Share this link via:

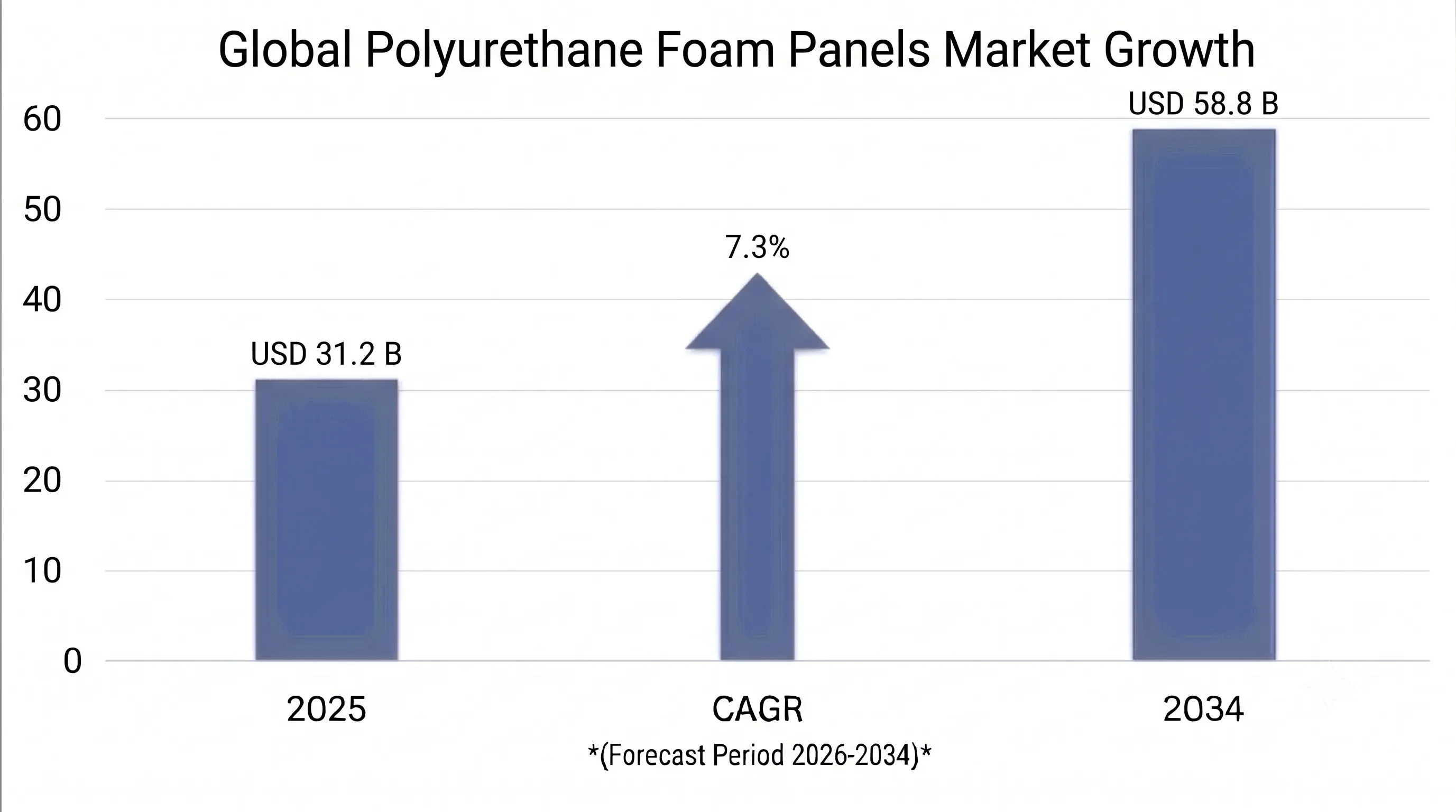

The global polyurethane foam panels market size was valued at USD 31.2 billion in 2025 and is projected to reach USD 33.4 billion in 2026, expanding to USD 58.8 billion by 2034, growing at a CAGR of 7.3% during the forecast period (2026-2034).

