Share this link via:

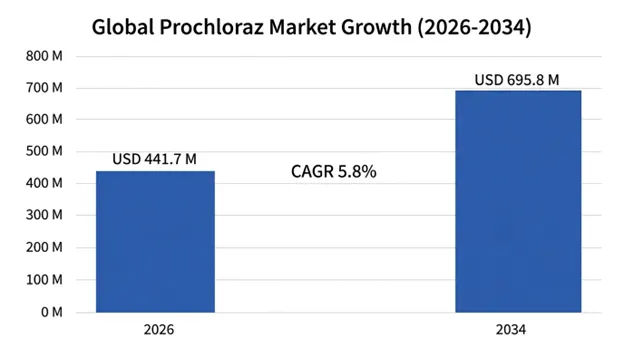

The global prochloraz market was valued at USD 418.3 million in 2025 and is projected to reach USD 441.7 million in 2026, expanding to USD 695.8 million by 2034, growing at a CAGR of 5.8% during the forecast period (2026-2034).

Prochloraz is an imidazole fungicide with a broad spectrum and is included in the group of ergosterol biosynthesis inhibitors (EBIs), being a sterol 14α-demethylase inhibitor which inhibits fungal membrane synthesis by preventing ergosterol synthesis. This mode of action provides both protective and curative effects against a variety of economically important pathogens such as Fusarium, Alternaria, Botrytis cinerea, Septoria tritici, and Penicillium.

Prochloraz works through inhibition of the enzyme sterol 14α-demethylase, which is a cytochrome P450 dependent enzyme involved in the ergosterol biosynthesis process in the cell membranes of fungi. Such interference results in the formation of sterol intermediates that are harmful to cells while also leading to ergosterol depletion, resulting in malfunctioning of the cell membrane, inhibition of mycelium growth, decreased spore production and eventually killing the fungal cells. Prochloraz has systemic and translaminar characteristics, thus allowing redistribution within plant tissues for protective action on non-sprayed parts as well as curative effects.

The active substance demonstrates favorable physicochemical characteristics such as adequate solubility in water for good absorption and transportability, proper lipophilicity for good penetrance of the cuticle, and chemical stability in different pH levels.

In cereals production systems, prochloraz is an important fungicide used to control Fusarium head blight in wheat and barley, Septoria leaf blotch complex, and different types of crown rots and root rots affecting yield and grain quality. The effectiveness of the compound against Fusarium pathogens is especially important considering the danger of yield reduction as well as mycotoxin contamination. Indeed, deoxynivalenol and other trichothecene mycotoxins make grains unsuitable for food and feed purposes.

Horticultural uses can be divided into field applications and post-harvest treatments. Field applications include the use of prochloraz for the control of anthracnose, scabs, alternaria leaf spots, and powdery mildews in fruit and vegetable crops. Post-harvest applications represent a premium use since prochloraz helps prevent storage rots in citrus, bananas, stone fruits, and tropical fruits when stored for long periods and transported internationally, hence higher prices because of the premium nature of these commodities.

Current formulations of prochloraz have come a long way from conventional emulsifiable concentrates to modern suspension concentrates, microencapsulated formulations, and formulations for seed treatments. These advanced formulations improve environmental safety and better biological efficiency through increased rainfastness, prolonged residual action, and low risk of operator exposure. The microencapsulation technique ensures that the formulation releases the pesticide slowly to ensure sustained action.

Seed treatments use modern polymer-based coating technology, which allows for consistent application of prochloraz on the surface of the seed, compatibility with other seed applied compounds such as insecticides and microorganisms, and adhesion during the planting process. Seed treatment applications require 70–80% less active ingredient of the active ingredient than the foliar application technique.

| Report Coverage | Details |

|---|---|

| Base Year | 2026 |

| Base Year Value | USD 418.3 Million |

| Forecast Value | USD 695.8 Million |

| CAGR | 5.8% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Latin America |

| Segments Covered | By Formulation Type, Application Method, Crop Type, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Denmark, China, India, Japan, Australia, Brazil, Argentina, South Africa, Thailand |

| Key Market Playes | Syngenta AG, BASF SE, Bayer CropScience, FMC Corporation, Nufarm Limited, UPL Limited, ADAMA Agricultural Solutions |

Get more details on this report - Request Free Sample

The primary factor driving demand for prochloraz is the pressing requirement to maximize the output from agriculture to cope with increasing global food needs. In light of the estimated world population of 8.5 billion by 2030, there will be a great necessity to boost cereals output to ensure food security in wheat, rice, and barley where fungal infection is a major factor limiting crop yield. The loss of wheat and barley production due to fusarium head blight alone is estimated at more than USD 3 billion annually globally.

