Share this link via:

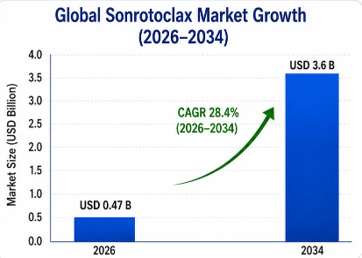

The global sonrotoclax market size was valued at USD 285.4 million in 2025 and is projected to reach USD 465.8 million in 2026, expanding to USD 3.6 billion by 2034, growing at a CAGR of 28.4% during the forecast period (2026-2034).

Sonrotoclax is an innovative second-generation, highly selective inhibitor of the B-cell lymphoma 2 (BCL-2) protein designed to overcome the problems of first-generation BCL-2 inhibitors, especially venetoclax, in clinical settings. Sonrotoclax, created by BeiGene, shows around 10 times higher affinity toward BCL-2 protein than venetoclax and also shows marked selectivity between BCL-2 and BCL-XL proteins. This selectivity is clinically relevant because BCL-XL inhibition leads to the dose-limiting side effect of thrombocytopenia associated with venetoclax therapy.

The sonrotoclax molecular action is dependent on the molecule's high binding capacity towards BCL-2 apoptosis inhibitor protein, which results in the displacement of BAX and BAK apoptosis promoters, and thus reestablishes the intrinsic apoptotic function in malignant B-cells, which become resistant to cell death via overexpression of the BCL-2 protein. This is especially true in hematological malignancies in which BCL-2 overexpression is the primary characteristic, allowing cancer cells to survive despite the presence of DNA damage, metabolic stress, and treatment. The structural optimization of the molecule allows for greater BCL-2 inhibition without causing platelet toxicity, which is common in venetoclax treatment.

Clinically, sonrotoclax targets important unmet clinical needs in the subset of about 30–40% of patients who acquire resistance to venetoclax via BCL-2 mutations, especially the G101V mutation that lowers the binding affinity of venetoclax without impacting sonrotoclax similarly. This ability to overcome resistance makes sonrotoclax not only a competitive product against venetoclax among treatment-naive populations but also a logical choice in venetoclax-resistant patients that lack options. The drug is currently being studied extensively in both single-agent and combination regimens, including combination with zanubrutinib, BeiGene’s novel BTK inhibitor.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 285.4 Million |

| Forecast Value | USD 3.6 Billion |

| CAGR | 28.4% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Indication, Therapy Type, Line of Treatment, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | BeiGene Ltd., AbbVie Inc., Roche (Genentech), Ascentage Pharma, Eli Lilly (Loxo Oncology) |

Get more details on this report - Request Free Sample

The major structural factor responsible for the growth of sonrotoclax market is the superior tolerability profile of sonrotoclax compared to venetoclax due to the lower degree of thrombocytopenia side effect, which is a dose-limiting toxicity limiting the development of first generation BCL-2 inhibitors. Thrombocytopenia associated with venetoclax occurs in 40-50% of patients and Grade 3-4 side effects are observed in 15-20% of patients requiring dose adjustment and complicated schedule of drug administration lasting 5 weeks in case of chronic lymphocytic leukemia.

The improved BCL-XL sparing ability of sonrotoclax results in clinically relevant reduced incidence of thrombocytopenia. Sonrotoclax does not require dose escalation and can be administered at a fixed dose right from the start due to tolerability issues. This makes it possible for patients with underlying cytopenias, low bone marrow reserve due to previous treatments, or other risk factors for venetoclax-induced thrombocytopenia to qualify for treatment.

The emerging population of patients who have been exposed to and become resistant to venetoclax-based regimens represents an unmet need that can be met by the potential of sonrotoclax to act on venetoclax-resistant BCL-2 mutations. Specifically, the emergence of the G101V mutation in BCL-2 protein causes venetoclax resistance because of the inability of venetoclax to bind to the mutated form of BCL-2 protein due to steric hindrance. In addition, the G101V mutation does not alter the BCL-2 protein function and continues to make the tumor cells dependent on the anti-apoptotic signal from BCL-2 protein.

