Share this link via:

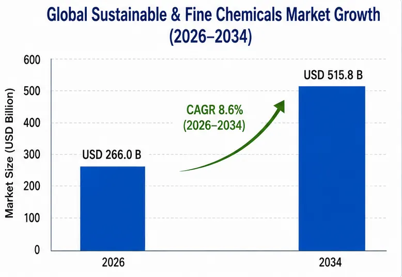

The global sustainable and fine chemicals market size was valued at USD 245.2 billion in 2025 and is projected to reach USD 266.0 billion in 2026, expanding to USD 515.8 billion by 2034, growing at a CAGR of 8.6% during the forecast period (2026-2034).

Sustainable and fine chemicals are a game-changing merger in the global chemical industry that produces high-value, high-purity molecular products using processes that are environmentally sustainable, have low carbon footprints, do not generate hazardous waste, and are based on renewable or circular raw materials. Fine chemicals are generally defined as complex active pharmaceutical ingredients, specialty intermediates, agrochemical compounds, flavors and fragrances, and performance additives produced through multi-step batch processes and having close to strict quality specifications. The sustainable dimension takes a radical approach to these production pathways based on principles of green chemistry, biocatalysis, precision fermentation, and advanced process technologies, which all contribute to improved environmental performance and manufacturing efficiency.

The market responds to the pressing challenges of the world in the areas of healthcare innovation, food security and climate action. Fine chemicals are critical ingredients in life-saving drugs, crop protection products vital to food production around the world and specialty materials used in cutting-edge technologies. Sustainable fine chemicals have become essential supply chain requirements for pharmaceuticals, agrochemicals, personal care and specialty materials moving from premium niche to essentials in the supply chain as regulations place further restrictions on use of dangerous chemicals and carbon emissions and corporate commitments to sustainability become mandatory in procurement requirements.

This technological transformation also involves several innovation pathways such as the biocatalysis, which involves the use of engineered enzymes for selective molecular transformations under mild conditions; precision fermentation, with the use of genetically modified microorganisms for production of complex molecules from renewable feedstocks; continuous flow chemistry, by replacing energy intensive batch processes with efficient continuous processes; and synthetic biology platforms that produce previously inaccessible molecules through biological processes. All these technologies contribute to significant benefits in terms of atom economy, energy efficiency, waste reduction and product quality and to the possibility of decoupling chemical production from fossil fuel consumption.

Beyond just selling products, the commercial value lies in the holistic value proposition, including regulatory compliance, supply chain resilience, brand differentiation, and long-term sustainability performance. Companies that can provide evidence of environmental gains via third-party certifications, lifecycle assessments and traceability documentation can achieve a premium price and preferred supplier status with customers further down the supply chain seeking suppliers aligned with science-based decarbonization targets. and circular economy commitments.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 245.2 Billion |

| Forecast Value | USD 515.8 Billion |

| CAGR | 8.6% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

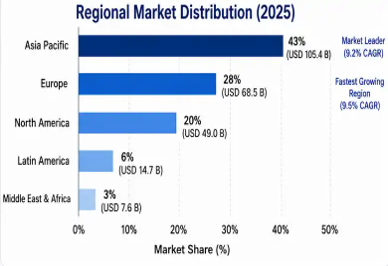

| Largest Market | Asia Pacific |

| Fastest Growing Market | Europe |

| Segments Covered | By Product Type, Technology, Application, Source, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | BASF SE, Lonza Group, Evonik Industries, DSM-Firmenich, Solvay, Dow Inc., Clariant, Novozymes |

Get more details on this report - Request Free Sample

Legally binding decarbonization plans and commitments, carbon pricing systems, and increasingly strict environmental laws directly affecting the chemical manufacturing process are the main structural forces driving sustainable fine chemicals market growth. Governments such as the European Union are progressively phasing out the traditional petrochemical synthesis methods with regulatory measures, such as REACH regulation, Chemical Strategy for Sustainability and phase-out of substances of very high concern, while encouraging the use of green chemistry. Carbon border adjustment mechanisms and emissions trading schemes provide direct cost advantages. to cleaner manufacturing processes, as carbon prices in leading markets are in the range of USD 85–100 per metric ton, potentially changing the economic competitiveness of renewable energy-based production routes compared to fossil-based ones.

