Share this link via:

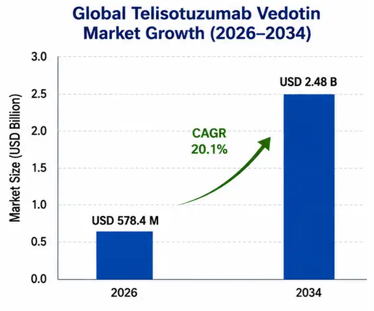

The global telisotuzumab vedotin market size was valued at USD 425.8 million in 2025 and is projected to reach USD 578.4 million in 2026, expanding to USD 2.48 billion by 2034, growing at a CAGR of 20.1% during the forecast period (2026-2034).

Telisotuzumab vedotin is a novel antibody-drug conjugate designed to specifically bind the c-Met receptor tyrosine kinase, which is an important oncogenic receptor critical for tumor cell proliferation, invasion, metastasis, and resistance to therapy in various solid tumor cancers. This complex molecular structure features a humanized anti-c-Met monoclonal antibody linked to a protease-cleavable valine-citrulline peptide, which carries a highly potent microtubule disrupting cytotoxic agent, monomethyl auristatin E (MMAE). This targeted delivery system allows receptor mediated endocytosis of the cytotoxic agent in c-Met expressing tumor cells, thus maximizing the tumor killing effects, while limiting systemic toxicity over conventional chemotherapy.

The c-Met signaling pathway activates downstream cascades such as the PI3K/AKT pathway, RAS/MAPK pathway and STAT3 pathway that all participate in regulating cell proliferation, survival, motility and angiogenesis. The mechanisms of dysregulation involve gene amplification, activating mutations, protein overexpression, and alternative splicing events, and c-Met was found to be overexpressed in 25–50% of non-small cell lung cancers, 20–35% of gastric cancers, 15–30% of colorectal cancers and in important numbers of hepatocellular, head and neck, and other solid tumors. This wide distribution across the spectrum of malignancies creates significant patient populations with little effective therapeutic options after failure of standard of care therapy.

Telisotuzumab vedotin has the most significant clinical effect when administered to patients with advanced solid tumors with high protein overexpression of c-Met, who have failed other standard therapies. Addressing an important unmet medical need in biomarker selected populations, including EGFR wild-type non-small cell lung cancer patients who do not have actionable driver mutations that can be targeted by drugs. This class of patients has limited available effective therapies when progressing on platinum-based chemotherapy and immune checkpoint inhibitors, and there is significant unmet need for which telisotuzumab vedotin is designed to directly address with precision targeted action.

The business opportunity extends beyond pharmaceutical revenues but in the whole precision oncology ecosystem, including companion diagnostic testing, analysis protocols and focused infrastructure. The success of telisotuzumab vedotin drives the need for systematic c-Met expression testing using standardized immunohistochemistry assays, leading to an enabling synergistic expansion across the diagnostic service, pathological infrastructure and oncology treatment network. The therapy also represents a shift in targeted therapy and precision medicine from the traditional widespread cytotoxic treatment, providing new treatment guidelines for patient selection, treatment monitoring, and treatment optimization in oncology treatment.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 425.8 Million |

| Forecast Value | USD 2.48 Billion |

| CAGR | 20.1% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Europe |

| Segments Covered | By Indication, Therapy Line, Biomarker Status, Combination Regimen, End-User, Distribution Channel |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Merck & Co. Inc., Daiichi Sankyo Co. Ltd., Partner Therapeutics |

Get more details on this report - Request Free Sample

The primary structural force driving the expansion of the telisotuzumab vedotin market is the significant unmet medical need among patients suffering from solid tumors with c-Met overexpression who have undergone conventional treatment without any success in controlling their disease. Specifically, the group of non-small cell lung cancer patients who suffer from EGFR wild-type tumors with c-Met overexpression can be identified as the most underserved since these patients have no targetable driver mutation and tend to show poor outcomes in relation to immunotherapy. Patients in this group experience low objective response rates in second line and beyond at only 10-20% and median progression-free survival of 3-5 months.