As venetoclax becomes more prevalent in the first-line treatment regimen for chronic lymphocytic leukemia and B-cell malignancies, the number of venetoclax-experienced patients requiring second-line therapy increases, generating additional markets for sonrotoclax without competing with venetoclax.

Despite having optimized pharmacological characteristics, sonrotoclax is a highly effective BCL-2 inhibitor with inherent risks of tumor lysis syndrome in its early stages of administration, making extensive monitoring protocols necessary that create significant logistics and economic hurdles in the commercialization of this drug. Tumor lysis syndrome refers to an oncologic emergency that occurs when there is a massive spillage of contents from the inside of tumor cells into the blood after their rapid destruction, which might lead to acute renal failure, cardiac dysrhythmias, and even death.

The regulators have made it mandatory to follow extensive monitoring protocols in the dose escalations phase, such as regular lab tests, prophylactic hydration, lowering of uric acid levels in the body, and even hospitalization of certain at-risk patients.

The biggest commercial opportunity for sonrotoclax comes from the development of sonrotoclax in combination first-line therapies, especially when combined with zanubrutinib as a preferred chemotherapy-free treatment option for treatment-naïve chronic lymphocytic leukemia patients. This population is the largest with the best therapeutic response and fewest complications from previous therapies. Clinical development that shows better minimal residual disease negativity than current standards would quickly make sonrotoclax in combination as the preferred first-line therapy.

The field of hematologic oncology is currently moving to personalize the duration of therapy by utilizing minimal residual disease tests for the decision to continue or discontinue therapy. Rather than employing a set duration regimen, the newer methods involve using very sensitive molecular methods to check residual diseases and make personalized treatments whereby patients with undetectable minimal residual disease would be able to stop taking drugs early while others with remaining disease will continue or change the regimen.

Minimal residual disease endpoints are included in ongoing clinical trials of sonrotoclax as a way of positioning them in the newer therapeutic regimens to be compared with other drugs. This is in line with value-based health care that aims at optimizing drug use.

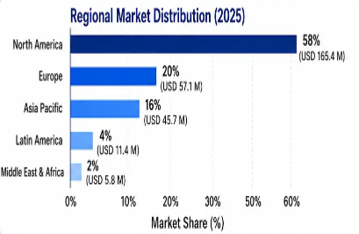

North America holds a 58% share of the global sonrotoclax market with revenue worth USD 165.4 million in 2025 and is expected to grow at a CAGR of 27.8% until 2034. Dominance is due to well-developed infrastructure for hematological oncology, quick adoption of advanced targeted therapies, comprehensive health coverage for breakthrough oncology medications, and presence of experts in the field of sonrotoclax owing to their involvement in many clinical trials. Programs for breakthrough therapy designation, fast track approvals, and priority reviews of treatments by FDA in US for serious conditions with no available treatment help accelerate development time of such treatments.

Infrastructure for reimbursement of costly oncology medications administered both orally and intravenously in the form of Medicare Part D and specialty pharmacy benefits for commercial insurance plans that already exist that serve as the basis for sonrotoclax introduction after its regulatory approval. Specialized pharmacy distribution networks with patient assistance programs for venetoclax require minor investments for adaptation for sonrotoclax.

Asia-Pacific is the region with the highest expected growth rate, reaching 31.7% over 2034 owing to the strategic placement of BeiGene as a firm based out of China with complete regulatory, clinical, and commercial capabilities in major markets across Asia. The National Medical Products Administration in China shows its increasing ability to assess novel oncology medicines with reduced review periods for breakthrough designations. Furthermore, the inclusion of China in BeiGene’s international clinical studies allows for joint regulatory filings for major markets.

The rising burden of hematology cancers in Asia-Pacific, especially an increase in chronic lymphocytic leukemia prevalence because of the ageing population and improved diagnostics, provides a growing addressable market for BeiGene owing to its geographical strengths. There are other high-value markets such as Japan, South Korea, and Australia that already have reimbursement schemes for innovative oncology drugs.

