Share this link via:

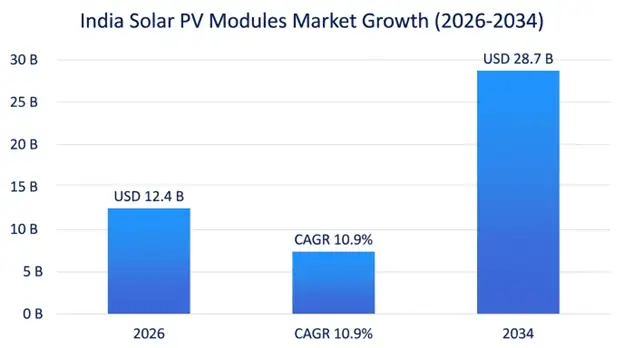

The India solar photovoltaic modules market was valued at USD 10.9 billion in 2025 and is projected to reach USD 12.4 billion in 2026, expanding to USD 28.7 billion by 2034, growing at a CAGR of 10.9% during the forecast period (2026-2034). In capacity terms, India’s annual solar module demand reached approximately 38-40 GW in 2025, with projections indicating growth to 70-75 GW annually by 2034, driven by the country’s ambitious target of achieving 500 GW of non-fossil fuel capacity by 2030.

Solar photovoltaic panels form the key technology in the energy transition efforts being undertaken by India, which convert sunlight into direct current electricity using the photovoltaic effect and serving as the basic building blocks for utility-scale solar power plants, industrial and commercial installations, residential rooftop PVs and rural electrification programs through standalone systems. The solar power industry in India has undergone a structural transformation in the supply of panels from a completely import-dependent market to a more sustainable manufacturing sector due to proactive policies such as the PLI Scheme for manufacturing high-efficiency solar modules, ALMM guidelines requiring domestic supply in government tenders and levy of BCD.

In terms of technology innovation, the shift from traditionally used multicrystalline silicon modules to high-efficiency monocrystalline solar PVs, especially PERC modules, along with advancements in next-generation technologies such as TOPCon and heterojunction technologies, which provide module efficiency greater than 22-24%. The usage of bifacial modules has grown significantly within utility-scale applications because as they utilize reflected radiation from the ground to increase energy generation potential of up to 8-15%.

The market spans a wide range of deployment applications ranging from huge solar parks covering thousands of hectares of land in the arid desert region of Rajasthan state to distributed rrooftop installations over commercial and residential buildings in cities; floating solar projects over water bodies, lakes, and dams; and agri-voltaic projects, which integrate agriculture with solar power generation. All segments have their own distinctive technologies, procurement processes, financing structures, and performance standards that determine demand dynamics along the entire value chain of photovoltaic modules.

India’s solar capacity deployment trend has consistently exceeded official projections in terms of solar capacity addition, with installed solar capacity exceeding the 75 GW target as of March 2025 with actual installed capacity of 84 GW, highlighting the inherent economic feasibility of solar generation in India, where ample solar insolation of 5.0 – 5.5 kWh per square meter on a daily basis allows the levelized cost of electricity for utility-scale solar generation to be as low as INR 2.0 -2.5 per kWh, far lower than conventional coal-based thermal power generation costs.

| Report Coverage | Details |

|---|---|

| Base Year | 2025 |

| Base Year Value | USD 10.9 Billion |

| Forecast Value | USD 28.7 Billion |

| CAGR | 10.9% |

| Forecast Period | 2026-2034 |

| Historical Data | 2022-2025 |

| Largest Market | West India |

| Fastest Growing Market | North India |

| Segments Covered | By Product Type, Technology, Application, End-User, Installation Type, Region |

| Region Covered | North India, South India, West India, East & Northeast India |

| Key Market Playes | Waaree Energies, Adani Solar, Vikram Solar, Tata Power Solar, Premier Energies, Goldi Solar |

Get more details on this report - Request Free Sample

The primary driver behind the growth. of India’s solar photovoltaic module market is the overall set of policies that are geared towards reaching 500 gigawatts of non-fossil power generation capacity by 2030, with solar energy expected to contribute around 280 gigawatts toward this target. The introduction of the Production Linked Incentives Scheme, with an investment of INR 24,000 crore, has significantly transformed the economics of local manufacturing by introducing financial support for production of efficient modules which include new and innovative designs like HJT and TOPCon which generate higher revenues.