The global chemical industry, with about 6% share of global GHGs, is under more pressure than ever to reach net-zero status by 2050 through full transition to renewable feedstocks, circular economy models and energy-efficient synthesis routes. More than 2,400 companies with USD 38 trillion in revenues have set science-based emissions reduction targets which clearly call for low-carbon procurement of chemical inputs, thus ensuring ongoing demand for sustainably produced fine chemicals with verified environmental credentials.

The development trend in the pharmaceutical industry to more complicated biological drugs, personal medicine, and green production approaches is one of the key driving factors behind the growth in the requirement for high-purity sustainable fine chemicals and pharmaceutical intermediates. In 2025, the world market value of pharmaceuticals exceeded USD 1.6 trillion, where the share of active pharmaceutical ingredients and their intermediate chemicals was between 25-35%, resulting in a USD 248.6 billion market value for pharmaceutical fine chemicals.

Major pharmaceutical firms such as Pfizer, Novartis, and AstraZeneca have implemented supplier sustainability scorecards that focus on carbon footprint, waste production, and renewable energy adoption, alongside quality and cost considerations, to be part of their procurement considerations. The patent cliff, with about USD 250 billion of branded pharma revenues will be under threat from generics by 2030, not only calls for affordable API manufacture but also necessitates innovation of novel molecules whose synthesis will require increasingly sophisticated sustainable processes.

The value of the pharma contract development and manufacturing organization market stood at USD 185 billion in 2025, where sustainable chemistry skills became key differentiators fetching price premium of 15-28% against traditional manufacturers and entering long-term supply arrangements due to customer preference for environmentally sustainable supply relationships.

One of the largest constraints that hinder rapid and sustainable development of fine chemicals is extremely high capital costs and the highly technical nature of converting from existing petrochemical manufacturing processes to new, sustainable manufacturing processes. Existing processes have benefited from over a hundred years of optimizing the process, as well as the economies of scale inherent in large, established plants. Sustainable production methods, on the other hand, will need entirely new facilities including biorefineries, precision fermentation processes, continuous flow reactors, and new purification units costing USD 80-350 million with an eight-year lead time.

Technical complexities range far past equipment cost into sophisticated knowledge about process chemistry, advanced analytical techniques, and regulatory revalidation for medicinal grade chemicals when a change in manufacturing process needs documentation, stability testing, and approval by regulatory bodies. Failure rates for scaling up biological chemical production from pilot to commercial scale remain around 35% due to challenges in maintaining microbial stability, optimizing heat transfer, and securing renewable feedstocks. of scaling up involves maintaining stability of microbial strains, fine tuning of flow dynamics in heat management, and supply of renewable materials.

Cost-effectiveness is difficult due to 18-25% higher prices of the bio-based fine chemicals over those derived from petroleum-based processes in 2025, making such products unaffordable in cost-sensitive applications even if they offer better environmental attributes. Cost-intensiveness, technical uncertainties, and long lead times make it difficult for other firms to enter this industry.

Increasing outsourcing of pharmaceuticals and specialty chemicals offers significant scope for sustainable chemistry-enabled CDMO players that can provide full-service process development, scale-up, and manufacturing operations. In the case of contract manufacturing pharmaceuticals, the market is valued at USD 185 billion in 2025. Fine chemicals and API contract manufacturing account for USD 68 billion with a compound annual growth rate of 11.4%.

Competitive advantages in sustainable chemistry competencies have become increasingly apparent, such that pharmaceutical companies are incorporating sustainability departments in their vendor evaluation processes along with procurement and technical departments. Manufacturers that are employing sustainable green chemistry technologies, using renewable energy sources, and showing a track record of reducing carbon footprints can realize considerable premium pricing in addition to long-term contracts due to customer preference for sustainable sourcing.

