Share this link via:

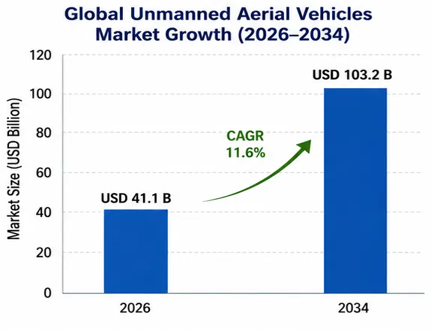

The global unmanned aerial vehicles market size was valued at USD 36.2 billion in 2025 and is projected to reach USD 41.1 billion in 2026, expanding to USD 103.2 billion by 2034, growing at a CAGR of 11.6% during the forecast period (2026-2034).

UAVs represent one of the most transformative developments in modern aviation and defense systems and span a wide range of remotely piloted and autonomously controlled aircraft from smaller nano-drones that weigh less than 10 grams, to strategic high altitude long endurance aircraft with wingspan greater than 40 meters and endurance exceeding 40 hours of continuous flight. These advanced systems have fundamentally transformed operational paradigms across military, commercial, civil, and consumer sectors, allowing for continued aircraft presence, precise payload delivery, extensive sensor coverage, and complex mission operations without risk to human operators, costs, and physiological limits of manned aviation platforms.

Modern UAVs incorporate a complex array of technological systems, including aerodynamic structures designed for specific missions, advanced propulsion systems from electric motors for commercial quadcopters to turbofan engines for strategic reconnaissance missions, full avionics suite that includes inertially guided navigation systems and GPS receivers, terrain-following algorithms, collision avoidance systems, as well as a variety of payloads, including electro-optical and infrared cameras, synthetic aperture radars, electronic intelligence sensors, communications relay equipment, precision munitions, cargo delivery mechanisms, and specific scientific instruments. Miniaturized electronics, advanced battery technologies, AI processing power, advanced communications, and autonomous decision-making algorithms have dramatically increased the operational envelope and lowered costs to an extent that has led to commercial and consumer adoption.

The strategic and commercial value of UAVs extends across modern society and military operations, having a significant impact on the way organizations operate in their intelligence collection, logistics delivery, infrastructure inspection, agricultural management, emergency response and combat operations. In the defense sector, the introduction of UAVs has revolutionized the way intelligence, surveillance, and reconnaissance are conducted, precision strike delivery is executed, electronic warfare is managed, and force protection is provided, all while acting as a force multiplier through persistent surveillance that cannot be costed or manned in the same way as a manned aircraft. UAV technology has been adopted by commercial operators for precision agriculture monitoring, with the use of multispectral imaging; for comprehensive infrastructure inspections which minimize risk to humans; for last-mile logistics delivery, for rapid supply chain optimization and for construction site management by automated progress monitoring, and for emergency response co-ordination, providing real-time situational awareness during crisis situations.

|

Market Metric |

Details & Data (2026-2034) |

|

2025 Market Valuation (Base Year) |

USD 36.2 Billion |

|

2026 Estimated Value |

USD 41.1 Billion |

|

2034 Projected Value |

USD 103.2 Billion |

|

CAGR (2026-2034) |

11.6% |

|

Market Scope |

2022-2034 |

|

Report Coverage |

Revenue Forecast, Technology Assessment, Combat Validation Analysis, Regulatory Landscape, Payload Integration, Autonomy Development, Competitive Intelligence |

|

Segments Covered |

By Class, Type, Mode of Operation, Application, Payload, End-User |

|

Geographies Covered |

North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

|

Countries Covered |

US, Canada, Mexico, UK, Germany, France, Italy, Israel, Turkey, China, Japan, India, Australia, South Korea, UAE, Saudi Arabia, Brazil |

|

Dominant Region |

North America |

|

Fastest Growing Region |

Asia Pacific |

|

Key Market Players |

General Atomics, Northrop Grumman, Lockheed Martin, DJI, AeroVironment, Textron Systems, Elbit Systems, Skydio |

A key factor transforming the global UAV market is the proven operational effectiveness of unmanned systems that unmanned systems offer in various fronts of active warfare, which has completely influenced military procurement policies in defense institutions around the world. The war in Ukraine has produced the widest operational experience in the field of UAS operations in history, showcasing UAS capabilities in reconnaissance, precision strike, electronic warfare, logistics support, and psychological operations – and highlighting the vulnerabilities of UAS to electronic countermeasures and kinetic counter-UAS systems. Armed UAS have proven to be effective in Ukraine, particularly the commercially available DJI quadcopter with modifications for munitions delivery and the purpose-built platforms of Turkish origin, the Bayraktar TB2, plus domestic solutions, consuming thousands of platforms each month, and proving the versatility of unmanned systems across tactical applications.