Through the Approved List of Models and Manufacturers approach, an exclusive domestic market is provided through limited procurement processes using only domestically produced modules that meet strict efficiency and quality standards, thus ensuring guaranteed demand for domestic manufacturers as they increase their manufacturing capacity. Additionally, through tariffs in the form of Basic Customs Duties of 40% for imported modules and 25% for imported cells, domestic manufacturers are assured that they have adequate protection against foreign manufacturers who produce at reduced costs.

Purchase obligations at the state level ensure that distribution utilities are required to obtain specific percentages of their energy requirements from renewable sources, thus ensuring continuous demand for solar energy projects and associated module purchases. Net metering provisions in key states ensure that solar projects are profitable to both households and businesses.

Key Performance Metrics:

The sustained decline in solar photovoltaic module prices has changed solar electricity from a subsidized technology into one of the cheapest sources of electricity generation in most of India's electricity markets. The average price of photovoltaic modules fell from USD 0.38 per watt peak in 2020 to USD 0.18-0.22 per watt peak for imported modules in 2025, while domestic manufacturing prices ranged between USD 0.24-0.28 per watt peak, considering higher costs of manufacturing but reduced by import duty advantage.

Electricity consumers in the C&I sector are facing grid prices of INR 7.5-12.0 per unit in key states, whereas power purchase agreements with solar projects are signed at INR 3.0-4.5 per unit, allowing the customers cost savings on electricity usage of up to 50-65%, translating into payback periods of 3-5 years for rooftop solutions and 6-8 years for open access cases.

Residential is positively impacted by lower costs as well as greater access to finance, with average payback periods on residential solar systems reducing from between 8 and 10 years during 2018 to between 4 and 6 years in 2025 under favorable net metering policies, thus making it financially viable for middle-class households.

Cost Reduction Impact Metrics:

Although there have been many developments in the capacity building for modules, the Indian solar PV manufacturing value chain is still incomplete due to significant import dependence on critical upstream materials such as solar-grade polysilicon, silicon ingot and wafer, and high-efficiency solar cells, of which 80-85% of global production capacity belongs to Chinese firms. The dependency on imported upstream materials poses challenges of cost unpredictability and supply risk that hinder Indian companies from competing with vertically integrated Chinese companies which benefit from economies of scale and low input costs.

Price fluctuation of polysilicon between USD 6-38/kg over 2020-2023 introduces significant unpredictability in the upstream material cost of domestic cell manufacturers who aim to form long-term contracts and financing projects with stable cost structures. The imposition of the Basic Customs Duty (BCD), which protects Indian domestic module makers, also increases the cost of project development for Indian companies that use imported cells in their domestic module assembly process.

Supply Chain Impact Metrics:

The PM Surya Ghar Muft Bijli Yojana program, introduced at an investment of INR 78,000 crore for the installation of rooftop solar systems across 10 million households, is the largest residential solar market opportunity in the history of renewable energy in India. This program grants a subsidy of INR 30,000 per kW system, INR 60,000 for 2 kW systems, and INR 78,000 for 3 kW systems, making investment costs economically feasible to allow households of middle and lower-middle classes that could not afford such systems earlier.

The residential market offers favorable traits for local module producers, including smaller module sizes, importance placed upon visual appearance and warranty, and relative indifference toward price as compared with utility projects where thin margins are achieved. Distribution via the installer channel, consumer electronic stores, and financial institutions presents avenues for accessing markets outside traditional project developer channels.

Residential Opportunity Metrics:

The extensive water infrastructure existing in India consisting of irrigation reservoirs, hydro-reservoirs, and industrial water bodies offers vast untapped potential for floating solar power plant installations, which can overcome the problem of availability of limited land area while taking advantage of performance improvements of 5-10% resulting from cooling over comparable ground-mounted systems.

According to the estimates of the National Institute of Solar Energy, India’s floating solar potential is about 280 GW, but currently India has only around 500 MW of installed capacity. Agrivoltaics enables agriculture and solar power generation to occur on the same piece of land, using raised module mounting structures, thereby resolving inherent conflicts between preserving agricultural lands and renewable energy sources.

