Share this link via:

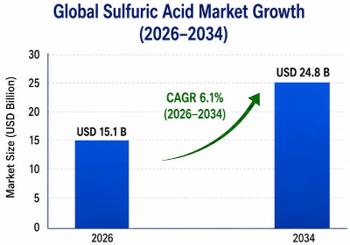

The global sulfuric acid market size was valued at USD 14.2 billion in 2025 and is projected to reach USD 15.1 billion in 2026, expanding to USD 24.8 billion by 2034, growing at a CAGR of 6.1% during the forecast period (2026-2034). In volume terms, global production exceeded 280 million metric tons in 2025, establishing sulfuric acid as the most produced industrial chemical worldwide and a fundamental indicator of global industrial activity.

Sulfuric acid represents the cornerstone of modern industrial chemistry, functioning as an essential building block across diverse manufacturing sectors through its unique properties as a strong acid, dehydrating agent, and chemical intermediate. The compound is primarily manufactured through the contact process, where sulfur dioxide undergoes catalytic oxidation to sulfur trioxide using vanadium pentoxide catalysts, followed by absorption in concentrated acid to achieve conversion efficiencies exceeding 99.5% in modern double-absorption plants. This technological maturity, combined with the chemical’s fundamental role in phosphate fertilizer production, metal processing, petroleum refining, and chemical synthesis, creates a market characterized by stable demand growth tied to global agricultural output, industrial expansion, and environmental compliance requirements.

The market’s structural foundation rests on the phosphate fertilizer industry, which consumes approximately 55-60% of global sulfuric acid production through the conversion of phosphate rock to phosphoric acid and downstream fertilizer products including diammonium phosphate, monoammonium phosphate, and triple superphosphate. This agricultural linkage connects sulfuric acid demand directly to global food security imperatives, population growth dynamics, and agricultural intensification trends across developing economies. Lithium and rare earth elements that are essential for clean energy technologies; petroleum refining alkylation processes producing high-octane gasoline components, and chemical manufacturing spanning titanium dioxide pigments, synthetic fibers, and industrial intermediates.

The supply landscape is dominated by recovered sulfur from oil and gas refining operations, which accounts for over 85% of elemental sulfur feedstock, alongside involuntary production from base metal smelting where environmental regulations mandate sulfur dioxide capture and conversion to sulfuric acid. This creates a complex supply-demand dynamic where sulfuric acid availability is closely tied to upstream refinery utilization rates, crude oil sulfur content, and base metal production levels, resulting in regional supply imbalances and significant transportation constraints due to the chemical’s corrosive nature and hazardous classification.

Modern sulfuric acid production increasingly emphasizes energy integration and environmental compliance, with advanced plants incorporating waste heat recovery systems that generate steam and electricity, achieving overall energy efficiencies approaching 98% while meeting stringent emission standards. The market is experiencing structural evolution through growing demand from battery material processing for electric vehicles, critical mineral extraction supporting renewable energy infrastructure, and circular economy initiatives focused on spent acid regeneration and reuse.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 14.2 Billion |

| Forecast Value | USD 24.8 Billion |

| CAGR | 6.1% |

| Forecast Period | 2022-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Middle East & Africa |

| Segments Covered | By Raw Material, Grade, Application, End-Use Industry, Region |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, Germany, France, UK, Italy, Spain, Russia, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa, Morocco |

| Key Market Playes | OCP Group, Nutrien Ltd., The Mosaic Company, BASF SE, PVS Chemicals, Aurubis AG, Chemtrade Logistics |

Get more details on this report - Request Free Sample

The fundamental driver propelling sulfuric acid market expansion is the escalating global requirement for phosphate fertilizers essential to sustaining agricultural productivity for a world population projected to reach 9.7 billion by 2050. Phosphate fertilizer production, consuming approximately 140 million metric tons of sulfuric acid annually in 2025, represents the largest single application driving market demand through the conversion of phosphate rock to phosphoric acid and downstream fertilizer products. The process requires approximately 2.2-2.8 metric tons of sulfuric acid per metric ton of phosphoric acid produced, creating a direct correlation between global food security needs and sulfuric acid consumption.

