Share this link via:

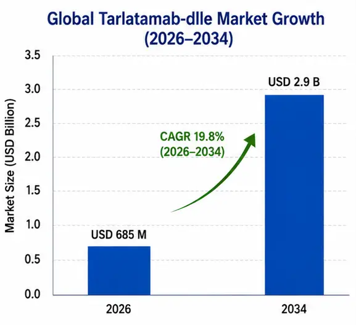

The global tarlatamab-dlle market size was valued at USD 520 million in 2025 and is projected to reach USD 685 million in 2026, expanding to USD 2.9 billion by 2034, growing at a CAGR of 19.8% during the forecast period (2026-2034).

Tarlatamab-dlle, commercially available as IMDELLTRA from Amgen Inc., is a novel therapeutic agent which is the first bispecific T-cell engager approved for the treatment of solid tumors. As an immunotherapeutic drug, it acts by binding delta-like ligand 3 protein present on tumor cells and CD3 on cytotoxic T cells to form an immunological synapse to guide the body's immune system to destroy cancer cells that express DLL3. It works in an MHC-independent and T-cell receptor-independent manner, allowing it to exert its anti-tumor activity even in immunosuppressive tumor microenvironments.

Small-cell lung cancer is one of the most aggressive and deadly thoracic malignancies, making up about 15% of lung cancers worldwide with more than 250,000 patients diagnosed each year. The cancer is distinguished by its fast-growing nature, quick dissemination to other parts of the body, sensitivity to platinum-based chemotherapy at first but later leading to a recurrence, and poor clinical outcome for recurrent or refractory patients. Before the introduction of tarlatamab-dlle, patients with small-cell lung cancer whose condition progressed post-first-line therapy had few treatment options, with response rates less than 25% and median survival of 4-6 months.

Tarlatamab-dlle has transformed this therapeutic approach with its focus on DLL3, a membrane-bound protein that is overexpressed in 85-96% of small cell lung cancer tumors while being virtually absent in adult tissues, thus offering a perfect candidate to serve as a target for tumor-associated antigens. During the key Phase II DeLLphi-301 study, tarlatamab-dlle showed a 40% objective response rate and median response duration of 9.7 months in heavily pre-treated patients, which was more than two times better than the response rates seen in patients treated with traditional second-line therapy options.

The commercial potential of tarlatamab-dlle is not limited to its existing indication but includes the proof-of-concept of the bispecific T-cell engager technology in solid tumors, thereby paving the way for treating other cancers that express DLL3 such as large cell neuroendocrine carcinoma and neuroendocrine tumors extra-pulmonary in nature. The success of the drug has led to further clinical trials for evaluating the effectiveness of the drug in earlier treatment lines and even through combinations with chemotherapy and checkpoint inhibitors.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 520 Million |

| Forecast Value | USD 2.9 Billion |

| CAGR | 19.8% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By Indication, Line of Therapy, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, Japan, China, India, Australia, South Korea, Brazil, Argentina |

| Key Market Playes | Amgen Inc., Roche (competitive pipeline), Bristol-Myers Squibb (competitive programs), AbbVie Inc |

Get more details on this report - Request Free Sample

The primary driving force behind the market growth of tarlatamab-dlle is the significant unmet medical need in the case of relapsed and refractory extensive stage small cell lung cancer, where the patients experience life-threatening disease progression with very limited treatment possibilities. More than 250,000 patients are diagnosed with small-cell lung cancer exceeds 250,000 cases per year worldwide, with approximately 70% of all the patients suffering from an extensive stage of the disease at the time of diagnosis.

Second-line therapy has been an area that is relatively stable for many years, with approved FDA treatments such as topotecan, lurbinectedin, and chemotherapy having objective response rates of 15 to 25 percent and median overall survival of 4 to 6 months. The biologic aggressiveness of small-cell lung cancer, which includes fast doubling time, resistance to platinum, and risk of developing central nervous system metastases, is leaving patients with very limited treatment options after disease progression. within several months after diagnosis.

Tarlatamab-dlle effectively bridges this critical gap by offering an immunotherapy strategy that is different in terms of mechanism and demonstrated superior efficacy in the pivotal trial DeLLphi-301. The drug achieved an objective response rate of 40% at the dose of 10 mg, which was approved, after two or more previous treatments with a median duration of response of 9.7 months and disease control rate of 68%. All of this is quite impressive compared to historical data and positions tarlatamab-dlle as the most effective treatment for relapsed or refractory small cell lung cancer.

The success achieved by tarlatamab-dlle in the clinical setting is the first definite proof of concept for the effectiveness of bispecific T-cell engagers in solid tumor cancers, which are generally more difficult targets to treat compared to hematological cancers owing to immunosuppressive tumor microenvironment, poor infiltration of T-cells, and heterogeneity of antigen presentation. This breakthrough in therapy highlights the importance of designing bispecific antibodies and their appropriate targeting to overcome the obstacles faced by T-cell therapies for solid tumors.