Pilot studies have shown that farming beneath solar panels can continue at 60-80 percent agricultural yields while stable revenues from electricity generation significantly improve farmers’ income security.

The Indian solar module market is witnessing an accelerated technological shift from standard PERC cell structures towards passivated contact technology, particularly tunnel oxide passivated contact (TOPCon) technology that offers module efficiencies between 22%-24% against conventional PERC technology that gives efficiencies in the range of 20%-21.5%. The domestic companies such as Waaree Energies, Vikram Solar, and Adani Solar have made considerable investments in manufacturing TOPCon technology modules with expected domestic production capacities of 15-20GW by 2026.

Higher-efficiency modules command premium prices of USD 0.03-0.06 per watt over conventional PERC modules while offering significant benefits in space-constrained areas and rooftop modules due to restrictions on the space available for the installation of systems. The utility-scale project developers prefer to use modules with advanced technology to leverage land and infrastructure costs during competitive bidding.

Technology Transition Metrics:

Agrivoltaics is a novel approach that combines agriculture with the generation of electricity using the solar power system through raised platforms that allow for the growth of crops, grazing of livestock, and other forms of horticulture activities below and among the solar panels. This helps solve major issues arising from the struggle between agricultural land conservation and renewable energy installation in land-limited areas.

TThe PM-KUSUM scheme provides a policy framework that supports agrivoltaic development via feeder-level solar installations, plus individual farmer pump solarization, and the buildup of small solar power plants right on agricultural land. For agrivoltaic uses the module specifications are kind of specific require elevated mounting heights in the range of 2.5-4.0 meters, and then bifacial designs that take advantage of ground-reflected radiation, and wider row spacing to allow farm machinery to operate efficiently, which ends up creating different product requirements.

The West India region, consisting of Gujarat, Rajasthan, and Maharashtra, holds the largest regional market share of 35% in the module demands in 2025. The primary reasons for the huge market presence include the availability of solar energy resources in Gujarat, its extensive solar energy policy and framework, and availability of several manufacturing units in the region.

Rajasthan is currently the most prominent utility-scale solar project developer in the country, housing around 18 GW of commissioned solar capacity with over 45 GW in various stages of the development pipeline. It enjoys ample availability of land, high solar irradiance above 5.5 kWh per sq m/day, and improvements in the transmission network from solar rich areas to the consumption center.

Solar power adoption has increased among large industries in Maharashtra, which seek open access of solar energy due to their cost-effectiveness and sustainability policies.

South India holds a 28% regional market share, which is led by Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana that exhibit advanced commercial and industrial solar energy markets, capabilities in developing large utility-scale projects, and pioneering initiatives in floating solar and green hydrogen utilization. These states have good solar power potential, an already developed transmission network, and supportive state electricity regulatory regimes to enable competitive discovery of tariff rates.

Karnataka and Tamil Nadu are leading in terms of the uptake of commercial and industrial solar rooftops due to high industrial tariffs, progressive net metering laws, and presence of companies from the tech industry committed to their environmental sustainability efforts. The southern part of India is establishing itself as a preferred destination for setting up green hydrogen manufacturing plants that require solar power generation.

The North region, including Uttar Pradesh, Punjab, Haryana, and Himachal Pradesh, shows the highest growth rate of 12.8% CAGR till 2034 due to PM Surya Ghar Residential Solar installation, PM KUSUM Solar project for agriculture purposes, and the large population providing good market opportunity for distributed solar. The agricultural solar segment in Punjab and Haryana shows robust growth in its market through solar pumps and feeders installation decreasing electricity subsidy expenses of the state while providing extra income opportunities for farmers.

Uttar Pradesh’s large population and improving infrastructure make this state a huge consumer for rooftop solar projects, which would increase once the grid becomes more reliable and consumers become aware of solar energy economics.