The increased intensity in the production systems of cereals, due to the lack of land as well as financial issues, results in higher levels of disease pressure. This creates conditions where multi-fungicide application programs become economically viable. The broad spectrum of action as well as its compatibility with other fungicides makes prochloraz a critical component in resistance management programs.

The expanding global fresh produce industry, estimated to be worth USD 298 billion in 2025, growing at 6.2% per year, poses a high demand for fungicides that will help retain the quality of fresh produce during long periods of storage and international shipment. Prochloraz is widely valued for its effectiveness in protecting against common post-harvest pathogens such as the Penicillium in citrus, Colletotrichum in tropical fruits, and Botrytis cinerea on many different crops.

This product enjoys higher pricing between USD 8-15 per kilogram of the active substance as opposed to USD 3-6 for field application because of the higher costs associated with commodities in protected crops and the need for higher levels of effectiveness. Prochloraz-based products have become widely used in countries that export fruits such as Ecuador, Philippines, Chile and South Africa.

The primary restraint affecting the prochloraz market lies in the regulation of the substance in the European Union due to a full risk assessment performed by the European Food Safety Authority, which found that the fungicide had endocrine disrupting properties, resulting in refusal to renew the approval of the product under Regulation (EC) 1107/2009. The result of the regulatory action is the loss of an important market with sales volume of about USD 95-115 million per year.

The approach adopted by the EU regulators influences international market forces because exporters are required to either abstain from using prochloraz on crops destined for the EU or apply the pesticide in such a way that the residues fall within the EU MRLs. This leads to market segmentation whereby a particular crop would need to have different fungicide regimes depending on the target markets.

Resistance issues to Prochloraz are well-known in various economically significant pathogens due to the selection of reduced susceptibility by the intensive use of this fungicide. The populations of the Botrytis cinerea fungus affecting valuable horticulture crops exhibit resistance in various agricultural locations, and therefore the need for integration with other fungicide groups arises. Likewise, Penicillium species responsible for post-harvest citrus rot have exhibited progressive sensitivity changes due to its historical usage.

The requirements for resistance management add complexity and costs due to rotation with other fungicides, decreased applications, and surveillance systems. Although industry stewardship programs tackle the problem by providing resistance management practices, the requirement for an integrated approach restricts the market from growing further.

Significant growth potential exists in the formulation of prochloraz products which solve the environmental and safety problems but still retain or enhance their biological efficacy. The use of microencapsulation techniques helps reduce the exposure of the active substance to the environment initially, thus prolonging its effect.

This allows for the development of formulations that can be sold at a higher price than standard formulations by 25-40% while addressing more strict environmental and safety regulations.

The development of nanotechnology-based delivery systems offers an interesting area for targeted delivery of the fungicide, which would not only enhance the uptake and translocation but also reduce the amount of the active substance required.

There is an opportunity to develop new combination products that can incorporate prochloraz with fungicides having different modes of action to create differentiated products which would have premium prices. Combination of prochloraz with fungicides such as SDHIs, strobilurins and multisites would give a wider coverage than products based on a single active ingredient.

The biological integration possibilities consist of the combination of prochloraz with beneficial microorganisms such as Bacillus species and Trichoderma species that contribute to disease suppression through a complementary effect as well as the achievement of sustainable agricultural goals.

The introduction of precision agriculture technology such as variable rate applicators, disease forecasting based on weather, and drones as applicators is changing the dynamics of fungicide application and hence its demand. Disease forecasting systems allow farmers to apply the fungicides at optimal times when infection rates are highest, and thus reduce the number of applications without compromising efficacy.

Drone-based application systems require products whose formulation allows for application by drones, which are products whose viscosity and droplets can be controlled. This creates an opportunity for formulating fungicide products to suit this method of application.

One of the latest trends that have influenced the prochloraz market is the trend towards adopting seed treatment applications. This is since seed treatments offer protection that utilize relatively fewer active ingredients compared to foliar applications to protect crops, thus fulfilling environmental stewardship goals. The use of advanced polymer coatings helps in delivering the right amount of active ingredients.