Success of tarlatamab-dlle is prompting major funding from the pharmaceutical industry for the development of other DLL3-targeting therapies and other bispecific T cell engagers for the treatment of other solid tumors. DLL3 expression is not limited to small cell lung cancer but can also be seen in large cell neuroendocrine carcinoma, extrapulmonary neuroendocrine tumors, and some prostate cancers.

The platform validation can help in the development of combinations involving the tarlatamab-dlle and existing cancer drugs, such as chemotherapy, checkpoint inhibitors, and targeted therapies, thus increasing the therapeutic value while keeping the risk at an acceptable level. The early-stage studies on the use of the tarlatamab-dlle in combination with platinum-etoposide chemotherapy and PD-L1 inhibitors in first-line extensive-stage small cell lung cancer patients can be considered the most promising areas for the further development of the molecule.

The primary factor limiting market adoption of tarlatamab-dlle is the management of the immune-related adverse effects that come from the use of a bispecific T-cell engager. These include cytokine release syndrome and immune effector cell-associated neurotoxicity syndrome which require special equipment and expertise of the healthcare professionals to be administered safely. According to the DeLLphi-301 study, the occurrence rate of cytokine release syndrome in patients receiving the approved 10 mg dose was 51%, including grade 3 or higher cases in 6% of patients.

The requirement for inpatient monitoring during the initial treatment cycles creates significant logistical challenges. such as added costs for patient care besides the cost of the drugs, oncology bed scarcity due to need for prolonged monitoring, and interference in the workflow of community cancer centers that do not have processes in place for managing bispecific T-cell engagers. Neurological adverse effects like immune effector cell-associated neurotoxicity syndrome were observed in 10% of the participants, 6% of which had grade 3 or higher toxicity.

Safety factors that are associated with this treatment will limit its use to bigger academic hospitals, cancer centers, and community oncology clinics equipped with the right infrastructure; thus, its immediate penetration into the market will not be achieved in the smaller healthcare facilities and rural clinics where many of the patients suffering from cancer seek treatment. Toxicity management requires extensive healthcare provider training.

The most important potential areas for market growth for tarlatamab-dlle include its clinical development as first- and second-line therapies in combination with other treatments for small cell lung cancer such as platinum-etoposide chemotherapy and PD-L1 checkpoint inhibitors. The drug is currently used for the treatment of small cell lung cancer that has become resistant to platinum treatment; however, the patient population eligible for the treatment constitutes only a small portion of all small cell lung cancer patients.

Current phase III studies such as DeLLphi-304 evaluating tarlatamab-dlle in combination with carboplatin, etoposide, and atezolizumab as a first-line treatment for extensive-stage small cell lung cancer represent significant commercial opportunities. In case combination therapies are found to be more effective than existing standards of care, tarlatamab-dlle can become the base for treatment as opposed to being used only as a salvage one, increasing its potential patient pool by 4-5 times and prolonging average treatment period per patient.

The scientific background of combination therapies is rather convincing because chemotherapy-induced immunogenic cell death will increase DLL3 antigen presentation, whereas checkpoint inhibitors’ use will keep T-cell activation and prevent T-cell exhaustion on account of extended bispecific T-cell engager therapy. Preliminary clinical results indicate synergistic mechanisms of action of T-cell redirection by tarlatamab-dlle and immune reinvigoration through checkpoint inhibitors.

A key trend is the transition from inpatient to outpatient administration of tarlatamab-dlle. to outpatient infusion centers and even community oncology clinics as healthcare practitioners acquire more experience in dealing with cytokine release syndrome and immune effector cell-associated neurotoxicity syndrome. The first release of the drug necessitated inpatient treatment due to safety concerns, but experience shows that most adverse events can be controlled when prophylactic measures are undertaken.

Standardization in toxicity management practices, training initiatives for healthcare professionals, and innovations in monitoring solutions, such as wearable technology and telehealth tools, make it possible to implement the approach into different healthcare environments. It is vital to make sure that access to the drug becomes available not only at academic medical institutions but also among community oncology practices that care for most cancer patients.

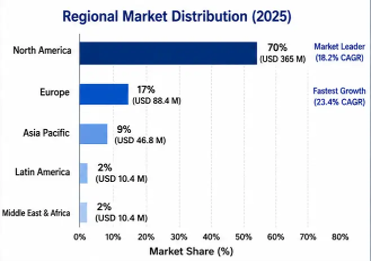

Market share in North America was the largest with USD 365 million in 2025, accounting for 70% of total worldwide tarlatamab-dlle sales and expected CAGR of 18.2% through 2034. US accounts for 89% of regional sales owing to FDA accelerated approval in May 2024, coverage by Medicare and commercial payers for approved indications in oncology, and existing bispecific T-cell engager administration facilities in major cancer centers across the country.

