Share this link via:

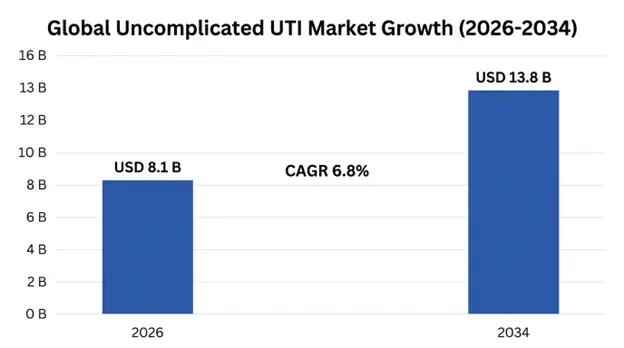

The global uncomplicated urinary tract infections market was valued at USD 7.2 billion in 2025 and is projected to reach USD 8.1 billion in 2026, expanding to USD 13.8 billion by 2034, growing at a CAGR of 6.8% during the forecast period (2026-2034).

Uncomplicated UTI refers to acute bacterial infections of the lower urinary tract, including cystitis and urethritis, that occur in otherwise healthy, non-pregnant individuals without structural urological abnormalities, immunosuppressive conditions, or other predisposing illnesses. Uncomplicated UTI is among the most commonly diagnosed infections worldwide, with an estimated 400–500 million cases reported annually, with females being more predisposed due to anatomical factors such as short urethra, closeness of the urethral meatus to the perianal area, and the impact of hormones on urogenital epithelium sensitivity to bacteria.

Clinical manifestations include dysuria, urinary frequency, urinary urgency, suprapubic pain, and occasionally hematuria, suprapubic pain, and sometimes hematuria; E. coli is responsible for 75-90% of pathogens involved in these infections among various geographical and sociodemographic groups. Pathogenesis involves ascending bacterial infection from the periurethral area through the urethra into the bladder through bacterial virulence factors such as type 1 fimbriae, that allow attachment to uroepithelial cells followed by invasion and development of intracellular bacterial communities.

The treatment landscape is undergoing significant transformation due to rising antimicrobial resistance and evolving healthcare delivery models. While traditional therapies such as nitrofurantoin, trimethoprim-sulfamethoxazole, and fosfomycin continue to retain their significance in multiple markets, resistance against such first-line therapies has been on the rise over time. This growing threat has necessitated the need for development of alternative therapeutic options. Resistance rates among E. coli to fluoroquinolones have reached 20%–35% in Europe and exceed 40% in selected Asian markets, while resistance to trimethoprim-sulfamethoxazole ranges between 15%–25% in North America and Europe.

Market Architecture: Generic antibiotics account for the majority of prescriptions, while newer premium therapies include novel oral antibiotics targeting multidrug-resistant pathogens, non-antibiotics used as prophylactics against recurrent diseases, and technology platforms that help in remote diagnostics and treatments. Market value extends beyond drug sales to include integrated care ecosystems involving rapid diagnostics, antimicrobial stewardship, patient education, and outcomes-based reimbursement systems involving fast diagnosis, antimicrobial stewardship, patient education, and outcomes-based payments systems.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 7.2 Billion |

| Forecast Value | USD 13.8 Billion |

| CAGR | 6.8% |

| Forecast Period | 2025-2034 |

| Historical Data | 2022-2025 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | By Drug Class, Pathogen, Treatment Setting, Patient Demographics, Distribution Channel |

| Region Covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

| Countries Covered | US, Canada, Mexico, UK, Germany, France, Italy, Spain, Netherlands, China, Japan, India, Australia, South Korea, Brazil, Argentina, UAE, Saudi Arabia, South Africa |

| Key Market Playes | GlaxoSmithKline plc, Iterum Therapeutics plc, Utility Therapeutics, Shionogi & Co. Ltd., Merck & Co. Inc., Pfizer Inc., Bayer AG |

Get more details on this report - Request Free Sample

Key Factors Driving Structural Changes in the UTI Market

A key factor driving changes in the straightforward UTI market structure is the rising global challenge of antibiotic resistance, which has increasingly compromised existing empirical treatment guidelines, thus offering strong business potential in new products that can deal with resistant uropathogens. In the case of fluoroquinolone resistance by Escherichia coli, which is responsible for 75-90% of uncomplicated UTIs, resistance levels have become significant in leading global health markets such that European countries record 20-35%, South and Southeast Asian nations have 40-55% prevalence while North American communities record 15-22% resistance making fluoroquinolones unreliable in empirical treatment.

