Share this link via:

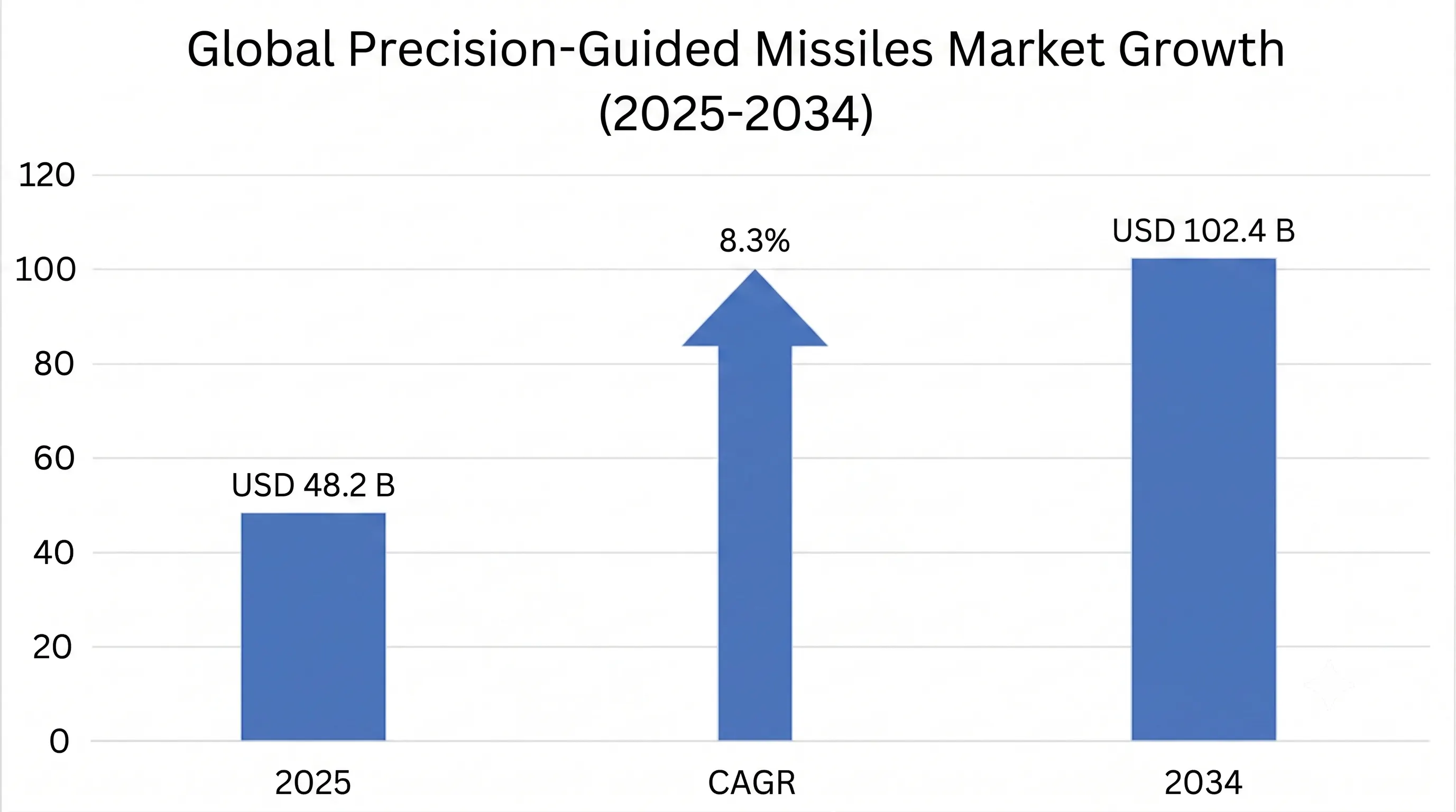

The global precision-guided missiles market size was valued at USD 48.2 billion in 2025 and is projected to reach USD 53.8 billion in 2026, expanding to USD 102.4 billion by 2034, growing at a CAGR of 8.3% during the forecast period (2026-2034).

Precision-guided missiles are among the most strategically important and technologically advanced weapons in today's defense arsenals, combining advanced propulsion systems, multi-mode guidance architectures, and increasingly autonomous targeting capabilities to produce lethal effects with circular error probabilities in the single digit meters, as opposed to the hundreds of meters seen with unguided munitions. These weapon systems have revolutionized military doctrine and have enabled proportional, discriminate use of force that is effective in both maximizing the destruction of the target and minimizing collateral damage in a variety of operations, such as contested electromagnetic warfare (EW) environments, urban combat scenarios, maritime interdiction operations and integrated air defense suppression missions (IADS).