Overexpression of the c-Met biomarker identifies a molecular subset of cancer patients with approximately 25-50% of non-small cell lung cancer patients, 20-35% of gastric cancer patients, and 15-30% of colorectal cancer patients; such a molecular subset of patients is quite large with more than 400,000 people in the world each year requiring targeted therapy for their condition with respect to the c-Met biomarker. While c-Met exon 14 skipping mutations are much smaller in proportion with successful treatment using small molecule tyrosine kinase inhibitors, c-Met overexpression is not addressed with any targeted therapy.

There is extensive preclinical and translational evidence on the role of c-Met overexpression in the development and progression of various cancers because of the function of the receptor in promoting survival, invasion, metastasis, and resistance to treatment of the tumors. Patients with c-Met overexpression tend to have more severe biology and prognosis, being resistant to current therapy with a need for alternative targeted treatment approaches.

Increasing regulatory recognition of the effectiveness of telisotuzumab vedotin in leading pharma markets is an important catalyst that will foster commercialization and market uptake. Regulatory approvals based on strong clinical trial data proving the effectiveness of the treatment through high rates of objective responses as well as durability of response among pretreated patients will create a new standard of care for selected biomarkers. This process of approval pathway validation will result in immediate access to the drug commercially and insurance coverage for its use.

Success of the regulatory process in the initial market creates a platform for approvals to follow in other markets through the review processes in Europe, Japan, and other key markets. Each regulatory approval creates an avenue for tapping into more patients as well as more revenue streams, since Europe accounts for about 28% of the world’s expenditure on oncology pharmaceuticals, while the Asia Pacific region is gaining market share due to large patient population and better healthcare infrastructure.

The biomarker-driven regulatory approach sets the stage for implementing precision medicine approach to achieve optimal outcomes. The approval process provides validation for the use of precision oncology approach.

The primary barrier to market uptake is the high cost of the therapy, which in turn brings about challenges in obtaining reimbursements from payers across various health systems worldwide. The price of advanced antibody drug conjugates is relatively high, considering the complicated process of their development, manufacturing, and overall clinical benefit they offer; the cost of the treatment per patient per year typically ranges between USD 150,000 and 250,000 in advanced countries.

Systems of healthcare that use frameworks for health technology assessment consider cost-effectiveness and comparative efficacy prior to reimbursement. This results in delay in making the drug available to patients 12-18 months after approval. The indication of the drug based on biomarkers even though being clinically relevant is limited in terms of the population size that it can target as opposed to an unselected indication. Prior authorizations, step therapy, and prescriber restriction may further limit access to the drug, especially in community oncology practices where administrative challenges and reimbursement issues can limit its use.

Markets outside the US that use centralized systems of price negotiations can be expected to request price discounts or restrictive utilization requirements that make it commercially less attractive than list pricing. Thus, the combination of premium pricing, challenging reimbursement process and selection of the population based on biomarkers create an inherent conflict between commercial and access goals.

Transformational commercial potential lies in the development of telisotuzumab vedotin-based combination therapies targeting an addressable patient population greater than that of c-Met overexpression alone using high selectivity and potentially improving the effectiveness by virtue of the complementary mechanism of action. It is scientifically justifiable to explore a combination therapy of telisotuzumab vedotin and immune checkpoint inhibitors because c-Met signaling causes immunosuppression in tumor microenvironments and the death of tumor cells caused by ADC can be immunogenic in nature.

Clinical studies evaluating telisotuzumab vedotin in combination with PD-1/PD-L1 inhibitors are yielding initial results that indicate increased response rate and sustainability compared to monotherapy. The success of the combination would increase the potential target group to also include those with intermediate levels of c-Met expression. It would also allow for earlier lines of treatment positioning and would possibly counter the mechanisms of resistance to monotherapeutic treatments.

Other combination strategies that involve the use of telisotuzumab vedotin in combination with EGFR inhibitors in situations involving resistance of c-Met, in addition to anti-angiogenesis inhibitors, or other targeted therapies in selected biomarker groups are further options for expansion into additional indications.

Telisotuzumab vedotin is witnessing notable changes in the field of diagnostic testing that support effective patient selection and management. Whereas tissue-based immunohistochemistry testing continues to be the standard method used for measuring c-Met overexpression, recent technological advancements in liquid biopsy testing allow for non-invasive determination of c-Met expression using either circulating tumor DNA or circulating tumor cells. This addresses issues relating to the availability of tissues, but more importantly, allows for dynamic monitoring of biomarker expression during therapy.

