Share this link via:

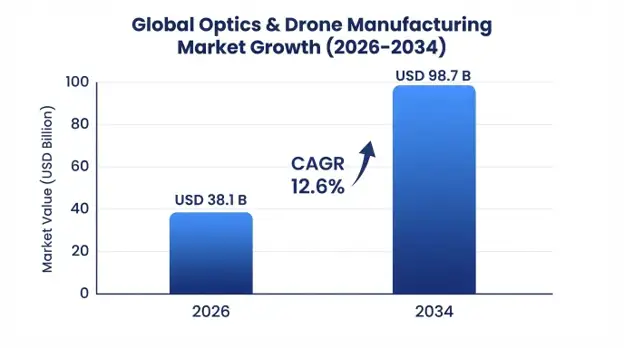

The global optics and drone manufacturing market was valued at USD 32.4 billion in 2025 and is projected to reach USD 38.1 billion in 2026, expanding to USD 98.7 billion by 2034, growing at a CAGR of 12.6% during the forecast period (2026–2034).

The optics and drone manufacturing market is an integration of precision optical science and unmanned aerial vehicle (UAV) platforms of precision optical science and the unmanned aerial vehicles platform to form a technology that revolutionizes intelligence collection, monitoring, and automation in both the military and civilian sectors. The optics and drones manufacturing market includes the entire spectrum of the value chain starting from the manufacture of optical devices such as electro-optics, infrared imaging systems, LIDAR scanners, and laser designators to the manufacture of the drone airframes and its related propulsion and control systems.

The technical basis of this market is in the integration of the state-of-the-art optical payload capabilities into more complex autonomous drone platforms. Very long run-on sentence. Split into two or three sentences for readability., which feature high-resolution visible cameras able to provide ground sampling distances of 5-15 cm from altitudes of 5,000 m, thermal infrared cameras sensitive enough to detect temperature differences of 0.05°C for equipment condition assessment, and laser rangefinder that provides accurate target location within one meter at distances of 15-25 km. Commercial drones offer similar capabilities., with agricultural drones integrating multi-spectral cameras for monitoring health indices of crops within 4-12 spectral bands, precise GPS for achieving centimeter accuracy in repeat flights, and on-board computing capability for processing data and creating real-time images.

The commercial significance of the market extends well beyond the conventional aerospace and defense markets to include innovative uses in infrastructure monitoring, precision farming, environmental observation, and future logistics systems. Energy companies use thermal camera drones and LiDAR scanners to monitor power lines, blades of wind turbines, and solar panels, detecting maintenance needs before equipment failure and cutting down inspection costs by 60-75%, as opposed to using helicopters, and increasing safety through avoidance of exposure to high voltage. Drones equipped with photogrammetry and LiDAR scanners can generate 3D site models of sites with millimeter precision, allowing regular monitoring and volumetric calculations impossible to achieve cost-effectively through traditional surveys on foot.

Integrating artificial intelligence and edge computing within optical payloads is a shift in paradigms from simple data gathering systems to self-sufficient analysis systems. Contemporary drones with optical payloads have incorporated AI processors that allow for real-time object recognition, autonomous anomaly recognition, and predictive analytics which convert the captured data into useful information using AI without the need for any ground processing equipment. Such technology helps create autonomous infrastructure inspection systems which can detect and recognize structural anomalies mid-flight, autonomous agricultural monitoring systems which are able to detect disease breakouts and pests within crops and autonomous security surveillance systems that can monitor suspicious activity.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 32.4 Billion |

| Forecast Value | USD 98.7 Billion |

| CAGR | 12.6% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Optics Component, Drone Platform, Application, End-User, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, Israel, China, Japan, South Korea, India, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | DJI Technology Co. Ltd., Lockheed Martin Corporation, Northrop Grumman Corporation, L3Harris Technologies, Teledyne FLIR, Elbit Systems Ltd., AeroVironment Inc. |

Get more details on this report - Request Free Sample

The key growth factor of the optics and drones manufacturing market includes the significant rise in the investment made by governments around the world in unmanned aerial systems (UAS) along with advanced optical technology. The deployment of drones by military forces for ISR operations, precision strike operations, electronic warfare, and logistical operations has created a need for high performance optical technology. Increased geopolitical tensions and experience gained through recent wars have boosted the procurement programs related to drones in all leading defense sectors.