Resistance is now being faced by several groups of antibiotics simultaneously, leading to progressively narrower treatment alternatives based on empirical treatment principles. ESBL-producing strains of E. coil that were initially isolated from only hospital settings have spread to become community-acquired causes of urinary tract infections, comprising up to 5-12% and 8-15% of cases of uncomplicated UTIs in Europe and Asia, respectively. This results in failures of oral beta-lactam antibiotics unable to overcome resistance mechanisms.

Such treatment failures increase the need for additional antibiotic use, urine culture testing, and, in some cases, hospitalization for parenteral therapy, but also create an intense demand for new therapeutics on the market. The pipeline for new uncomplicated UTI antibiotics has become increasingly dynamic, as exemplified by Phase III data confirming non-inferiority to nitrofurantoin of a new triazaacenaphthylene antibiotic gepotidacin, which retained activity against fluoroquinolone-resistant strains, and by novel thiopenem oral antibiotic sulopenem.

Key Performance Metrics:

The fundamental epidemiological driver of sustained market demand is the high prevalence of uncomplicated UTIs, especially amongst females irrespective of their age groups. The lifetime incidence rate in females is estimated at 50-60%, whereas the yearly incidence rate for sexually active younger females is 0.5-0.7 episodes per person year and higher rates for the post-menopausal population suffering from changes in urogenital conditions due to estrogen deficiencies. The recurrent UTI population, comprising patients who experience two or more infections in 6 months or three or more cases in 12 months, consists of about 25-35% of patients infected once.

Management of recurrent UTIs extends beyond acute treatment and often includes antibiotic prophylaxis, non-antibiotic approaches, and thorough diagnosis, making for a long-term treatment relationship that adds therapeutic worth throughout life. In particular, the postmenopausal population shows significant incidence of recurrence of infection, where about 10-15% of postmenopausal females suffer from recurrent infections requiring prolonged treatment.

Disease Burden Impact Metrics:

The primary factor limiting market value expansion is the widespread availability of generic antibiotics across multiple therapeutic classes, resulting in constant pressure from prices, which prevents growth even in cases when high prescription volume is observed. First-line drugs such as nitrofurantoin, trimethoprim-sulfamethoxazole, and fosfomycin have been out of patents for a long period, while their generic versions can be found on the market at prices of USD 8-25, compared to USD 150-350 required by new branded drugs.

Generic Competition Impact:

Antibiotic prescribing policies developed across several countries to limit the over-prescription of antibiotics include systematic limits on antibiotic prescriptions by requiring diagnostics, limiting the time for treatment and restricting the practice of empiric treatment. The WHO Global Action Plan on Antimicrobial Resistance has led to national programs that minimize the use of antibiotics and prescribe culture-specific treatments.

Stewardship Program Impact:

Significant commercial opportunities exist for next-generation antibiotics that demonstrate efficacy against fluoroquinolone-resistant and multidrug-resistant uropathogens with innovative mechanisms that provide a proven record of activity against both fluoroquinolone-resistant and multidrug-resistant uropathogens. Gepotidacin is currently the leading innovative candidate with a novel mechanism of action, using triazaacenaphthylene chemistry to inhibit DNA replication by bacteria at target sites other than those affected by fluoroquinolones, demonstrating strong efficacy against fluoroquinolone-resistant E. coli with non-inferiority to nitrofurantoin demonstrated in a pivotal Phase III trial.

Other innovations under development in addition to Gepotidacin include oral sulopenem which provides thiopenem class efficacy against ESBL-producing uropathogens, zoliflodacin providing unique topoisomerase inhibition with spiropyrimidinetrione chemistry, and repurposed drugs like pivmecillinam with approval now pending in other geographic territories. Significant commercial opportunities exist due to the cost of treatment failures, particularly when hospitals are willing to pay a premium price to avoid admissions.