Polyurethane foam panels are advanced engineered building materials produced through the controlled chemical reaction of polyols and diisocyanates (mostly MDI or TDI) while employing blowing agents, catalysts and additives, resulting in high-performance thermal insulation and structural products. The panels provide excellent thermal resistance, with typical values of lambda ranging from 0.020 W/m·K to 0.028 W/m·K, which is significantly higher than other insulation materials such as mineral wool (0.030-0.040 W/m·K), expanded polystyrene (0.033-0.038 W/m·K) and extruded polystyrene (0.029-0.035 W/m·K). This thermal advantage allows for the use of thinner wall sections and complies with the strictest building energy codes, offering essential benefits in space-constrained building applications where each centimetre of usable space has a premium value.

There are several configurations available for the product, depending on the performance needs. Rigid polyurethane sandwich panels combine metal, fiber cement or composite facings with foam core to provide thermal insulation, structure and weather protection for industrial applications, cold storage applications and commercial construction. Spray polyurethane foam systems deliver easy installation for retrofit applications, odd shapes, and roofing applications in which continuous thermal barrier eliminates thermal bridging. Structural insulated panels are factory-made wall and roof systems that feature a core of polyurethane foam and an outer layer of oriented strand board or metal sheets and offer faster construction schedules and better energy efficiency than standard framed construction with cavity foam insulation.

The strategic value of the market goes beyond construction to sectors such as temperature-controlled logistics, pharmaceutical storage, food processing facilities and industrial process insulation, where there is a direct link between the temperature control and the product quality, the energy costs and the regulatory compliance. Rigid polyurethane foam closed cell panels are moisture resistant to less than 2% per volume; maintain dimensional stability over a wide temperature range; with compressive strength ranging from 150-250 KPa, these panels are suitable for load bearing, continuous insulation systems and harsh environmental conditions, such as extreme temperatures from -40°C to +120°C in special formulations.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 31.2 Billion |

| Forecast Value | USD 58.8 Billion |

| CAGR | 7.3% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Middle East & Africa |

| Segments Covered | By Product Type, Density, Application, End-User, Thickness, Facing Material, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Kingspan Group, BASF SE, Covestro AG, Huntsman Corporation, Metecno Group, ArcelorMittal, Rockwool International, Recticel NV, Dow Inc., NCI Building Systems |

Get more details on this report - Request Free Sample

Energy efficiency in construction, along with the increasing number of building energy performance laws enacted globally, is one of the key factors responsible for growth in the polyurethane foam panels market. Many governments today have adopted various laws that promote the usage of energy-efficient buildings to lower carbon footprints from building operations, as buildings are known to consume a considerable amount of energy annually.

The primary reason why builders choose polyurethane foam panels is because of their exceptional insulating capacity, which ensures that the heat loss and gain through walls is minimized, leading to energy savings in heating and cooling systems. High insulation capacity allows the panels to meet stringent building regulations without increasing wall or roof dimensions.

Mandatory energy-efficient guidelines are also being implemented by emerging countries due to the rise of urbanization and infrastructural construction. With increased attention on green construction, sustainable construction, and carbon reduction schemes, there is a high likelihood that there will be more use of polyurethane foam panels in construction activities. With increasing stringent energy policies and construction guidelines from governments worldwide, polyurethane foam panels are likely to experience increased demand in the future.

Global demand for polyurethane foam panels is being driven by the rapid growth of global cold chain infrastructure as temperature-controlled storage and distribution facilities need to maintain a constant, high performance thermal barrier, which polyurethane foam panels offer better than the alternative insulation materials. The global cold chain market is expected to reach USD 312 billion by 2025, marking an annual growth rate of 11.8% on account of growing demand for cold chain infrastructure for the delivery of biologics and advanced therapeutics, rising food safety standards in the developing economies, urbanization and changing dietary habits driving frozen and prepared food consumption, and the complex last-mile cold storage needs of e-commerce grocery delivery infrastructure.

