Share this link via:

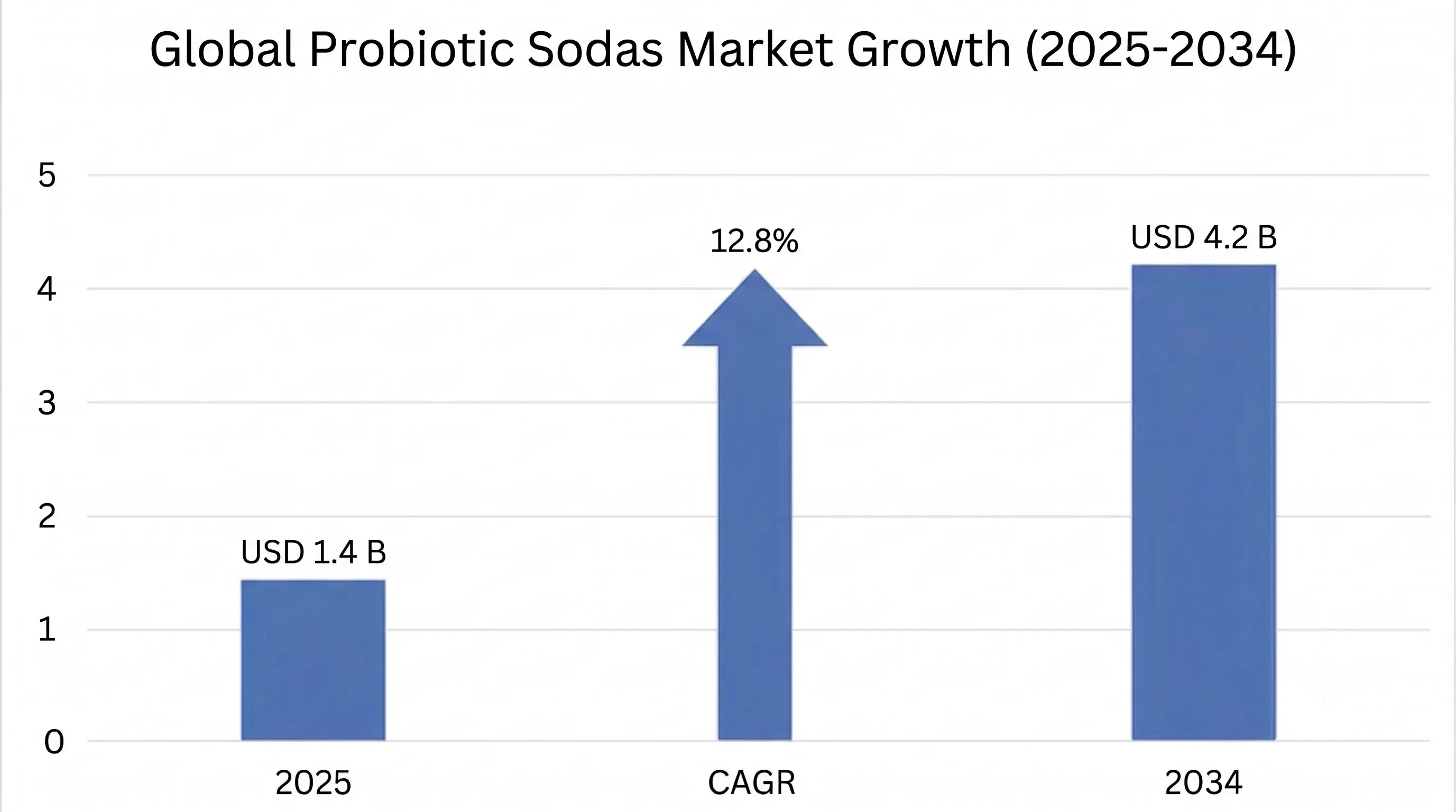

The global probiotic sodas market size was valued at USD 1.4 billion in 2025 and is projected to reach USD 1.6 billion in 2026, expanding to USD 4.2 billion by 2034, growing at a CAGR of 12.8% during the forecast period (2026-2034).