Novel Antibiotic Opportunity Metrics:

UTI prevention in recurrent cases presents an attractive niche for approaches that are not antibiotics for the 25-35 % of females affected by UTIs that require long-term management rather than short-term treatments. Vaccine-based approaches directed against bacteria using urovirulence factors such as the FimH adhesin and Type 1 fimbriae present the most innovative option with clinical trials showing 40-65 % fewer recurrences without antibiotic administration.

Alternative approaches which include the use of D-mannose, cranberry extracts, vaginal estrogen treatments for post-menopausal women and bacteriophages provide prophylactic benefits alongside growing patient/clinician preferences for reduced use of antibiotics.

Prophylaxis Market Opportunity:

The incorporation of innovative diagnostic technologies that will facilitate fast identification of pathogens and susceptibility testing for antibiotics is a disruptive trend in UTI patient care. Diagnostic technologies utilizing PCR-based molecular analysis can identify pathogens and antimicrobial resistance genes will help identify such pathogens as E. coli and Klebsiella pneumoniae and resistant genes like ESBL determinants and fluoroquinolones resistance genes in just 30-90 minutes.

These rapid diagnostic capabilities help overcome the limitations associated with the 24–48-hour turnaround time required for traditional urine culture results in traditional urine cultures. Historically, that necessitated choosing the antibiotics empirically by taking into consideration population resistance patterns rather than susceptibility patterns of an individual patient. Home-based sample collection and mail-in testing in combination with telehealth are especially innovative.

Diagnostic Integration Impact:

Artificial intelligence and machine learning technologies are increasingly being integrated into UTI management through symptom-scoring algorithms, risk prediction models, and antibiotic selection support tools, risk scoring models, and recommendations for optimal antibiotics based on patient history and local resistance profiles. UTI management systems are being developed using digital health technologies to support an ecosystem for UTIs including education, monitoring of symptoms and adherence.

Such platforms allow for implementing stewardship programs, personalized medicine programs, and even generating real-world evidence that would support regulatory approvals and reimbursement for new drugs.

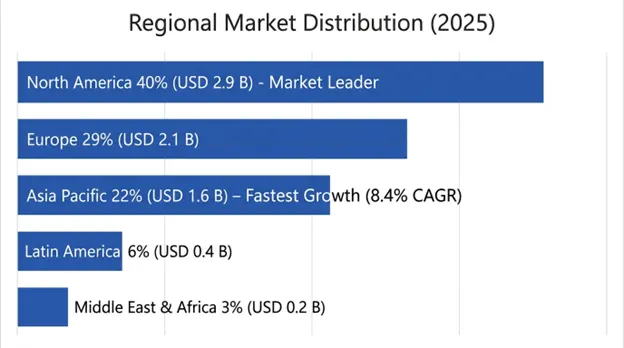

North America held the maximum share of the market, worth USD 2.9 billion in 2025, and is forecast to retain a projected CAGR of 6.5% up until 2034. The dominance of North America can be attributed to the widespread provision of health insurance coverage, well-established primary care facilities, and the US being the first market for launching new antibiotics. The Generating Antibiotic Incentives Now Act grants additional market exclusivity on QIDs and hence offers conducive commercial conditions for novel UTIs.

North America demonstrates the highest adoption of telemedicine services for UTI management, and the total number of episodes managed by large service providers exceed 4.8 million per year. Full insurance coverage, including tests and antibiotics, under Medicare and commercial payers makes the acceptance of expensive novel drugs possible.

North American Performance Metrics:

In Europe, the region was valued at USD 2.1 billion in 2025 based on an estimated 6.2% CAGR during 2025-2034 owing to advanced stewardship policies, robust resistance surveillance systems, and advancements in culture-directed therapy guidelines. The four major countries of Europe that together accounted for 64% market share include Germany, France, United Kingdom, and Italy with different prescribing behaviors.

The regulatory policies in Europe focus on conservation of antibiotics where restrictions have been imposed by the European Medicines Agency on fluoroquinolone use in uncomplicated UTIs due to high resistance rate and first-line drugs considered include nitrofurantoin and fosfomycin.