Polyurethane foam sandwich panels are the primary construction material for cold storage facilities., and the thickness of the panel varies according to the requirements of each room; wall, ceiling and floor thickness requirements for chilled storage are 80-100mm, which can keep the temperature at 0-5℃; wall, ceiling and floor thickness requirements for frozen storage are 150-200mm, which can keep the temperature at -18℃ to -25℃; wall, ceiling and floor thickness requirements for special ultra-low temperature are 200mm or more, and they can be used in pharmaceutical and biotechnology cold storage. The annual demand for polyurethane foam panels in cold storage construction is more than 150 million square meters worldwide, and the demand for the panel materials alone in a standard 15,000 square meter cold storage facility is USD 2.4-3.2 million, due to the surface area of the envelope.

The pharmaceutical cold chain is a major growth area in demand after the COVID-19 vaccination requirements revealed the weak points in the cold chain infrastructure across the world. Exacting pharmaceutical storage regulations for Good Distribution Practice call for exact temperature control, verified thermal performance, pharmaceutical grade hygienic surface finishes and built-in monitoring, which is why top tier polyurethane foam panel systems are being adopted that deliver superior thermal consistency, surface finishes and monitoring capabilities. Biologic drugs are driving premium panel demand in the long-term as the biologics market expands with more than 1,400 biologic drugs in clinical development that require cold chain storage.

Significant challenges for the polyurethane foam panels market stem from price volatility in raw materials along with the concentration in the supply chain, as the panels are produced using raw materials like polymeric MDI (Poly MDI) and methylene diphenyl diisocyanate (MDI) which account for 40-50% of production costs, polyol blends that make up 30-35% of costs, and specialized blowing agents, flame retardants and surfactants that make up the remainder of costs. Prices for these materials tend to be quite volatile and are tied closely to the prices of crude oil and natural gas feedstocks, world commodity markets, and geopolitical factors influencing crude oil and natural gas production and transport.

As is evident from the MDI market, the supplier base is highly concentrated: BASF, Covestro, Huntsman, Wanhua Chemical and Dow account for roughly 87% of the global production capacity, with all suppliers operating large-scale capital-intensive manufacturing plants that require significant technical expertise and regulatory oversight. This concentration leads to periodic supply constraints especially after an unplanned production outage or during a force majeure event at the big chemical complexes or during the demand surge when the production is out of available capacity. The 2021 Texas winter storm caused simultaneous shutdowns of several isocyanate plants, causing a shortage of MDI globally which drove prices up from USD 1,950/tonne to over USD 3,400/tonne in just eight months, which caused panel manufacturer margins to be squeezed and impacted construction project schedules across various regions.

As the industry moves away from hydrofluorocarbons (HFCs) in systems, where global warming potential (GWP) is subject to phase-down limits under the Kigali Amendment, to systems that use hydrofluoroolefins (HFOs) with lower GWP, there are further cost pressures associated with environmental regulations. Environmental regulations contributing to blowing agent transitions are further cost drivers in moving away from hydrofluorocarbons (HFCs) in systems through the phase-down schedule in the Kigali Amendment towards hydrofluoroolefins (HFOs) with lower global warming potential (GWP), but at a price premium of 4-6 times conventional HFC cost. A blowing agent transition adds USD 10-18/m² to the cost of making the product, or 15-25% more to the cost of the material for construction customers that are bidding on construction projects and are competing.

The growing focus on decarbonization and circular economy concepts opens large market potential for polyurethane foam panel manufacturers willing to formulate new products using polyols derived from bio-sources, recycled materials, and blowing agents with low GWP for their production to meet the stringent carbon footprints demanded by the market. Bio-based polyurethanes made with castor oil polyols, soybean oil, rapeseed oil or lignin-based polyols are a new premium product segment that can earn a higher price premium of 18-28% over conventional panels and can receive green building certification credits and be within the scope of procurement preferences of corporate real estate occupiers who are sensitive to sustainability.

Comprehensive sustainable building commitments have been announced by major multinational companies such as Microsoft, Amazon, Apple, Google, and many European companies, all committed to using low-carbon building materials – establishing new premium market segments for bio-based and recycled content polyurethane foam panels. The embodied carbon of building products is becoming more of a regulatory focus with the upcoming mandatory Whole Life Carbon assessments in new buildings in the UK, the EU taxonomy for sustainable activities, and voluntary initiatives such as the Embodied Carbon in Construction Calculator from the Carbon Leadership Forum, which is stimulating the use of low carbon insulation alternatives with verified environmental product declarations.

