Share this link via:

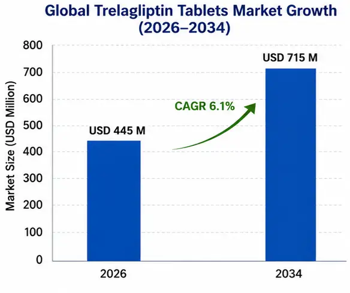

The global trelagliptin tablets market size was valued at USD 405 million in 2025 and is projected to reach USD 445 million in 2026, expanding to USD 715 million by 2034, growing at a CAGR of 6.1% during the forecast period (2026-2034).

The world's first and only weekly oral DPP-4 inhibitor, Trelagliptin is a paradigm-shifting innovation in the type 2 diabetes mellitus (T2DM) pharmacotherapy that fundamentally changes the way diabetes is managed by tackling the most significant challenge in effective diabetes management adherence. Trelagliptin, commercially available as Zafatek, works by highly selective and reversible DPP-4 inhibition, which sustains the effect of the endogenous incretin hormones, GLP-1 and GIP, to promote glucose-stimulated insulin secretion and inhibit inappropriate glucagon secretion by physiologically harmonious mechanisms that reduce the risk of hypoglycemia.

Trelagliptin has a unique pharmacokinetic profile, with molecular engineering providing plasma half-life characteristics that are optimised for once-weekly use., with levels > 80% inhibited in the plasma for a weekly period high protein binding for greater sustained systemic exposure, and tissue distribution properties that provide therapeutic levels at the target sites over the weekly dosing interval. This pharmacological architecture was carefully developed to offer the glycemic effect of constant DPP-4 inhibition, with reduction of medication administration frequency from 365 doses per year to only 52 doses per year, facing the medicine adherence crisis which affects up to 50% of patients in the first year of treatment initiation.

Beyond its pharmaceutical breakthroughs, trelagliptin's commercial promise lies in its potential as a patient-centric therapeutic option, offering a solution to the multifaceted nature of diabetes treatment, burden, and adherence in real-world settings. An established safety profile of cardiovascular neutrality and low hypoglycemia risk when used as monotherapy along with favourable tolerability in elderly and renally impaired patients makes the drug attractive to use in patients with various demographics, with once-a-week convenience offering a strong competitive differentiation in the very competitive oral antidiabetic market that remains dominated by daily dosing.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 405 Million |

| Forecast Value | USD 715 Million |

| CAGR | 6.1% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Middle East & Africa |

| Segments Covered | By Indication, Dosage Strength, Patient Demographics, Distribution Channel, End-User |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | Japan, China, India, South Korea, Bangladesh, Thailand, Indonesia, Brazil, Mexico, UAE, Saudi Arabia, South Africa |

| Key Market Playes | Takeda Pharmaceutical Company, Beacon Pharmaceuticals, Incepta Pharmaceuticals, Square Pharmaceuticals |

Get more details on this report - Request Free Sample

Medication non-adherence is a major challenge in diabetes treatment, and the widespread non-adherence of patients in the first year of taking daily oral antidiabetic drugs is well established, as results from a series of comprehensive real-world studies confirm with adherence dropping to 30-35% by year three creating a strong opportunity for trelagliptin to stand out as a foundational growth driver for its expansion in the market. This failure to adhere poses catastrophic clinical consequences: suboptimal glucose control leads to the development of microvascular complications like diabetic nephropathy, retinopathy, and neuropathy, and macrovascular complications like coronary artery disease, stroke, and peripheral vascular disease, which are the major causes of diabetes-related morbidity, mortality, and health care costs.

Clinical evidence supporting the adherence benefits of once-weekly therapy is compelling.: comparative effectiveness studies have shown that medication possession ratios for weekly oral therapy are 78-84% over 12-month time periods, versus 52-61% for daily therapy, which directly correlates to the clinical improvement seen in the weekly oral therapy group, as reflected in HbA1c reductions, which were maintained at clinically meaningful levels during the extended follow-up period. The adherence benefit is even more notable in elderly adults, in which cognitive impairment, polypharmacy treatment burden and physical conditions that inhibit medication self-administration are significant challenges to adherence to daily dosing, and in which the weekly regimen of trelagliptin may provide important clinical utility.

The rapidly growing global type 2 diabetes epidemic is the primary structural driver of the market., with the International Diabetes Federation estimating 537 million adults were affected by type 2 diabetes globally in 2025 and a projected 783 million by 2045 the largest growing category of chronic diseases, with with new cases occurring every three seconds globally. The disease burden is heavy in the Asia-Pacific regions where trelagliptin is already commercially available China and India have 140 million and 77 million diabetes patients respectively, making for the world's largest addressable patient populations for oral antidiabetic therapy.

Demographic aging is giving rise to very favourable market conditions because patients aged 65 and above are the fastest growing segment of the diabetes population as well as being the most severely affected by the challenge of taking multiple medicines every day, with cognitive decline, increased complexity of medicine and reduced support systems. This demographic match is supported by Japan, as it was the first country to launch trelagliptin, a drug that has proven effective in this setting with a 7.4% prevalence of diabetes in the general population, and with 29% of its population aged 65 years and older.

The primary factor limiting the market potential of trelagliptin is its regulatory approval in the specific markets, which are mainly in Japan and some Asian countries, and the lack of regulatory approval in major western pharmaceutical markets such as the United States and European Union, thereby limiting commercial activity to Asian markets and reducing revenue diversification into higher value per-patient healthcare systems. The results of these comprehensive cardiovascular outcomes trials, adequate for current regulatory requirements, would require up to USD 400-600 million in development investment along the regulatory pathway to FDA and EMA approval.