The market is driven by Amgen’s substantial oncology commercial capabilities, strong ties with National Cancer Institute-designated comprehensive cancer centers, and patient assistance program for uninsured and underinsured patients. Quick incorporation in National Comprehensive Cancer Network treatment guidelines and formulary uptake at leading healthcare facilities led to the rapid uptake in eligible patients with relapsed or refractory extensive-stage small cell lung cancer.

Europe is the fastest growing region with CAGR of 23.4% forecast until 2034 and is expected to transition from clinical trial availability to commercial availability after 2026 when European Medicines Agency is expected to approve the drug. Europe has centralized healthcare systems that allow for quick adoption of the standard-of-care after completion of health technology assessments, cancer registry systems allowing for patient identification, and experience with managing complicated immunotherapy treatments in specialized cancer centers.

The countries with the highest value among all other European countries will be Germany, France, and the UK, considering the presence of developed healthcare systems, framework of reimbursement for innovative oncological drugs, and high incidence of lung cancer.

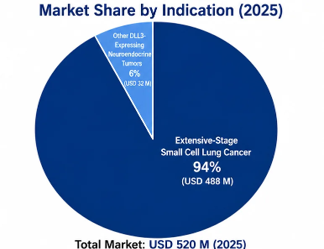

Extensive Stage Small Cell Lung Cancer is the leading market segment with a 94% market share worth USD 488 million in 2025, which is the current approved indication for patients experiencing progressive disease during or after treatment with platinum-containing chemotherapy. The Extensive-Stage Small Cell Lung Cancer segment will remain the dominant market segment. until 2034 owing to possible indication expansion to second line setting post-DeLLphi-303 Phase III trial outcome. Other DLL3-Expressing Neuroendocrine Tumors comprise the upcoming market segment having a current market share of 6%, while exhibiting a CAGR of 28.7%.

Third Line and beyond holds market share of 76% for USD 395 million in 2025, which is reflective of the approved patient pool having undergone two or more lines of therapy. Second-Line Therapy holds 24% market share currently but will emerge as the dominant segment in the future once the DeLLphi-303 data is released in 2026 and will hold 58% of the market by 2030 if the results from Phase III studies favor label expansion. First-Line Maintenance is a new segment with insignificant revenues currently, but high growth potential in the future.

The Hospitals & Cancer Centers segment accounted for 68% of the market, valued at USD 354 million. in 2025, based on the existing need for administrative facilities and in-patient monitoring in the first cycle of treatment. The Academic Medical Centers are another segment that accounts for 21% of the market share, playing the major role in clinical trials and initial commercialization. The specialty oncology clinics are expected to be the fastest growing segment with 24.8% CAGR.

Tarlatamab-DLL3 market currently exists in a monopolistic setting dominated by Amgen Inc. due to Amgen’s proprietary development of the first-ever bispecific T-cell engager for solid tumors together with the broad scope of intellectual property rights related to DLL3-targeted bispecific antibodies. The main competitive strengths of Amgen Inc. are represented by the position as the first company in the DLL3-targeting field, robust production facilities for complex bispecific antibodies, strong oncology commercialization platform, and continued clinical programs aimed at expanding indications.

Tarlatamab-dlle has no commercial competition at present, but the DLL3-targeting area has several other clinical-stage products under development by various firms, such as Roche, Bristol-Myers Squibb, and Johnson & Johnson, in terms of alternative bispecific constructs, antibody drug conjugates, and DLL3-targeted CAR-T cells. Amgen’s priority is to establish tarlatamab-dlle as the standard DLL3-targeting product prior to its competitors launching their products commercially.

The competitive landscape could change significantly if alternative DLL3-targeting therapies demonstrate superior efficacy, safety, or ease of administration., safer, and easier to administer in clinical trials. Nonetheless, the vast patent protection that Amgen has along with the advantages in manufacturing scale and clinical trials will form formidable barriers to entry for its competition in the coming period.

May 2024: The FDA approved tarlatamab-dlle (IMDELLTRA) for treatment of extensive-stage small cell lung cancer in adult patients who have progressive disease after being treated with platinum-containing chemotherapy drugs under accelerated approval based on DeLLphi-301 study's objective response rate and duration of response.

March 2026: Amgen provided topline positive results of DeLLphi-303 Phase III clinical trial indicating that there is a statistically significant increase in overall survival of tarlatamab-dlle when compared with topotecan as second-line treatment. The submission for label expansion is expected to be made in Q3 2026.

February 2026: European Medicines Agency Committee for Medicinal Products for Human Use provided positive opinion on conditional marketing authorization of tarlatamab-dlle with European Commission decision expected in Q2 2026.

January 2026: Amgen commenced Phase III DeLLphi-304 study investigating the safety and efficacy of tarlatamab-dlle along with carboplatin, etoposide, and atezolizumab in first-line treatment of extensive stage small cell lung cancer among participants enrolled at 200 locations worldwide.

December 2025: Amgen announced Phase II clinical trial of subcutaneous injection of tarlatamab-dlle with promising efficacy results as compared to intravenous administration with lower CRS incidence rate.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.