The Nagorno-Karabakh conflict proved that low-cost tactical UAVs can systematically neutralize conventional armored formations, air defense systems, and logistics infrastructure, and provide strategic effects that would have previously called for much larger and more expensive manned aviation assets. It has influenced procurement decisions in dozens of countries that were previously hesitant to use UAS, providing the impetus for national modernization programs that are focused on accelerating the integration of UAS into all service branches. In the Middle East, UAVs have been further proven with Israeli precision strike campaigns, Houthis attacks with one-way attack platforms, and Iranian proxy use of UAVs with one-way attack platforms, making UAVs a focal point of modern combined arms warfare that demands specific doctrine, training and procurement.

The commercial UAV market is experiencing unprecedented growth with the systematic development of comprehensive regulatory frameworks that will enable Beyond Visual Line of Sight (BVLOS) operations, urban air mobility integration and scaled autonomous deployment by major aviation authorities around the world. The Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), and other key regulators have increasingly developed standardized certification processes for BVLOS operations, integration of Unmanned Aircraft Systems (UAS) into air traffic management, operations over populated areas, and advanced air mobility type certification, all moving commercial drone operations from the limited experimental exemption to a structured framework for viable services at scale.

These regulatory milestones have created significant economic opportunities in various commercial sectors, including automated inspection operations, autonomous delivery networks in remote and urban areas, precision agriculture applications with advanced sensor integration, and emergency response systems that provide real-time situational awareness during disasters and security events, to name a few. Establishing repeatable, optimized, and economically viable operations through the introduction of standardized operational categories, standardized remote pilot certification, and risk-based approval processes will help commercial operators to operate more efficiently without having to perform a series of costly demonstrations to earn approval from the industry regulator.

Regulatory frameworks governing unmanned aircraft operations at national, regional, and local levels remain highly complex and inconsistent, posing significant compliance challenges that limit the flexibility of operations, deployment costs and the ability to implement economically optimal service models across markets. In addition to Visual Line of Sight operations, which are fundamental and crucial in the economic viability of delivery services, infrastructure inspection and large area surveillance missions, for which specific regulatory authorizations are required, are not available or very restricted in many key markets, restricting commercial operators to VLOS operations and drastically reducing the coverage areas and costs of the services operated.

In the case of UAM operations, the regulatory process is complicated, especially because the safety cases to be demonstrated are historic for commercial aviation, the vehicle designs that have never been certified have no performance databases yet, the new vehicle operating in the airspace must be integrated into the existing air traffic management system, which is designed for manned aircraft that have different performance envelopes, and local airspace may be restricted by regulatory authorities. The lack of internationally agreed standards leads to the scenario of non-uniform regulatory frameworks which means that operators face different approval procedures, technical requirements and operational constraints in each jurisdiction, increasing the costs of compliance and significantly delaying the commercial services launches in multi-national markets.

The need for extensive risk assessment, environmental impact assessment, security clearance checks and continuous monitoring during operation generates high administrative burden that disproportionately impacts smaller enterprises and startups, which may not have the resources to manage the complex bureaucracy and thereby inhibit diversity and innovation in commercial markets.

The development and commercialization of heavy-lift cargo UAVs represent one of the most significant market opportunities that can carry a payload ranging from 100kg to more than 1,000kg is one of the most significant gaps in the global logistics infrastructure that could lead to new and reimagined service models in the transport of goods, supplies, and goods across the region that would otherwise demand manned aircraft. This middle mile logistics corridor provides significantly faster point-to-point transport than ground transport, but costs much less than traditional manned cargo aviation, making it an attractive economic option for delivering time-sensitive and high-value cargo.

Heavy lift UAV applications are especially relevant in offshore oil platforms and wind farms for delivery of oil & gas supplies, disaster relief missions to deliver emergency supplies to remote locations, medical logistics for transporting organs and critical medications, and the mining & construction site resupply eliminating dependence on ground-based vehicle access and connecting remote manufacturing facilities to major distribution networks. Advanced Air Mobility is developed into a concept for reducing carbon emissions and bypassing the congested ground system, so too does UAV technology open opportunities to automated cargo networks.

Autonomous flight management, dynamic route optimization and predictive maintenance systems can make cargo UAV networks as efficient as traditional logistics infrastructure while ensuring flexibility and responsiveness that is not possible with fixed transportation infrastructure, thus providing a sustainable competitive edge to the early adopters in various industrial sectors.

