Share this link via:

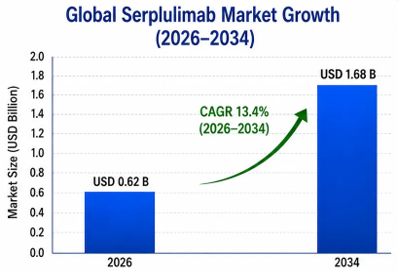

The global serplulimab market size was valued at USD 520 million in 2025 and is projected to reach USD 615 million in 2026, expanding to USD 1.68 billion by 2034, growing at a CAGR of 13.4% during the forecast period (2026-2034).

Serplulimab is an innovative recombinant humanized monoclonal antibody against programmed death-1 that has completely changed the treatment modalities of extensive stage small cell lung cancer and several solid tumors because of its unique mechanism of action of immune checkpoint inhibition. This medicine is manufactured by Shanghai Henlius Biotech, Inc. and acts by inhibiting the binding of programmed death-1 (PD-1) receptors on T cells to their ligands, PD-L1 and PD-L2, present on tumor and antigen presenting cells. Thus, it blocks the immunosuppression caused by programmed death-1/PD-L1 interaction and restores the normal function of the immune system in fighting the tumors. The unique features of serplulimab include its high affinity, subnanomolar dissociation constants and reduced antibody dependent cell mediated cytotoxicity.

The commercial potential of serplulimab is not only associated with the compound’s position as an innovative anti-PD-1 inhibitor but also lies in its pioneering nature as the first approved first-line agent for extensive-stage small cell lung cancer – a notoriously deadly form of the disease for which there were no effective treatment solutions and whose patients had very poor prognosis. According to results of the groundbreaking ASTRUM-005 Phase III trial, the median overall survival was 15.4 months in patients who received serplulimab in addition to carboplatin and etoposide versus 10.9 months for chemotherapy alone, translating to 38% lower risk of mortality. Such impressive results have made serplulimab a key player in oncology algorithms and at the same time opened opportunities for development in other solid tumors, such as esophageal squamous cell carcinoma, gastric cancer, and microsatellite instability-high solid tumors.

The market encompasses the entire therapeutic ecosystem that include revenues from the pharmaceutical products, the companion diagnostics developed for patient selection based on the biomarkers, the combination therapies that consist of chemotherapy and targeted therapies, as well as the oncology-specific support services needed for immune checkpoint inhibitors.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 520 Million |

| Forecast Value | USD 1.68 Billion |

| CAGR | 13.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Europe |

| Segments Covered | By Indication, Therapy Type, Line of Therapy, Distribution Channel |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, UK, Germany, France, Italy, Spain, China, Japan, India, South Korea, Australia, Brazil, Mexico, UAE, Saudi Arabia |

| Key Market Playes | Shanghai Henlius Biotech, Fosun Pharma, KGbio, Elevar Therapeutics |

Get more details on this report - Request Free Sample

A key market driver for serplulimab is its outstanding clinical trial success. for ES-SCLC. Small cell lung cancer (SCLC) is a form of cancer that has very few treatments and an extremely high mortality rate. Being the first PD-1 inhibitor approved for ES-SCLC, serplulimab has carved out a distinct niche in the immunotherapy market.

The key ASTRUM-005 study showed very promising survival effects for the use of serplulimab alongside carboplatin and etoposide chemotherapy. Patients receiving combination therapy had significantly better overall survival rates compared to those who were under treatment only by chemotherapy, demonstrating the efficacy of the drug in providing better outcomes among patients who had a poor therapeutic history in the past.

Along with the enhancement in survival rates, serplulimab also provides an acceptable safety profile comparable to other PD-1 inhibitors and fits well into the current regimen. The efficacy, tolerability, and growing clinical acceptance of serplulimab are driving market growth.

A key factor that differentiates serplulimab among the existing Western checkpoint inhibitors in terms of structural growth is the fact that the drug is strategically priced to ensure broad access to patients in developing healthcare markets, while remaining commercially viable due to volume pricing. The inclusion of serplulimab in the National Reimbursement Drug List after the negotiation of lower prices in China led to patient cost reduction of the drug by about 68%, relative to imported PD-1 inhibitors, making it cheaper to use widely across hospitals.