Probiotic sodas represent a new generation of functional nutrition beverages that combine the appeal of carbonated drinks with probiotic benefits., where familiar and refreshing carbonated soda formats are loaded with live gut-friendly microorganisms, mimicking the sensory and social experience of carbonated soft drinks, but with positive digestive health and wellness benefits. This is a rapidly growing segment that addresses a major consumer need: the desire of health-conscious consumers for something that is not just a paltry substitute for the negative nutritional impact of sugar-based beverages but also provides real functional benefits.

The scientific foundation of probiotic sodas has advanced significantly with the identification of new and improved strains, especially ones that are spore-forming and more stable in the carbonated beverage environment like Bacillus coagulans and Bacillus subtilis. Whereas traditional vegetative probiotic strains rapidly lose viability when exposed to low pH, carbonation pressure, and ambient temperature storage, spore-forming probiotics exhibit survival due to protective endospore mechanisms to ensure clinically relevant CFU levels reach the intestinal tract during manufacturing, distribution, and storage.

Today’s probiotic soda brands combine cutting-edge beverage science such as microencapsulation systems, pH optimization, controlled levels of carbonation and innovative packaging techniques to preserve the viability of the probiotics and provide a flavor that closely mimics popular conventional soda varieties like cola, root beer, fruit punch and citrus. The “stealth health” strategy allows the entire sod sector to be replaced in a seamless and transparent way without the need to alter the taste of the product or the drinking experience in social settings, thereby opening the door to a larger market than just the dedicated health food consumer: the mainstream consumer looking for a functional soda when they want a soda.

It’s not just about niche positioning for functional beverages; it represents a direct challenge to the USD 350 billion global carbonated beverage market, taking a bite out of the market for empty calories among health-conscious consumers and growing the number of beverage consumption occasions through functional beverage positioning that turns refreshment into proactive health support. The category enjoys strong cultural momentum – as people increasingly consider gut health, they have seen a reduction in their appetite for conventional soft drinks, are looking for products with clean labels, and are prepared to pay high price premiums for functional authenticity.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 1.4 Billion |

| Forecast Value | USD 4.2 Billion |

| CAGR | 12.8% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Product Type, Probiotic Strain, Formulation, Distribution Channel, Target Demographics |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Olipop PBC, Poppi, GT’s Living Foods, Health-Ade Kombucha, KeVita Inc., Culture Pop, Remedy Drinks, Humm Kombucha |

Get more details on this report - Request Free Sample

The primary structural driver of the probiotic soda market is is the paradigm shift of the awareness and understanding of gut health and the microbiome among the general population, which has become a part of their lifestyle rather than a medical niche. Evidence from scientific studies linking the diversity of microbes in the gut with systemic health benefits, such as immunity, mental health via the gut-brain connection, increased metabolic efficiency, and prevention of chronic disease, has excited consumers to consider taking daily probiotics via simple, palatable, and convenient products.

The fact that approximately 90% of serotonin is synthesized in the gastrointestinal tract and that gut microbial composition plays a direct role in neurotransmitter synthesis has particularly resonated with consumers experiencing chronic stress, anxiety and mood dysregulation. Consumer research shows that in 2025, 71% of adults in developed markets are aware of the health benefits of the gut microbiome, up from 38% in 2019, highlighting a significant shift toward preventive nutrition approaches.

Probiotic sodas help address compliance issues associated with traditional probiotic supplements, as probiotic capsules have an average adherence rate of 6-months of only 39%, while consumers who switch to daily probiotic beverage use have an adherence rate of 64%. This enhanced compliance benefit makes probiotic sodas a better delivery platform than conventional probiotic supplement products that are often abandoned by consumers because of their inconvenience or forgetfulness.

As consumers become increasingly aware of the health effects of added sugars, concerns about artificial ingredients, and government regulations, such as sugar taxes, drive a structural market opportunity for probiotic soft drinks because they can be seen as increasingly functional alternatives. Conventional soda sales have been falling at a faster rate in developed markets, where per capita consumption dropped 24% for the 2000-2025 period; especially among millennial and Gen Z consumers, who are actively looking for drinks that deliver health benefits.

Probiotic sodas solve the basic consumer conundrum of wanting social fun, the taste and the carbonation of traditional sodas, while also striving to achieve health goals that are actively being impeded by traditional soda. The category allows consumers to seamlessly switch between popular flavor profiles, like cola, root beer and fruit varieties and avoids unnecessary refined sugars, artificial additives and high fructose corn syrup which conventional soda is known for and what would otherwise be the subject of health concerns.