The potential of a drone swarm of dozens to hundreds of drones working together in unison has the greatest potential for military and civilian impact of any new military or civilian drone development. Distributed intelligence networks enable individual platforms to communicate with each other with respect to their mission status, share sensor data, coordinate movement patterns, and dynamically redirect tasks among surviving units if a platform is lost or has malfunction, Swarm systems create resilient operational capabilities that are not achievable with single-vehicle systems.

Swarm applications in the military range from saturation attacks to saturate enemy air defense systems, distributed electronic warfare operations in large geographic areas, collaborative collection of intelligence using multiple sensor platforms, and autonomous force protection, where coverage is provided around high-value assets. The U.S. Department of Defense Replicator Initiative aims to deploy thousands of attritable autonomous systems is multi-billion-dollar investment into the development of swarm technology and its integration into the operational environment.

Commercial swarm applications include coordinated spraying/monitoring in agriculture, distributed sensor networks for extensive infrastructure inspection, automated inventory management in warehouses via indoor coordinated flight operations, search and rescue operations on large areas with coordinated search patterns, and entertainment applications such as drone light shows to replace traditional fireworks displays at large-scale events.

North America accounted for the largest regional market, valued at USD 15.4 billion in 2025 and is expected to maintain the momentum with a CAGR of 11.2% during 2025 to 2034 as the United States is the biggest market leader in military UAV development, procurement, and deployment globally. The region’s dominance is driven by the world's most comprehensive defense UAV programs, strategic platforms such as MQ-9 Reaper systems and RQ-4 Global Hawk systems, carrier-based MQ-25 Stingray refueling platforms, loyal wingman development programs and wide-ranging classified programs focused on threats from peer competitors in multiple domains.

The US Department of Defense Replicator program is a first for the DoD in investing in thousands of coordinated, attritable autonomous systems to outnumber a peer adversary and to provide a showcase of American's technological advances in swarm operations and AI integration. The world's leading defense contractors, such as General Atomics, Northrop Grumman, Lockheed Martin and Boeing, have continued to invest in R&D, have access to classified programs and offer full systems integration, giving them a global lead in developing and producing high-end military UAVs.

Commercial UAV leadership exemplifies the development of progressive regulatory frameworks and deployment of commercial delivery service for Beyond Visual Line of Sight (BVLOS) operations and urban air mobility in multiple states. The United States is poised as the main market for commercial UAV services scaling and technology validation, given the structured approach that the Federal Aviation Administration (FAA) has taken towards BVLOS certification, the type certification pathways for advanced air mobility vehicles, and the development of Unmanned Traffic Management (UTM) systems.

Asia Pacific is the fastest-growing region, projected to grow at a CAGR of 13.2% through 2034., with China dominating the global commercial UAV market, accounting for more than 70% of the global consumer and prosumer market, with the likes of DJI, Autel Robotics and newer market participants taking the lead. The region has well-established electronics value chains and has the capability to facilitate rapid prototyping, reduced manufacturing costs, mass production and constant innovation for UAV parts and systems.

China has the largest commercial UAV company, major defense UAV development initiatives for Wing Loong and CH series UAVs exported worldwide, and the largest agricultural UAV deployment, over 2.3 million agricultural UAVs have been registered, and there are government subsidies and training programs. The cooperation between UAV technology and Belt and Road Initiative provides China with export opportunities in developing markets and it also enables technology transfer and capability building in China.

India is a fast-growing market because of the indigenization needs of the entire defense sector, initiatives of the Government like the SVAMITVA program for rural property mapping with the use of millions of UAV sorties, the modernization of agriculture and the need for precision application technologies, and the policy of “Make in India” which has a negative impact on imported complete systems, but a positive impact on developing the indigenous industrial base. Heavy-lift agricultural applications, development of infrastructure for urban air mobility, and introduction of UAV systems into smart city projects for demographic change and infrastructure modernization needs are demonstrated in Japan and South Korea.

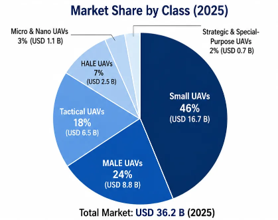

While small UAVs (under 25 kg) are the market leaders with 46% market share in 2025, the market is set to expand by 12.8% CAGR through 2034. This segment spans commercial use in real estate photography, construction mapping, farming surveillance, infrastructure auditing, and public safety. They are the first-place companies go to with UAV programs, and the volume of commercial operations is the highest worldwide due to their relatively low acquisition costs, simplified regulatory requirements, ease of deployment and the rapid advances of their sensor capabilities.

MALE UAVs accounted for approximately USD 8.8 billion in market value and are expected to remain a leading defense segment, featuring aircraft such as MQ-9 Reaper, Bayraktar TB2, and Wing Loong systems that have proven essential for prolonged intelligence, surveillance, reconnaissance, and precision strike operations. These platforms offer satellite-like coverage services for significantly less cost than space-based platforms and have the operational flexibility that space-based platforms cannot achieve.