AI-powered digital pathology tools provide greater accuracy and consistency in the process of scoring c-Met immunohistochemistry tests and eliminating any inter-pathologist variability which might affect patient selection. Application of machine learning algorithms to digital pathology images shows promise in identifying additional predictive factors beyond the biomarker expression score.

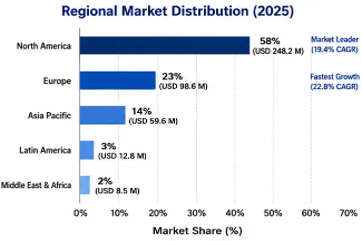

The North American region holds the largest market share of USD 248.2 million in 2025, contributing to 58% of the global market value with CAGR of 19.4% forecast till 2034. This is due to advanced infrastructure for the oncology treatment process, fast regulatory approval processes through the FDA breakthrough therapy designation, and reimbursement models that support novel cancer therapies. The US accounts for 89% of the regional market due to its high cancer burden and precision oncology treatment methods in place.

The region has strong clinical research capabilities that help in developing evidence, performing post-marketing trials and researching combination therapy options which will increase the applicability and commercial prospects for the drug. The coverage policies for Medicare and commercial insurers which demand prior authorization and medical necessity have created good opportunities for approval and usage of telisotuzumab vedotin among the eligible patients.

The European region is expected to be the fastest-growing regional market, expanding at a CAGR of 22.8% during the forecast period (2026–2034). The market was valued at USD 98.6 million in 2025 and is projected to witness robust growth over the forecast period. Growth is expected to be driven by sequential regulatory approvals and health technology assessment completions from major European regions, which include Germany, France, and the United Kingdom. In this region, once reimbursement approval is obtained, centralized healthcare systems facilitate market access following reimbursement approval.

Oncology centers in the European region have shown high incidence of comprehensive molecular profiling and biomarker-driven therapy selection. This makes this region the ideal place for the drug to penetrate the market and gain success.

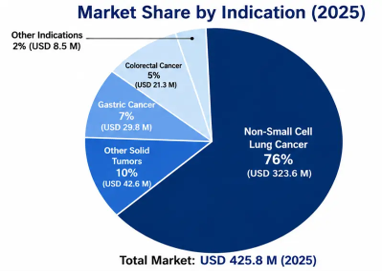

The leading segment is Non-Small Cell Lung Cancer, which accounts for 76% market share worth USD 323.6 million in 2025 owing to being the major approved indication and biggest addressable patient pool that has reliable testing for c-Met overexpression.

Other Solid Tumors and Gastric Cancer represent key future growth opportunities due to their ongoing clinical developments, which are reaching Phase II/III studies. Growth prospects of these segments are very promising as more clinical data is becoming available, and more indication extensions can become a reality. By 2034, they may contribute up to 35-40% of the total market value.

The Second Line and Third-Line therapy market segments combined make up 84% of the total market revenue, as these therapies have an approved position for use in patients who have already been treated using other treatments in the first line. The most promising area of opportunity lies within the First-Line therapy market segment.

The market for telisotuzumab vedotin is characterized by a unique antibody-drug conjugate environment where direct competition in the c-Met-targeted ADC space remains limited. However, there is a competitive market where other oncology therapeutics compete for the market share. Patent protection grants the innovator market exclusivity while being faced with future competition from biosimilars and competing c-Met-targeted products.

March 2026: Acceptance of regulatory filing for telisotuzumab vedotin in c-Met positive non-small cell lung cancer for the EU, with conditional marketing approval expected by end of 2026.

February 2026: Start of phase II trial testing telisotuzumab vedotin with pembrolizumab as first-line therapy for c-Met positive non-small cell lung cancer; results from primary endpoint expected in 2028.

January 2026: Expansion of companion diagnostic collaboration to use automated immunohistochemistry systems, which would facilitate better standardization and availability of c-Met testing in global pathology labs.

December 2025: Completion of regulatory filing for telisotuzumab vedotin in Japan with priority review status, which should help speed up approval by mid-2026.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.