An opportunity presents itself in the emerging drug markets of Southeast Asia, Latin America, and Africa in which rising ambitions within manufacturing necessitate the transfer of technology from sustainable fine chemical producers that already possess these capabilities. Precision fermentation and flow chemistry enable efficient small-scale production compared with conventional large-batch chemical facilities.

In the realm of sustainable fine chemicals, systematic applications of artificial intelligence and machine learning platforms in chemical synthesis design, process optimization, and sustainability assessment workflows are driving transformative innovations in the sector. AI-based retrosynthetic analysis systems that are fed millions of chemical reaction data can suggest new synthetic pathways, where green chemistry parameters such as preferred solvents, renewable feedstocks, and target environmental performance metrics are considered parameters in the design phase.

Before laboratory experimentation, machine learning models optimize catalyst selection, reaction conditions, and process parameters. to maximize yields, minimize waste generation and reduce energy consumption all at once. Predictive toxicology and lifecycle assessment algorithms can be used to assess environmental and human health impacts at an early stage of chemical development helping to expedite chemical replacement of legacy chemicals and minimize development costs and time.

Digital twins of chemical manufacturing plants can be used to optimize continuous processes, fermentation processes and purification processes in the downstream, where the quality specifications of the product are kept while the use of resources is maximized, and optimization can take place in real time. AI driven process control coupled with advanced analytics provides tangible gains on sustainability performance and lower manufacturing costs, providing a competitive edge for technology-driven sustainable chemical producers.

The transformation from a conventional approach utilizing batch reactor technology to a system using continuous flow technology constitutes perhaps the most important development in fine chemical processing that allows for improvements not only in process safety and product quality but also in efficiency and environmental impact. The use of flow chemistry provides control over the process parameters such as temperature, pressure, residence time and stoichiometry on a millisecond time scale that was not possible with batch reactors.

Environmental gains encompass savings of up to 40-70% in terms of solvent usage, savings of 50-80% in terms of waste production, an increase in energy efficiency by 30-55%, and prevention of thermal runaway incidents related to large batch exothermic reactions. These benefits result in reductions in the E-factors used to evaluate the sustainability of our customers, in the pharmaceutical and specialty chemicals industries.

This technology enables a modular and scalable manufacturing approach., which is particularly useful for manufacturing fine chemicals of value at lower volumes, where flexibility and responsiveness can offer competitive advantages against larger batch systems.

Asia-Pacific dominated the market share with revenue of USD 105.4 billion in 2025 while holding a CAGR of 9.2% until 2034. It holds this regional dominance due to being the central global location for chemical production, which includes having significant production capabilities for APIs, agrochemicals, and specialty chemicals. Around 60% of global APIs are produced by China and India, along with 40% of fine chemical production capacity.

The area is undergoing a state-led transition into sustainable manufacturing due to China’s commitments to reach its Dual Carbon goals by 2060, along with an increased focus on green chemistry by India to satisfy the demands of their Western customers in the pharmaceutical industry. China invested USD 14.2 billion in bio-manufacturing facilities. in 2025 alone, while India saw its specialty chemical exports rise by 14%.

The regional manufacturers have access to plentiful feedstocks for renewable production, increasing know-how related to biotechnology and fermentation processes, as well as favorable government policies that support environmentally friendly industrial growth. Its manufacturing scale, competitive pricing, and sustainability capabilities position the Asia-Pacific region as the leading provider of sustainable fine chemicals globally.

Europe is the most rapidly growing segment with a CAGR of 9.5% until 2034 to attain a market value of USD 68.5 billion in 2025. Regional leadership is driven by stringent regulations such as REACH and European Green Deal policies that create global benchmarks of sustainability and competitive advantages for European firms that adhere to the regulations. Europe has some of the leading fine chemical companies such as BASF, Evonik, DSM-Firmenich, and Lonza with advanced research capabilities in green chemistry.

The manufacturers from the European continent enjoy premium prices for their sustainable products, in addition to entering long-term contracts with pharmaceutical and specialty chemicals consumers globally. Europe holds a leadership position when it comes to innovation in areas such as biocatalysis, continuous flow chemistry, and integration with the circular economy. It is also notable that the funding for sustainable chemistry research in the region exceeds EUR 4.5 billion through various programs within Horizon Europe.