Finally, natural sweetener systems that couple stevia, monk fruit, and erythritol allow for probiotic sodas to be created with authentic flavor at a much lower sugar content, typically 2-5 grams per serving compared with 35-45 grams in conventional sodas. These products are gaining traction among consumers with diabetes and those seeking lower-sugar alternatives are demanding a dramatic reduction in sugar, and at the same time, it offers flavor satisfaction that will enable continued product use.

One of the key challenges facing the probiotic soda market, the most important is the challenge of having sufficient levels of live probiotics through manufacturing, distribution, retail storage, and end-user storage, because probiotic organisms face significant viability challenges during manufacturing, distribution, and storage in terms of heat exposure, interaction with oxygen, pH change, carbon dioxide pressure, and shelf-life duration. The high carbon dioxide pressure, acidic nature, and low water activity in carbonated beverages make it extremely difficult to ensure viable probiotics in these beverages.

In many markets where there are regulations on probiotic foods, it is mandatory that probiotic foods maintain minimum levels of one billion CFUs per serving throughout the product lifetime and not just until the manufacturing period, and such stringent standards create several difficulties for manufacturers of these foods. It is reported that only 70% of probiotic beverages can maintain the label viable counts throughout their shelf-life period.

The premium pricing of probiotic beverages limits their mass-market adoption because most consumers are very sensitive when it comes to spending money on such products. The average cost of a probiotic beverage is USD 3.20 per bottle, and it is not affordable for most people to purchase regularly.

Inexpensive manufacturing of products involving probiotic bacteria, use of natural sugar alternatives, high quality packaging, and special equipment make expensive pricing mandatory, thus creating a core conflict of delivering functional benefits versus meeting the affordable mass market requirement.

The development of synbiotic probiotic beverages, which will utilize live cultures along with prebiotics like inulin, resistant starch, and oligosaccharides that feed specifically on probiotics, presents a huge potential market for business as they have better results in terms of gut health compared to simple probiotics since they will be supplying nutrition to both the new and native beneficial gut bacteria.

Fiber’s addition makes it possible for companies to claim two benefits for synbiotic beverages related to improved digestive function and diversity of the microflora by overcoming the deficiency of fiber consumption among the public who take less than 50% of their recommended dietary amount of fiber. Addition of 5-8 grams of fiber per bottle makes them full-fledged digestive beverages.

Significant growth opportunities exist for probiotic soda brands to expand from niche health-food channels into mainstream retail outlets, such as grocery stores, mass merchants, and even convenience stores where increased consumer exposure will encourage consumer trial and acceptance of products. Probiotic sodas on mainline retail shelves will help validate the functional beverage concept among general consumers and allow economies of scale in terms of pricing.

Major retailers such as Walmart, Target, and Kroger have increased their space allocation for probiotic sodas, with designated functional drink categories generating 2.8 times more sales per foot than regular carbonated drinks in equal locations.

The probiotic soda market is increasingly favoring nostalgic, classic soda flavors that replicate familiar taste profiles of conventional sodas like cola, root beer, orange cream and grape soda, rather than those of botanical or aggressively fermented flavors. Its strategic development allows “stealth health” positioning where the consumer can still enjoy the taste of the product he or she is used to while enjoying added functional benefits, thus opening a wide range of addressable market opportunities, including those of dedicated health food consumers.

Leading probiotic soda brands invest heavily in flavor development to replicate the taste of the original product, whether that's a cola or a lemonade, but they also throw in the probiotic benefits to ensure that their beverages are fulfilling both a nostalgic desire and a health objective.

Advances in spore-forming probiotic strains and packaging technologies, along with better packaging options, will enable us to create probiotic sodas that have shelf-life stability and remain viable even at room temperature, thereby eliminating cold-chain storage and transportation costs, which amount to reductions of about 25-35%.

North America dominated the market, generating USD 580 million in revenue in 2025, while the CAGR stood at 12.2%, predicted up until 2034. Market dominance is due to a developed health & wellness culture, efficient distribution channels for natural products, and presence of some innovative functional beverages brands that have grown from startups to become successful players within the region. In terms of country-level performance, the U.S. held an 86% market share within North America, supported by VC funding above USD 650 million in probiotic beverages from 2022-2025.