Global fertilizer demand is experiencing sustained growth driven by declining per-capita arable land availability, soil nutrient depletion from intensive cultivation practices, and government policies promoting food self-sufficiency across major agricultural economies including India, Brazil, Indonesia, and Sub-Saharan Africa. India’s fertilizer subsidy program, allocating approximately USD 24 billion annually, directly stimulates domestic phosphate fertilizer production requiring substantial sulfuric acid inputs, while China’s agricultural modernization initiatives and Southeast Asian crop intensification programs create additional demand pressure.

The structural nature of this demand driver is reinforced by the essential role of phosphorus in plant nutrition, with no viable substitutes for phosphate-based fertilizers in maintaining crop yields necessary to feed growing populations. Morocco’s OCP Group, controlling approximately 70% of global phosphate rock reserves, has expanded integrated phosphate processing capacity requiring over 12 million metric tons of sulfuric acid annually by 2025, illustrating the scale of acid consumption in modern fertilizer production complexes.

The accelerating global transition toward electrification is creating transformative new demand streams for sulfuric acid through battery material processing, critical mineral extraction, and energy storage manufacturing. Electric vehicle sales reached 14.2 million units globally in 2025, representing 18% of total vehicle sales and projected to exceed 40 million units annually by 2030 under current policy trajectories. This transition requires massive expansion of lithium, cobalt, nickel, and manganese processing capacity, with hydrometallurgical extraction and purification processes consuming approximately 2.5-3.2 metric tons of sulfuric acid per metric ton of battery-grade metal salts produced.

Lithium processing represents the fastest-growing application segment, with global lithium carbonate equivalent production reaching 185,000 metric tons in 2025 and projected to exceed 750,000 metric tons by 2034. Spodumene concentrate processing, the dominant hard rock lithium extraction method, requires sulfuric acid for roasting and leaching operations, while lithium brine processing utilizes acid for pH adjustment and impurity removal. The development of domestic lithium processing capacity in North America, Europe, and Australia to reduce dependence on Chinese supply chains is driving regional sulfuric acid demand growth.

Critical mineral processing for rare earth elements, used in permanent magnets for electric vehicle motors and wind turbines, relies heavily on sulfuric acid for ore digestion and separation chemistry. The United States, Australia, and Canada are developing domestic rare earth processing capabilities requiring dedicated sulfuric acid supply infrastructure, with announced projects representing over USD 8 billion in investment through 2030.

Increasingly stringent environmental regulations governing sulfur dioxide emissions from refineries, power plants, and metal smelters are mandating comprehensive sulfur recovery systems that convert previously released emissions into commercially valuable sulfuric acid. The International Maritime Organization’s sulfur regulations limiting marine fuel sulfur content to 0.5% have accelerated refinery desulfurization processes, increasing recovered sulfur availability for acid production while simultaneously creating compliance obligations for sulfur utilization or disposal.

Base metal smelting operations face particularly stringent emission controls, with regulations in China, Europe, and North America requiring sulfur capture efficiencies exceeding 99.5%, effectively mandating on-site sulfuric acid production from smelter off-gases. This regulatory framework has converted sulfur from an atmospheric pollutant to a regulated co-product requiring commercial outlets, creating structural supply growth that must find demand through fertilizer production, metal processing, or export markets.

The copper smelting industry exemplifies this dynamic, with global copper smelter capacity producing approximately 28 million metric tons of by-product sulfuric acid annually in 2025, representing 10% of total global production. Chile’s copper smelting complex generates over 5 million metric tons of surplus sulfuric acid annually, requiring exports to regional fertilizer and mining operations across South America

Sulfuric acid’s classification as a hazardous material under international transport regulations creates substantial logistical constraints that limit market efficiency and maintain persistent regional price differentials. The chemical requires specialized corrosion-resistant transport equipment including lined tank trucks, railcars with protective coatings, and double-hulled marine vessels, adding USD 35-85 per metric ton to delivered costs depending on distance and transport mode. These logistics constraints prevent efficient arbitrage of regional supply-demand imbalances, creating market fragmentation where surplus regions experience depressed pricing while deficit areas face elevated costs.

Regional oversupply situations are particularly acute in areas with high base metal smelting activity or refinery concentration, where by-product acid production exceeds local consumption capacity. The Middle East, with substantial oil refining capacity, and Chile, with extensive copper smelting operations, generate acid surpluses that must be exported at discounted prices, creating pricing pressure throughout regional markets. Conversely, import-dependent regions including parts of Sub-Saharan Africa and Southeast Asia face supply constraints and price volatility due to limited local production and dependence on international shipments subject to freight rate fluctuations and port infrastructure limitations.