European Market Characteristics:

Asia-Pacific proved to be the leading regional market with estimated CAGR of 8.4% until 2034, to reach USD 1.6 billion in 2025. The regional market growth can be attributed to the high prevalence of UTIs owing to huge population size along with increasing healthcare accessibility and the presence of highest antimicrobial resistance rates across the globe.

The potential growth markets include China and India due to huge population sizes and increased healthcare spending whereas Japan, South Korea and Australia exhibit higher adoption of novel therapies and diagnostics. The presence of the highest global antimicrobial resistance rates makes it an opportunity and challenge at the same time.

Asia Pacific Growth Drivers:

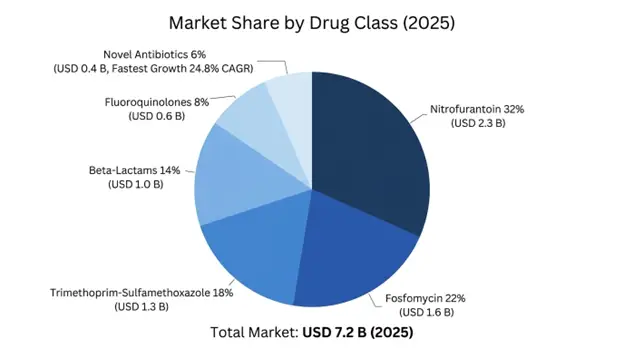

Nitrofurantoin holds the maximum share of 32%, estimated to be worth USD 2.3 billion by 2025 with a CAGR of 5.8% through 2034. It is preferred as the first choice of treatment based on the global guidelines due to its high susceptibility rate (greater than 95%) and proven safety profile. The multiple mechanisms of action targeting cell wall synthesis, DNA replication, and cellular respiration in bacteria make it resistant to developing resistance.

The fosfomycin segment is expected to grow with a share of 22% in the urinary tract infection market at USD 1.6 billion with a growth rate of 8.4%. Trimethoprim-sulfamethoxazole shares hold 18%, worth USD 1.3 billion, showing negative growth because of increasing resistance in many parts of the world while being effective in some regions based on susceptibility rates. Novel antibiotics share 6%, valued at USD 432 million and growing at 24.8%.

Escherichia coli has the largest share of 84%, due to its being the causative agent in most of the uncomplicated UTIs. E. coli strains show growing resistance towards multiple classes of antibiotics, leading to high demands for development of innovative treatment strategies. S. saprophyticus has 8% share and affects mainly young women who practice active sex life. K. pneumoniae has only 4% share but is highly resistant, producing ESBLs.

Primary Care & Outpatient Clinics will have the maximum market size in terms of value with USD 3.9 Billion at 54% Market Share in 2025, with most uncomplicated UTIs being managed by general physicians or urgent care. Telemedicine Platforms have a 28% Market Share with USD 2.0 Billion and will be growing at 18.6% CAGR and is the fastest growing segment.

The global market for uncomplicated UTIs consists of two categories of competition, namely; a highly volume-driven generic market controlled by established brands such as Teva Pharmaceuticals, Sandoz, and Sun Pharmaceuticals with competition on basis of logistics efficiency and price, and innovative bio-pharmaceutical companies like Glaxo Smith Kline, Iterum Therapeutics, and Shionogi which compete on their premium antibiotic products using innovation, clinical advantages, and patient support programs.

April 2026: GlaxoSmithKline announced FDA approval for Gepotidacin for uncomplicated UTI, which marks the first new oral antibiotic class to be approved for the treatment of UTIs for more than 20 years, with commercial introduction anticipated in Q3 2026.

March 2026: Iterum Therapeutics presented real-world evidence from studies of oral Sulopenem showing 94% clinical success rates for treating UTIs caused by ESBL-producing E. coli where intravenous therapy was required.

February 2026: Pivmecillinam availability increased in North American markets as a result of positive phase III study results proving its efficacy in the treatment of fluoroquinolone-resistant uropathogens.

January 2026: FDA published final guidance for UTI clinical trial design including primary endpoint criteria and patient definition, allowing easier development of new drugs in this field.

December 2025: Major telemedicine company introduced at-home UTI diagnostic test to enable full virtual treatment process from initial symptom identification to prescribing specific antibiotics within a day.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

23 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.