Europe with its first operational exoatmospheric missile interception capability for intermediate and intercontinental range threats.

November 2025: Northrop Grumman bagged an USD 3.2 billion development contract for the Next Generation Interceptor program that aims at replacing the aging Ground-Based Interceptors with an advanced kill vehicle until 2028.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.