This development will significantly increase the use of EO/IR camera systems, thermal imagers, laser rangefinding systems, multispectral imaging sensors, and target locating payloads to increase the efficiency of such missions. Continuous advancements in optics are driven by military requirements for long range detection capability, high resolution imaging and accurate target recognition in difficult situations. The high price of these products and technological sophistication will help increase revenue from the sector, and R&D in this sector may help the commercial drone sector.

The commercial drone sector is experiencing rapid adoption owing to impressive return on investment results demonstrated in the use of drones in infrastructure inspection, precision farming, construction surveillance, and emergency services where the use of drone-based optical sensing offers unprecedented efficiencies when contrasted against traditional methodologies. The power utility companies utilizing drones with thermal infrared sensors for inspection of their transmission network identify failures and insulation problems at an average cost of USD 12-18 per structure whereas traditional helicopter-based inspection methods cost USD 220-350 per structure.

Pipeline companies using drone inspection systems over thousands of miles of pipelines have reported savings of 65-80% costs when compared to helicopter inspection. High resolution imaging from drones is capable of detecting corrosion, mechanical problems, and any other encroachments in a manner better than helicopters can provide. An aerial drone inspection mission that creates terabytes of imagery of the pipeline corridor gives permanent digital evidence for baseline comparison and AI-based automated anomaly detection capabilities.

The utilization of drones for photogrammetric and LiDAR surveys in the construction industry has brought about revolutionary changes to site monitoring, earthworks volume calculation, and progress tracking processes. Drones provide high-precision three-dimensional site models within hours, where the process used to take days through the efforts of ground survey crews, thus allowing for site monitoring daily or weekly, detecting any schedule variances, discrepancies in quantities, and safety issues to be discovered before they cause major project delays. The global construction industry, valued at approximately USD 14.8 trillion in 2025, has great addressable opportunities since drone surveys cover only 22 percent of projects in developed markets.

The most important constraint on the growth of the optics and drones manufacturing industry is related to the complex and evolving regulatory environment concerning unmanned aircraft systems operations that poses high operational costs due to the difficulty in compliance, geographic scalability, and uncertainties in developing platforms that comply with varying regulations. The core issue is integrating drone operations into shared airspace with manned aviation used by manned aviation This requires additional communication and surveillance equipment, increasing operational costs.

Despite being the biggest business opportunity for drone optical systems, beyond visual line of sight operational permits are still constrained in many jurisdictions, where regulatory frameworks demand case-by-case authorization, which is not scalable for business service providers. The U-Space regulatory framework introduced by the European Union has well-defined guidelines for drone operations in urban settings but needs infrastructure investment in each member state that is growing very slowly. These regulatory limitations directly hinder the growth of the market by constraining the scenarios of operation where drone optical systems can be deployed commercially.

The development of the urban air mobility ecosystem comprising autonomous drone delivery network, air taxis, and emergency logistics networks is a revolutionary market that needs to adopt advanced optical sensing technology for safe autonomous navigation, collision avoidance, and precise landing in urban environments. The drone delivery network being designed by big logistics firms needs to deploy an advanced optical sensing system that combines a high-resolution camera for autonomous navigation, thermal sensing technology for obstacle detection in low visibility condition, and LiDAR technology for 3D environment mapping.

The Urban Air Mobility industry is projected to reach of USD 21.8 billion by 2030, out of which the optical sensors segment is expected to account for 28-35% of the platform hardware revenue in case of delivery drones and 40-52% in case of passenger carrying aircraft owing to the need for safety critical redundant sensing systems. The need for precise landing of delivery drones to deliver packages to specific addresses will demand optical positioning systems.