The highly corrosive nature of sulfuric acid imposes substantial regulatory compliance costs related to handling, storage, transportation, and worker safety that can constrain market participation, particularly for smaller operators and developing market participants. Facility design requirements include specialized storage tanks with corrosion-resistant linings, secondary containment systems, emergency response equipment, and worker protection protocols that collectively add USD 15-35 per metric ton to production costs compared to less hazardous chemicals.

Environmental regulations governing sulfuric acid production facilities continue to tighten globally, with emission standards for sulfur dioxide, particulates, and acid mist requiring advanced control technologies including wet gas scrubbing, electrostatic precipitation, and monitoring systems. The European Union’s Industrial Emissions Directive and analogous regulations in China and North America mandate best available technology standards that increase capital requirements for new facilities while requiring retrofits of existing plants.

The global energy transition is creating unprecedented demand for sulfuric acid in processing critical minerals essential for renewable energy infrastructure, electric vehicles, and energy storage systems. Lithium processing represents the highest-growth opportunity, with global lithium demand projected to increase 8-fold by 2034 driven by battery manufacturing expansion. Spodumene concentrate processing, the dominant hard rock lithium source, requires 2.8-3.2 metric tons of sulfuric acid per metric ton of lithium carbonate equivalent produced, creating substantial incremental demand as new processing facilities are developed in Australia, Canada, and the United States.

Rare earth element processing offers additional growth potential as Western nations develop domestic supply chains to reduce dependence on Chinese production. Planned rare earth processing facilities in the United States, Australia, and Europe will require approximately 350,000 metric tons of sulfuric acid annually by 2030, representing entirely new demand not served by existing supply infrastructure. The premium pricing for high-purity acid used in these applications, typically 40-60% above industrial grade pricing, creates attractive margin opportunities for suppliers capable of meeting stringent quality specifications.

Copper processing through heap leaching and hydrometallurgical extraction is expanding as mining operations exploit lower-grade ore deposits amenable to acid leaching technologies. The Democratic Republic of Congo and Zambia are developing substantial new copper processing capacity requiring dedicated sulfuric acid supply, with projected consumption reaching 8 million metric tons annually by 2030 in Central Africa alone.

Growing corporate sustainability commitments and tightening environmental regulations are driving demand for spent sulfuric acid regeneration services that recover and reconcentrate used acid from petroleum refining, metal processing, and chemical manufacturing operations. Spent acid regeneration achieves 85-92% recovery efficiency while reducing hazardous waste disposal costs and lowering net fresh acid consumption for industrial users. The petroleum refining sector generates approximately 15 million metric tons of spent alkylation acid annually, representing the largest feedstock source for regeneration operations.

The circular economy opportunity extends beyond simple regeneration to comprehensive acid management services where specialized operators provide build-own-operate facilities at major industrial sites, managing the complete acid lifecycle from fresh supply through regeneration and disposal of residual wastes. This service model reduces customer capital requirements while ensuring regulatory compliance and optimizing acid utilization efficiency.

Technological advances in regeneration processes, including improved thermal decomposition systems and enhanced purification methods, are expanding the range of spent acid streams amenable to recovery while improving product quality to meet increasingly stringent specifications for reuse applications.

Modern sulfuric acid production facilities are increasingly designed as integrated energy hubs within industrial complexes, capturing waste heat from exothermic oxidation and absorption reactions to generate steam and electricity for broader site operations. Advanced heat recovery systems in double-absorption contact process plants achieve overall energy efficiencies approaching 98%, with surplus steam supporting fertilizer production, metal smelting, or chemical manufacturing processes within integrated facilities.

This energy integration trend is particularly pronounced in new phosphate processing complexes where sulfuric acid plants serve as central energy providers, generating steam for phosphoric acid concentration, electricity for materials handling, and process heat for granulation operations. The Maaden phosphate complex in Saudi Arabia exemplifies this approach, with sulfuric acid production integrated into a comprehensive energy network serving the entire fertilizer manufacturing site.

Cogeneration capabilities are becoming standard features in new sulfuric acid plants, with waste heat recovery systems producing 15-25 MW of electrical power in world-scale facilities. This energy integration reduces overall production costs by USD 8-15 per metric ton while improving environmental performance through enhanced energy efficiency and reduced greenhouse gas emissions per unit of output.