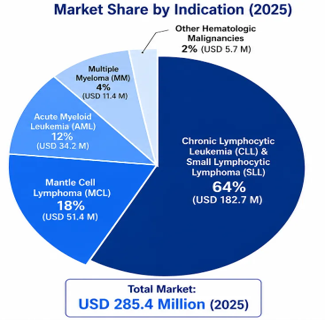

Chronic Lymphocytic Leukemia and Small Lymphocytic Lymphoma represent the major indications with 64% market share of USD 182.7 million in 2025, experiencing 29.1% CAGR till 2034 as key indications propelling clinical developments and expected first-time regulatory approvals. The indication is supported by significant prevalent patient base, relapsing disease course, requiring multiple lines of therapy, and proven dependency on BCL-2, providing excellent commercial platform. Mantle Cell Lymphoma captures 18% market share with USD 51.4 million and 28.6% CAGR, reflecting key priority indication with considerable unmet medical need in relapsed settings.

Acute Myeloid Leukemia holds 12% market share with USD 34.2 million and 32.4% CAGR, as fastest-growing indication segment, due to ongoing combination trials with hypomethylating agents in older or unfit patients. Multiple Myeloma and other hematologic cancers contribute to remaining market share with growth potential as the clinical portfolio matures.

The Combination Therapy market segment leads with 79% market share worth USD 225.5 million in 2025, growing at 29.8% CAGR owing to the synergistic effect of sonrotoclax and other therapies, especially BTK inhibitors and anti-CD20 antibodies. The market is driven by the scientific rationale behind multi-targeted mechanisms of action and superior efficacy compared with monotherapy. as opposed to monotherapy and paradigm shift towards non-chemotherapy-based approaches.

Monotherapy represents 21% market share worth USD 59.9 million and is mainly applied in heavily pre-treated patients who are unable to use combination therapies or maintenance therapies after successful induction. Even though revenue contribution is much lower, the monotherapy approach is still crucial for treating certain categories of patients.

Relapsed/Refractory indications capture 68% market share worth USD 194.1 million in 2025, because sonrotoclax was initially developed in highly pretreated patients where unmet need was greatest and the regulatory pathway was more straightforward. First-Line indications make up 24% market share worth USD 68.5 million, growing at a 33.2% CAGR to become highest growth segment owing to pivotal combination trials that may position sonrotoclax as a standard of care in the first-line indication.

Second-Line indications will hold 8% market share catering to bridging patient population between first line and heavily pretreated indications. Growth here is contingent upon showing efficacy in particular resistance situations.

The competitive landscape for sonrotoclax is shaped by the broader BCL-2 inhibitor market. and targeted hematology-oncology, wherein venetoclax, developed jointly by AbbVie and Roche, is in an enviable position owing to its efficacy data, regulatory approval, and prescriber loyalty. The differentiation strategy that underpins sonrotoclax’s competitiveness includes better tolerability leading to a wider utility for combinations, continued activity in venetoclax-resistant diseases, and BeiGene’s capabilities across both BCL-2 and BTK inhibition platforms.

Competitors that are emerging include lisaftoclax (APG-2575), which is being developed by Ascentage Pharma, and LOXO-338 from Eli Lilly. Both products are currently in clinical development for the same indication. There are other competitors for alternative mechanisms of action, such as reversible BTK inhibitors, bispecific antibodies, and CAR-T cells. BeiGene’s key competitive advantage is its ownership of both zanubrutinib and sonrotoclax.

June 2026: BeiGene submitted NDA application to the FDA for sonrotoclax plus zanubrutinib for the treatment of relapsed/refractory chronic lymphocytic leukemia patients, with expected action date in Q1 2027 through priority review process.

April 2026: Data from pivotal Phase III MAHOGANY trial showed that sonrotoclax plus zanubrutinib provided statistically significant progression-free survival benefit compared to standard chemoimmunotherapy in first-line mantle cell lymphoma patients.

February 2026: Orphan Drug Designation was granted by European Medicines Agency for sonrotoclax use in the treatment of acute myeloid leukemia.

December 2025: BeiGene initiated a global Phase III clinical trial. to compare the effectiveness of triplet therapy comprising sonrotoclax, zanubrutinib, and obinutuzumab with venetoclax-obinutuzumab in first-line chronic lymphocytic leukemia with superior results.

October 2025: The results presented during a major hematology meeting showed that sonrotoclax had an overall response rate of 72% when used alone in heavily pretreated relapsed/refractory chronic lymphocytic leukemia.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.