The region benefits from a well-established kombucha culture that has built up the required infrastructure for consumer education and retail distribution channels to be later utilized by probiotic soda producers. Companies such as Olipop and Poppi have demonstrated strong commercial success by becoming successful across retail markets nationally.

Asia Pacific was valued at USD 285 million in 2025 and is projected to grow at a CAGR of 15.1% through 2034. The market growth will be facilitated due to the high level of cultural awareness for fermented products, including drinks, which provides an inherent interest among consumers in probiotic sodas. Japan represents the most mature market in the region.

China emerges as the biggest opportunity for growth in the region, owing to the health awareness among the expanding middle class, the advanced e-commerce infrastructure which allows brands to connect directly with consumers, and government emphasis on preventive nutrition.

Europe represented an advanced market valued at USD 295 million in 2025 at an 11.8% CAGR till 2034 with high clean-label regulations, preference for organic certification, and sustainability. Countries such as Germany, the United Kingdom, and Netherlands are leading consumers in the region due to the existence of natural products retail system.

The regulatory frameworks within Europe concerning health claims on probiotics allow brands that can prove the benefits of their products clinically to gain a market advantage by distinguishing themselves on quality and justifying high prices.

Fruit-Based Probiotic Sodas held the largest market share of 38% with a market valuation of USD 532 million in 2025 by offering broad consumer appeal and a low barrier to trial., coupled with their natural tanginess resulting from fermentation processes. The classical cola and root beer alternative options have the highest growth potential, growing at a CAGR of 16.8%, which will help attract customers looking for alternatives to conventional soda products.

Multi-Strain Blends held the largest market share with 42% market share, offering a wide variety of microbial species that will attract customers looking for an all-round solution to their digestive problems. Spore-Forming Probiotics have a 28% market share and experience the highest CAGR at 18.2% due to better stability characteristics and ease of distribution through packaging solutions. Lactobacillus strains have a stable market share of 22%.

The Supermarkets & Hypermarkets have the largest channel share with 41%, because of efficient mainstream retailing and functional merchandising of beverages. Specialty Health Stores accounted for 26% of the market due to their role in product discovery and staff-led recommendations. and health-focused merchandising. Online Retail comes in third place with 19% market share but is showing the fastest growth rate of 21.4% CAGR.

The Millennials along with Generation Z consume 58% of the goods due to their concern about health, influence of social media, and their desire to pay more for functional benefits. The Market Share for Health-Conscious Adults is 31%, who have demonstrated the maximum per capita consumption and brand loyalty. The market share of Athletes and Fitness enthusiasts is 11%.

The probiotic soda market is highly fragmented since the leading eight players account for only about 42-48% of the total market size. The nature of the product and the relatively low market entry barriers due to its innovation make the market highly fragmented. Competitive advantages in probiotic sodas include strain efficacy and evidence base, naturalness of flavors, distribution channels, and sustainability.

Leading brands differentiate themselves through advanced flavor development, robust probiotic stability, and strong digital marketing strategies., and by their aggressive online marketing campaigns, which target health-oriented millennials and members of Generation Z via social media sites.

April 2026: Olipop PBC raised Series D funding of USD 350 million at a valuation of USD 2.2 billion. The raised money is expected to be used for company expansion overseas as well as for conducting further research in conjunction with top universities regarding probiotics.

March 2026: Poppi was acquired by a major beverage company in a deal worth USD 1.7 billion. This transaction shows an ongoing trend of industry consolidation of independent successful probiotic soda companies.

February 2026: Living Foods by GT developed a clinical quality probiotic soda range using strains with proven efficiency in treating certain digestion-related issues, marketing its products both to the healthcare professionals as well as to regular consumers.

January 2026: KeVita Inc. offered ambient stable formulations for probiotics based on Bacillus coagulans strains that allowed it to use traditional distribution networks without a need for refrigeration and lower prices by 18%.

December 2025: Health-Ade Kombucha added probiotic sodas with monk fruit-based and prebiotic fiber-containing zero-sugar formulations to cater to ketogenic and diabetes populations.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

01 Jul 2026

Intellectual Market Insights Research © 2026. All rights reserved.