Chemical recycling methods such as glycolysis and acidolysis enable the recycling of end-of-life polyurethane foam to polyols that can be used in new panel manufacturing, thereby solving the problem of historical disposal and providing recycled content for new panels. Companies that deliver commercially viable, high-performance panels with a high proportion of recycled content or bio-based feedstocks are well placed to enjoy premium pricing, preference in government and corporate sustainability led projects, and access to sustainable product libraries to be used by architects, engineers and ESG motivated real estate investors.

Technological innovation is transforming the polyurethane foam panels market, especially as digital technologies, sensors and the Internet of Things are integrated into passive insulation materials to become active systems for the monitoring and optimization of building performance. Smart polyurethane panels feature built-in sensors that continuously monitor temperature differentials, moisture, structural stress and thermal performance, allowing predictive maintenance, improved energy efficiency, and early detection of performance degradation. of degradation in the performance of the building envelope which might affect building energy use or the comfort of the building's occupants.

Sensors integrated into polyurethane panels ensure continuous monitoring of the integrity of the insulating material, temperature uniformity and thermal bridge detection fundamental to the regulatory compliance of cold chain applications, such as pharmaceutical storage and food processing. They produce complete data streams to satisfy Good Manufacturing Practice (GMP) and Hazard Analysis Critical Control Point (HACCP) validation requirements and provide accurate monitoring of the refrigeration system and predictive analytics for operating optimization.

Digital monitoring combined with high-performance polyurethane insulation yields data assets which fuel building commissioning, facility maintenance and performance optimization across the whole building lifecycle. Advanced panels include RFID tags for automated inventory and installation verification, and machine learning algorithms that analyze performance data to optimize HVAC system operation, forecast maintenance needs and determine opportunities for further energy savings by performance tweaks or specific envelope improvements.

Polyurethane foam panels market in Asia Pacific is expected to be the leading region as it is expected to generate almost 46% of the total global revenue in 2025. Rapid urbanization, large-scale construction projects, increasing industrial activities and investments in cold chains make the region dominant. The construction industry in China, coupled with its industrial growth and interest in designing energy efficient buildings, is driving the demand for the region. The extensive construction industry in China, coupled with its industrial growth and interest in designing energy efficient buildings, is driving China's regional demand. The government's campaigns for carbon reduction and sustainable construction are still encouraging the use of new and improved insulation materials, including polyurethane foam panels.

India is the region’s fastest-growing major market, which is being driven by industrialization, infrastructure improvement, logistics growth and the need for temperature-controlled storage facilities. The government's housing initiatives and industrial investments are also driving market growth. The government's housing programs and manufacturing investments are also contributing to the growth of the market. As the Southeast Asian nations like Vietnam, Indonesia, Thailand, and Malaysia are experiencing manufacturing growth and foreign direct investment, the demand is also increasing in these regions. Polyurethane panel use is increasing with the demand for high-energy efficiency in industrial buildings and warehouses as well as in cold storage operations. The region is expected to maintain its market leadership over the forecast period. thanks to the continued economic growth and investments in infrastructure.

The Middle East & Africa is the world’s fastest-growing polyurethane foam panels market. is the Middle East & Africa, fueled by the rapid construction of large-scale infrastructure projects, the rise in industrial activities, and energy efficient buildings. Gulf countries, especially Saudi Arabia and the United Arab Emirates, are investing significantly in infrastructural projects that include residential, commercial, tourism and logistics sectors within the context of long-term economic diversification policies. Due to the extremely harsh weather conditions and the cooling demands, polyurethane foam panels have proven to be an ideal choice owing to their excellent thermal insulation capabilities and energy efficiency.

Sub-Saharan African countries are experiencing strong market growth. in the market on account of the growth in the infrastructure for cold chain and pharmaceutical distribution sectors. The increased investments in the food industry are contributing towards the increased demand for polyurethane foam panels in these countries including South Africa, Nigeria, Kenya, and Egypt.