Competitive pricing is supported by low-cost manufacturing in the home country with capacity for producing on a large commercial scale, efficient distribution via Henlius’s commercial integration, and clinical support services via hospital partnerships. The penetration marketing strategy focusing on cost effectiveness over high pricing is in line with the objectives of healthcare policies in various emerging markets with similar healthcare budgetary challenges.

Economic differentiation provides sustainable competitive advantages in terms of pricing in Southeast Asia, Latin America, and the Middle East, where healthcare systems suffer from budgetary challenges like those in China. The combination of high clinical efficiency and affordable prices of serplulimab makes it highly attractive when compared to other Western checkpoint inhibitors sold at higher prices.

Intense competition may constrain the market growth potential of serplulimab include the formidable market presence of existing checkpoint inhibitors such as pembrolizumab, nivolumab, atezolizumab, and durvalumab that account for about 78% of the total market revenue of immune checkpoint inhibitors through their wide indication’s portfolio, real-world data on safety, and well-developed programs aimed at educating physicians and patients. The drugs mentioned above have decades of history in clinical practice, approval for several tumor types based on strong evidence from Phase III studies, guidelines endorsement by leading oncology societies, and integration into healthcare systems.

Especially in Western markets, oncologists show a strong preference for known checkpoint inhibitors that have proven themselves to be efficacious and safe; hence, serplulimab needs to prove its superiority either in terms of efficacy or economics to motivate oncologists to switch their prescription protocol from their present practice. Approval of the drug in the United States and Europe requires comprehensive clinical data packages that may involve further Phase III studies for the Western population segment.

Transformational market potential of serplulimab can be realized through effective regulatory approval and product launch in the North American and European markets, where the annual cost per patient for using checkpoint inhibitors ranges from USD 125,000-185,000, against USD 12,000-18,000 in China post reimbursement discussion. A conservative market penetration of 3-5% in large populations of patients suffering from extensive-stage small cell lung cancer and other indications is expected to contribute financially to the existing Asia market performance.

Strategic alliances with reputable pharmaceutical firms with Western market commercial capability, experience, and knowledge, along with expertise in oncology specialists, serve as channels that allow quick market entry without the need to create independent commercial organization structures. The alliance with Elevar Therapeutics for the commercialization of its products in North America is an example of this strategy.

The development of advanced regulatory bridging techniques that make use of clinical data from Asians for approval in the West without compromising on regulatory agency requirements for heterogeneity and generalizability in terms of geography is an essential new trend. The validation by the European Medicines Agency of serplulimab's Marketing Authorization Application marks an important step in this respect, as it shows that high quality clinical data obtained in Asians is acceptable according to Western regulatory standards.

This reflects the broader evolution of global regulatory frameworks to allow global clinical trial strategies which will take advantage of centers of excellence geographically and ensure that high levels of safety and efficacy standards are met, all leading to faster approvals and lower development costs of new treatments.

Asia Pacific holds the leading market share contributing to 76% of total global serplulimab sales worth USD 395 million in 2025 owing to its well-developed commercial structure, regulatory approvals in different indications, and the epidemiology of diseases that match with the areas of focus in serplulimab’s clinical development. China is the key market, with approximately 138,000 new extensive-stage small cell lung cancer cases annually. along with esophageal squamous cell carcinoma having more than 320,000 new cases.

Reimbursement inclusion on the National Reimbursement Drug List had a profound effect on the market landscape through increased accessibility from commercially insured patients to all 1.3 billion beneficiaries within the nationwide health insurance scheme, thus increasing the treatment penetration rate from 12% prior to reimbursement to 38% in 2025. Secondary markets in Japan and South Korea have well-established regulatory frameworks as well as favorable reimbursement experience for checkpoint inhibitors.

Europe is predicted to be the fastest-growing regional market, having a CAGR of 16.8%, till 2034, because of expected EMA approval followed by commercial launches within EU countries. European regulation system, which implies centralization and scientific health technology appraisal, offers clear strategies for marketing of serplulimab based on clinical and health-economic evidence.

Favorable approaches to the analysis of cost-effectiveness and budget impact of therapies, together with the presence of check point inhibitors' treatment programs and infrastructure, create favorable conditions for fast integration of serplulimab after registration and reimbursement decisions.