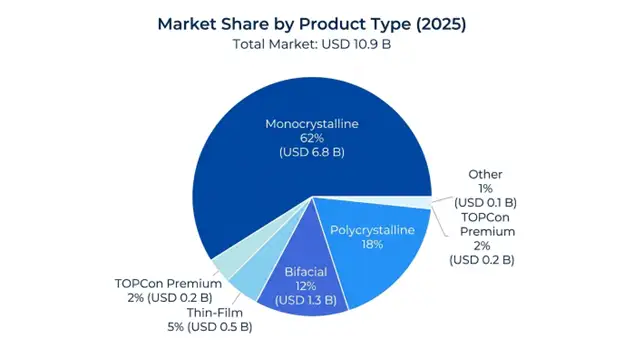

The monocrystalline module segment dominates the market, capturing a market share of 62% that is valued at USD 6.8 billion in 2025, recording an 11.4% CAGR through 2034 owing to the prevalence of the high-efficiency single-crystal silicon system. The segment enjoys several advantages including enhanced energy generation rates during high temperatures, improved generation performance during the monsoon season, and declining price differences with its polycrystalline counterparts.

Bifacial modules are the most rapidly expanding category, with an average annual growth rate of 16.8% till 2034, growing from USD 1.3 billion in 2025, owing to the growing inclination of utility-scale players toward specifying bifacial configurations that leverage reflected sunlight from the ground to boost output by 8-15%, without adding to their capex.

Market share of PERC technology stands at 54% valued at USD 5.9 billion in 2025, which is the mainstream technology with existing capacity, competitive prices, and substantial operational experience. TOPCon technology accounts for 28% of the market and is projected to grow at an 18.2% CAGR through 2034, making it the fastest-growing segment owing to its growth in local production capacities and efficiency benefits despite lower pricing.

Utility-scale applications account for a 58% market share with revenue of USD 6.3 billion in 2025, as India’s development approach relies on generating power from large-scale and centralized sources via bidding processes. The commercial and industrial end-use segment captures 26% market share with revenue of USD 2.8 billion during 2025-2034 at a growth rate of 13.1% CAGR.

Independent Power Producers, accounting for 45% market share worth USD 4.9 billion in 2025, which includes renewable energy companies purchasing photovoltaic panels for large-scale utility projects via power purchase agreements. Government organizations account for 22% of the market share, including central and state government entities at both the center level and state level that generate solar power and use captive power plants to lower energy expenses.

The India solar photovoltaic modules market is witnessing steady growth, where with domestic manufacturers gaining a competitive advantage. In fact, the top six local players are estimated to control around 65% of domestically manufactured supply, helped by policy protection, better technology and just generally expanding manufacturing scale. Waaree Energies, Adani Solar, and Vikram Solar show up as the three biggest manufacturers when you look at both capacity and revenue. They also have integrated cell manufacturing, which provides more stable structural cost advantages compared with module assemblers that still rely on imported cells, and such reliance can affect pricing stability.

Competitive differentiation tends to revolve around manufacturing scale for cost competitiveness, plus a wider technology portfolio that covers multiple cell architectures. There’s also financial strength, which supports performance guarantees, and distribution network development aimed at rooftop markets. Beyond that, export capability matters too, since it brings revenue beyond purely domestic procurement mandates.

March 2026: Waaree Energies launched operations at its 5 GW TOPCon cell production facility of its 5 GW TOPCon cell line in Gujarat, thereby creating one of India’s largest integrated manufacturing capacities with an efficiency rate of 23.1% for top-end bifacial modules.

February 2026: The Ministry of New and Renewable Energy revised ALMM norms by setting higher standards for efficiency for monocrystalline modules at 21.5%, thereby accelerating the technology transition.

January 2026: Adani Solar commenced operations at the country’s first ever utility-scale polysilicon plant with an annual production capacity of 3,500 metric tons per year.

December 2025: Vikram Solar signed a US $400 million contract for supplying 1.8 GW of TOPCon modules to the USA, affirming India’s position as a reliable alternative supplier destination for international customers.

November 2025: Solar Energy Corporation of India launched a 10 GW agrivoltaics tender under the second phase of PM-KUSUM project, thereby opening a separate procurement path for specialized raised-mount and bifacial modules.

List of Key Players in India Solar Photovoltaic Modules Market

India Solar Photovoltaic Modules Market Segments

By Product Type:

By Technology:

By Application:

By End-User:

By Installation Type:

By Region:

You'll get the sample you asked for by email. Remember to check your spam folder as well. If you have any further questions or require additional assistance, feel free to let us know via-

+1 724 648 0810 +91 976 407 9503 sales@intellectualmarketinsights.com

19 May 2026

Intellectual Market Insights Research © 2026. All rights reserved.