Rigid Polyurethane Foam Panels hold the largest market share owing to their superior insulation capacity, strength, and durability. Rigid polyurethane foam panels are widely applied in industrial buildings, cold storage, commercial structures, and logistical facilities. They are popular owing to their superior energy efficiency, easy installation process, and longer life span.

The Spray Polyurethane Foam Systems segment is expected to witness the highest growth during the forecast period owing to the growing preference for building renovation and roof insulation. Spray polyurethane foam systems provide a perfect fit for residential as well as commercial buildings due to their energy-saving properties. Spray polyurethane foam systems reduce thermal bridging and are air and moisture resistant.

Structural Insulated Panels (SIPs) are gaining popularity in residential as well as light commercial constructions due to their capacity to provide both strength and insulation. SIPs play a vital role in accelerating the construction timeline along with improving energy efficiency.

Flexible Polyurethane Foam Panels have gained a small share in the polyurethane panels market owing to their use in specialized applications like soundproofing, automobiles, and architectural designs.

Building & Construction is currently the biggest segment, owing to increasing usage of polyurethane foam panels for industrial, commercial, and residential buildings. They are used because of their high thermal properties, structural integrity, and attractive appearance, and can be used on walls, roofs, and floorings. Increasing preference for energy-saving buildings and sustainable building practices is anticipated to propel the segment growth over the forecast period.

The fastest growing segment in terms of application is Cold Chain & Refrigeration owing to increasing usage of cold storage and food and drug processing centers. Polyurethane foam panels are increasingly employed in cold chains and food processing plants owing to their superior insulation capabilities, water-proof properties, and consistent internal temperatures maintenance.

Industrial facilities account for the largest market share of 42%, comprising factories, logistic warehouses, food processing centers, and pharmaceutical production units in which PU foam sandwich panels play a key role in providing building envelope systems with thermal control, structural strength, and hygiene. The commercial construction industry comprises 31% market share, which includes retail stores, office buildings, hotels, and institutions adopting advanced insulation systems to comply with the energy and green building codes.

Residential Construction forms 15% of the market share due to programs for energy-efficient houses, prefabricated construction methods, and retrofit insulation installations in which polyurethane systems help meet tough thermal requirements. The Cold Chain Logistics market contributes 12% catering to cold storage centers which require a continuous thermal barrier as well as regulated environment controls.

The global market for polyurethane foam panel products features a relatively concentrated structure wherein the leading players in the market account for roughly 48-55% of the market share based on their robust product offerings, widespread manufacturing capabilities, and strong connections with prominent contractors and developers. Leading positions in the industry require significant spending on research and development efforts amounting to 6-10% of total sales to stay up to date with technological trends as well as building standards for safety and environmental concerns.

Competitive differentiation is driven by superior thermal performance, fire safety compliance proven through extensive testing and certification, quality control measures to ensure consistent product performance and tolerance, and technical expertise, including design assistance, installation training, and engineering services for projects. Market consolidation is underway because large firms have been acquiring smaller firms in particular geographical regions to gain customers and technical expertise in growing market segments.

April 2026: Kingspan Group revealed the start of its state-of-the-art manufacturing plant in Chennai, India, with an annual manufacturing capacity of 12 million square meters of insulated metal panels using the latest technology of continuous lamination aimed at the fast-growing market of India.

March 2026: BASF SE introduced its innovative Neopor P+ polyurethane foam system that enables the production of panels with 22% reduction in embodied carbon using partially bio-based feedstock and advanced process technology, achieving preliminary certification for Europe.

February 2026: Covestro AG obtained a Class A2 rating for its Bayfit polyurethane foam with thermal conductivity of 0.024 W/m·K in accordance with EN 13501-1, solving key access problems in Europe for high-rise construction projects.

January 2026: USD 185 million acquisition by Huntsman Corporation of Europe-based company specializing in spray foam systems helped expand downstream footprint in high-growth retrofit applications and contractor training programs in twelve European countries.

December 2025: EcoPanel+ ultra-high-performance insulation from Metecno Group met the 0.020 W/m·K target and included up to 20% recycled content, meeting premium green building certification and corporate sustainability purchasing requirements.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.