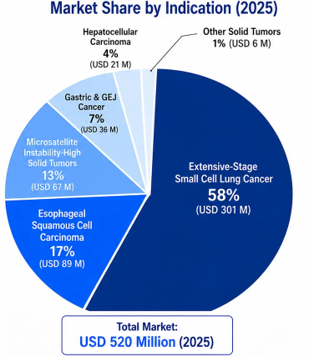

EXT-STG SMALL CELL LUNG CANCER has emerged as the dominant indication, accounting for 58% market share worth USD 301 million in 2025, with an impressive CAGR of 14.2% to 2034. Such dominance is mainly attributed to the ground-breaking approval of serplulimab, along with existing clinical protocols in combination with carboplatin and etoposide chemotherapy, coupled with many patients who do not have many other treatment options.

Esophageal Squamous Cell Carcinoma is the fastest-growing segment, valued at USD 89 million. with an anticipated CAGR of 18.7% till 2034 fueled by positive outcomes from the ASTRUM-007 trial and the huge unmet need within the epidemiology which is highly prevalent within the Asian geography wherein serplulimab already has an established presence. The growth dynamics of the segment also derive benefit due to lack of penetration of checkpoint inhibitors in Asian patients suffering from esophageal cancer.

The Microsatellite Instability-High Solid Tumors market is valued at USD 67 million in 2025, representing a promising precision oncology indication in precision medicine due to its response to checkpoint inhibition therapy in biomarker-positive patients.

Combination Therapy is expected to constitute 73% of total market value worth USD 380 million in 2025. This is driven by the fact that serplulimab has its main regulatory approvals and clinical developments mainly as a part of combination therapy with other chemotherapy, antiangiogenics, and targeted treatments. Monotherapy constitutes 27% of market share worth USD 140 million in 2025. Combination therapy is mainly driven by the changing paradigms in the field of oncology treatment based on rational drug combinations.

Monotherapy is primarily used for the use of checkpoint inhibitors in the case of microsatellite instability high solid tumors and biomarker selected population.

Hospital Pharmacies account for 78% of the market share of distribution channel at USD 406 million by 2025, due to the needs of institutional administration for IV delivery of checkpoint inhibitors, eligible patient population being confined to oncology departments with adequate monitoring facilities, and hospital-based procurement policies concerning checkpoint inhibitors.

Specialty Cancer Centers account for 18% of the market, valued at USD 94 million in 2025. This is due to oncology hospitals that will have high rates of checkpoint inhibitors and specific patients who require immunotherapy treatment.

The competitive landscape in the global serplulimab market is uniquely distinctive due to the proprietary control of Shanghai Henlius Biotech over the development, manufacturing, and global marketing of serplulimab, in comparison with other PD-1/PD-L1 inhibitors such as pembrolizumab, nivolumab, atezolizumab, and durvalumab. The company’s competitive advantage is driven by strong clinical evidence from understudied populations, competitive pricing to enable healthcare adoption, development of strategic alliances for market penetration, and innovative combinations that prove superiority among certain molecular subgroups.

Henlius’ competitive strengths include vertically integrated operations from the clinical development, state-of-the-art biomanufacturing with commercial production scale, regulatory network in Asia, and strategic commercial partnerships to enable market expansion globally.

March 2026: Positive Phase III data from the study of serplulimab and chemotherapy as a first-line therapy for esophageal squamous cell carcinoma, ASTRUM-007, was reported by Shanghai Henlius Biotech, with evidence of overall survival benefit being statistically significant.

January 2026: Scientific evaluation of the marketing application of serplulimab for extensive-stage small cell lung cancer conducted by the EMA is now completed. The final decision on marketing authorization of the drug is expected to be made in Q2 2026.

November 2025: Approval for serplulimab was obtained in Indonesia via cooperation with KGbio, thus increasing its commercial reach throughout the Southeast Asian region to aid in the formulation of pan-regional commercial strategy before entering Western markets.

September 2025: Follow-up data from the ASTRUM-005 trial that was presented at the European Society for Medical Oncology Congress showed prolonged survival advantages with 23% overall survival rates at three years for serplulimab-based treatment compared to 11% for chemotherapy alone.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.