The technological components include advanced multi-domain guidance architectures, inertial navigation systems for all-weather autonomous navigation without external guidance, Global Navigation Satellite System receivers for meter-level terminal accuracy, active and semi-active radar seekers for all-weather, autonomous target acquisition, imaging infrared seekers for man-in-the-loop flexibility, and laser designation compatibility for precision strikes directed by forward air controllers. Artificial Intelligence (AI) and machine learning (ML) algorithms are increasingly being used in modern systems to enable them to identify targets, plan flight paths to avoid them and coordinate the use of multiple missiles, as well as to engage moving targets, representing a paradigm shift from manually guided weapons to more and more autonomous systems operating within pre-defined engagement parameters.

The Ukraine conflict has had a transformative impact on the market as the critical weakness in Western munitions supply chains was exposed and lessons were learned about the industrial scale consumption rates of precision weapons in peer-competitor conflicts. The daily expenditure rates of anti-tank guided missiles, precision artillery rounds, and air defense interceptors far outstripped the annual production rates and forced emergency procurement programs and basic reorientation of defense industrial base capacity planning. The fact of this operational reality has triggered the biggest defense procurement spree since the Cold War: NATO allies have collectively increased operational precision munitions spending by over 60% over the last three years (2022–2025) and are also spending billions on building up precision munitions manufacturing and strengthening supply chains.

Commercial revenue doesn't just apply to individual weapon systems, but also to the wider kill chain infrastructure, such as targeting systems, battle management networks, electronic warfare countermeasures and logistics support systems that all play a role in the effectiveness of the kill chain. Precision missiles can be combined with unmanned platforms, real-time information feeds and networked command systems to become part of a ‘sensor-to-shooter network' as opposed to a point solution providing significant market opportunities in system integration, software development, and lifecycle support services in addition to the primary weapon hardware.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 48.2 Billion |

| Forecast Value | USD 102.4 Billion |

| CAGR | 8.3% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By Missile Type, Guidance Technology, Platform, Range Classification, Propulsion Technology, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Italy, Poland, Israel, Russia, China, Japan, India, South Korea, Australia, Saudi Arabia, UAE, Turkey, Brazil |

| Key Market Playes | Lockheed Martin, Raytheon Technologies, MBDA, Boeing Defense, Northrop Grumman, BAE Systems, Rafael Advanced Defense Systems, Kongsberg Defence |

Get more details on this report - Request Free Sample

The most critical factor behind the expansion of the precision-guided missiles market is the previously unseen exhaustion of the Western arsenal observed during the Ukraine War, showing that the daily consumption rate of precision weapons in highly intense battles against peers is much higher than assumed in the context of peacetime production capabilities and planning for strategic reserves. The war resulted in exceptionally high consumption rates of of anti-tank missiles, artillery precision munitions, and air defense missiles.

This new operational environment has changed the way defense procurement is approached in both NATO and partner countries, leading to the shift away from just-in-time operations into strategic depth, where maintaining months-or even years’ worth-of combat stockpiles is essential in reserve stockpiles. In 2022 alone, the US allocated over 24 billion dollars for the replenishment of precision munitions. Europe increased its budget for the procurement of precision weapons by 68% during the period 2022-2025. The German army’s 100-billion-euro modernization program will give priority to precision munitions, and Poland pledged 4 percent GDP expenditure on standoff munitions.

Replenishment is not only about replacement but also about upgrading to more sophisticated equipment that has better guidance precision, long-range capacity, electronic warfare resistance, and multi-mode seekers. This creates a continued need for expensive advanced equipment at the same time demanding enormous growth in production capacity for both old and new equipment.

The resurgence of great power competition and the resulting emphasis on high-intensity conflict and contested environments have led to growth in the missile market because major nations and regional powers are refocusing their military capabilities on missions that require standoff engagement capabilities against high-tech integrated air defenses. The move from missions focused on counterinsurgencies to preparing for a peer competitor means that missiles must be able to operate in GPS denied environments while striking high value targets.

China’s rapid military modernization and development of anti-access/area denial systems have led to substantial investments by the United States and its allies in long-range precision fires, hypersonic, and advanced cruise missiles capable of breaching highly defended areas. Under the US Pacific Deterrence Initiative, more than USD 27 billion was devoted exclusively to developing precision strike systems, whereas Japan, Australia, and South Korea have made considerable acquisitions of long-range precision weapons.

The Indo-Pacific security contest has led to a multi-domain demand where the naval arms race involves heavy investments in anti-ship cruise missiles, the ground race involves procurement of extended range precision fires with 500-km range plus, and the air arms race involves development of beyond visual range air-to-air missiles and standoff air-to-ground missiles.