The hazardous nature and high transportation costs of sulfuric acid are driving trends toward localized production and on-site captive facilities that minimize logistics requirements while ensuring reliable supply for major consumers. Large-scale phosphate producers, copper smelters, and integrated chemical complexes increasingly favor captive sulfuric acid production over merchant supply relationships, reducing transportation risks and costs while enabling tight integration with upstream sulfur recovery and downstream consumption processes.

This localization trend is reinforced by the development of modular sulfuric acid plant designs that enable economic production at smaller scales suitable for dedicated industrial applications. Advanced process control systems and standardized equipment packages allow efficient operation of 500-1,500 metric tons per day facilities that would have been uneconomical with traditional plant designs requiring minimum scales of 2,000-3,000 metric tons per day.

The emergence of industrial cluster development models, particularly in emerging economies, creates opportunities for shared sulfuric acid infrastructure serving multiple smaller consumers within concentrated industrial zones. These shared facilities achieve economies of scale while minimizing individual transportation requirements for participating companies.

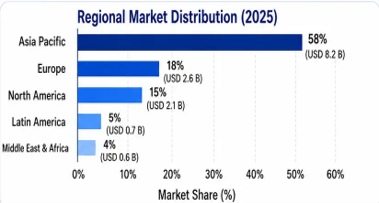

Asia Pacific dominates the global sulfuric acid market with approximately 58% of consumption valued at USD 8.2 billion in 2025, driven by China’s massive industrial base, India’s expanding fertilizer sector, and the region’s concentration of base metal smelting and chemical manufacturing operations. China alone accounts for 42% of global sulfuric acid production and consumption, with annual output exceeding 115 million metric tons from an integrated network of contact process plants, smelter by-product facilities, and pyrite roasting operations concentrated in Yunnan, Guizhou, Shandong, and Inner Mongolia provinces.

The Chinese market is characterized by tight integration between sulfuric acid production and downstream consumption through state-owned enterprises and large private conglomerates that operate vertically integrated phosphate fertilizer, titanium dioxide, and chemical fiber complexes. This integration model provides supply security and cost optimization while creating barriers to entry for international suppliers seeking to penetrate the Chinese market.

India represents the second-largest and fastest-growing major market within the region, with domestic consumption reaching 18.2 million metric tons in 2025, primarily driven by phosphoric acid and phosphate fertilizer production supporting the country’s agricultural sector. India’s limited domestic sulfur resources create dependence on imported elemental sulfur from Canada, the Middle East, and Kazakhstan, making the country vulnerable to supply chain disruptions and price volatility in international sulfur markets.

With a projected CAGR of 8.9% through 2034, driven primarily by Morocco’s OCP Group phosphate processing expansion, Saudi Arabia’s industrial diversification under Vision 2030, and Sub-Saharan Africa’s emerging copper and critical mineral processing sectors. Morocco has established itself as the global center of integrated phosphate processing, with OCP Group operating the world’s largest sulfuric acid consumption complex requiring over 12 million metric tons annually to support phosphoric acid and fertilizer production for domestic use and export.

The region benefits from abundant natural resources including phosphate rock reserves in Morocco and Western Sahara, substantial oil and gas resources providing elemental sulfur feedstock, and emerging critical mineral deposits in the Democratic Republic of Congo, Zambia, and South Africa that require hydrometallurgical processing using sulfuric acid. Saudi Arabia’s MAADEN mining and metals company has developed integrated phosphate and aluminum processing facilities consuming over 3 million metric tons of sulfuric acid annually, while expanding into specialty chemicals and advanced materials production.

Sub-Saharan Africa presents significant long-term growth potential through expanding copper and cobalt mining operations where heap leaching and hydrometallurgical extraction methods using sulfuric acid are the dominant processing technologies. The Democratic Republic of Congo’s copper production reached 2.9 million metric tons in 2025, with approximately 50% produced through acid leaching methods requiring 6.8 million metric tons of sulfuric acid annually.

Elemental Sulfur dominates raw material sourcing with 78% market share, primarily recovered from oil and gas refining operations where hydrogen sulfide removal from crude oil and natural gas streams produces elemental sulfur as a mandatory by-product. This recovered sulfur provides cost-effective feedstock for sulfuric acid production while addressing environmental compliance requirements in the petroleum sector. The tight linkage between refinery operations and sulfur availability creates supply dynamics closely correlated with global crude oil processing rates and fuel sulfur specifications.