The geographic restriction also significantly restricts the total revenues that can be generated from the sales of this oral antidiabetic pharmaceutical because the U.S. and European markets account for around 55-60% of the global revenue in this class. Takeda has not been investing heavily in this therapeutic area as there is a high saturation level in both the U.S. and European markets with established DPP-4 inhibitors and competitive pressure from newer therapeutic classes in the regions.

The most promising market opportunity lies with generic trelagliptin proliferation in emerging healthcare markets where branded medications remain unaffordable for the majority of the population., with pharmaceutical companies in countries such as Bangladesh, India and other Asian nations successfully creating and commercializing generic versions that cost a fraction of what branded medications do and offer convenient once-weekly dosing. The ability to create generic versions of trelagliptin allows healthcare systems to provide a superior level of convenience in dosing at affordable prices, which could allow them to expand their customer base from those who are insured in urban settings to more of their population who need cost-effective diabetes management strategies.

The potential for volume expansion in emerging markets is significant, and generic pricing allows treatment costs to be comparable to appropriate daily generics, yet treatment has better adherence properties, making the product a more suitable option for formulary and physician preference in the face of limited budgets in a health care system looking to achieve the best clinical outcomes within a budget constraint.

The trelagliptin market is increasingly intersecting with digital therapeutics. via connected pill dispensers, smartphone medication reminder apps, and diabetes management systems that take advantage of the regularity provided by once weekly dosing to ensure effective tracking and engagement. The once-weekly dosing regimen easily fits into the digital health check-ups process, providing for thorough glucose level monitoring sessions.

The accumulation of real-world evidence from Japan and emerging markets is adding more weight to the clinical value of trelagliptin through its effectiveness data, safety data in various population groups, and better adherence data that will help position the drug in more guidelines and payer coverage policies.

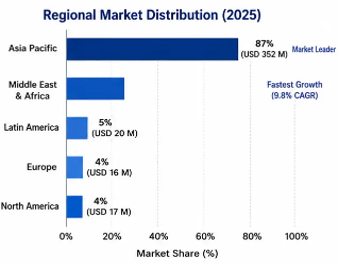

Asia-Pacific holds immense dominance in the market and constitutes 87% of global trelagliptin sales revenue amounting to USD 352 million in 2025, on the strength of its foundational market of Japan, wherein the drug gained immense traction in the category of DPP-4 inhibitors by virtue of its adherence benefits in the oldest nation of the world.

Japan is the dominant contributor to regional sales and accounts for 68% of regional revenues due to its well-accepted clinical profile and reimbursement status, besides the familiarity with the drug among physicians.

China represents the largest opportunity for market expansion. owing to the vast number of diabetes patients in the country amounting to 140 million in numbers. India, South Korea, and the Southeast Asia region are other options for regional expansion.

The Middle East & Africa is projected to be the fastest-growing regional market. for the forecast period up until 2034 at a projected CAGR of 9.8%, because of increasing imports of the generic trelagliptin in the face of increasing diabetes incidence in the GCC countries, and improving healthcare facilities in the Sub-Saharan countries in Africa.

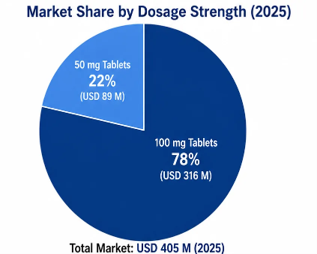

The 100 mg tablets have a high market share of 78%, with sales revenue reaching USD 316 million in 2025. They represent the therapeutic dose required for treatment in adults with normal or slightly decreased renal function, contributing substantially to the treatment revenue through the weekly dosage administration to the broad type 2 diabetes patient population. This dosage benefits from simplified prescribing without dose titration and effective data.

The 50 mg tablets represent 22% of the market share with revenue of USD 89 million in 2025. The patient population served by 50 mg tablets has a need for dose adjustment due to the decreased ability to clear trelagliptin caused by moderate to severe renal impairment.

The Retail Pharmacy segment holds a 48% market share at USD 194 million by 2025 on account of the one-time weekly administration route's compatibility with dispensing and self-administration by patients without the need for any clinical assistance. The Hospital Pharmacy segment has gained a market share of 32%, catering to initial treatment and patient management. The online pharmacy has gained a market share of 15%, growing at a CAGR of 11.2%.

Market share held by Hospitals & Clinics is around 52%, with revenue estimated to be USD 211 million by 2025, including endocrinology centers, internal medicine clinics, and primary care centers, which are responsible for treating the major chunk of type 2 diabetes population. The Endocrinology Centers have a market share of 28%.

The competitive landscape of the global trelagliptin tablets market for trelagliptin tablets is distinct in that Takeda Pharmaceutical controls the branded versions exclusively and competes with generic versions manufactured by new players in Asia and other emerging countries. Competitive advantages of Takeda Pharmaceutical include clinical proof, regulatory relations, and manufacturing expertise; competitive advantages of generic version manufacturers consist of cost-effectiveness and local distribution.

March 2026: Several generic manufacturers announced the expansion of trelagliptin manufacturing capabilities in response to rising demand in Southeast Asia and the Middle East, with their new factories expected to go into full operation by the fourth quarter of 2026.

January 2026: Evidence on trelagliptin effectiveness based on its use in the Japanese market showed reductions in HbA1c levels that were maintained for 48 months.

November 2025: The manufacturer Takeda Pharmaceutical announced additional patient support initiatives including the use of digital applications to monitor drug compliance during one weekly administration.

September 2025: Generic trelagliptin got approved in three more emerging markets.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.