Is undergoing rapid technological transformation driven by continuous optimization in Size, Weight, Power, and Cost, which allows for the creation of complex sensors in ever smaller and more economical devices. The development of solid-state LiDARs with no moving parts has significantly shrunk the size of such systems, made them more reliable, and decreased their power requirements, thus allowing for their application in small multirotor vehicles that before could only carry camera payloads.

Snapshot hyperspectral imagery using state-of-the-art filter array technology has allowed the development of hyperspectral imagers weighing less than 500 grams with spectral resolution sufficient for precision farming, environment monitoring, and geology applications.

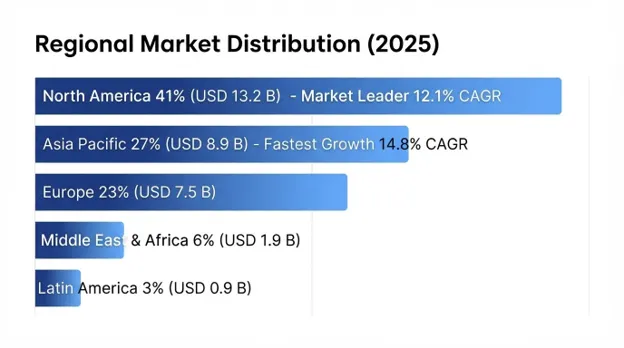

North America held the largest regional market share at approximately USD 13.2 billion in 2025, experiencing a forecasted CAGR of 12.1% until 2034. The region’s dominance is attributed to the U.S as the world’s largest procurement market for defense drones, presence of leading aerospace industry players, optical systems manufacturers, advanced commercial drone services, and significant government spending in developing unmanned systems via research from DARPA, AFRL, and NASA.

The budget of the US Department of Defense dedicated to the purchase of unmanned systems was estimated at USD 4.8 billion in fiscal year 2025, with the most expensive payload segment being electro-optical and infrared sensors. The advantage of the commercial market lies in well-established regulatory framework, which offers operational pathways via FAA Part 107 licensing and gradual BVLOS permitting programs. There were over 1.2 million commercially operated drones licensed by the FAA in 2025.

Asia-Pacific is the fastest-growing regional market and holds a CAGR of 14.8% during 2025-2034, forecasted to touch USD 8.9 billion by 2025. Regional growth is attributed to China being the global leader in drone manufacturing, rapid adoption in the commercial market, particularly in agriculture and infrastructure sectors, and rising defense modernization efforts which involve development of drones with optics.

China, the largest drone manufacturing hub in Asia-Pacific, hosts the world’s leading commercial drone manufacturers and possesses full supply chains for optical devices and is thus cost-effective and technologically advanced. Japan and South Korea are sophisticated markets of commercial adoption with increasing demographics prompting drone automation with government support programs encouraging adoption in agriculture and infrastructure sectors.

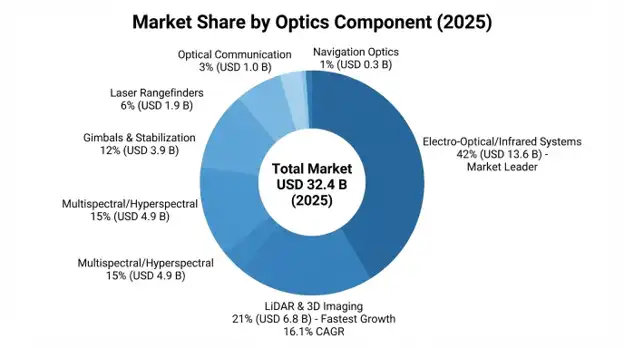

The Electro-Optical and Infrared Systems segment leads the components market with 42% share worth USD 13.6 billion in 2025 and is projected to grow at 12.2% CAGR until 2034. It includes visible cameras, thermal infrared imagers, as well as multi-sensor systems used for surveillance, inspection, and targeting applications in military and civilian markets. It is leading because of its universal application and innovations in multi-sensor systems incorporating day cameras, cooled thermal imagers, and lasers in stabilized platforms.