The seed treatment market offers better growth opportunities, having a CAGR of 8.4% until 2034, due to its ability to simplify application procedures for farmers, as well as limiting their exposure. Farmers prefer seed treatments since they can be applied alongside other products like insecticides and biologicals.

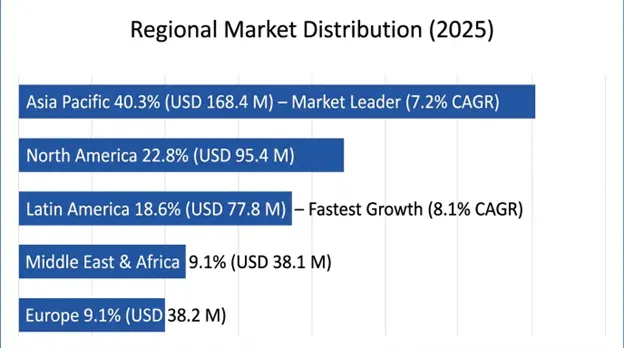

Asia Pacific leads the market, valued at of USD 168.4 million in 2025 accounting for 40.3% of the market value globally, registering a CAGR of 7.2% from 2026-2034. The regional dominance is a result of the huge agricultural landscape that includes large-scale cultivation of rice, wheat, and horticulture crops, resulting in high fungicides demand. China accounts for 45% of the regional market value due to local manufacturing and consumption of fungicides, while India emerges as the fastest-growing region due to modernization of agriculture and commercial farming.

The region also boasts of favorable regulations on active ingredients, low manufacturing cost, and the use of improved farm practices by the commercially focused farmers. Major rice-producing regions in China, India, Thailand, and Vietnam ensure steady demand for fungicides to control blast and sheath blight, while expanding fruits production ensures post-harvest fungicide use.

Latin America is the fastest-growing regional market with expected CAGR of 8.1% from 2024-2034 due to the development of agriculture focused on exports in Brazil, Argentina, Chile, and Colombia. High disease pressure in Latin America owing to its tropical and subtropical climatic zones demands intensive use of fungicides, while the development of soybeans, fruits, and vegetables exports calls for disease management.

Brazil leads the regional market with share of 52%, due to huge production of soybeans and corn in which prochloraz acts against Asian soybean rust and different leaf spot diseases. Moreover, Brazil’s fruit export market develops fast with export of citrus and tropical fruits in need of preserving their quality by post-harvest fungicides.

The European market is projected to decline to USD 38.2 million by 2025, accounting for 9.1% of total global market share owing to gradual regulatory restrictions imposed in EU member countries. The United Kingdom holds the biggest European market following its regulation independence after Brexit, although Denmark, being an EU member country, has kept a small market share due to derogations.

This regulatory landscape is still developing, which can lead to more regulations in the future, thus creating uncertainty and restricting investments in product development and market expansion. The use of products in cereals to prevent Fusarium head blight still holds market significance for managing mycotoxins.

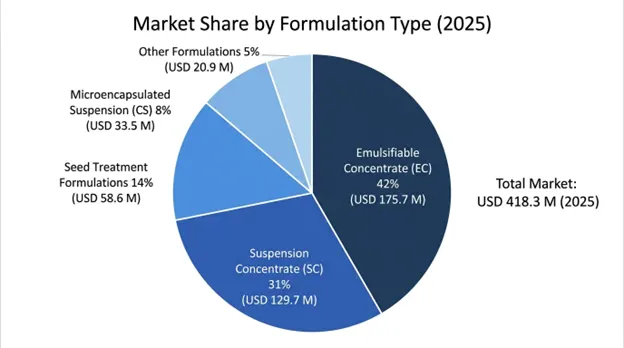

The Emulsifiable Concentrate (EC) formulations have the highest market share at 42%, valued at USD 175.7 million in 2025. These formulations are the conventional type of formulations used for foliar application in both cereals and horticultural crops. This formulation is preferred due to its ready-to-use formulation, ease of manufacture, compatibility with tank mixers, and farmer awareness; however, the adoption of this formulation is limited due to its environmental impact and safety.