One of the primary constraints on the precision-guided missiles market is, the most prominent one is related to the supply chain problems that include dependency on sole sources, shortages of specific components, and limited capacities to manufacture some crucial subsystems like guidance systems, solid rocket engines, and special materials. This situation has resulted from industry consolidation observed within the defense industry during recent years.

The critical bottlenecks here involve the limited manufacturing capability of solid rocket motors by a few qualified manufacturers; the specific fabrication capability of microelectronics needed for guidance computers, and the availability of sophisticated materials such as titanium, rare earths, and alloys that go into these systems. Consequently, there is delayed product deliveries for over 24-36 months for sophisticated systems.

Export controls like the Missile Technology Control Regime, International Traffic in Arms Regulations, and bilateral licensing requirements create obstacles for market access and restrict chances for technology transfer. Such export control systems hinder the sale of advanced and precise ammunition to friendly nations, while at the same time creating complex approval systems taking around 18-36 months.

These limitations especially apply to systems that make use of high-technology guidance systems or incorporate AI systems, as well as systems with increased operational ranges that result in the need for further review, and possibly denial, since an increased risk of proliferation. Nations attempting to gain indigenous capability will be limited in terms of technology transfers, as well as Western suppliers.

AI-powered guidance systems present significant growth opportunities for AI-powered weapons, where missiles can autonomously recognize the target, coordinate their actions with other weapons, and achieve effective terminal guidance against maneuvering targets. By training the machine learning algorithms based on large-scale databases of target signatures, missiles will be able to perform the task of target recognition independently of the operators.

Swarm coordination capabilities represent one of the most promising development opportunities, allowing many missiles to coordinate their actions against defended targets, share information about sensors, and perform attack geometry to overwhelm point defenses. Using edge computing and neural networks for processing can create premium pricing options while meeting the need for independent operation.

Several market opportunities arise for designing modular architectures of missiles using open systems standards that provide flexibility in capability incorporation, customization depending on missions, and minimize lifecycle costs through standardization of components. The modular architecture enables military services to interchange seekers, warheads, and propulsion units according to mission needs without rebuilding the entire weapon system.

The advantage of modular design is that commercial technologies, such as high-end processors, sensing devices, and software, can be integrated using standard interfaces, thus creating a revenue stream through upgrades. This will also reduce reliance on proprietary systems which hinder competition and inflate costs.

Loitering munition systems have transformed the precision-guided missile market that merge a long stay within the target area with precision terminal guidance systems for less than the conventional missiles' price points. The successes recorded from the use of loitering ammunition in contemporary wars have proved their ability to attack high-value targets and their cost efficiency.

The combination of loitering munitions transcends conventional distinctions between UAVs and missiles, allowing for the inclusion of precision strike capabilities within infantry operations but also ensuring that there is the ability to terminate such attacks if the identification of targets remains in doubt. Such capabilities not only democratize precision but also create entirely new markets.

The transition of hypersonic weapons from development to operational deployment constitutes a major market shift, where the weapons can attain constant speed greater than Mach 5 along with the capability to retain guidance despite being exposed to intense heat and plasma interference. The flight trajectory and uncertainty associated with hypersonic weapons have the potential to change the dynamics of strategic deterrence completely.

The hypersonic competition spans air-breathing scramjet cruise missiles, boost-glide vehicles powered by rockets, and combined cycle propulsion vehicles which together constitute the biggest technological leap in precision strike capability since the development of cruise missiles, thus motivating huge amounts of research and new market segments for vendors.

North America held the largest regional market share, with USD 22.8 billion recorded in 2025, and was expected to exhibit a CAGR of 7.9% during the forecast period of 2024-2034. The leading position in the regional segment is driven by the fact that the USA remains the world leader in terms of its military defense procurement budget of USD 886 billion in fiscal year 2025.

The U.S. precision munition industry represents one of the most technologically advanced industrial bases for precision munition development and manufacturing worldwide. Companies like Lockheed Martin, Raytheon Technologies, and Boeing Defense lead in all types of precision munitions in their respective segments. Long-range precision fires, hypersonic missiles, and advanced air-launched weapons requiring expensive pricing with lucrative revenue from development efforts remain the focus owing to Pentagon’s interest in multi-domain and great power competition.

Significant research funding has been allocated to the region through programs like DARPA, well-developed foreign military sales organizations, and an existing integration with allied procurement programs which help in generating export dollars. The recently enacted legislation that includes multi-year procurement authorities and supplemental appropriations ensures financial stability.

The European market is growing at the highest pace with a forecasted CAGR of 10.2% during the analysis period, growing to USD 12.4 billion in 2025. The Russia-Ukraine conflict triggered the fastest increase in defense expenditure by European countries since the Cold War, as Germany, Poland, countries from Scandinavia, and Eastern Europe stepped up their purchases of precision weapons, while working on developing their production capacity independently from the USA.