Base Metal Smelter Off-Gases account for 18% of raw material input, representing involuntary production where environmental regulations mandate capture and conversion of sulfur dioxide emissions from copper, zinc, and nickel smelting operations. This source provides geographically concentrated supply in mining regions but creates market dynamics where acid production is driven by metal demand rather than acid market fundamentals.

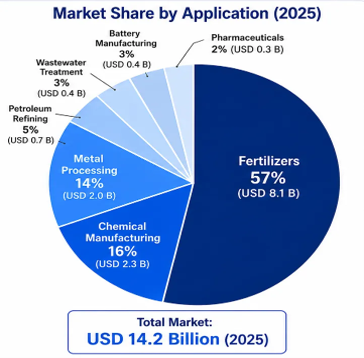

Fertilizers represent the dominant application segment at 57% of global consumption valued at USD 8.1 billion in 2025, encompassing phosphoric acid production, direct acidulation of phosphate rock, and pH adjustment in fertilizer manufacturing processes. This application demonstrates stable long-term growth tied to global agricultural output requirements and population growth dynamics.

Chemical Manufacturing accounts for 16% of consumption through production of titanium dioxide pigments, caprolactam for synthetic fibers, hydrofluoric acid, and diverse industrial intermediates. This segment benefits from industrial expansion in emerging economies and growing demand for specialty chemicals in electronics and advanced materials applications.

Metal Processing represents 14% of consumption through hydrometallurgical extraction of copper, zinc, nickel, uranium, and increasingly lithium and rare earth elements essential for clean energy technologies. This application segment demonstrates the highest growth rates driven by energy transition material requirements.

Agriculture dominates end-use consumption through fertilizer production, accounting for 57% of total market volume and providing stable demand growth aligned with global food security requirements. Mining represents 19% of consumption through ore processing and metal extraction operations that are expanding to meet critical mineral demands for renewable energy infrastructure. The automotive industry accounts for 8% through lead-acid battery manufacturing and is undergoing significant evolution as electric vehicles gradually penetrate global markets while maintaining requirements for conventional starter batteries.

The global sulfuric acid market exhibits regional concentration with limited international trade due to transportation constraints, creating competitive dynamics focused on supply chain integration, operational efficiency, and customer proximity rather than global market share competition. Leading market participants include OCP Group, which operates the world’s largest integrated phosphate and sulfuric acid complex in Morocco with over 12 million metric tons annual consumption; Nutrien Ltd. and The Mosaic Company, which produce sulfuric acid for captive use in North American phosphate fertilizer operations; and BASF SE, which operates integrated chemical manufacturing networks in Europe requiring substantial sulfuric acid inputs for diverse applications.

By-product acid producers including Aurubis AG in Europe, Freeport-McMoRan in North America, and Codelco in Chile generate sulfuric acid as unavoidable output from copper smelting operations, competing with merchant producers on pricing in regional markets. The competitive landscape is characterized by vertical integration strategies where major consumers develop captive production capabilities to ensure supply security and cost optimization.

March 2026: OCP Group announced the commissioning of a new 1.5 million metric ton per year sulfuric acid plant at its Jorf Lasfar complex in Morocco, featuring advanced double-absorption technology achieving 99.8% sulfur conversion efficiency and integrated waste heat recovery systems generating 28 MW of electrical power for the broader phosphate processing facility.

February 2026: Nutrien Ltd. completed a USD 285 million expansion of its Geismar, Louisiana phosphoric acid complex, including a new 2,800 metric ton per day sulfuric acid plant utilizing elemental sulfur from Gulf Coast refineries and incorporating state-of-the-art emission control systems achieving zero liquid discharge standards.

January 2026: BASF SE announced the development of next-generation vanadium catalyst formulations for contact process sulfuric acid plants, achieving 99.9% sulfur dioxide conversion at reduced operating temperatures and extending catalyst life by 35%, enabling more efficient operation of smaller-scale plants serving specialized applications.

December 2025: PVS Chemicals expanded its spent sulfuric acid regeneration capacity in the US Gulf Coast by 520,000 metric tons per year, targeting growing demand from petroleum refineries seeking comprehensive acid management services to meet corporate sustainability commitments and circular economy objectives.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.