LiDAR and 3D Imaging Sensors segment is expected to be the fastest-growing component segment and will be worth USD 6.8 billion in 2025, growing at 16.1% CAGR until 2034 due to an increase in the usage of the surveying and mapping applications, autonomous navigation needs, as well as advancements in solid-state technology that decreases costs and weight.

Multi-Rotor Drones lead the Platform segment with 48% of market share worth USD 15.6 billion in 2025, and include quadcopters, hexa-copters, and octo-copters used in inspection, agricultural, and short distance surveillance operations. Vertical takeoff capability, hovering capability, and payload capacity which allows for variable optical payload configuration without changing the platform design.

Fixed Wing Drones have 35% market share worth USD 11.3 billion in 2025 with 13.4% CAGR. Fixed wing drones are employed in surveillance, survey, and military reconnaissance where multi-rotor drones are hindered by low flight endurance. Fixed wing platforms which can achieve flight endurance of 8-36 hours allow for extended operation missions and range, justifying expensive optical payload investment.

Is the largest application segment, valued at USD 14.8 billion in 2025, growing at a CAGR of 12.8% until 2034, due to the global trend toward defense modernization, combined with high prices for military optical systems. It features non-discretionary procurement, long-term programs and constant improvements of performance.

Commercial Inspection & Monitoring is valued at USD 7.4 billion in 2025, with 15.6% CAGR, being the fastest-growing commercial segment due to infrastructure inspections, proven return on investments, and increased permissions for commercial operations.

Defense and Security Agencies is the largest end-user category accounting for a market size of USD 14.9 billion in 2025, having 46% share owing to increasing defense procurements and homeland security applications. The category sustains its leadership position by virtue of value-based system procurement and constant upgrading of capabilities.

Energy and Utilities account for USD 4.2 billion in 2025, growing at a CAGR of 17.3%. This is the fastest growing commercial end user application area because of automation in inspection and predictive maintenance in critical infrastructure.

The global optics and drone manufacturing industry exhibits a segmented competitive landscape. that shows two different competitive landscapes within defense and commercial sectors. Is characterized by an established aerospace contractor ecosystem. involving companies such as Lockheed Martin, Northrop Grumman, and L3Harris Technologies competing via their long-term contracts, system integration capabilities, and security clearance. The commercial sector is highly dynamic with competition between DJI leading the platform market and Western competitors making security-oriented systems and optical payload suppliers with high performance sensors and AI capabilities.

The combined revenues of the top 12 companies amount to about 54-61% of total market revenue, and the competitive edge is based on the performance capabilities of optical systems, integration of platforms, AI, and other autonomous capabilities, and complete solutions that include hardware, software, and analytics. Market consolidation is going on with strategic acquisitions of optical technology from platforms and vice versa.

June 2026: The aerospace corporation Lockheed Martin was awarded the contract modification worth $1.8 billion related to the upgrade of optical sensors of the next-generation drones with artificial intelligence-enabled multi-spectrum targeting systems which are capable of improved target identification and longer detection ranges up until 2030.

May 2026: DJI Technology introduced the Enterprise Pro line with built-in solid-state LiDAR and 150 megapixels camera systems mounted on a single gimbal with the price of USD 45,000 that incorporates AI-based technology designed specifically for professional applications.

April 2026: Teledyne FLIR revealed its new thermal imaging module with 8K visible imaging for drone installation that will have simultaneous 1280×1024 thermal imaging and 8K visible imaging in a 75-gram module priced at USD 12,500 each for use in inspection missions.

March 2026: L3Harris Technologies showcased the ability of drones to communicate through an advanced laser datalink technology that will provide high-definition intelligence exchange in GPS-denied environment for distributed surveillance networks.

February 2026: Elbit Systems concluded testing the integration of its advanced EO targeting system on drones with 25 kilometers' identification range and AI-based automatic tracking and laser designation features.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

08 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.