Tactical UAVs account for 18% of the market and are primarily used for military and security applications that demand reconnaissance, target designation and battle damage assessment at brigade and battalion levels. This segment has seen tested operational efficiency in recent engagements and is aiding to force modernization initiatives in allied countries looking to improve on their situational awareness and precision engagement capabilities.

The versatility of rotary-wing UAVs to take off and land vertically in tight spaces, precise hovering for detailed inspection and delivery, and mechanical simplicity as compared to fixed-wing alternatives, provides the market with a leading advantage, accounting for 44% of the market in 2025 at USD 15.9 billion. Commercial and consumer use is based on multi-rotor designs, and military and industrial applications are based on helicopter designs.

Fixed-Wing UAVs make up 35% of the market at USD 12.7 billion and are used for the applications that demand long distance, high altitude and long duration flights such as strategic military reconnaissance, large area agricultural surveys, pipeline inspection, and regional cargo delivery. This portion can be aerodynamically designed for much longer endurance and range than the rotary portion and can be used for special missions with performance requirements.

Hybrid VTOL UAVs represent the fastest-growing type segment at 16.8% CAGR, as they combine the vertical take-off with good forward flight features to meet the operational needs for precision landing in an enclosed space and extended range and endurance required for regional missions such as cargo delivery, infrastructure inspection, and emergency response operations.

The Military & Defense sector represents the highest application share of 48%, worth USD 17.4 billion in 2025, on account of consistent procurement of strategic reconnaissance systems, tactical solutions, precision attack technologies, and development of loyal wingmen solutions. The Military & Defense sector enjoys the advantage of well-established operational success in the form of UAVs being integrated into warfare scenarios.

Commercial applications represent the fastest-growing segment with a CAGR of 14.6%, reaching USD 13.2 billion in 2025, as there will be an increase in deployment for precision agriculture applications, infrastructure inspection, logistics deliveries, and emergency coordination. The development of the regulatory structure that allows for Beyond Visual Line of Sight operations and urban air mobility is aiding commercial growth.

The global UAV industry exhibits distinct competitive dynamics within the defense and commercial sectors where the defense sector is highly concentrated with incumbent prime contractors with security clearance, integration skills, and government relations while the commercial sector is fragmented and competition arises through technology and production.

Market leadership in defense continues to be dominated by large aerospace contractors such as General Atomics, Northrop Grumman, Lockheed Martin, and Boeing, which hold about 65% share of total military procurement dollars by virtue of their complete range of solutions in strategic platforms, tactical systems, and R&D programs. Such contractors have competitive strengths derived from classified access, robust R&D spend, superior systems integration expertise, and customer connections in the defense space.

Competition in the commercial marketplace is defined by the market dominance of Chinese company DJI, which holds 70% of the consumer and prosumer market through its competitive advantages of manufacturing capability, innovation, and ecosystem formation, which includes both hardware and software. Competitors in the West such as Skydio, Autel Robotics, Parrot, and new entrants to the industry compete through enterprise-oriented products, security orientation in response to demands from governments and critical infrastructure providers, and advanced autonomy systems.

May 2026: General Atomics Aeronautical Systems has been awarded USD 2.1 billion worth of multi-year deal for MQ-9B SkyGuardian production for the USAF and its international partners’ procurement programs featuring improved artificial intelligence, upgraded electronic warfare capabilities, and advanced weaponizing capabilities.

April 2026: Skydio has concluded a USD 230 million Series E financing that will allow the company to continue developing its autonomous enterprise solutions and increasing its manufacturing capabilities to meet the increasing demand for compliant commercial systems.

March 2026: The Northrop Grumman B-21 Raider aircraft teamed up with loyal wingmen during classified testing, achieving autonomous teaming between the two UAVs, thereby demonstrating next-generation warfare techniques involving both manned and unmanned aircraft for air penetration missions.

February 2026: AeroVironment bagged a USD 1.3 billion deal to develop next-generation loitering munitions with advanced AI-based target identification, enhanced range, and network capabilities for carrying out coordinated swarming operations.

January 2026: DJI introduced a security system for enterprise use which met the needs of government agencies and critical infrastructures with security systems, encryption technology, and supply chain visibility.

November 2025: Textron Systems demonstrated its success in autonomous delivery of goods using heavy-lift unmanned aerial vehicles, delivering 200 kilograms in cargo within a distance of 150 kilometers.

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

30 Jun 2026

Intellectual Market Insights Research © 2026. All rights reserved.