The European defense industry, led by MBDA, Kongsberg, Saab, and other manufacturers,, and other national producers now have indigenous precision weapon capabilities for aerial, surface, and naval strike missions. Through initiatives such as the European Defense Fund and those under NATO, hundreds of billions are invested in collaborative development.

Asia Pacific shows robust growth at a rate of 8.8% CAGR till 2034, expected to hit USD 10.6 billion in 2025, due to growing tension between China and Taiwan, threats from North Korea, and overall regional security rivalry leading to high investments in precision strike capabilities. The anti-access/area denial capabilities along with hypersonic weapon development in China have compelled Japan, South Korea, Australia, and India to invest heavily in their capabilities.

Japan’s shift in defense doctrine to develop counterstrike capabilities will entail huge investments in precision weapons including hundreds of Tomahawks along with indigenous standoff weapons. South Korea will require large inventories of precision ballistic and cruise missiles for its Three-Axis Defense, whereas India will develop its BrahMos supersonic cruise missile along with its indigenous hypersonic systems.

The Air-to-Surface Missiles segment holds the largest market share (36%), valued at USD 17.4 billion in 2025. of USD 17.4 billion by 2025 and a CAGR of 8.7% until 2034. The segment is defined using tactical to long-range cruise missiles for attacking targets using precise strikes. These include notable projects such as the JASSM-ER, Storm Shadow, and Taurus.

Anti-Tank Guided Missiles represent the fastest-growing major missile category, growing at 12.4% CAGR to reach USD 7.8 billion in 2025 due to high demand for use in Ukraine warfare and rearmament for the NATO force. Some of the notable systems include Javelin, NLAW, and Spike which proved their effectiveness in combating armor.

Another fast-growing emerging class of guided missiles is Loitering Munitions at 18.6% CAGR from USD 2.8 billion in 2025 shifting from specialty applications to become common tactical strike weapons.

The Multi-Mode Guidance Systems lead the high-end market segments, accounting for 42% of the precision guided weapons revenue share due to necessity of resistance against electronic warfare and all-weather capability. GPS/INS Guided weapons hold maximum market volume share of 38%, providing cost-efficient solutions for permissive environment.

Artificial Intelligence-Enhanced Autonomous Targeting is the fastest-growing technology segment, with a CAGR of 24%. shifting focus from development stage to operational stage with increasing price premium on autonomous features.

Airborne Platforms constitute the major segment with 43% market share worth USD 20.7 billion in 2025, owing to dominance of air power in precision strike strategy and higher unit prices of air-launched weapons. Naval Platforms contribute 28% of the market share owing to investments in anti-ship missiles and submarine-launched land-attack technology.

Ground-Based Systems are witnessing rapid growth at a CAGR of 11.8%, mainly attributed to long range precision fires systems and advancements in mobile air defense platforms.

The global precision-guided missiles market is highly concentrated due to dominance of well-known defense prime contractors that occupy around 65-72% of the global market in terms of market value based on their diversified product range of different types of guided weapons. Competitive advantages of leading companies include advanced guidance system, multi-mode functionality, combat readiness and reliability, integration with different platforms, relations with export markets, as well as technological developments against new threats.

The competitive landscape is evolving as technology companies that specialize in artificial intelligence, commercial drone makers, and materials companies venturing into the development of precision munitions, especially loitering munitions with AI-based guidance using commercial technologies whose advancements outpaced military development schedules.

April 2026: Lockheed Martin wins USD 4.2 billion multiyear contract for the JASSM-ER long-range cruise missile, marking the biggest order of precision weapons for the company ever, as Air Force steps up Pacific Theater deterrence capability, and international orders continue to flow in.

March 2026: MBDA successfully tests networked Spear 3 mini-cruise missiles working together in cooperative engagement against defended targets with coordination among missiles using target data and carrying out simultaneous terminal strikes, securing initial USD 1.8 billion production contract from UK Ministry of Defence.

February 2026: Raytheon Technologies finished expanding their production facilities for hypersonic weapons in Arizona, making possible production of air-launched rapid reaction weapons for US Air Force as well as setting the foundation for exports depending on license approvals.

January 2026: RAFAEL Advanced Defense Systems revealed their new AI-integrated Spike version that utilizes autonomous target recognition capability with 97% accuracy rate in detecting armored vehicles in tests, leading to first contract worth USD 850 million by European NATO allies.

December 2025: Kongsberg Defence received record orders totaling to USD 3.4 billion of the Naval Strike Missiles from nine allied countries in a single year, the highest ever recorded annual NSM procurement amid increased focus on anti-ship precision attacks.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.