The Suspension Concentrate (SC) formulations account for 31% market share worth USD 129.7 million in 2025. The segment grows at a CAGR of 7.8% during 2026-2034. This technology is primarily used in seed treatment applications since uniform coverage, high adhesion, and compatibility with automatic seed treating machines are some key criteria to consider while choosing seed treatment formulations. SC formulations offer better environmental performance than EC formulations.

The Foliar Spray applications form the biggest segment with 48% market share that includes disease management programs in cereals, horticultural field applications, and rice blast control wherein the application of prochloraz in the canopy results in both protective and curative disease control. The performance of this segment is highly correlated to seasonal disease pressure levels resulting in year-on-year variability due to favorable weather conditions for fungi formation.

The Post-Harvest Treatment has a market share of 26% worth USD 108.8 million in 2025 and forms the most valuable segment per kilogram. Premium pricing is supported by the high value of commodity treated and high efficacy required to maintain export standards. This segment exhibits consistent growth because of growth in global fresh produce trade and improvements in cold chain infrastructures.

The Seed Treatment applications form the third largest segment in the market with a market share of 19%. The segment has the fastest compound annual growth rate of 8.4% during 2026-2034. Growth is attributed to farmers’ preference for easy application, environmental reasons, and application in combination with seed treatment programs.

Cereals & Grains dominate crop segmentation with 44% market share, valued around USD 184.1 million in 2025, and it shows prochloraz is already pretty established in wheat barley and rice disease management programs across the globe. This segment is supported by extensive cultivated acreage, plus those proven economic returns, from yield protection.

Fruits & Vegetables account for 35% of market share in 2025 worth USD 146.4 million, including both field and post-harvest uses. The category has high prices because of high value of crops and quality standards required for domestic and export markets. Post-harvest usage is the most profitable part of the category.

The Oilseeds & Pulses category accounts for 16% of the market share and is dominated by the soybean application in Latin America where prochloraz is used for controlling Asian soybean rust and various leaf spots.

The global prochloraz market demonstrates a moderate degree of concentration in terms of its formulations with multinational agrichemical companies holding dominant positions in the market on account of their advanced formulation technologies, distribution networks, and crop protection solutions. Syngenta AG, BASF SE, and Bayer CropScience together hold around 35-42% share of the global market based on branded products.

Generic competition has increased greatly after patents expiry, with Chinese manufacturers such as Shandong Sino-Agri United Biotechnology Company and Jiangsu Yangnong Chemical Group manufacturing technical prochloraz at competitive prices to supply the international formulation market. This has led to reduced margins in commodity formulations while creating room for differentiation using superior formulation technology and service packages.

Competitive differentiation is driven by formulation innovation such as micro-encapsulation and controlled release systems, resistance management, comprehensive technical services and development of proprietary mixture products containing prochloraz in combination with other active substances.

Market positioning varies across regions where multinational corporations emphasize premium formulations and a complete crop protection program, whereas regional companies target cost-effectiveness and knowledge of the local markets in developing agricultural economies.

Recent Developments

April 2026: Prochloraz-tebuconazole microcapsule combination fungicide was introduced by Syngenta AG for use in cereals in Brazil and Argentina, showing 22% higher control of Fusarium head blight than any standard product, and at 15% lower rate due to controlled release technology.

March 2026: BASF SE was granted clearance in India for a novel prochloraz suspension concentrate fungicide formulation designed for spraying by drones on rice crops, providing equal disease control against blast and sheath blight with reduced water requirement by 35%.

February 2026: UPL Limited capacity expansion for manufacture of prochloraz in India through setting up of a new technical synthesis facility valued at USD 28 million to guarantee availability for the Asia Pacific and Middle East markets through reducing dependency on Chinese technical sources.

January 2026: Nufarm Limited made a strategic partnership with a major biological control firm to develop prochloraz-biological fungicides for disease management in high-value horticultural crops with the objective of lowering fungicide use by 30%.

December 2025: FMC Corporation successfully acquired the company which developed proprietary prochloraz wax coating formulations, allowing the company access to treatments with extended residual activity showing 40% longer lasting protection in citrus and stone fruits.

November 2025: Bayer CropScience initiated Phase III registration trials on a new prochloraz plus biological seed treatment for the control of soil-borne diseases in wheat and barley with the same efficacy as conventional chemical seed treatment but with an improved environmental profile.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

21 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.