Demand from consumers for sustainable products such as those in the pharmaceutical industry, cosmetic industry, and food ingredient industry enables European manufacturers to earn premiums, in addition to innovating continuously in terms of green chemistry technologies and sustainable manufacturing.

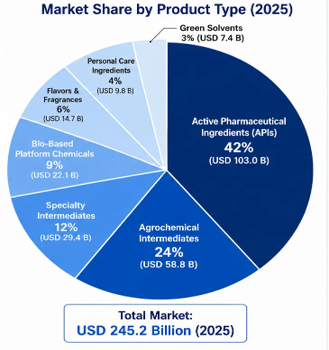

Active Pharmaceutical Ingredients lead the market with 42% market share valued at USD 103.0 billion in 2025, which is expected to grow at a CAGR of 9.1% through 2034. This segment demands the highest purity level and advanced synthesis technologies along with sustainable production processes that have become crucial in material sourcing among the leading pharmaceuticals. The segment thrives with inelastic demand and premium prices.

The fastest-growing segment is the bio-based platform chemicals segment, with 13.4% CAGR, and includes organic acids produced by fermentation process, specialty alcohols, and renewable intermediates, which serve as alternatives to petrochemical intermediates. Agrochemicals hold 24% market share valued at USD 58.8 billion due to regulations against synthetics chemicals, and demand for sustainable biodegradable agrochemicals is rising.

Biocatalysis and Enzymatic Reaction Processes and Fermentation and Biotechnology account for 54% of market value due to advancements in biological processes used for synthesizing fine chemicals. The use of such technologies has proven their advantage in terms of high specificity, milder process conditions, and lower waste generation levels.

Adoption of Continuous Flow Chemistry technology increased dramatically, with its adoption increasing from 12% in 2020 to 47% in 2025, facilitated by gains in safety, efficiency, and sustainability at the same time. Green Synthesis & Catalysis continues to advance through innovations through innovations in catalyst technology and process intensification.

The Pharmaceuticals segment constitutes the largest segment, accounting for 45% of the market with revenues expected to reach USD 110.3 billion in 2025 due to the demand for sophisticated APIs, sustainability needs, and outsourcing trends. The Personal Care & Cosmetics segment is the fastest-growing segment with a compound annual growth rate of 10.2%.

Applications in Food & Beverages continue to rise due to increasing demands for natural flavorings, clean label products, and fermentative additives, whereas the Electronics & Semiconductors industry demands ultra-pure chemicals with the highest possible environmental controls.

The global sustainable fine chemicals industry is highly concentrated, with a dominant presence of major chemical companies. of major chemical companies that have substantial market share due to their well-integrated manufacturing process, heavy spending on R&D activities, and wide range of products. The industry is highly competitive, with frequent mergers and acquisitions between chemical and biotechnology companies. for access to new production technologies and sustainable platforms.

The key points of competition include unique manufacturing processes, regulatory expertise, sustainability performance, and execution of difficult chemical manufacturing operations. Collaboration between large chemical companies and small biotech companies is also quite prevalent in this industry.

May 2026: BASF SE started production at its large-scale bio-intermediate plant in Germany using novel fermentation processes to generate high purity chiral molecules for pharmaceutical use, eliminating the traditional petrochemical route with a significant carbon footprint cut of 75%.

March 2026: Lonza Group expanded its continuous flow chemistry platform in Switzerland by building four new reactor trains catering to pharmaceutical companies that demand sustainable and safer APIs manufacturing process.

Evonik Industries launched a full range of biosurfactants and cosmetic actives using enzymatic technology to have 100% renewably sourced carbon feedstocks without compromising product performance.

Reducing the number of chemical synthesis steps that cut down the number of chemical steps needed to produce cardiovascular active pharmaceutical ingredients (APIs) from 12 to just 3 without any toxic metals and solvents.

December 2025: Dow Inc. acquired a top synthetic biology company at a deal value of USD 650 million to scale up its bio-based specialty polymers.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.